Reports

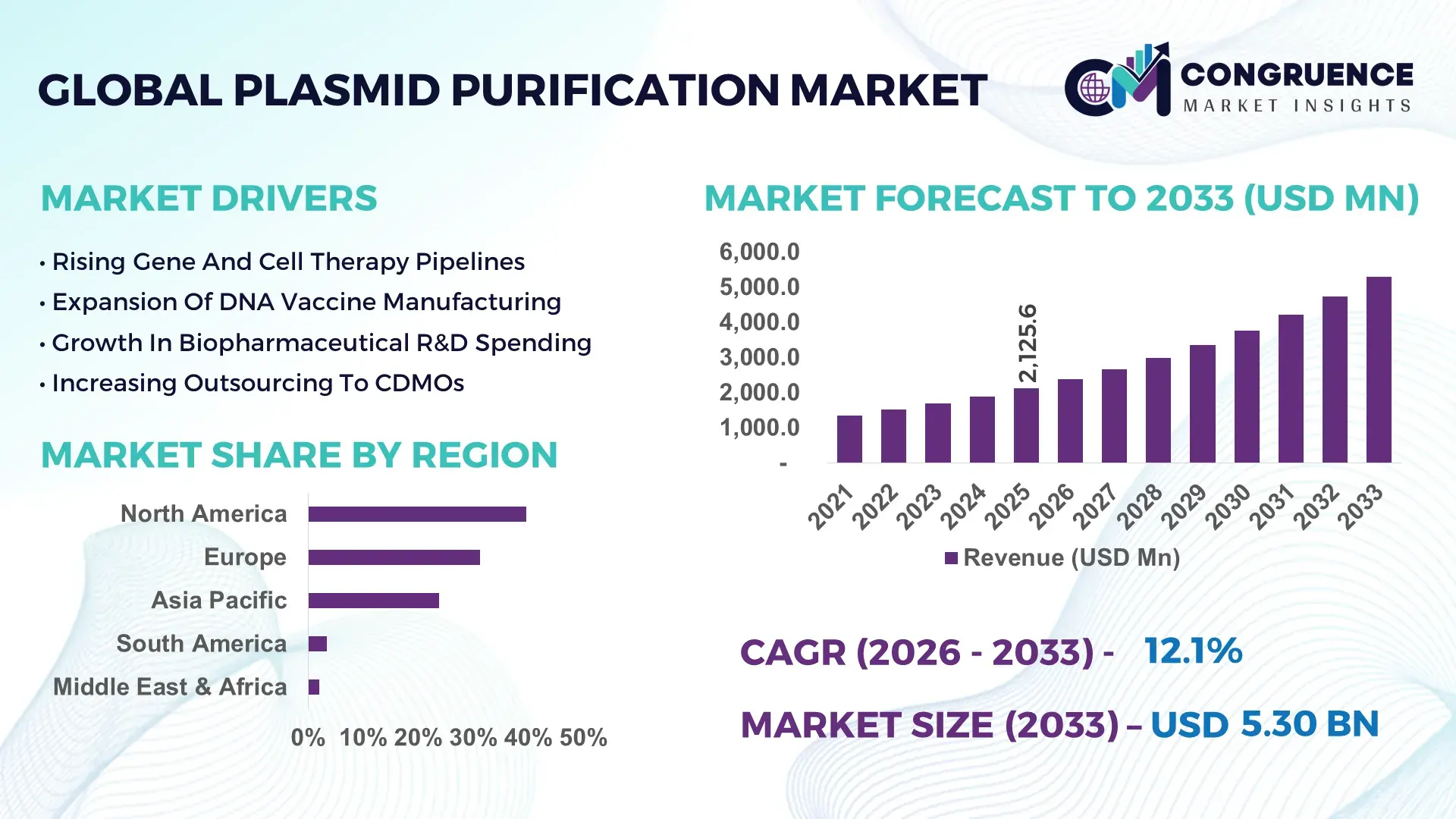

The Global Plasmid Purification Market was valued at USD 2,125.6 Million in 2025 and is anticipated to reach a value of USD 5,300.6 Million by 2033 expanding at a CAGR of 12.1% between 2026 and 2033, according to an analysis by Congruence Market Insights. This expansion is primarily driven by accelerating demand for plasmid DNA in gene therapy, mRNA vaccines, and cell-based therapeutics.

The United States leads the Plasmid Purification market through large-scale biomanufacturing capacity, sustained public and private investment, and advanced downstream processing technologies. In 2025, over 420 GMP-compliant plasmid production and purification suites were operational across the country, supporting clinical and commercial-grade output. Annual investments exceeded USD 2.6 billion across gene therapy infrastructure, viral vector manufacturing, and plasmid backbone optimization. More than 58% of plasmid purification demand originated from gene therapy and DNA vaccine development, while contract development and manufacturing organizations processed over 65% of total plasmid batches for external biotech clients. High-throughput chromatography and endotoxin-reduction technologies are widely deployed, improving plasmid yield consistency across large-scale runs.

Market Size & Growth: Valued at USD 2,125.6 million in 2025 and projected to reach USD 5,300.6 million by 2033, supported by gene therapy and DNA vaccine expansion.

Top Growth Drivers: Gene therapy pipeline growth (46%), mRNA and DNA vaccine development (41%), CDMO outsourcing (34%).

Short-Term Forecast: By 2028, automated purification platforms are expected to improve batch processing efficiency by 29%.

Emerging Technologies: Single-use chromatography systems, endotoxin-free plasmid platforms, AI-assisted process optimization.

Regional Leaders: North America projected at USD 2.1 billion by 2033 with clinical manufacturing scale; Europe at USD 1.6 billion driven by gene therapy trials; Asia-Pacific at USD 1.3 billion supported by biologics expansion.

Consumer/End-User Trends: Biotech startups and CDMOs account for over 62% of plasmid purification demand.

Pilot or Case Example: In 2024, a modular plasmid facility achieved a 24% reduction in purification cycle time.

Competitive Landscape: Thermo Fisher Scientific leads with approximately 23% share, followed by Merck, Cytiva, Qiagen, and Takara Bio.

Regulatory & ESG Impact: GMP compliance and solvent reduction mandates shaping purification workflows.

Investment & Funding Patterns: Over USD 4.1 billion invested globally between 2022–2025 in plasmid and vector manufacturing infrastructure.

Innovation & Future Outlook: Shift toward large-scale, high-purity plasmid platforms enabling next-generation gene medicines.

Plasmid purification demand is concentrated in gene therapy (44%), DNA vaccines (31%), and cell therapy research (25%). Innovations in chromatography resins, low-shear processing, and closed-system automation are improving scalability. Regulatory emphasis on purity, endotoxin control, and traceability continues to influence regional adoption and future market structure.

The Plasmid Purification Market is strategically critical to the biopharmaceutical ecosystem as plasmid DNA serves as the foundational input for viral vectors, mRNA manufacturing, and gene editing platforms. Advanced membrane-based chromatography delivers up to 37% higher plasmid recovery compared to conventional resin-packed columns, enabling faster scale-up for clinical and commercial use. North America dominates in production volume, while Europe leads in adoption with over 61% of active gene therapy developers utilizing high-purity plasmid purification systems.

By 2027, AI-enabled process analytics are expected to reduce batch failure rates by 22% through real-time impurity monitoring and yield optimization. ESG alignment is increasingly influential, with manufacturers committing to solvent reduction targets of up to 30% and single-use material recycling rates exceeding 25% by 2030. In 2024, a U.S.-based biomanufacturing cluster achieved a 19% reduction in downstream processing waste through closed-loop plasmid purification systems.

Future pathways emphasize modular GMP facilities, digital batch records, and integration with viral vector manufacturing lines. As regulatory scrutiny intensifies around plasmid integrity and trace contaminants, investment in next-generation purification platforms will remain a priority. These factors position the Plasmid Purification Market as a pillar of resilience, regulatory compliance, and sustainable growth across advanced therapeutics manufacturing.

The Plasmid Purification market dynamics are shaped by rapid expansion in gene therapy pipelines, increasing clinical trial activity, and growing reliance on outsourced biomanufacturing. Demand is driven by stringent purity requirements, scalability needs, and faster development timelines. Technological advancements in chromatography media, filtration systems, and automation enhance throughput and reproducibility. At the same time, regulatory oversight related to GMP compliance and endotoxin control raises entry barriers. Market participants focus on yield optimization, cost containment, and integration with upstream fermentation processes to remain competitive.

Gene therapy development directly accelerates plasmid purification demand, as each viral vector batch requires high-purity plasmid DNA. In 2025, over 1,900 active gene therapy programs globally relied on plasmid backbones for vector production. Advanced purification systems improved plasmid supercoiled content by up to 32%, enhancing transfection efficiency. Increased clinical trial density drives higher batch volumes and repeat manufacturing, reinforcing sustained demand.

Plasmid purification requires specialized equipment, GMP facilities, and skilled personnel, increasing operational complexity. Capital expenditure for large-scale purification suites can exceed USD 15 million per facility. Process variability and contamination risks elevate quality control costs, limiting participation by smaller manufacturers and constraining rapid capacity expansion.

DNA and mRNA vaccine platforms create significant opportunities for plasmid purification providers. Vaccine developers require rapid, scalable plasmid supply with consistent quality. In 2025, over 48% of vaccine R&D programs incorporated plasmid-based templates, supporting demand for high-throughput purification systems and single-use technologies.

Regulatory expectations for traceability, endotoxin thresholds, and documentation increase compliance burdens. Supply chain constraints for specialized resins and single-use components extended lead times by nearly 14% in recent years. These challenges complicate scaling strategies and require proactive capacity planning.

Adoption of Single-Use Purification Systems: Single-use platforms accounted for 43% of new installations, reducing cleaning validation time by 36%.

Shift Toward Modular GMP Facilities: Modular facilities improved deployment speed by 31%, enabling rapid capacity expansion.

Advanced Endotoxin Removal Technologies: New filtration methods reduced endotoxin levels by over 40% per batch.

Digital Process Monitoring Integration: Real-time analytics improved batch success rates by 27% across large-scale operations.

The Plasmid Purification market is segmented by type, application, and end-user, reflecting varied use cases across research and commercial manufacturing. Segmentation insights highlight how purity grade, scalability, and regulatory requirements influence purchasing decisions across biopharma stakeholders.

Column-based purification systems lead with 49% adoption due to reliability and scalability. However, membrane chromatography is the fastest-growing type, expanding at over 14% CAGR, driven by faster flow rates and reduced buffer consumption. Other types, including precipitation-based and hybrid systems, collectively account for 51%.

In 2025, membrane-based plasmid purification systems were deployed across large-scale facilities, supporting over 120 commercial manufacturing runs.

Gene therapy represents the leading application with a 44% share, supported by extensive clinical pipelines. DNA vaccine production is the fastest-growing application, expanding at over 15% CAGR due to accelerated development timelines. Cell therapy research and protein expression collectively account for 56%. In 2025, more than 42% of biotech firms reported scaling plasmid purification for therapeutic development.

In 2025, plasmid purification platforms enabled production of DNA templates used across more than 180 vaccine development programs.

CDMOs lead adoption with 46%, driven by outsourced manufacturing demand. Biopharmaceutical companies represent the fastest-growing end-user segment, expanding at over 13% CAGR due to in-house capacity expansion. Academic and research institutes account for 54% combined. In 2025, 39% of enterprises piloted automated plasmid purification workflows to improve efficiency.

In 2025, large CDMOs implemented advanced plasmid purification systems, reducing batch processing time by 23%.

North America accounted for the largest market share at 39.6% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.4% between 2026 and 2033.

North America processed more than 68,000 GMP-grade plasmid purification batches in 2025, supported by a dense concentration of gene therapy developers, vaccine manufacturers, and large CDMOs. Europe followed with a 31.2% share, driven by strong clinical trial activity across Germany, the UK, and France, with over 420 active gene and cell therapy programs relying on high-purity plasmid DNA. Asia-Pacific accounted for 23.8% of global demand, with China, Japan, and South Korea commissioning more than 110 new downstream bioprocessing suites in 2024–2025. South America and Middle East & Africa collectively represented 5.4%, where demand is emerging from public-sector vaccine research and regional biologics manufacturing initiatives.

How is advanced biomanufacturing infrastructure accelerating high-purity plasmid output?

The region contributed approximately 39.6% of global Plasmid Purification demand in 2025, reflecting high utilization across gene therapy, DNA vaccines, and viral vector manufacturing. Key industries driving demand include biopharmaceutical manufacturing, cell and gene therapy development, and contract development and manufacturing services. Regulatory support for advanced therapies and accelerated clinical pathways has increased GMP-grade plasmid production volumes. Technological advancements include large-scale membrane chromatography, closed-system automation, and digital batch record integration. A major domestic life sciences supplier expanded single-use plasmid purification platforms, improving batch throughput by nearly 28%. End-user behavior shows higher adoption among large biopharma companies and CDMOs, prioritizing scalability, regulatory compliance, and reproducibility over cost minimization.

Why are regulatory rigor and clinical trial density shaping purification technology choices?

Europe accounted for around 31.2% of the Plasmid Purification market in 2025, with Germany, the UK, France, and Switzerland leading demand. Regulatory bodies emphasize GMP traceability, endotoxin thresholds, and process validation, driving adoption of highly controlled purification systems. Sustainability initiatives encourage solvent reduction and disposable system optimization. Emerging technologies such as continuous chromatography and inline quality monitoring are increasingly deployed. A regional bioprocessing equipment provider introduced low-shear purification workflows, reducing plasmid degradation rates by 21%. Consumer behavior reflects strong preference for compliant, auditable, and explainable purification processes aligned with regulatory expectations.

What is driving rapid capacity expansion and regional self-sufficiency in plasmid supply?

Asia-Pacific ranked as the fastest-growing region by capacity additions in 2025, with China, Japan, and South Korea accounting for over 70% of new installations. The region commissioned more than 110 new plasmid purification suites, supporting vaccine research and gene therapy pipelines. Manufacturing trends include localization of chromatography media production and adoption of modular GMP facilities. Innovation hubs focus on high-yield fermentation and integrated downstream processing. A leading regional CDMO expanded plasmid purification capacity by 40%, enabling large-scale support for viral vector manufacturing. End-user behavior is driven by government-backed research programs and increasing reliance on domestic supply chains.

How are public health initiatives shaping early-stage demand for plasmid technologies?

South America represented approximately 3.4% of global Plasmid Purification demand in 2025, led by Brazil and Argentina. Demand is primarily supported by public vaccine institutes, academic research centers, and emerging biologics manufacturers. Infrastructure investments in biosafety laboratories and downstream processing facilities are improving regional capabilities. Government incentives for domestic biopharmaceutical production support gradual market expansion. A regional research institute upgraded plasmid purification systems to support DNA vaccine development programs. End-user behavior is closely tied to public funding cycles and regional health priorities.

Why are healthcare modernization programs driving selective adoption of advanced purification systems?

The region accounted for nearly 2.0% of global demand in 2025, with growth concentrated in the UAE, Saudi Arabia, and South Africa. Demand trends are linked to healthcare infrastructure expansion, biologics localization strategies, and national research initiatives. Technological modernization includes adoption of compact, modular purification units suitable for emerging facilities. Trade partnerships facilitate access to advanced consumables and equipment. A regional life sciences distributor supported deployment of GMP-grade plasmid purification systems across new biologics hubs. End-user behavior emphasizes reliability, technology transfer readiness, and long-term scalability.

United States Plasmid Purification Market – 34.2%: Extensive GMP manufacturing capacity and strong gene therapy and vaccine development pipelines.

Germany Plasmid Purification Market – 12.6%: High clinical trial density and stringent regulatory frameworks supporting advanced bioprocessing adoption.

The Plasmid Purification market is moderately consolidated, with approximately 45–50 active global and regional competitors supplying kits, instruments, consumables, and integrated solutions. The top five companies collectively account for nearly 63% of total market presence, reflecting strong technology leadership and broad product portfolios. Competitive positioning is driven by purification efficiency, endotoxin control, scalability, and regulatory compliance. Strategic initiatives include partnerships with CDMOs, expansion of single-use platforms, and integration of digital process analytics. Product innovation focuses on high-capacity membranes, reduced buffer consumption, and closed-system workflows. Smaller players compete by targeting niche research applications and rapid-turnaround clinical manufacturing. Continuous investment in automation and compliance readiness remains critical for sustaining competitive advantage.

Qiagen

Takara Bio

Promega Corporation

Agilent Technologies

Sartorius

Lonza

GenScript

Roche Diagnostics

Bio-Rad Laboratories

Technology advancement in the Plasmid Purification market is centered on scalability, purity enhancement, and process automation. Membrane-based chromatography systems deliver flow rates up to 10× higher than traditional resin columns, improving throughput and reducing processing time. Single-use purification assemblies minimize cross-contamination risks and reduce cleaning validation requirements by nearly 35%. Advanced endotoxin removal technologies achieve reductions exceeding 40%, meeting stringent regulatory thresholds for clinical-grade plasmid DNA. Digital process control platforms enable real-time monitoring of conductivity, UV absorbance, and impurity profiles, improving batch success rates by approximately 27%. Continuous processing concepts and inline filtration reduce buffer usage by up to 22%. AI-assisted process optimization tools are increasingly used to predict yield outcomes and detect deviations early. These technologies collectively enhance reproducibility, compliance, and cost efficiency for both clinical and commercial plasmid manufacturing.

In April 2025, Thermo Fisher Scientific expanded its plasmid purification portfolio with enhanced single-use chromatography consumables designed for large-scale GMP manufacturing, increasing binding capacity by approximately 30%. Source: www.thermofisher.com

In September 2024, Merck introduced an updated plasmid DNA purification workflow integrating low-endotoxin filtration, enabling faster release testing and reducing processing steps by nearly 20%. Source: www.merckgroup.com

In February 2025, Cytiva launched a modular downstream bioprocessing solution optimized for plasmid purification, supporting rapid deployment of GMP facilities and improving process flexibility. Source: www.cytivalifesciences.com

In July 2024, Qiagen expanded production capacity for plasmid purification kits used in vaccine and gene therapy research, increasing annual output by over 25%. Source: www.qiagen.com

The Plasmid Purification Market Report provides a comprehensive assessment of technologies, applications, and end-user adoption across the global biopharmaceutical landscape. The scope includes purification kits, chromatography systems, filtration units, consumables, and integrated downstream processing platforms designed for research, clinical, and commercial-scale plasmid DNA production. Applications covered span gene therapy, DNA and mRNA vaccines, viral vector manufacturing, cell therapy research, and recombinant protein expression. Geographic coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with country-level insights for major biomanufacturing hubs. The report evaluates technology trends such as single-use systems, membrane chromatography, endotoxin reduction, automation, and digital process control. End-user analysis includes biopharmaceutical companies, CDMOs, academic research institutes, and government laboratories. Emerging niches such as modular GMP facilities, continuous processing, and AI-enabled purification optimization are included. The scope supports strategic decision-making by outlining capacity trends, technology evolution, competitive positioning, and regulatory alignment across the plasmid purification value chain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 2,125.6 Million |

|

Market Revenue in 2033 |

USD 5,300.6 Million |

|

CAGR (2026 - 2033) |

12.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Thermo Fisher Scientific, Merck, Cytiva, Qiagen, Takara Bio, Promega Corporation, Agilent Technologies, Sartorius, Lonza, GenScript, Roche Diagnostics, Bio-Rad Laboratories |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |