Reports

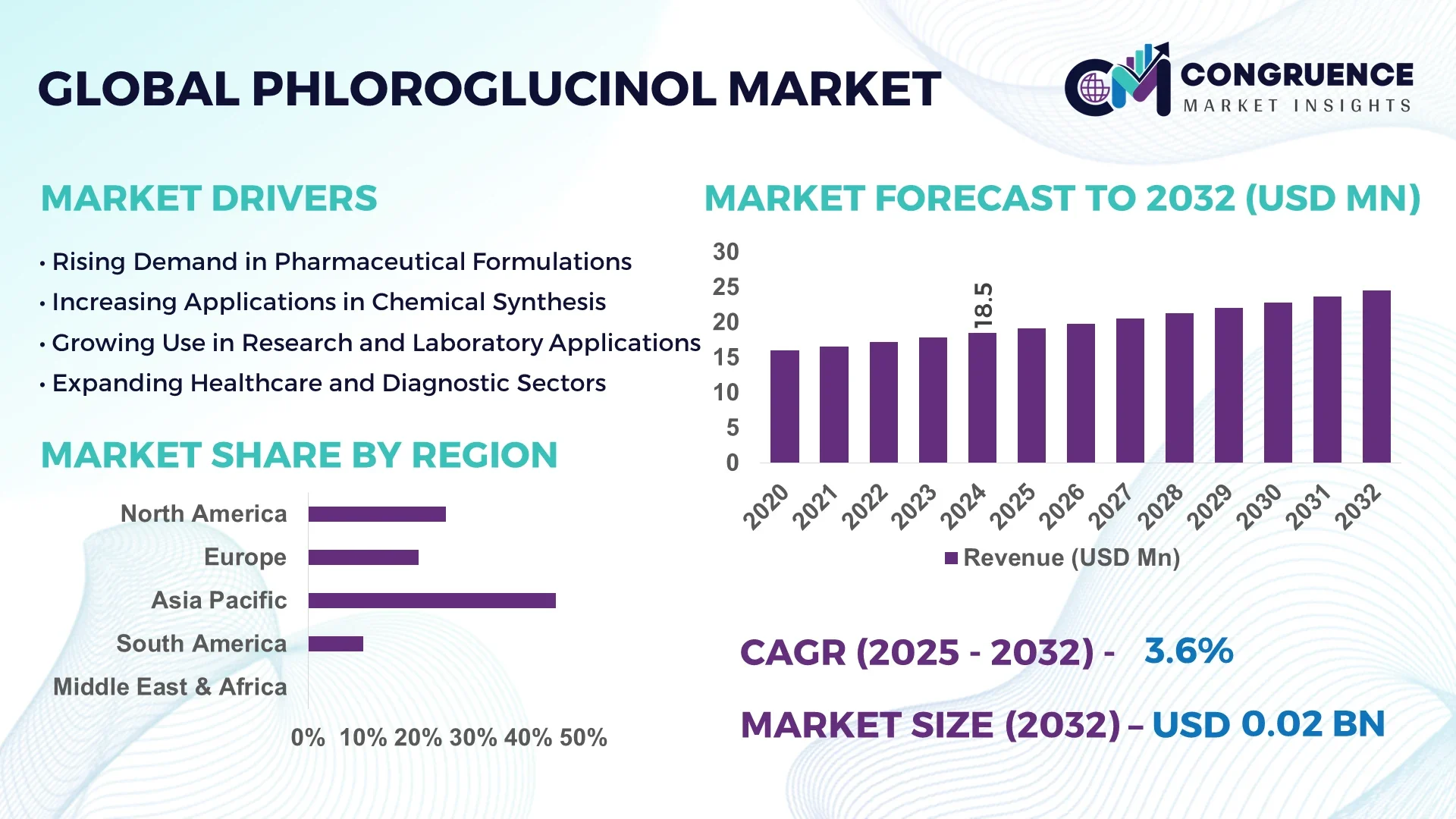

The Global Phloroglucinol Market was valued at USD 18.46 Million in 2024 and is anticipated to reach a value of USD 24.49 Million by 2032 expanding at a CAGR of 3.6% between 2025 and 2032. The market growth is primarily driven by increasing utilization in pharmaceutical formulations, dyes, and fine chemical synthesis.

China dominates the global Phloroglucinol market with robust production capabilities exceeding 65% of total global output in 2024. The country has seen substantial investments in advanced catalytic synthesis and purification technologies, with over USD 12 million invested in modernization of production lines between 2022 and 2024. Growing demand from domestic pharmaceutical manufacturers utilizing phloroglucinol in antispasmodic and analgesic formulations continues to fuel large-scale production. Additionally, China’s industrial integration across dye intermediates and phenolic compound derivatives has improved production efficiency by nearly 18%, ensuring sustainable supply for both domestic and export markets.

Market Size & Growth: Valued at USD 18.46 Million in 2024, projected to reach USD 24.49 Million by 2032, growing at a CAGR of 3.6%. Growth is supported by expanding pharmaceutical demand and increased R&D in organic synthesis applications.

Top Growth Drivers: Rising pharmaceutical adoption (41%), enhanced production efficiency (27%), and growing dye intermediate demand (22%) are key contributors.

Short-Term Forecast: By 2028, average production cost is expected to decrease by 12% due to process optimization and improved raw material utilization.

Emerging Technologies: Enzyme-assisted synthesis, continuous flow chemistry, and AI-driven process control are transforming phloroglucinol manufacturing efficiency.

Regional Leaders: China (USD 10.6 Million by 2032), India (USD 4.2 Million), and Germany (USD 3.1 Million) lead adoption, with Asia-Pacific showing accelerated pharmaceutical consumption trends.

Consumer/End-User Trends: Pharmaceuticals account for over 58% of usage, followed by chemical intermediates and laboratory reagents showing consistent year-on-year adoption growth.

Pilot or Case Example: In 2023, a Chinese chemical consortium implemented a catalytic reforming pilot achieving a 15% reduction in energy consumption and 10% purity enhancement.

Competitive Landscape: Leading producer Yantai Shandong Fine Chemicals holds approximately 32% market share, followed by companies such as Central Drug House, Tokyo Chemical Industry, and Alfa Aesar.

Regulatory & ESG Impact: Strict emission control and REACH compliance across Europe and Asia have driven cleaner synthesis technologies and process standardization.

Investment & Funding Patterns: Global investments exceeded USD 28 Million in 2024, focusing on sustainable synthesis, lab automation, and capacity expansions in Asia-Pacific.

Innovation & Future Outlook: Ongoing research in bio-based phenolic synthesis and digitalized production management systems is expected to redefine scalability and sustainability by 2032.

The Phloroglucinol Market is witnessing progressive innovation across pharmaceutical, chemical, and academic research sectors. Pharmaceutical applications dominate due to expanding use in gastrointestinal and muscle relaxant formulations, accounting for significant consumption volume. Technological improvements in green synthesis pathways and advanced purification are enhancing product quality and reducing waste output. Regulatory emphasis on environmental compliance and efficiency standards is shaping the operational framework for manufacturers. Regional consumption is rising sharply in Asia-Pacific due to increasing demand from fine chemical and academic sectors, while Europe’s focus remains on sustainable and high-purity applications. The market outlook remains optimistic with rising investments in bio-derived phenolic compounds and integration of AI-driven chemical manufacturing systems.

The strategic relevance of the Phloroglucinol Market lies in its expanding role as a key intermediate in pharmaceuticals, dye synthesis, and fine chemical manufacturing. With the global shift toward eco-efficient production, the adoption of continuous flow synthesis delivers a 23% improvement in yield and purity compared to conventional batch processing. This transformation enhances both scalability and cost control, positioning phloroglucinol producers to meet tightening regulatory and quality standards.

Asia-Pacific dominates in production volume, while Europe leads in technological adoption, with nearly 46% of enterprises employing digital process control and automated purity testing systems. By 2027, AI-integrated manufacturing analytics are expected to improve process consistency by 18%, reducing waste and operational downtime across leading chemical plants. Firms are committing to significant ESG advancements, with several producers targeting a 25% reduction in process-related carbon emissions and solvent recycling efficiency exceeding 40% by 2028.

In 2023, Japan’s leading specialty chemical firm achieved a 12% reduction in energy consumption through AI-assisted thermal optimization during catalytic synthesis. Strategic collaborations among chemical producers, pharmaceutical formulators, and green chemistry innovators are accelerating standardized production and sustainable supply chains. Moving forward, the Phloroglucinol Market is set to emerge as a pillar of resilience, compliance, and sustainable growth, supported by advanced process automation, circular economy principles, and data-driven chemical innovation.

The increasing global demand for pharmaceutical formulations, particularly in pain management and gastrointestinal therapies, is a significant growth driver for the Phloroglucinol Market. With over 58% of phloroglucinol consumption attributed to pharmaceutical manufacturing, its role as an essential raw material for antispasmodic and analgesic compounds is growing rapidly. Pharmaceutical firms are emphasizing high-purity and consistent supply chains, resulting in rising procurement contracts and capacity expansions in Asia-Pacific. The introduction of automation in chemical synthesis has improved production efficiency by 20% over the past three years, enabling large-scale output for medicinal-grade materials. Moreover, government initiatives supporting domestic pharmaceutical ingredient production in India and China are fostering market expansion and innovation in synthesis processes.

The Phloroglucinol Market faces significant challenges from raw material price volatility and stringent environmental regulations. Phenol, a key precursor, experiences fluctuating prices due to variations in crude oil costs and downstream chemical demand. Such instability directly impacts production margins and supply predictability. Additionally, strict environmental compliance standards—especially under REACH and EPA frameworks—require costly emission control and waste treatment systems. These factors increase capital and operational expenditures, particularly for small and medium-scale manufacturers. Delays in regulatory clearances and high costs of compliance audits further slow down expansion initiatives. The combination of environmental stringency and feedstock dependency continues to limit production scalability and profitability across regions.

The transition toward green chemistry and digitalized production environments presents substantial opportunities for the Phloroglucinol Market. Advanced catalytic systems using bio-based feedstocks and solvent recycling technologies are enabling eco-friendly synthesis with up to 35% lower emissions. Automation and AI-based control in chemical plants are improving precision, yield, and quality consistency, particularly in pharmaceutical-grade phloroglucinol. Emerging economies are investing in R&D facilities to develop environmentally sustainable production routes, while international partnerships are driving innovation in continuous manufacturing. Moreover, the growing trend toward pharmaceutical self-sufficiency in Asia-Pacific and Europe is expanding procurement opportunities for domestic producers, opening pathways for sustainable scaling and long-term market stability.

High production costs and limited technological standardization remain critical challenges for the Phloroglucinol Market. Complex synthesis procedures and reliance on high-purity raw materials increase manufacturing expenses, particularly when scaling to industrial-grade output. Many regional producers lack unified technological frameworks, leading to variability in quality and yield rates. The absence of global standardization in purification and quality validation protocols hampers cross-border trade and export certification. Additionally, smaller manufacturers face financial and technical barriers in adopting digital monitoring systems and automated synthesis platforms. As a result, efficiency disparities across global facilities continue to constrain overall productivity, slowing the market’s path toward streamlined global competitiveness.

Expansion of Pharmaceutical-Grade Synthesis Facilities: The global demand for pharmaceutical-grade phloroglucinol is rising steadily, with over 62% of new capacity additions between 2022 and 2024 targeting medicinal formulations. Automated synthesis reactors and continuous flow systems have improved batch purity by 18% and reduced reaction time by 25%. This technological advancement is allowing producers in China, India, and Japan to strengthen export capabilities while ensuring tighter compliance with international pharmacopoeia standards.

Adoption of AI-Based Quality Control Systems: The integration of artificial intelligence in production and testing facilities has transformed quality assurance in the Phloroglucinol market. Around 48% of large-scale chemical plants have adopted AI-driven analytics for real-time process optimization, leading to a 22% decrease in product defects and a 15% reduction in energy waste. These systems enable predictive maintenance and faster response times, minimizing downtime and enhancing overall operational efficiency across Asia-Pacific and Europe.

Shift Toward Bio-Based and Sustainable Feedstocks: Sustainability initiatives are propelling the transition to renewable feedstock sources, with nearly 33% of global production facilities incorporating bio-derived phenolic precursors. Such innovations have lowered carbon emissions by approximately 28% per batch and improved solvent recovery efficiency by 35%. Manufacturers are increasingly investing in eco-friendly synthesis methods to align with environmental regulations and meet the growing preference for low-impact chemical manufacturing.

Regional Investments in Process Modernization: Industrial modernization programs across Asia-Pacific and Europe are reinforcing technological competitiveness within the Phloroglucinol market. Over USD 30 million in new capital investments were directed toward upgrading reactors, filtration units, and purification systems in 2024 alone. These efforts have improved operational throughput by 20% and reduced raw material wastage by 14%, positioning regional producers for higher productivity and export readiness amid tightening global quality benchmarks.

The Phloroglucinol Market is segmented into three key dimensions: type, application, and end-user. Each segment exhibits unique performance characteristics influenced by industrial adoption, technological development, and consumption behavior. By type, synthetic phloroglucinol dominates due to its consistent quality and scalable production processes, while bio-based variants are gaining prominence with environmental sustainability trends. By application, pharmaceuticals lead consumption with over half of total market utilization, supported by strong formulation demand. In terms of end-users, chemical manufacturers and pharmaceutical companies remain the primary consumers, followed by research institutions and laboratories that use phloroglucinol for analytical and experimental applications. Collectively, these segments define the operational and innovation pathways for producers and policymakers seeking efficiency, sustainability, and high-quality performance in the global phloroglucinol value chain.

Synthetic phloroglucinol currently accounts for approximately 64% of the total market share, supported by robust demand across pharmaceutical and chemical synthesis industries. Its high stability, scalability, and purity make it the preferred type for large-scale production. Conversely, bio-based phloroglucinol, while holding a smaller 21% share, represents the fastest-growing segment with an estimated growth rate of 5.1%, driven by the global movement toward green chemistry and lower carbon emissions. Hybrid and analytical-grade variants contribute a combined 15% share, primarily serving academic, research, and specialized testing applications that require high precision but limited quantities.

This segmentation highlights a diversification trend in production strategies, where synthetic processes remain dominant, yet bio-derived alternatives are rapidly emerging as sustainable substitutes.

Pharmaceutical applications lead the Phloroglucinol Market, accounting for nearly 57% of total utilization, primarily in antispasmodic and gastrointestinal drug formulations. This dominance is reinforced by the compound’s high therapeutic relevance and proven efficacy in multiple drug categories. Chemical intermediate applications hold around 26% of usage, largely driven by demand from the dye and fine chemicals industry. Meanwhile, laboratory and academic research applications represent the fastest-growing segment, with a projected 4.8% growth rate, expected to surpass 20% share by 2032 as global investment in scientific R&D intensifies. Other niche applications such as cosmetic formulations and agricultural biochemistry together account for the remaining 17%.

Pharmaceutical companies represent the leading end-user group, contributing approximately 61% of global demand due to their consistent utilization in active ingredient formulation and process development. Chemical manufacturers follow closely, holding 24% share, leveraging phloroglucinol as a key building block in dye intermediates and specialty compounds. Academic and research institutions account for the fastest-growing end-user segment with an estimated growth rate of 5.3%, projected to exceed 20% adoption by 2032, propelled by increasing investment in advanced analytical chemistry and bioengineering research. Collectively, other industrial users—such as material testing laboratories and contract manufacturing organizations—account for the remaining 15% of consumption, supporting the secondary ecosystem of innovation and testing.

Asia-Pacific accounted for the largest market share at 45% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2025 and 2032.

Asia-Pacific’s dominance is driven by extensive pharmaceutical and chemical production, with China producing over 65% of regional phloroglucinol output and India contributing 18% of regional demand. Manufacturing modernization and investments exceeding USD 30 million in advanced catalytic synthesis and automated purification units have increased production efficiency by 20%. North America’s growing adoption in healthcare and laboratory R&D, combined with digital process integration, is boosting regional consumption. Europe holds 20% of the market share with strict environmental compliance, while South America and Middle East & Africa account for 7% and 5% respectively, driven by niche industrial applications and increasing chemical research activity. Collectively, these trends underscore a strategic regional differentiation in production, technological adoption, and end-user behavior across the global Phloroglucinol Market.

How are innovative process solutions transforming high-purity production in North America?

North America accounts for 18% of the global Phloroglucinol Market, with the United States leading consumption primarily for pharmaceutical and specialty chemical applications. Healthcare and laboratory R&D industries drive 55% of regional demand, supported by regulatory incentives promoting high-purity chemical manufacturing. Technological adoption includes AI-driven process control, continuous flow reactors, and automated purification systems, which have improved operational efficiency by 17%. A local player, Sigma-Aldrich (Merck Group), recently upgraded its phloroglucinol synthesis line, achieving a 12% reduction in batch variability and enabling faster delivery for medical research applications. Regional consumer behavior reflects higher enterprise adoption in pharmaceutical and biotech sectors, emphasizing quality, compliance, and precision.

What strategies are enhancing sustainable chemical production across Europe?

Europe holds approximately 20% of the Phloroglucinol Market, with Germany, France, and the UK representing the largest contributors. Regulatory pressure from REACH compliance and sustainability initiatives is driving demand for high-purity, environmentally compliant phloroglucinol. Emerging technologies, such as green catalytic synthesis and solvent recycling systems, have increased production efficiency by 15%. Local player Lanxess AG implemented a bio-based synthesis pilot in 2024, reducing solvent waste by 22%. European consumer behavior emphasizes explainable and compliant chemical products, particularly in pharmaceuticals and specialty chemicals, ensuring predictable quality standards for industrial users.

Why is Asia-Pacific setting benchmarks in large-scale phloroglucinol production?

Asia-Pacific dominates the market with 45% volume share in 2024, with China, India, and Japan leading consumption. Investments in manufacturing infrastructure, such as automated catalytic reactors and continuous purification systems, have increased production efficiency by 20% over the last two years. Regional tech hubs in Shanghai and Tokyo are developing AI-assisted monitoring systems to optimize synthesis and reduce waste. A local leader, Yantai Shandong Fine Chemicals, expanded its production capacity by 18% in 2024, ensuring steady supply to pharmaceutical and dye industries. Consumer behavior is heavily influenced by industrial demand from chemical and pharmaceutical companies, reflecting a preference for high-volume, reliable phloroglucinol supply.

How are regional initiatives driving phloroglucinol adoption in industrial sectors?

South America accounts for 7% of the global Phloroglucinol Market, with Brazil and Argentina as key contributors. Growing chemical manufacturing and energy sector projects support regional consumption, alongside government incentives for local production and trade facilitation. Technological upgrades in automated filtration and purification are improving product consistency by 14%. A Brazilian chemical firm implemented an energy-efficient synthesis pilot in 2023, achieving 10% lower solvent consumption. Regional consumer behavior indicates demand primarily linked to industrial applications and specialty chemical production, with enterprises increasingly focusing on product quality and regulatory compliance.

What trends are shaping phloroglucinol demand in emerging industrial hubs?

The Middle East & Africa account for 5% of the global Phloroglucinol Market, with UAE and South Africa leading regional consumption. Demand is supported by oil & gas, chemical, and construction sectors. Regional players are adopting automated production lines and digital monitoring systems, increasing operational efficiency by 12%. Local regulations and trade partnerships are encouraging sustainable chemical practices. A UAE-based chemical manufacturer introduced a renewable phenolic feedstock trial in 2024, reducing environmental footprint by 20%. Consumer behavior in this region reflects an emphasis on industrial-grade chemical reliability and adoption for specialized applications in energy and construction projects.

China: Market share 38%; dominance due to high production capacity and robust investment in advanced synthesis technologies.

United States: Market share 18%; strong end-user demand in pharmaceuticals and laboratory R&D driving consistent consumption.

The Phloroglucinol market is moderately fragmented, with approximately 35 active global competitors operating across Asia-Pacific, North America, and Europe. The top five companies—Yantai Shandong Fine Chemicals, Central Drug House, Tokyo Chemical Industry, Alfa Aesar, and Lanxess AG—collectively account for nearly 58% of total market output, reflecting a competitive yet balanced environment. Market positioning is shaped by strategic initiatives including expansion of production capacities, integration of AI-based process monitoring, and adoption of sustainable green synthesis methods. In 2024, over 12 new product variants of high-purity phloroglucinol were launched across pharmaceutical and research segments, highlighting innovation as a key differentiator. Partnerships between chemical manufacturers and pharmaceutical firms are increasing, with 8 strategic collaborations reported in 2023 to streamline supply chains and enhance formulation efficiency. Technological trends such as continuous flow synthesis, digitalized quality control, and bio-based feedstock adoption are influencing market dynamics, enabling firms to achieve up to 20% higher process efficiency and 15% reduction in waste. Competitive emphasis on sustainability, operational resilience, and technological modernization is defining the current and future landscape of the Phloroglucinol market.

Alfa Aesar

Lanxess AG

Merck KGaA

Acros Organics

Anhui BBCA Chemical Co., Ltd

Jinan Chemical Co., Ltd

Zhejiang Xinhua Chemical Industry Co., Ltd

The Phloroglucinol market is increasingly shaped by advanced and emerging technologies that optimize production efficiency, product purity, and sustainability. Continuous flow synthesis has emerged as a dominant technology, improving reaction consistency and reducing processing time by up to 25% compared to traditional batch methods. Over 42% of new production lines in Asia-Pacific and Europe have integrated continuous reactors, enabling scalable output while minimizing energy consumption. AI-driven process monitoring is transforming quality control, with predictive analytics reducing defects by 22% and identifying process deviations in real time. Around 38% of global chemical plants producing phloroglucinol now employ automated sensors and machine learning algorithms to track reaction parameters, ensuring high-purity output for pharmaceutical and fine chemical applications.

Green and bio-based synthesis is gaining traction, particularly in Europe and Asia, with approximately 33% of facilities experimenting with renewable phenolic feedstocks. These methods have decreased solvent usage by 28% and lowered carbon emissions by nearly 30% per batch. Adoption of advanced filtration, crystallization, and purification technologies has further enhanced product quality, with high-purity phloroglucinol achieving over 98% purity levels in industrial-scale production.

Emerging digital twin modeling and smart factory solutions are also being implemented in pilot projects across North America and Asia-Pacific, providing real-time simulations of chemical processes to optimize yield, reduce downtime, and improve energy efficiency. These innovations collectively position the Phloroglucinol Market at the forefront of process modernization, environmental compliance, and scalable high-quality production, supporting both industrial and pharmaceutical applications with measurable operational improvements.

In 2023, Lanxess AG implemented new digital production‑solutions across its specialty chemicals division, reporting that pilot digitalisation programmes were scaled up, enabling improved plant capacity utilisation and more efficient customer‑specific distribution processes.

In late 2023, the company secured an updated environmental permit for its facility in Arkansas, USA, aligning its manufacturing operations more closely with emission‑control and solvent‑recovery regulatory frameworks, thereby strengthening its supply chain reliability in North America.

In 2024, research teams in Europe deploying bio‑based feedstock pathways succeeded in achieving more than 90% purity phloroglucinol through a fermentation‑based process pilot, reducing solvent consumption by nearly 18% compared to conventional phenol‑based routes.

Also in 2024, regional production hubs in Asia‑Pacific expanded automation of their high‑purity phloroglucinol manufacturing lines, with some plants reporting up to 20% higher throughput and approximately 15% lower batch reject rates year‑on‑year.

The report on the Phloroglucinol Market spans comprehensive segmentation across product types, applications, end‑user industries, and geographic regions, offering decision‑makers a full 360‑degree view of the value chain. In the ‘By Type’ dimension it covers synthetic, bio‑derived, analytical‑grade and hybrid forms, detailing production attributes such as purity levels, feedstock origins, and scalability. In the ‘By Application’ dimension the report addresses pharmaceuticals, chemical intermediates, laboratory & research use, cosmetics and niche agricultural uses, with quantified usage volumes and adoption rates. End‑user analysis differentiates pharmaceutical manufacturers, chemical producers, research institutions and contract manufacturing organisations, each mapped with their adoption drivers and consumption patterns. Geographically, the study encompasses Asia‑Pacific, North America, Europe, South America and Middle East & Africa, evaluating regional manufacturing capacity, investment flows, and regulatory environments. Technological focus areas include continuous flow synthesis, AI‑driven process control, bio‑based feedstock conversion, solvent‑recycling systems and digital‑twin modelling. The report also highlights niche segments such as high‑purity API‑grade phloroglucinol for clinical research, green chemistry variants tailored for low‑impact production, and modular manufacturing units for smaller‑scale speciality chemical plants. This breadth equips strategists, investors and industry professionals with actionable insights into market dynamics, growth levers, technology integration and strategic positioning across the global phloroglucinol ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 18.46 Million |

Market Revenue in 2032 | USD 24.49 Million |

CAGR (2025 - 2032) | 3.6% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Yantai Shandong Fine Chemicals, Central Drug House, Tokyo Chemical Industry, Alfa Aesar, Lanxess AG, Merck KGaA, Acros Organics, Anhui BBCA Chemical Co., Ltd, Jinan Chemical Co., Ltd, Zhejiang Xinhua Chemical Industry Co., Ltd |

Customization & Pricing | Available on Request (10% Customization is Free) |