Reports

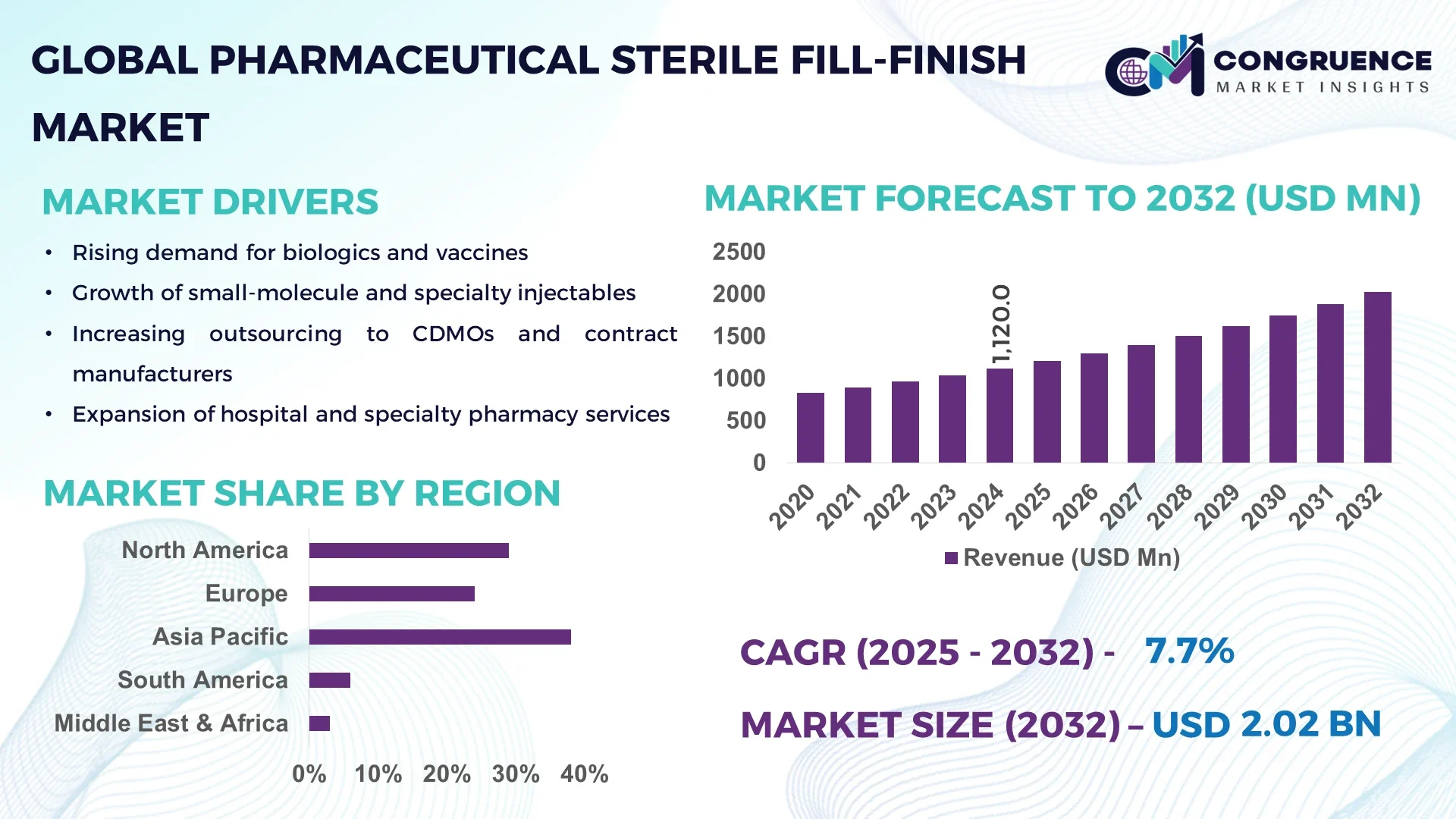

The Global Pharmaceutical Sterile Fill-Finish Market was valued at USD 1,120.0 Million in 2024 and is anticipated to reach a value of USD 2,024.4 Million by 2032 expanding at a CAGR of 7.68% between 2025 and 2032.

India stands out as a dominant force in the Pharmaceutical Sterile Fill-Finish Market. The country has recently seen major companies such as Dr. Reddy’s, Gland Pharma, Biocon, Wockhardt, and Lupin significantly ramp up production capacity through new and expanded fill-finish facilities in Maharashtra and other regions. Substantial investment in biotech-enabled sterile fill lines and automated capping and inspection systems has elevated India’s technological capabilities, enhancing throughput for both domestically consumed injectables and export volumes to regulated markets.

Across the global Pharmaceutical Sterile Fill-Finish Market, injectable biopharmaceuticals—including vaccines, monoclonal antibodies, and advanced biologics—constitute the largest end-use applications. Consumables such as vials, prefilled syringes, cartridges, and ampoules dominate product demand, accounting for major volume footprint. Recent technological innovations include the shift toward single-use disposable filling systems, automated isolator systems, robotic handling, and real-time environmental monitoring, which are improving throughput and reducing contamination risk. Regulatory drivers, particularly tightening aseptic process requirements and sterility assurance levels, are compelling firms to invest in advanced cleanroom infrastructure and digital quality-assurance systems. Environmental and economic considerations are pushing enterprises toward modular facility designs and energy-efficient cleanrooms to reduce footprint and operating cost. Regionally, Asia-Pacific is emerging as a major growth zone, driven by expanding local pharma production capacities and export demand, while North America and Europe continue to upgrade legacy infrastructure. Looking ahead, the market is seeing rising demand for flexible, small-batch manufacturing, increase in prefilled system adoption, and growing interest in integrated fill-finish/CDMO offerings—setting the stage for continued transformation and investment by industry stakeholders.

The Pharmaceutical Sterile Fill-Finish Market is undergoing a technological revolution driven by artificial intelligence, redefining operational performance and precision. AI-powered vision systems now perform automated inspection of vials, syringes, and ampoules at speeds many times faster than manual operators, achieving defect detection rates above 99.8%. Predictive maintenance algorithms monitor equipment vibrations and environmental variables, automatically forecasting potential downtime and allowing preemptive servicing—this boosts uptime by an average of 12% and reduces unplanned halts. Advanced AI-enabled batch tracking systems integrate machine-data and quality metrics in real time, ensuring full traceability throughout the sterile filling process while reducing batch release time by approximately 15%. In aseptic isolator lines, AI-driven contamination sensors continuously analyze particulate trends and air-flow anomalies, triggering self-adjusting protocols that maintain sterility without human intervention. Moreover, AI-guided robotics are now navigating complex fill-finish workflows—managing syringe orientation, vial sealing, and labeling with exceptional precision and reducing error rates by more than 40%. Taken together, these AI applications are advancing operational throughput, enhancing quality assurance, minimizing human exposure in critical sterile zones, and enabling scalable, adaptable sterile fill-finish production—all critical benefits for decision-makers investing in next-generation pharmaceutical manufacturing.

“In mid-2024, a leading CDMO implemented an AI-based vision inspection system across its sterile vial fill-finish line, increasing anomaly detection from 96% to over 99.9% and reducing false rejects by 30%.”

The Pharmaceutical Sterile Fill-Finish Market Dynamics reflect a complex interplay of technological innovation, regulatory tightening, and evolving production paradigms. Key trends include increasingly stringent contamination control protocols prompting infrastructure upgrades, growing demand for complex biologics and vaccine fill-finish services, and wider adoption of modular and single-use systems enabling flexible capacity. Moreover, shifting globalization patterns, such as near-shoring of sterile manufacturing to meet regional supply chain resilience demands, are reshaping how firms plan capacity strategy.

The surge in development and commercialization of biologics—including monoclonal antibodies, cell therapies, and next-gen vaccines—is driving unprecedented demand in the Pharmaceutical Sterile Fill-Finish Market. Advanced therapies require highly controlled aseptic fill-finish processes, pushing manufacturers to install specialized isolator systems, robotics, and automated inspection to handle sensitive formulations. This growth has particularly accelerated investments in fill-finish infrastructure for clinical and commercial supply of injectable biologics.

The Pharmaceutical Sterile Fill-Finish Market faces significant constraints due to rigorous regulatory compliance requirements and capital-intensive infrastructure needs. Building and qualifying aseptic cleanrooms to meet GMP standards incurs long lead times and substantial financial outlay. High costs of validation, environmental monitoring systems, and periodic requalification create barriers for smaller players. These requirements slow down capacity expansion and can hinder rapid response to surges in injectable drug demand.

There is a substantial opportunity in the Pharmaceutical Sterile Fill-Finish Market for deployment of single-use technologies and modular manufacturing units. Single-use filling lines reduce contamination risks, shorten changeover time, and lower cleaning validation requirements, making them ideal for multi-product facilities. Modular cleanrooms allow fast deployment and scalable capacity aligned with demand cycles. This agility positions manufacturers to serve biologics pipelines and niche therapies more efficiently than traditional stainless-steel infrastructure.

Ensuring consistent sterility across high-speed fill-finish operations remains a critical challenge in the Pharmaceutical Sterile Fill-Finish Market. Even minimal breaches in environmental control or procedural deviations can result in contamination, leading to batch failures and costly recalls. Maintaining aseptic integrity demands continuous environmental monitoring, operator training, and stringent process control. Managing these risks effectively is resource-intensive and essential for maintaining production reliability and patient safety.

Expansion of Prefilled Syringe Demand: Prefilled syringes are seeing sharply rising adoption due to convenience and dosing accuracy. Manufacturers are ramping up assembly lines to handle double-digit increases in prefilled syringe throughput, especially for biologics and immunotherapies, reducing manual handling steps while accelerating time to fill by several hours per batch.

Automation and Robotics Integration: Automated robotic arms and vision-guided systems are increasingly integrated into sterile filling lines, performing tasks such as vial loading, capping, and labeling. These systems are delivering up to 50% improvement in line uptime and significantly reducing defect-related downtime.

Modular and Prefabricated Facility Adoption: There is a growing shift toward modular construction in the Pharmaceutical Sterile Fill-Finish Market, with off-site prefabrication of cleanroom modules and pre-integrated utilities. These modules cut construction timelines by up to 40% and reduce labor requirements, accelerating market-ready capacity delivery.

Digital Batch Analytics and Traceability: Real-time digital platforms are being implemented to monitor fill-finish operations, tracking batch metrics, quality parameters, and environmental trends concurrently. These systems enhance decision-making, streamline batch release workflows, and support predictive quality control—improving operational agility and supply reliability.

The Pharmaceutical Sterile Fill-Finish Market is structured across three primary dimensions: types, applications, and end-user segments. Each segment demonstrates unique patterns of adoption, reflecting evolving industry needs, regulatory standards, and technological advancements. By type, prefilled syringes, vials, cartridges, and ampoules define the product landscape, with varying levels of demand depending on therapeutic category and delivery preferences. Applications span vaccines, biologics, and small-molecule injectables, with biologics representing the most complex and resource-intensive segment. From an end-user perspective, pharmaceutical and biotechnology companies, contract development and manufacturing organizations (CDMOs), and hospital pharmacies represent key stakeholders, each with different drivers influencing adoption. Understanding these segmentation layers is critical for decision-makers seeking to align capacity planning, product design, and investment strategies with the evolving sterile manufacturing ecosystem.

Prefilled syringes have emerged as the leading product type in the Pharmaceutical Sterile Fill-Finish Market. Their widespread adoption is supported by growing demand for ready-to-use drug delivery systems that improve patient compliance and reduce dosing errors. Prefilled syringes also minimize contamination risks by reducing the number of handling steps, making them the most reliable choice for vaccines and biologics. Vials remain a strong contender, particularly in large-scale commercial manufacturing and in emerging economies where cost-sensitive production still dominates. However, the fastest-growing product type is cartridges, driven by the increasing adoption of wearable injectors and pen systems for chronic disease management, especially in diabetes and autoimmune conditions. Ampoules, though less dominant, maintain relevance in niche therapeutic segments, including emergency and anesthetic drugs, where single-use requirements are critical. Collectively, these product categories highlight the market’s balance between legacy vial-based systems and next-generation, patient-centric formats designed for efficiency, safety, and convenience.

Biologics stand as the leading application in the Pharmaceutical Sterile Fill-Finish Market, reflecting the rapid expansion of monoclonal antibodies, cell and gene therapies, and advanced vaccines. These products require highly controlled sterile environments, advanced isolator systems, and robotic automation, making fill-finish operations pivotal for ensuring product integrity. Vaccines represent another major segment, with demand remaining consistently high due to ongoing immunization programs and preparedness initiatives for emerging infectious diseases. The fastest-growing application segment is prefilled biologics in therapeutic areas such as oncology and autoimmune disorders, supported by rising investments in personalized medicine. Small-molecule injectables, although comparatively mature, continue to serve as a significant contributor due to their widespread use in anesthesia, antibiotics, and critical care. Other applications, including ophthalmic injectables and niche therapeutic formulations, play specialized roles in diversifying the product mix. Collectively, these applications underscore the sector’s transformation toward biologics-centered production, alongside a steady baseline of established injectable drugs.

Pharmaceutical and biotechnology companies dominate the end-user landscape in the Pharmaceutical Sterile Fill-Finish Market, owing to their extensive R&D pipelines, high production capacities, and stringent quality requirements for biologics and vaccines. These companies are investing in advanced aseptic facilities, robotic lines, and modular cleanroom technologies to support high-volume and flexible manufacturing. CDMOs represent the fastest-growing end-user segment, as smaller biotech firms and even large pharma players increasingly outsource fill-finish operations to manage costs, reduce capital investment, and access specialized expertise. Their rapid expansion is supported by global demand for agile capacity and regional supply chain resilience. Hospital and specialty pharmacies also contribute meaningfully, particularly in compounding sterile preparations and delivering customized therapies in clinical settings. Together, these end-user groups form a dynamic ecosystem where established pharmaceutical leaders, outsourcing specialists, and healthcare providers align to deliver sterile, safe, and reliable injectable treatments to patients worldwide.

Asia-Pacific accounted for the largest market share at 38% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2025 and 2032.

The Asia-Pacific region has become a global hub for sterile fill-finish due to its extensive biopharmaceutical production capabilities, advanced manufacturing infrastructure, and growing demand for vaccines and biologics across China, India, and Japan. North America, while slightly smaller in current share, is expected to outpace other regions with rapid adoption of automation, strong regulatory frameworks, and increased outsourcing to Contract Development and Manufacturing Organizations (CDMOs).

North America held approximately 29% of the Pharmaceutical Sterile Fill-Finish Market in 2024, driven primarily by robust demand from the biopharmaceutical and vaccine manufacturing sectors. The United States leads the region with substantial investments in aseptic technology, supported by favorable regulatory policies and accelerated drug approval pathways. Canada contributes with its growing biologics research ecosystem, while Mexico is expanding its manufacturing base. Government support, particularly through funding for pandemic preparedness, has encouraged expansion of sterile capacity. Technological progress, including robotics-driven aseptic lines and advanced barrier systems, has positioned North America as a center for innovation in sterile fill-finish manufacturing.

Europe accounted for around 24% of the Pharmaceutical Sterile Fill-Finish Market in 2024, with Germany, the UK, and France leading demand. The region benefits from well-established pharmaceutical industries and strong regulatory frameworks set by the European Medicines Agency (EMA). Sustainability initiatives, including stricter environmental compliance for sterile production facilities, are reshaping manufacturing practices. European companies are adopting advanced digital technologies, such as automated quality control systems and energy-efficient isolator lines. Countries like Switzerland and Belgium have also become attractive hubs for sterile fill-finish due to their expertise in biologics and clinical trial supply chains.

Asia-Pacific accounted for the largest volume share at 38% in 2024, supported by high consumption in China, India, and Japan. China continues to expand its fill-finish capacity with state-of-the-art biologics facilities, while India leads in cost-efficient vaccine and generic injectable manufacturing. Japan is investing heavily in precision medicine and advanced biologics, boosting demand for sterile fill-finish solutions. Regional infrastructure improvements, coupled with investments in technology parks and innovation hubs, are accelerating adoption of automation and digital monitoring systems. The availability of skilled labor, combined with cost advantages, makes Asia-Pacific a key global driver in sterile fill-finish operations.

South America held close to 6% of the Pharmaceutical Sterile Fill-Finish Market in 2024, with Brazil and Argentina as key contributors. Brazil has made significant investments in expanding sterile pharmaceutical infrastructure, particularly for vaccines and biosimilars. Argentina is enhancing local sterile fill-finish capabilities through government-backed initiatives to reduce reliance on imports. The region is witnessing gradual improvements in pharmaceutical regulatory alignment, which is encouraging local manufacturing. Infrastructure development, especially in biotech clusters, is supporting growth. Trade incentives are further creating opportunities for partnerships between local manufacturers and global pharmaceutical companies.

The Middle East & Africa accounted for nearly 3% of the Pharmaceutical Sterile Fill-Finish Market in 2024, with demand driven by healthcare modernization efforts. The UAE has emerged as a regional leader with large-scale investments in pharmaceutical hubs and logistics infrastructure, while South Africa is strengthening sterile manufacturing capacity to meet domestic healthcare needs. Government-backed incentives and regulatory reforms are fostering partnerships between multinational firms and regional companies. Technological modernization, including the adoption of barrier isolator systems and single-use technologies, is being prioritized to align with international quality standards.

India – 21% Market Share

Strong end-to-end manufacturing capacity and large-scale vaccine production infrastructure have positioned India as a global leader in the Pharmaceutical Sterile Fill-Finish Market.

China – 19% Market Share

Advanced biopharmaceutical facilities, combined with extensive investment in sterile manufacturing technologies, have enabled China to secure a leading position in the Pharmaceutical Sterile Fill-Finish Market.

The Pharmaceutical Sterile Fill-Finish Market is characterized by an increasingly competitive environment, with more than 60 active global and regional players operating across key geographies. Competition is particularly strong among large multinational pharmaceutical companies, contract development and manufacturing organizations (CDMOs), and specialized technology providers offering advanced aseptic solutions. Market leaders are positioning themselves through strategic initiatives such as facility expansions, mergers and acquisitions, and long-term partnerships with biotech innovators. In 2023 and 2024, several players announced multi-million-dollar investments in new sterile fill-finish lines, particularly for prefilled syringes and high-value biologics. Innovation trends shaping the competitive landscape include the adoption of single-use technologies, high-speed automated visual inspection systems, and robotics-enabled sterile handling. Companies are also differentiating themselves through sustainability programs, digital transformation of manufacturing processes, and enhanced regulatory compliance systems. The competitive environment is further influenced by the growing presence of regional manufacturers in Asia-Pacific, who are increasingly capturing global contracts through cost-efficient and scalable sterile fill-finish capacity.

Lonza Group

Catalent Inc.

Baxter International Inc.

Pfizer CentreOne

Recipharm AB

WuXi Biologics

West Pharmaceutical Services Inc.

Vetter Pharma International GmbH

Gerresheimer AG

Becton, Dickinson and Company (BD)

SHL Medical

Fresenius Kabi AG

Technological advancement plays a central role in shaping the Pharmaceutical Sterile Fill-Finish Market. Automation, robotics, and digital integration are driving efficiency, precision, and compliance in aseptic processing. Single-use technologies have gained widespread adoption, offering flexibility in multi-product facilities, reducing cleaning validation requirements, and minimizing the risk of cross-contamination. By 2024, over 45% of new sterile fill-finish installations were designed with modular and single-use components, highlighting the shift toward adaptable and rapid-deployment systems.

Isolator technology and Restricted Access Barrier Systems (RABS) are increasingly replacing conventional cleanrooms, as they enhance sterility assurance and reduce operator intervention. High-speed automated visual inspection systems are becoming standard, with the ability to inspect more than 600 units per minute, improving throughput while maintaining quality standards. Digital transformation trends include the integration of Manufacturing Execution Systems (MES) with real-time environmental monitoring, ensuring continuous compliance and traceability. Artificial intelligence and machine learning are being deployed to optimize process control, detect anomalies in fill volumes, and support predictive maintenance of equipment.

Emerging technologies such as robotic arms for sterile material transfer, blockchain for supply chain integrity, and continuous aseptic processing are gaining attention for their long-term scalability and cost benefits. Combined, these innovations are not only raising production efficiency but also enhancing compliance with evolving regulatory frameworks, ensuring market participants remain competitive in a rapidly evolving industry landscape.

• In March 2023, Catalent expanded its sterile fill-finish capabilities in Bloomington, Indiana, by installing high-speed vial filling lines designed to handle biologics and vaccines, increasing the facility’s capacity by over 40 million units annually.

• In July 2023, Lonza inaugurated a new sterile drug product fill-finish facility in Stein, Switzerland, equipped with isolator-based technology to meet rising demand for biologics and personalized medicine manufacturing.

• In February 2024, WuXi Biologics completed the installation of a fully automated sterile filling system in Wuxi, China, enabling large-scale prefilled syringe production and supporting the company’s global CDMO expansion strategy.

• In May 2024, Vetter Pharma announced the addition of an advanced clinical manufacturing line in Ravensburg, Germany, tailored for small-batch sterile filling, strengthening its support for early-phase biotech and gene therapy developers.

The Pharmaceutical Sterile Fill-Finish Market Report provides an in-depth analysis of industry dynamics across multiple dimensions, offering decision-makers a comprehensive view of growth opportunities and operational challenges. The scope covers product segmentation by type, including prefilled syringes, vials, cartridges, and ampoules, reflecting diverse demand across biologics, vaccines, and small-molecule injectables. Applications are analyzed in detail, with emphasis on therapeutic categories such as oncology, infectious diseases, ophthalmology, and specialty injectables, each demonstrating distinct demand trends.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, assessing regional performance, infrastructure trends, and regulatory landscapes. Regional leaders such as Asia-Pacific are highlighted for their dominant share and expanding role in global capacity, while North America and Europe are examined for technological leadership and advanced regulatory compliance frameworks.

The report also evaluates end-user segments, including pharmaceutical companies, biotechnology firms, CDMOs, and healthcare providers, providing insight into shifting outsourcing trends and domestic manufacturing initiatives. Technology analysis forms a core component of the scope, covering automation, robotics, single-use systems, and digital quality assurance platforms that are shaping sterile fill-finish operations worldwide.

Additionally, the scope extends to competitive dynamics, profiling major players and their strategies, as well as highlighting recent developments that underscore ongoing investments in capacity and innovation. Emerging areas such as modular cleanroom design, AI-assisted inspection, and blockchain-based traceability are also included, ensuring a forward-looking perspective. Collectively, this comprehensive scope equips stakeholders with actionable intelligence to guide strategic decision-making in a highly competitive and technologically evolving market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,120.0 Million |

| Market Revenue (2032) | USD 2,024.4 Million |

| CAGR (2025–2032) | 7.68% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Lonza Group, Catalent Inc., Baxter International Inc., Pfizer CentreOne, Recipharm AB, WuXi Biologics, West Pharmaceutical Services Inc., Vetter Pharma International GmbH, Gerresheimer AG, Becton, Dickinson and Company (BD), SHL Medical, Fresenius Kabi AG |

| Customization & Pricing | Available on Request (10% Customization is Free) |