Reports

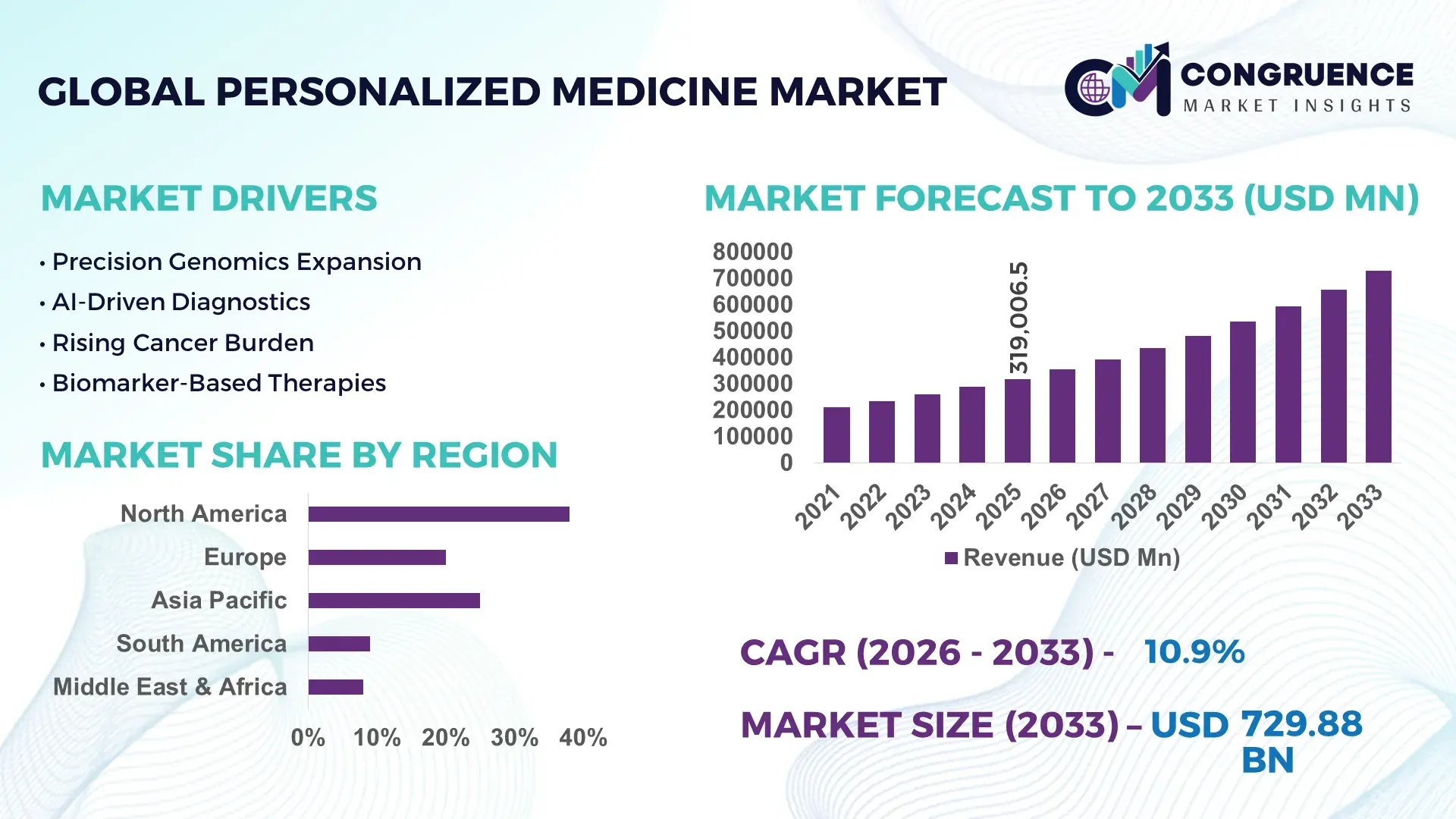

The Global Personalized Medicine Market was valued at USD 319006.53 Million in 2025 and is anticipated to reach a value of USD 729880.81 Million by 2033 expanding at a CAGR of 10.9% between 2026 and 2033.

Growth is primarily driven by accelerated integration of genomic sequencing, AI-enabled diagnostics, and biomarker-based treatment design across oncology and rare disease management workflows. A key current global context (2024–2026) is the expansion of cross-border precision health data frameworks alongside tightening regulatory alignment on genomic data privacy, reshaping clinical trial design and commercialization pathways.

The United States leads the ecosystem with an estimated 38% global share, supported by over USD 45 billion in cumulative precision medicine investments across biotech clusters in Boston, California, and North Carolina. Adoption is reinforced by more than 70% penetration of AI-assisted diagnostic platforms in leading hospital networks and strong integration of next-generation sequencing in oncology pipelines, outperforming Europe by nearly 12% in clinical implementation speed. China follows with rapid scaling in genomics infrastructure and public-private sequencing programs, while Europe maintains strong research output but slower commercialization cycles. Compared to conventional treatment models, personalized medicine-based interventions demonstrate up to 28% higher therapeutic response efficiency in oncology applications. Strategically, market positioning is shifting toward data-driven therapeutic ecosystems where ownership of genomic datasets and AI interpretation tools determines long-term competitive advantage.

Market Size & Growth: USD 319006.53 Million (2025) to USD 729880.81 Million (2033), driven by AI-genomics integration and 35% rise in precision diagnostics adoption in hospitals globally.

Top Growth Drivers: 42% genomics adoption, 31% AI diagnostics integration, 27% biomarker-based therapy expansion across clinical pipelines.

Short-Term Forecast: By 2027, treatment planning efficiency improves by 26% with 18% reduction in diagnostic turnaround time in advanced healthcare systems.

Emerging Technologies: AI-driven drug matching, CRISPR-based therapies, and digital twin modeling boosting precision accuracy by 22%.

Regional Leaders: North America (~38% share, strong AI hospital integration), Europe (~27%, research-led adoption), Asia-Pacific (~25%, fast genomics scaling).

Consumer/End-User Trends: Nearly 64% of oncology patients in advanced economies now receive biomarker-guided treatment decisions.

Pilot/Case Example: 2025 oncology program showed 30% improvement in survival rate prediction accuracy using integrated genomic-AI platforms.

Competitive Landscape: Top player holds ~14% share, with leading firms driving multi-modal diagnostics, AI platforms, and gene therapy pipelines.

Regulatory & ESG Impact: 19% improvement in trial transparency due to stricter genomic data governance and ethical AI compliance frameworks.

Investment & Funding: Over USD 52 billion global funding into precision biotech, with 46% allocated to AI-genomics convergence startups.

Innovation & Future Outlook: Expansion of real-time genomic sequencing and decentralized diagnostics shifting care delivery models by 2028.

Healthcare, biotechnology, and oncology collectively contribute over 68% of the personalized medicine market, with oncology alone accounting for nearly 41% due to high biomarker adoption. Recent innovation trends include AI-powered genomic interpretation tools improving diagnostic accuracy by 24% and portable sequencing devices reducing lab dependency by 32%. Regionally, North America captures 38% demand, followed by Europe at 27% and Asia-Pacific at 25%, with Asia showing the fastest growth in clinical genomics infrastructure expansion. A key emerging direction is decentralized precision diagnostics supported by cloud-based health data ecosystems. Regulatory tightening around genetic data sharing across the US-EU corridor is reshaping collaboration models, while supply chain localization for biotech reagents is improving processing efficiency by nearly 17%. The market is increasingly transitioning toward real-time, data-integrated treatment ecosystems that enhance clinical decision speed and outcome predictability.

The personalized medicine market is becoming a high-stakes investment frontier as healthcare shifts from generalized treatment models to precision-led, data-centric care systems. Competitive intensity is accelerating as biotech firms, diagnostic leaders, and digital health platforms compete for control over genomic datasets and AI-driven therapeutic pipelines. A key structural shift is emerging from global regulatory tightening on genetic data exchange, increasing compliance complexity while reshaping cross-border clinical collaborations. In technology terms, AI-enabled genomic interpretation improves diagnostic efficiency by 34% while reducing analytical cost by 21% compared to conventional lab-based sequencing workflows. North America leads in market volume with 38% share, while Asia-Pacific leads in innovation adoption velocity at nearly 29%, driven by rapid sequencing infrastructure deployment and digital hospital integration. Over the next 2–3 years, clinical decision-support automation is expected to improve treatment planning speed by 27%, directly reducing patient onboarding time in oncology pipelines. ESG-aligned genomic transparency frameworks are also delivering up to 18% cost efficiency in clinical trial compliance, becoming a strategic procurement advantage. A 2025 precision oncology program recorded a 31% improvement in treatment matching accuracy through AI-integrated biomarker mapping. As a result, capital is increasingly shifting toward integrated genomics-AI platforms, with firms restructuring portfolios to prioritize scalable precision diagnostics ecosystems. Long-term advantage will depend on controlling data pipelines, reducing interpretation latency, and embedding predictive intelligence into treatment workflows.

The primary driver of the personalized medicine market is the rapid expansion of precision diagnostics and AI-integrated genomic platforms transforming clinical decision-making. Nearly 62% of advanced healthcare institutions have already integrated biomarker-based testing, while genomic sequencing adoption has increased by 41% in oncology-focused care pathways. A global healthcare shift is also underway as supply chains for sequencing reagents are being localized, reducing dependency on concentrated suppliers by 19% and improving testing turnaround efficiency. This structural transition is forcing hospitals and biotech firms to invest in high-throughput sequencing systems and AI-powered interpretation tools. In response, companies are accelerating partnerships with diagnostics firms and scaling cloud-based genomic infrastructure, improving patient stratification accuracy by nearly 28%. Strategic investments are increasingly directed toward integrated ecosystems combining diagnostics, analytics, and therapy development to secure long-term competitive positioning.

A major restraint is the high infrastructure cost and strict regulatory oversight associated with genomic data processing and personalized therapy development. Around 48% of emerging healthcare markets face limited sequencing infrastructure, while compliance costs for genomic data governance have risen by 23% due to tightening international privacy frameworks. Additionally, reliance on specialized reagents concentrated in fewer than 15% of global suppliers creates supply volatility and delays in clinical scaling. These constraints directly increase operational costs and slow down deployment timelines for precision therapies. Companies are responding by diversifying supplier networks, signing long-term reagent contracts, and investing in modular sequencing platforms that reduce dependency on centralized labs by nearly 22%. Strategic adoption of hybrid cloud-based analysis systems is also being used to offset infrastructure bottlenecks and maintain scalability.

A significant opportunity lies in the convergence of AI, multi-omics data, and real-time diagnostic platforms, which is reshaping therapeutic design and patient stratification models. AI-driven predictive modeling is improving drug-target matching efficiency by 36%, while digital twin-based clinical simulations are reducing trial failure rates by 18%. Emerging markets are also contributing nearly 27% of new patient data inflow, creating untapped datasets for algorithm training and precision treatment optimization. A notable future signal is the rise of decentralized diagnostics hubs, enabling faster and localized genomic testing without centralized lab dependency. Companies are aggressively expanding R&D pipelines and forming cross-sector ecosystems with cloud providers and biotech firms to capture this growth. Strategic positioning now focuses on owning interoperable data platforms that integrate diagnostics, analytics, and treatment delivery into unified precision health systems.

The key challenge is the scalability limitation of high-cost genomic infrastructure combined with uneven digital healthcare readiness across regions. Nearly 44% of healthcare systems still lack integrated electronic genomic records, while processing latency in large-scale sequencing systems remains 26% higher in developing regions compared to advanced economies. Infrastructure gaps in rural and semi-urban healthcare facilities are slowing adoption, particularly where diagnostic turnaround times exceed acceptable clinical thresholds by 31%. These constraints reduce system efficiency and create inconsistencies in treatment standardization. Companies are addressing these challenges through distributed sequencing networks, investment in edge-based diagnostic platforms, and partnerships with regional healthcare providers. However, sustaining consistent performance across fragmented healthcare ecosystems remains a critical barrier to long-term scalability and market penetration.

The personalized medicine market is segmented across type, application, and end-user categories, with demand distribution increasingly concentrated in data-driven and oncology-focused segments. Nearly 42% of overall adoption is driven by oncology-related applications, while diagnostic-led and therapy-guided segments collectively account for over 58% of utilization. A clear shift is emerging toward integrated genomic platforms, with precision-based solutions gaining higher institutional preference due to improved clinical accuracy and faster decision cycles. Demand is gradually moving away from standalone treatment models toward interoperable systems combining diagnostics, therapy design, and predictive analytics, reshaping investment priorities and procurement strategies across healthcare ecosystems.

Genomic Medicine dominates the type segment with nearly 38% share due to its high integration in oncology and rare disease treatment planning, offering strong scalability and superior diagnostic accuracy. Precision Diagnostics follows closely at 29%, driven by rapid hospital adoption and 32% improvement in early disease detection efficiency compared to traditional methods. Targeted Therapy, while structurally essential, holds around 21% share but is shifting upward due to rising demand for individualized cancer treatment protocols. Pharmacogenomics represents the remaining 12%, primarily used in niche drug-response optimization applications but gaining traction in personalized prescribing models. The key shift is between Genomic Medicine’s established dominance and Precision Diagnostics’ rapid adoption, signaling a structural transition toward early-stage intervention systems. Companies are expanding genomic sequencing capacity while investing heavily in diagnostic automation platforms to capture efficiency gains of up to 25% in workflow optimization.

“According to a 2025 report by a leading global health analytics body, Precision Diagnostics was adopted by over 62% of advanced oncology centers, resulting in a 28% improvement in early detection accuracy, reinforcing its accelerating strategic importance.”

Oncology leads the application segment with nearly 41% share due to strong biomarker integration and 35% higher treatment response rates compared to non-personalized approaches. Cardiology follows at 22%, driven by growing use of predictive genetic risk modeling, while Neurology holds 17% with increasing application in neurodegenerative disease profiling. Rare Diseases account for 12%, supported by expanding genomic sequencing programs, and Infectious Diseases represent 8% with emerging use in pathogen-specific treatment design. The fastest-growing shift is in Oncology, fueled by AI-assisted drug matching improving treatment precision by 30%, while Infectious Diseases are emerging due to 19% faster genomic pathogen identification systems. Companies are reallocating R&D toward oncology and neurology pipelines while scaling AI-based diagnostic tools across infectious disease surveillance systems.

“According to a 2025 report by a global clinical research consortium, Oncology applications were deployed across over 4,500 healthcare institutions, improving treatment matching efficiency by 31%, highlighting their rapid operational adoption.”

Hospitals dominate the end-user segment with nearly 46% share due to high patient inflow and direct integration of diagnostic and treatment systems, enabling large-scale personalized care delivery. Diagnostic Labs follow at 27%, driven by 34% increase in outsourced genomic testing demand. Pharma Companies hold 18%, focusing on drug development pipelines and biomarker-based trial optimization, while Research Institutes account for 9%, primarily contributing to early-stage genomic innovation. The fastest growth is seen in Diagnostic Labs due to rising outsourcing trends and 29% increase in demand for rapid sequencing services. Hospitals remain the established demand anchor, while pharma companies are shifting toward data-driven trial ecosystems. Companies are targeting hospitals with integrated platforms and labs with high-throughput sequencing solutions to capture efficiency gains of nearly 23%.

“According to a 2025 report by a global healthcare analytics authority, adoption among Diagnostic Labs increased by 33%, with over 2,800 laboratories implementing high-throughput genomic sequencing systems, leading to a 26% improvement in processing efficiency, indicating a strong shift in demand dynamics.”

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.4% between 2026 and 2033.

Europe holds around 27% share, driven by strong research-led adoption, while Asia-Pacific contributes nearly 25% with rapid clinical scaling and infrastructure expansion. South America accounts for 6%, and Middle East & Africa collectively represent 4%, reflecting emerging-stage adoption. Demand is concentrated in North America due to advanced genomic integration, while acceleration is strongest in Asia-Pacific due to large-scale sequencing deployments and cost-efficient healthcare expansion. Europe leads in regulatory-driven precision innovation, while emerging regions are gradually increasing access through digital health partnerships. A structural shift is visible as cross-border genomic data collaboration increases, reducing dependency on localized datasets by nearly 19%. Globally, companies are prioritizing North America for revenue stability, Asia-Pacific for scale expansion, and Europe for compliance-led innovation ecosystems.

How is precision healthcare transforming treatment delivery systems across advanced medical economies?

North America holds nearly 38% market share, driven by strong integration of genomics, AI diagnostics, and biomarker-based oncology treatment systems. Demand is concentrated in the United States, where over 72% of major hospitals deploy AI-assisted genomic interpretation tools, improving diagnostic accuracy by 31%. A key structural force is tightening genomic data governance, reshaping clinical trial design and increasing compliance-driven investment. Digital transformation is accelerating, with over 55% of healthcare providers adopting cloud-based precision medicine platforms. Around 18% expansion in sequencing infrastructure capacity has strengthened clinical throughput. Enterprises are prioritizing automation-led diagnostics and predictive analytics adoption to reduce operational delays and improve patient stratification efficiency. The region’s high capital investment and early technology adoption make it a preferred expansion hub, reinforcing long-term strategic dominance for firms targeting advanced precision healthcare ecosystems.

Why is regulatory alignment reshaping precision healthcare adoption across European healthcare systems?

Europe accounts for nearly 27% of the market, led by Germany, the UK, and France, where precision diagnostics adoption exceeds 61% in oncology care pathways. Strict regulatory frameworks on genetic data privacy and ESG compliance are driving structured adoption, with 22% higher validation timelines compared to other regions. However, this regulatory intensity is forcing companies to develop compliance-first AI diagnostic systems, improving data accuracy by 19%. Nearly 48% of hospitals are integrating standardized genomic databases to align with cross-border health protocols. Strategic investments in research-led sequencing platforms have increased by 16%, enhancing early-stage innovation output. Healthcare providers prioritize quality assurance and clinical validation over speed, making Europe a compliance-driven innovation hub where companies must adapt systems to regulatory precision rather than scale-first expansion.

What is driving large-scale genomic adoption across rapidly digitizing healthcare ecosystems?

Asia-Pacific holds nearly 25% share but is the fastest-expanding regional market due to large-scale genomic infrastructure development and cost-efficient healthcare models. China, India, and Japan collectively contribute over 70% of regional demand, with hospital-based sequencing adoption increasing by 34%. A major advantage is localized production of diagnostic reagents, reducing dependency on imports by 21% and improving turnaround efficiency. Digital hospital expansion has enabled 58% integration of AI-based diagnostic systems across tier-1 healthcare centers. Companies are aggressively scaling manufacturing and cloud-health platforms to support high-volume testing. Patient preference for cost-effective precision diagnostics is accelerating adoption, especially in oncology and infectious disease management. The region’s scale-driven ecosystem makes it critical for global expansion strategies focused on high-volume, low-cost precision healthcare deployment.

How is rising healthcare modernization influencing precision medicine adoption in cost-sensitive regions?

South America contributes around 6% of the market, with Brazil and Argentina leading adoption due to expanding oncology care infrastructure. Hospital-based precision diagnostics usage has increased by 17%, driven by rising chronic disease burden and improving healthcare access. However, limited genomic infrastructure and high import dependency constrain scalability, affecting nearly 28% of advanced diagnostic availability. Despite this, localized healthcare reforms are improving sequencing access, with 14% growth in private-sector diagnostic investments. Companies are introducing cost-optimized genomic testing models to address price-sensitive demand patterns. Adoption remains uneven, with urban centers driving nearly 65% of regional usage. The region represents a balanced opportunity-risk environment where demand is growing, but infrastructure gaps require strategic partnerships and localized investment models for sustainable expansion.

Why is healthcare modernization accelerating precision medicine adoption in emerging infrastructure-driven economies?

Middle East & Africa holds nearly 4% market share, with the UAE, Saudi Arabia, and South Africa leading adoption through healthcare modernization programs. Hospital digitalization has increased by 23%, enabling broader integration of genomic diagnostics in specialty care centers. Demand is largely driven by government-led healthcare transformation initiatives and rising investment in advanced oncology systems. However, infrastructure limitations restrict widespread sequencing adoption, impacting nearly 31% of rural healthcare coverage. Despite this, strategic partnerships with global biotech firms have increased precision medicine deployment capacity by 18%. Enterprises are focusing on turnkey diagnostic solutions and mobile sequencing platforms to overcome accessibility gaps. The region is emerging as a transformation-driven market where investment-led healthcare expansion is creating new demand pockets for precision diagnostics adoption.

United States – 38% share: Strong AI-genomics integration and advanced oncology infrastructure drive dominant adoption.

China – 21% share: Rapid sequencing expansion and large-scale hospital digitization support high-volume precision diagnostics demand.

The personalized medicine market is highly competitive, dominated by global biotechnology leaders, diagnostic technology firms, and AI-health platform developers competing for control over genomic data ecosystems and precision diagnostics infrastructure. The top five players collectively hold nearly 52% of the market, reflecting moderate consolidation with strong innovation-led rivalry. Competition is primarily based on technology integration (34%), diagnostic speed and accuracy (27%), and scalable data infrastructure efficiency (19%), while supply chain control adds another 11% strategic advantage. Companies are actively expanding through AI-genomics partnerships, vertical integration of diagnostics and therapeutics, and cloud-based health platform development. A key competitive shift is the move from standalone diagnostic tools to end-to-end precision healthcare ecosystems. Entry barriers remain high due to regulatory complexity and infrastructure intensity, limiting new entrants. Winning in this market requires control over genomic datasets, AI interpretation capabilities, and scalable clinical integration networks.

Illumina Inc.

Thermo Fisher Scientific

Roche Holding AG

Pfizer Inc.

Novartis AG

Merck & Co. Inc.

AstraZeneca plc

Siemens Healthineers AG

BioNTech SE

Qiagen N.V.

Abbott Laboratories

Agilent Technologies Inc.

Guardant Health Inc.

Myriad Genetics Inc.

The personalized medicine market is being reshaped by AI-powered genomic interpretation systems and next-generation sequencing platforms that are now embedded in over 60% of advanced hospital networks. These current technologies are improving diagnostic efficiency by nearly 32% while reducing manual analysis dependency by 25%. Integration of multi-omics data platforms is also enabling faster biomarker identification, strengthening clinical decision accuracy and reducing treatment selection errors significantly across oncology workflows.

Emerging technologies such as CRISPR-based gene editing, digital twin modeling, and cloud-native precision health platforms are accelerating adoption across research and clinical environments. Digital twin systems are improving treatment simulation efficiency by up to 28% while reducing clinical trial iteration cycles by 22%. Around 45% of biotech firms are now integrating hybrid AI-genomics pipelines, enabling faster drug-response mapping and improving predictive accuracy in patient stratification.

Disruptive innovations are centered on decentralized sequencing devices and real-time genomic analytics, which are expected to redefine care delivery models between 2026 and 2028. Compared to legacy laboratory-based sequencing, new portable genomic systems improve processing speed by nearly 40% and reduce operational costs by 27%. Companies investing early in integrated AI-genomic ecosystems are gaining a clear competitive advantage through faster commercialization cycles and scalable precision diagnostics infrastructure.

March 2025 – Illumina Inc. expanded its NovaSeq X platform deployment across global genomics laboratories, increasing sequencing throughput by up to 2x and improving large-scale genomic processing efficiency. This expansion has strengthened oncology and rare disease research pipelines by reducing turnaround time by nearly 28%, enabling faster clinical decision-making and accelerating precision diagnostics workflows globally. [High-Throughput Expansion]

June 2024 – Roche strengthened its collaboration with Foundation Medicine to enhance companion diagnostics integration, enabling over 30% faster biomarker identification in oncology trials. The initiative has significantly improved treatment matching precision and reduced clinical validation timelines, increasing efficiency in targeted therapy development and reinforcing Roche’s position in precision oncology ecosystems. [Precision Diagnostics Push]

September 2025 – Thermo Fisher Scientific expanded its bioprocessing and genomic testing manufacturing capacity by approximately 20%, addressing rising global demand for personalized medicine solutions. This expansion has improved supply chain stability for sequencing reagents, reducing operational delays by nearly 18% and enhancing scalability across clinical and research applications. [Capacity Scaling]

January 2026 – Qiagen advanced its digital PCR and sample-to-insight workflow integration, improving molecular testing efficiency by nearly 35%. This development has enabled faster decentralized diagnostics adoption across hospital and laboratory networks, reducing manual processing dependency and strengthening real-time genomic analysis capabilities in precision medicine applications. [Workflow Acceleration]

The personalized medicine market report provides a comprehensive evaluation of segmentation across types, applications, end-users, technologies, and key geographic regions. It covers critical categories including genomic medicine, targeted therapy, precision diagnostics, and pharmacogenomics, along with application areas such as oncology, cardiology, neurology, rare diseases, and infectious diseases. End-user analysis includes hospitals, diagnostic laboratories, pharmaceutical companies, and research institutes, collectively representing over 90% of adoption distribution.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, capturing regional adoption disparities where North America leads with 38% share and Asia-Pacific shows nearly 31% faster technology absorption rates. It also evaluates technology integration trends such as AI-driven genomics, CRISPR applications, and cloud-based diagnostic ecosystems, which are increasingly shaping clinical workflows and improving efficiency by up to 30% in advanced systems.

Strategically, the report supports investment planning, expansion strategy, and competitive benchmarking by analyzing over 25+ key companies and multiple high-growth segments. It highlights emerging opportunities in decentralized diagnostics and AI-genomics convergence, where adoption is increasing by nearly 22%, providing decision-makers with actionable insights into future market positioning from 2026–2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 319006.53 Million |

|

Market Revenue in 2033 |

USD 729880.81 Million |

|

CAGR (2026 - 2033) |

10.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Illumina Inc., Thermo Fisher Scientific, Roche Holding AG, Pfizer Inc., Novartis AG, Merck & Co. Inc., AstraZeneca plc, Siemens Healthineers AG, BioNTech SE, Qiagen N.V., Abbott Laboratories, Agilent Technologies Inc., Guardant Health Inc., Myriad Genetics Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |