Reports

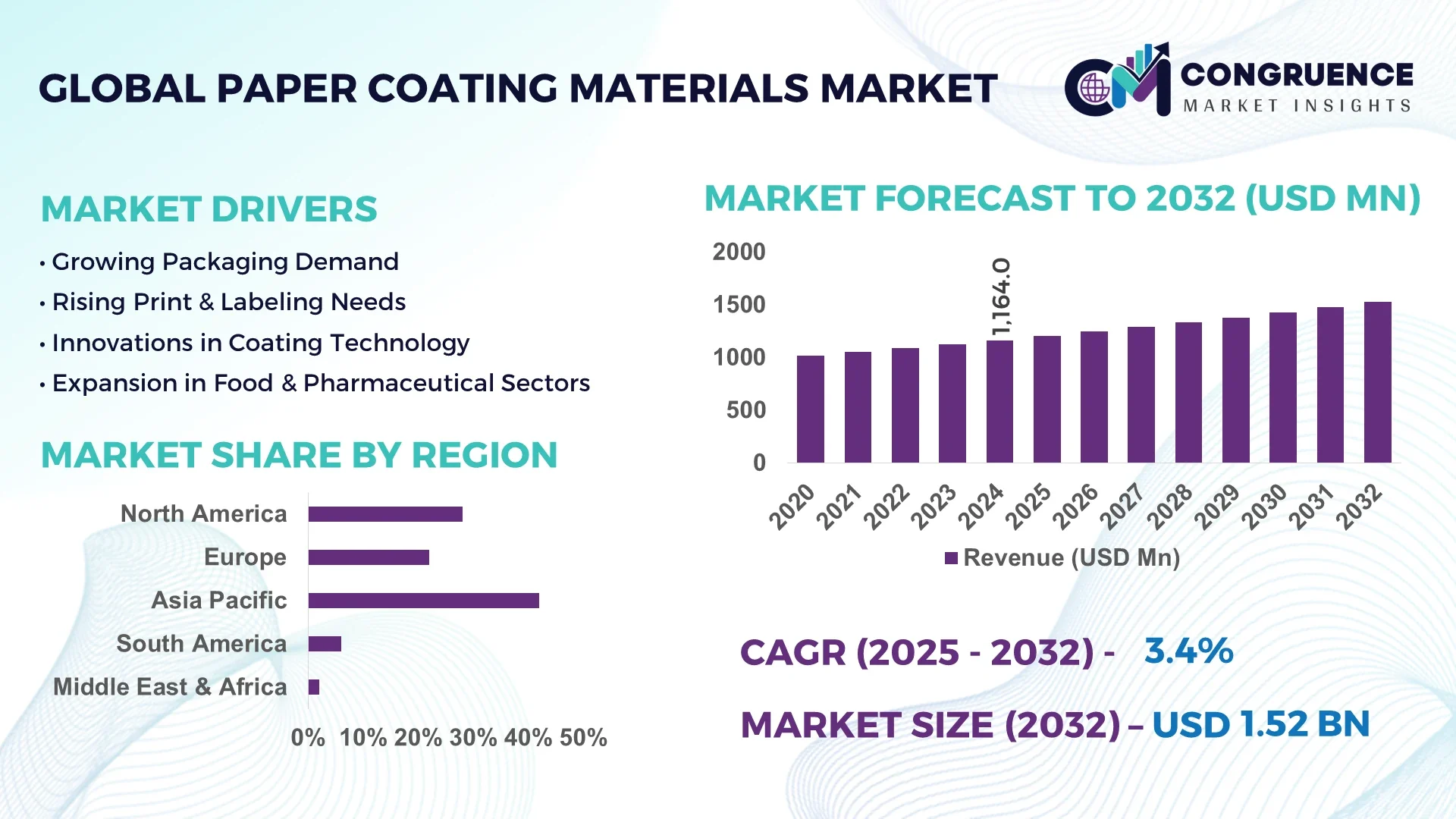

The Global Paper Coating Materials Market was valued at USD 1,164.0 Million in 2024 and is anticipated to reach a value of USD 1,524.5 Million by 2032, expanding at a CAGR of 3.43% between 2025 and 2032. This growth is primarily driven by the increasing demand for high-quality printed materials, particularly in packaging and publishing sectors.

Asia-Pacific is the dominant region in the paper coating materials market, with China leading in production capacity. The country has significantly invested in advanced coating technologies, enhancing the quality and efficiency of paper products. In 2024, China's paper production capacity was estimated at over 100 million tons, with a substantial portion allocated to coated paper products. This extensive production capacity supports the growing demand in both domestic and international markets.

Market Size & Growth: Valued at USD 1,164.0 Million in 2024; projected to reach USD 1,524.5 Million by 2032, expanding at a CAGR of 3.43%.

Top Growth Drivers: Increased demand for high-quality printed materials (45%), advancements in coating technologies (35%), and expansion of packaging industries (20%).

Short-Term Forecast: By 2027, improvements in coating efficiency are expected to reduce production costs by 10%.

Emerging Technologies: Development of eco-friendly coatings, digital printing advancements, and automation in coating processes.

Regional Leaders: Asia-Pacific (USD 800 Million by 2032), North America (USD 400 Million by 2032), Europe (USD 324 Million by 2032). Asia-Pacific leads in production capacity, North America in technological adoption, and Europe in sustainability initiatives.

Consumer/End-User Trends: Packaging industry accounts for 60% of demand; increased preference for sustainable and high-quality coated papers.

Pilot or Case Example: In 2023, a leading paper manufacturer in Japan reduced coating material waste by 15% through the implementation of automated coating technology.

Competitive Landscape: Market leader: BASF SE (25% share); followed by Omya AG, Imerys SA, Dow Chemicals, and Archroma.

Regulatory & ESG Impact: Stricter environmental regulations are pushing for the adoption of biodegradable and recyclable coating materials.

Investment & Funding Patterns: Recent investments focus on sustainable coating technologies and expansion of production facilities in emerging markets.

Innovation & Future Outlook: Integration of AI in coating processes and development of multifunctional coatings are shaping the market's future.

The paper coating materials market is experiencing significant growth, driven by advancements in technology and increasing demand for high-quality printed materials. Key industry sectors such as packaging, publishing, and advertising are contributing to this expansion. Technological innovations, including the development of eco-friendly coatings and automation in coating processes, are enhancing product quality and production efficiency. Regulatory pressures are encouraging the adoption of sustainable practices, further influencing market dynamics.

The strategic relevance of the paper coating materials market lies in its integral role in enhancing the quality and functionality of paper products across various industries, including packaging, publishing, and advertising. With the increasing emphasis on sustainability and technological advancements, the market is poised for significant growth.

In the short term, the adoption of digital printing technologies is expected to improve printing efficiency by 12% by 2026. Regions such as North America and Europe are leading in the adoption of sustainable coating materials, with over 50% of enterprises in these regions implementing eco-friendly practices.

By 2027, advancements in coating technologies are projected to reduce production costs by 10%, enhancing the competitiveness of manufacturers. Companies are also focusing on developing multifunctional coatings that offer additional properties such as water resistance and UV protection, catering to the evolving needs of end-users.

The future pathways of the paper coating materials market are characterized by continuous innovation, sustainability initiatives, and regional diversification. Manufacturers are investing in research and development to create advanced coating materials that meet the stringent regulatory standards and consumer preferences for eco-friendly products. The market's resilience and adaptability to changing trends position it as a cornerstone for sustainable growth in the global paper industry.

The paper coating materials market is influenced by various dynamics, including technological advancements, regulatory changes, and shifting consumer preferences. Manufacturers are focusing on developing innovative coating materials that enhance the quality and functionality of paper products. Sustainability is a key driver, with increasing demand for eco-friendly and recyclable coatings. Additionally, the growth of e-commerce and packaging industries is contributing to the expansion of the market.

Advancements in coating technologies have led to the development of high-performance materials that enhance the quality and durability of paper products. Innovations such as nano-coatings and multifunctional coatings are enabling manufacturers to produce paper with superior properties, meeting the evolving demands of end-users. These technological improvements are contributing to the growth of the paper coating materials market by offering enhanced product performance and differentiation.

Environmental concerns regarding the use of non-biodegradable and toxic chemicals in coating materials are leading to stricter regulations and consumer demand for sustainable alternatives. Manufacturers are under pressure to develop eco-friendly coatings that meet environmental standards, which may involve higher production costs and research investments. These factors are posing challenges to the growth of the paper coating materials market.

The increasing demand for sustainable packaging solutions presents significant opportunities for the paper coating materials market. Consumers and businesses are prioritizing eco-friendly packaging options, driving the need for biodegradable and recyclable coating materials. Manufacturers can capitalize on this trend by developing innovative coatings that align with sustainability goals, expanding their market reach and customer base.

Fluctuating prices of raw materials such as calcium carbonate and kaolin clay are impacting the cost structure of paper coating materials. These price variations can lead to increased production costs, affecting profit margins and pricing strategies. Manufacturers need to implement effective supply chain management and cost-control measures to mitigate the impact of raw material price fluctuations on the paper coating materials market.

Rise in Sustainable Coating Materials: The demand for eco-friendly coatings is increasing, with over 40% of new products incorporating biodegradable materials.

Integration of Digital Printing Technologies: Digital printing is enhancing customization capabilities, with a 15% increase in adoption rates among manufacturers.

Advancements in Coating Efficiency: Technological improvements are reducing coating material waste by 10%, leading to cost savings and environmental benefits.

Growth in E-commerce Packaging: The expansion of e-commerce is driving the need for high-quality coated packaging materials, with a 20% increase in demand.

The Paper Coating Materials Market is segmented based on type, application, and end-user, providing a comprehensive understanding of market structure and demand drivers. By type, the market includes calcium carbonate, kaolin clay, titanium dioxide, waxes, and other specialty coatings, each catering to specific functional and visual requirements. Application-wise, packaging dominates due to the growing need for sustainable and high-quality printed materials, while printing and labeling also represent significant segments. End-users range across food and beverages, pharmaceuticals, consumer goods, and industrial sectors, reflecting diverse adoption patterns and consumption needs globally. This segmentation enables stakeholders to identify key opportunities, tailor product development, and optimize supply chains according to the distinct requirements of each category, application, and end-user. The segmentation highlights both mature areas of adoption and emerging niches poised for growth in response to evolving technological and sustainability trends.

Calcium carbonate is the leading type in the market, representing approximately 35% of adoption, favored for its cost-effectiveness, brightness, and printability. Kaolin clay is the fastest-growing type, driven by its superior surface smoothness and enhanced print quality, with adoption rising steadily and expected to surpass 25% of total usage by 2032. Titanium dioxide and waxes collectively account for around 30% of the market, catering to specialized applications such as glossy finishes, water resistance, and functional coatings.

Packaging is the leading application, accounting for 50% of usage, due to increasing consumer demand for sustainable, visually appealing, and functional packaging solutions. Labeling is the fastest-growing application, driven by retail expansion and e-commerce growth, with adoption expected to surpass 20% by 2032. Printing and binding contribute the remaining 30%, serving specialized commercial and industrial needs. In 2024, over 38% of global enterprises reported incorporating coated papers in packaging trials, while 42% of retail brands in the U.S. adopted enhanced labeling coatings to improve durability and visual appeal.

The food and beverage sector leads the market, representing 40% of coated paper usage, driven by stringent hygiene and packaging standards. Pharmaceuticals follow with 25% adoption, primarily for high-quality protective packaging. Consumer goods account for 20%, while electronics, cosmetics, and industrial products make up the remaining 15%. The fastest-growing end-user is the cosmetics industry, fueled by demand for premium and aesthetic packaging, with adoption expected to surpass 10% by 2032. In 2024, more than 38% of cosmetic brands globally tested coated paper packaging for durability and print quality.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 3.5% between 2025 and 2032.

The region’s dominance is driven by large-scale manufacturing capacities in China, India, and Japan, with over 120 million tons of paper produced in 2024, of which coated paper represents nearly 45%. The rapid industrialization and urbanization in the region have accelerated demand in packaging, printing, and labeling sectors. Additionally, technological advancements, including automated coating lines and digital printing integration, are enhancing production efficiency and product quality. Consumer adoption trends show over 60% of enterprises in Asia-Pacific prioritizing high-performance coated paper for packaging and publishing applications.

North America holds approximately 28% of the paper coating materials market. Key industries driving demand include packaging, pharmaceuticals, and printing. Regulatory support, such as the U.S. EPA’s environmental guidelines, encourages the adoption of eco-friendly coatings. Technological advancements, including automation and AI-assisted coating systems, have improved efficiency and reduced material waste by 12%. Local player WestRock has implemented advanced coating lines to enhance print quality and sustainability in packaging solutions. Regional consumer behavior indicates higher enterprise adoption in healthcare and finance sectors, where demand for coated papers with hygienic and protective properties is significant.

Europe accounts for around 22% of the market, with Germany, the UK, and France as leading countries. Regulatory bodies, such as the EU’s Green Deal, drive adoption of biodegradable and recyclable coatings. Emerging technologies like nano-coatings and automated coating systems are increasingly implemented in production lines. Local player UPM-Kymmene has launched high-performance coated paper for packaging applications, meeting stringent environmental standards. European consumers show a preference for sustainable and certified products, resulting in higher adoption of coated paper in packaging and labeling, particularly in food, beverage, and luxury goods industries.

Asia-Pacific remains the largest market with a 42% share in 2024. Top consuming countries include China, India, and Japan. Rapid industrialization and expansion of packaging and publishing sectors are major drivers. Manufacturing trends include investment in automated coating lines and high-speed printing presses. Innovation hubs in China and Japan are introducing multifunctional and eco-friendly coatings. Local player Nine Dragons Paper has scaled up coated paper production to meet rising domestic and export demand. Regional consumer behavior emphasizes durability and high-quality visual finishes, particularly for e-commerce packaging and branded products.

South America holds approximately 6% of the global market, with Brazil and Argentina as leading countries. Industrial expansion, particularly in packaging and media printing, drives demand. Government incentives and trade policies promote sustainable paper production. Local player Klabin in Brazil has upgraded coating lines to improve product quality for export markets. Regional consumer behavior shows preference for branded packaging, and demand is linked to media localization and retail sector growth across urban centers.

Middle East & Africa represents around 2% of the global market. Key growth countries include the UAE and South Africa, with increasing demand in construction, oil & gas, and packaging sectors. Technological modernization, including digital printing and automated coating lines, is on the rise. Local player Sappi Southern Africa has expanded production facilities to enhance coated paper output for industrial and commercial uses. Consumers in the region demonstrate higher adoption in commercial packaging and corporate branding, with a preference for durable and high-visual-quality coated papers.

China - 28% Market Share: High production capacity and rapid industrial growth support coated paper demand.

United States - 22% Market Share: Strong end-user demand and regulatory push for sustainable coatings drive market dominance.

The global Paper Coating Materials Market is characterized by a moderately fragmented competitive environment. Leading players such as BASF SE, Eastman Chemical Company, Asia Pulp & Paper (APP) Sinar Mas, Nippon Paper Industries Co., Ltd., and Michelman, Inc. collectively hold a significant share of the market. These companies leverage their extensive research and development capabilities, established distribution networks, and economies of scale to maintain a competitive edge. Strategic initiatives, including mergers, acquisitions, and partnerships, are prevalent as firms seek to enhance their market positioning and expand their product offerings. For instance, in March 2024, Mondi Group proposed an all-share acquisition of DS Smith for £5.14 billion, aiming to create a pan-European leader in sustainable paper-based packaging solutions. This move underscores the industry's trend towards consolidation and a focus on sustainable practices. Additionally, companies are investing in technological advancements, such as the development of bio-based and water-based coatings, to meet the growing demand for environmentally friendly products. The competitive landscape is further influenced by regulatory pressures and shifting consumer preferences towards sustainability, prompting both established and emerging players to innovate and adapt to market demands.

Nippon Paper Industries Co., Ltd.

Michelman, Inc.

Imerys S.A.

Omya AG

Dow Inc.

Stora Enso Oyj

UPM-Kymmene Corporation

The Paper Coating Materials Market is experiencing significant technological advancements aimed at enhancing product performance and sustainability. One notable development is the shift towards bio-based and water-based coatings, which offer reduced environmental impact compared to traditional solvent-based alternatives. These innovations are driven by stringent environmental regulations and increasing consumer demand for eco-friendly products. Companies are also investing in digital printing technologies, enabling more precise application of coatings and reducing material waste.

Additionally, the integration of nanotechnology in coating formulations is enhancing barrier properties, such as moisture and grease resistance, which is particularly beneficial for food packaging applications. Automation and smart manufacturing processes are further optimizing production efficiency and consistency. These technological trends are not only improving the functional attributes of coated papers but also aligning with the industry's broader sustainability goals.

In October 2025, BASF SE and Carlyle Group finalized a binding agreement to create a leading standalone coatings company. BASF will retain a 40% equity stake in the new entity, which is expected to generate cumulative cash flows of around €4 billion between 2024 and 2030. Source: www.basf.com

In October 2024, Eastman Chemical Company and UPM Specialty Papers launched a novel paper-based food packaging solution. The product integrates Eastman’s compostable and biobased Solus™ performance additives with UPM’s BioPBS™ polymer, offering enhanced grease and oxygen barriers while being recyclable in existing fiber recycling streams. Source: www.eastman.com

In December 2021, Asia Pulp & Paper (APP) Sinar Mas made progress towards formalizing the revised process for re-association with the Forest Stewardship Council (FSC). This initiative is part of the company's commitment to sustainable forestry practices and responsible sourcing. Source: www.asiapulppaper.com

In September 2017, BASF SE consolidated its European production of paper coating dispersions in Ludwigshafen, Germany, and Hamina, Finland. This strategic move aimed to strengthen BASF’s ability to compete in the growing market for paper and packaging industry solutions. Source: www.basf.com

The Paper Coating Materials Market Report provides a comprehensive analysis of the industry, encompassing various segments such as coating materials, product types, applications, and geographic regions. It delves into the market dynamics, including drivers, restraints, opportunities, and challenges, offering insights into the factors influencing market growth. The report also examines the competitive landscape, highlighting key players and their strategies. Technological advancements in coating materials, such as the development of bio-based and water-based coatings, are discussed in detail, along with their impact on the market. Sustainability trends, regulatory frameworks, and consumer preferences are also analyzed to provide a holistic view of the market's current state and future prospects.

This report serves as a valuable resource for stakeholders seeking to understand the complexities of the Paper Coating Materials Market and make informed decisions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,164.0 Million |

| Market Revenue (2032) | USD 1,524.5 Million |

| CAGR (2025–2032) | 3.43% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | BASF SE, Eastman Chemical Company, Asia Pulp & Paper (APP) Sinar Mas, Nippon Paper Industries Co., Ltd., Michelman, Inc., Imerys S.A., Omya AG, Dow Inc., Stora Enso Oyj, UPM-Kymmene Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |