Reports

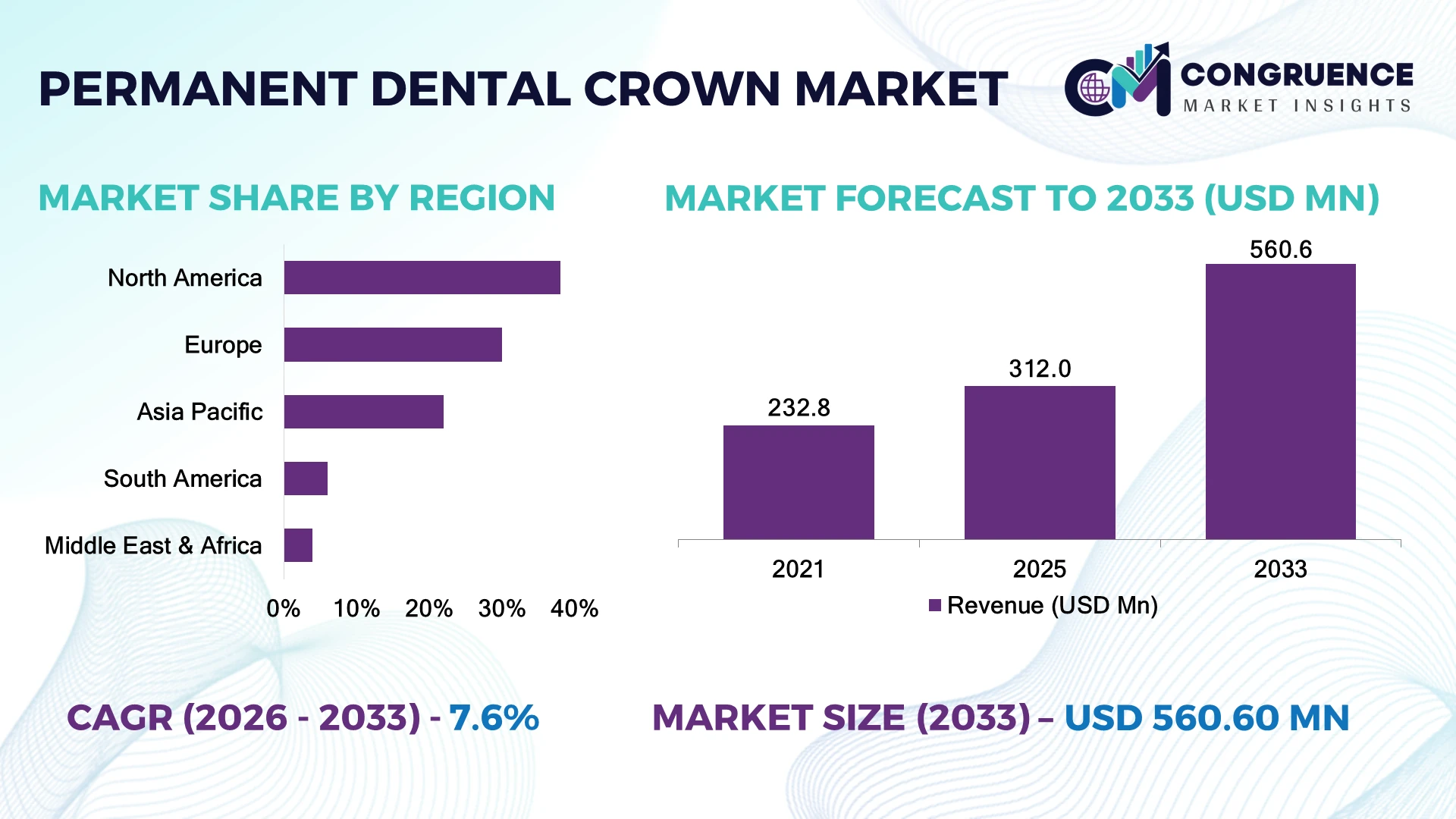

The Global Permanent Dental Crown Market was valued at USD 312 Million in 2025 and is anticipated to reach a value of USD 560.6 Million by 2033 expanding at a CAGR of 7.6% between 2026 and 2033. Growth is driven by rising adoption of CAD/CAM dental restoration systems, increasing preference for zirconia-based crowns, and expansion of digital dentistry workflows in clinics.

The United States accounted for nearly 35% of global permanent dental crown adoption in 2025, supported by advanced dental infrastructure, high cosmetic dentistry penetration, and investments in chairside milling technologies. Europe followed with strong ceramic crown utilization, while China expanded production capacity through domestic dental material manufacturing and digital dental laboratories. The U.S. dental technology sector recorded over 60% adoption of digital impression systems among advanced clinics, compared with lower penetration levels across emerging Asian markets.

The market landscape highlights a strategic shift toward digitally integrated, high-precision dental restoration ecosystems.

Market Size & Growth: Valued at USD 312 Million in 2025 and projected at USD 560.6 Million by 2033, supported by digital dentistry adoption and advanced ceramic material innovation.

Top Growth Drivers: Digital dentistry adoption (45%), zirconia crown preference (38%), and cosmetic dental procedures (32%) are key growth contributors.

Short-Term Forecast: By 2028, digital crown production workflows are expected to reduce fabrication time by 40% and improve fitting accuracy by 25%.

Emerging Technologies: AI-assisted dental design, CAD/CAM automation, and next-generation zirconia materials are transforming permanent crown manufacturing.

Regional Leaders: North America is projected at USD 210 Million, Europe at USD 165 Million, and Asia-Pacific at USD 140 Million, driven by technology adoption and expanding dental infrastructure.

Consumer/End-User Trends: Over 55% of dental patients increasingly prefer durable ceramic-based restorations for aesthetic and functional benefits.

Pilot/Case Example: In 2024, digital dentistry programs in advanced dental clinics reduced crown production turnaround time by 35% through automated design and milling.

Competitive Landscape: Leading companies including Dentsply Sirona, 3M, Ivoclar, Straumann, and Nobel Biocare maintain strong positions through material innovation and digital solutions.

Regulatory & ESG Impact: Sustainable dental manufacturing initiatives have improved material efficiency by nearly 20% through optimized production processes and reduced waste.

Investment & Funding: More than USD 500 Million in dental technology investments has supported digital laboratories, automation platforms, and advanced material development.

Innovation & Future Outlook: Next-generation biocompatible materials, AI-powered restoration planning, and integrated digital ecosystems are shaping future competitive strategies.

Permanent Dental Crown Market growth is increasingly concentrated around aesthetic restoration demand, digitally optimized treatment planning, and advanced biomaterial adoption. Zirconia and lithium disilicate crowns are gaining traction, with ceramic-based solutions representing over 60% of premium restoration preferences in developed markets. Recent supply-chain diversification across dental material producers and regional manufacturing hubs is improving availability and reducing dependency on limited suppliers, creating a stronger foundation for innovation-driven expansion.

The Permanent Dental Crown Market is becoming strategically important as dental providers shift toward precision-based restoration systems, supported by digital workflows, advanced materials, and patient expectations for durable aesthetic outcomes. Competition is increasingly influenced by manufacturers’ ability to integrate scanning, design, and automated production technologies into complete dental restoration ecosystems.

A major market shift is the restructuring of dental supply chains toward regional production centers and digitally connected laboratories. CAD/CAM crown manufacturing enables production cycles within hours compared with traditional multi-day laboratory processes, improving operational efficiency by nearly 50% while reducing manual adjustments. North America maintains leadership through high technology adoption and premium dental services, whereas Asia-Pacific is expanding rapidly through affordable dental care models and growing domestic manufacturing capabilities.

Dental laboratories and clinics are increasingly investing in intraoral scanners, automated milling systems, and material partnerships to improve workflow consistency. For example, digital crown production centers have enabled clinics to reduce patient visits from multiple appointments to same-day restoration procedures. Companies are prioritizing collaborations with dental technology providers and expanding manufacturing capabilities to strengthen market presence. Strategic positioning will depend on innovation speed, material quality, and the ability to deliver efficient digital restoration solutions.

The rapid adoption of digital dentistry platforms is the primary driver reshaping permanent dental crown manufacturing, with over 60% of advanced dental clinics in developed markets integrating digital impression technologies. CAD/CAM workflows reduce crown production cycles by nearly 50% compared with conventional laboratory methods, improving chairside efficiency and patient experience. The expansion of zirconia-based restoration systems has increased premium crown adoption by more than 35% in markets such as the United States and Germany. Companies are responding through investments in AI-assisted design platforms, automated milling partnerships, and integrated dental laboratory networks to strengthen precision restoration capabilities.

Permanent dental crown manufacturers face operational pressure from fluctuations in ceramic material costs, specialized equipment expenses, and dependence on advanced dental component suppliers. Zirconia and lithium disilicate materials account for more than 60% of premium crown applications, creating exposure to pricing instability and supply concentration. Countries including Japan and South Korea continue to rely on imported high-grade dental materials for advanced restoration systems, affecting production flexibility. Rising laboratory automation investments can increase initial setup costs by 25–40%, limiting adoption among smaller clinics. Companies are reducing exposure through localized manufacturing, multi-supplier contracts, and alternative biomaterial development strategies.

The integration of artificial intelligence, cloud-based dental design, and automated manufacturing creates new opportunities for permanent dental crown providers. AI-enabled restoration planning can improve design consistency by approximately 30% while reducing manual workflow requirements in dental laboratories. Emerging markets such as India and Brazil are expanding digital dental infrastructure, with private clinics increasingly adopting intraoral scanners and automated fabrication systems. Regulatory acceptance of digitally manufactured dental devices is supporting wider commercialization of advanced restoration technologies. Companies are positioning through R&D investments, software partnerships, and ecosystem development to capture demand for customized, faster, and more predictable crown solutions.

Long-term market expansion faces challenges related to digital workflow standardization, skilled technician shortages, and integration complexity between dental software and manufacturing systems. Nearly 40% of smaller dental laboratories continue operating with partially manual processes, creating consistency issues in high-volume crown production. Countries such as the United States and China are experiencing increasing demand for trained CAD/CAM specialists to support advanced restoration workflows. Differences in regulatory requirements and technology infrastructure also affect cross-border deployment of digital dental solutions. Companies must address these barriers through workforce training programs, interoperable platforms, and strategic partnerships to ensure reliable production quality and scalable operations.

AI Dental Design Adoption: AI-powered crown design platforms are gaining traction as dental laboratories integrate automated workflows, reducing design adjustments by nearly 30% and improving production consistency by 20%. Advanced clinics in the United States are combining intraoral scanning with cloud-based design systems, while manufacturers are expanding software partnerships to streamline restoration development and reduce technician dependency.

Zirconia Material Transition: Premium zirconia crowns are replacing traditional restoration materials, with adoption increasing by more than 35% in cosmetic dentistry applications due to higher durability and improved aesthetics. Dental manufacturers are scaling high-translucency zirconia production as clinics prioritize longer-lasting solutions. Supply-chain restructuring in Europe and Asia is improving access to specialized ceramic materials.

Chairside Manufacturing Growth: Same-day crown production is expanding as clinics deploy compact milling machines and digital fabrication systems, cutting patient visits by approximately 40% and reducing manual laboratory coordination. Dental groups in Japan and South Korea are accelerating chairside technology investments, creating demand for integrated scanner-to-milling ecosystems and automated workflow platforms.

Sustainable Dental Production: Dental manufacturers are adopting material optimization and waste-reduction processes, achieving approximately 15–20% improvements in production efficiency. Regulatory pressure on medical manufacturing sustainability is encouraging companies to redesign supply chains, localize production, and improve resource utilization. A non-obvious shift is the growing focus on digital inventory management to reduce unused dental material losses.

Zirconia crowns represent the leading type segment, accounting for approximately 45% of the permanent dental crown market due to superior strength, aesthetic performance, and compatibility with digital manufacturing systems. Their high fracture resistance and reduced maintenance requirements have increased adoption among premium dental clinics in the United States, Germany, and Japan. Porcelain-fused-to-metal crowns maintain relevance with nearly 30% share, supported by established clinical familiarity and cost advantages, particularly in price-sensitive markets. Lithium disilicate crowns are the fastest-growing type segment, expanding through demand for natural appearance and minimally invasive cosmetic procedures. Adoption has increased by more than 25% among aesthetic dentistry providers as digital workflows improve precision. Companies are increasing investments in advanced ceramic formulations, automated processing, and partnerships with dental laboratories to capture shifting preferences toward high-performance restoration materials.

Dental clinics represent the leading application segment, contributing approximately 55% of permanent dental crown demand due to high procedure volumes, cosmetic dentistry expansion, and direct patient access. Clinics increasingly integrate intraoral scanners, CAD/CAM systems, and automated milling equipment, reducing treatment turnaround times by nearly 40%. Dental laboratories remain a critical application area with around 30% share, supporting complex manufacturing and customized restoration production. Hospitals and specialized dental centers represent the fastest-growing application segment as healthcare systems expand advanced oral care capabilities. Adoption is increasing by approximately 20% as hospitals invest in integrated dental units and precision restoration technologies. Companies are responding by developing scalable digital platforms, expanding laboratory partnerships, and creating workflow solutions tailored for high-volume dental providers.

Private dental practices account for approximately 60% of permanent dental crown adoption due to higher cosmetic dentistry demand, faster technology adoption, and greater investment flexibility. These providers increasingly deploy digital scanning and chairside restoration systems, improving patient throughput by nearly 35%. Dental hospitals and academic institutions maintain a significant role with around 25% share, supporting complex procedures, training, and advanced clinical research. Dental service organizations represent the fastest-growing end-user category, expanding as consolidated dental networks invest in standardized technology platforms and centralized procurement. Adoption among these groups is rising by more than 30% as operators seek consistent restoration quality and operational efficiency across multiple locations. Companies are targeting this segment through customized software solutions, equipment partnerships, and bundled technology offerings.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2026 and 2033.

North America holds a dominant position in the permanent dental crown market, supported by advanced dental infrastructure, high cosmetic dentistry penetration, and widespread adoption of CAD/CAM restoration systems. The region contributes approximately 38% of global demand, with the United States representing the largest share through strong private dental networks and technology-driven clinics. More than 60% of advanced dental practices in the U.S. have adopted digital impression workflows, improving restoration accuracy and production speed. Companies are expanding through partnerships between dental technology providers and laboratories while increasing investments in AI-enabled design platforms and chairside manufacturing systems to strengthen operational efficiency.

United States Market Outlook: The United States remains the key market due to its large private dental practice ecosystem, advanced healthcare infrastructure, and high adoption of cosmetic restoration procedures. Over 70% of premium dental clinics utilize digital treatment planning tools, supporting demand for zirconia and digitally fabricated crowns. Manufacturers are focusing on domestic production capabilities, software integration, and technology partnerships to improve restoration workflows.

Europe maintains a strong position in the permanent dental crown market due to established dental technology infrastructure, high-quality healthcare systems, and strong demand for aesthetic restoration solutions. Countries including Germany, Switzerland, and Italy contribute significantly through advanced dental laboratories and ceramic material manufacturing capabilities. The region accounts for approximately 30% of market demand, with zirconia and lithium disilicate crowns gaining preference among premium dental providers. Nearly 55% of dental laboratories in leading European markets use digital fabrication technologies to improve customization and workflow efficiency. Companies are strengthening regional production networks and investing in sustainable manufacturing practices to comply with evolving medical device and environmental standards.

Germany Market Outlook: Germany leads European dental innovation through advanced laboratory networks, precision manufacturing capabilities, and strong adoption of digital dental equipment. Around 65% of specialized dental laboratories have integrated CAD/CAM technologies, supporting faster crown fabrication and improved consistency. Domestic manufacturers are expanding material development and automation capabilities to maintain competitiveness in premium restoration solutions.

Asia-Pacific represents the fastest-transforming market for permanent dental crowns, driven by expanding dental infrastructure, increasing private clinic investments, and rising adoption of digital restoration technologies. The region contributes approximately 22% of global demand and benefits from large-scale dental manufacturing capabilities in China, Japan, and South Korea. China has strengthened its dental material production ecosystem, while India is experiencing rapid growth in private dental chains and affordable restorative care models. Digital dentistry adoption among advanced clinics has increased by more than 30% across major urban centers. Companies are expanding manufacturing capacity, forming technology partnerships, and developing cost-efficient crown solutions to address diverse healthcare markets.

China Market Outlook: China holds strategic importance through its growing dental manufacturing base, domestic material production, and expanding healthcare technology investments. The country has increased adoption of automated dental laboratories, with digital workflows implemented across more than 40% of advanced urban dental facilities. Manufacturers are improving supply-chain localization and scaling production of ceramic-based restoration products.

South America is developing as an emerging permanent dental crown market, supported by expanding private dental services, increasing cosmetic dentistry awareness, and modernization of clinical infrastructure. Brazil represents the largest contributor due to its extensive dental professional network and growing investment in aesthetic procedures. The region accounts for approximately 6% of global demand, with urban dental centers increasingly adopting digital scanning and restoration technologies. Around 25% of advanced clinics in major cities have introduced digital workflow solutions, although equipment costs and technology access remain challenges. Companies are addressing market barriers through localized distribution partnerships, affordable product portfolios, and collaborations with dental laboratories.

Brazil Market Outlook: Brazil remains the leading South American market due to its large dental services sector and strong cosmetic dentistry demand. The country has more than 300,000 dental professionals, creating a significant customer base for crown manufacturers and technology providers. Companies are expanding local partnerships and improving access to digitally manufactured restoration solutions.

The Middle East & Africa market is experiencing gradual transformation through healthcare modernization programs, private hospital expansion, and investments in advanced dental services. Countries such as the United Arab Emirates and Saudi Arabia are increasing adoption of digital dental equipment through premium healthcare facilities and medical tourism initiatives. The region contributes approximately 4% of global demand, with private clinics representing the primary adoption channel. Over 35% of leading dental centers in Gulf countries have introduced digital scanning and advanced restoration workflows. Companies are targeting the region through distribution partnerships, localized service networks, and investments in technology-enabled dental care infrastructure.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as a strategic market due to healthcare infrastructure investments, private clinic expansion, and government-backed healthcare modernization initiatives. Dental facilities in major cities are increasingly adopting digital treatment systems, with more than 30% of advanced clinics integrating automated restoration technologies. Companies are strengthening regional partnerships to support long-term market penetration.

The Permanent Dental Crown Market features global technology leaders such as Dentsply Sirona, Straumann, Ivoclar, and 3M competing against regional ceramic manufacturers and dental laboratory specialists. The top five players collectively account for approximately 45% of market activity, competing through digital workflows, material innovation, supply reliability, and customization. Premium manufacturers focus on zirconia performance, CAD/CAM integration, and automation, while regional players compete through pricing, localized production, and faster delivery. Around 60% of leading clinics prioritize digital compatibility, and nearly 40% of purchasing decisions are influenced by workflow speed. Companies are expanding through laboratory partnerships, software integration, and vertical technology ecosystems. The competitive shift is moving from traditional crown manufacturing toward connected dentistry platforms, creating higher entry barriers around intellectual property, clinical validation, and digital infrastructure. Winning requires combining advanced materials, scalable production, and seamless digital restoration capabilities.

Ivoclar Vivadent

Straumann Group

3M Oral Care

Zimmer Biomet

Henry Schein

GC Corporation

Kuraray Noritake Dental

VITA Zahnfabrik

Coltene Group

Shofu Dental

Amann Girrbach

3Shape

Align Technology

Digital dentistry technologies are reshaping permanent crown production through CAD/CAM systems, intraoral scanners, and cloud-based design platforms. Advanced scanning workflows improve restoration accuracy by approximately 25–30% compared with conventional impressions, while automated milling reduces fabrication time by nearly 40%. More than half of advanced dental clinics in developed markets are integrating digital workflows, creating advantages in speed, customization, and patient experience.

Artificial intelligence is becoming a key technology layer for crown design optimization, automated margin detection, and treatment planning. AI-assisted systems reduce manual design adjustments by around 30% and improve workflow consistency for laboratories handling high restoration volumes. Companies benefiting most are technology-integrated manufacturers combining materials, software, and equipment ecosystems.

Between 2026 and 2028, disruptive technologies including cloud dentistry platforms, robotic manufacturing, and AI-generated crown proposals will accelerate workflow transformation. Compared with traditional manual fabrication, digitally connected systems provide faster turnaround, improved quality control, and stronger scalability. Companies investing in interoperable platforms and automated production networks are positioned to gain competitive advantages as dental providers prioritize efficiency and precision.

March 2025 — Dentsply Sirona introduced expanded connected dentistry solutions at IDS 2025, highlighting AI-enhanced workflows and cloud-based dental platforms. The company showcased Primescan 2 and DS Core integrations designed to improve digital restoration efficiency. Source: www.dentsplysirona.com

January 2026 — Dentsply Sirona and Benco Dental expanded their partnership to distribute connected dental technology solutions across the United States. The collaboration added CEREC systems and digital manufacturing tools, strengthening access to integrated crown production workflows. Source: www.investors.dentsplysirona.com

2025 — Straumann accelerated digital ecosystem development through its AXS cloud platform strategy, integrating hardware, software, and service capabilities. The company reported that Asia-Pacific sales represented more than 20% of business activity, supporting regional expansion initiatives. Source: www.reuters.com

2025 — Dentsply Sirona marked 40 years of CEREC innovation, reporting that more than 7 million crowns are milled annually through CEREC milling machines. The milestone reinforced chairside manufacturing adoption and strengthened single-visit restoration workflows.

The Permanent Dental Crown Market Report evaluates industry dynamics across major types including zirconia crowns, porcelain-fused-to-metal crowns, lithium disilicate crowns, and other advanced restoration materials. The analysis covers applications such as dental clinics, laboratories, hospitals, and specialized dental centers, along with end-users including private practices, dental service organizations, and healthcare institutions across North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

The report examines digital dentistry adoption, CAD/CAM workflows, AI-assisted design, advanced ceramic technologies, and automated manufacturing trends shaping market transformation. With coverage of leading companies, competitive positioning, supply-chain developments, and emerging technology opportunities, the study supports investment planning, expansion decisions, partnership strategies, and long-term positioning between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 312 Million |

| Market Revenue (2033) | USD 560.6 Million |

| CAGR (2026–2033) | 7.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Dentsply Sirona; Ivoclar Vivadent; Straumann Group; 3M Oral Care; Zimmer Biomet; Henry Schein; GC Corporation; Kuraray Noritake Dental; VITA Zahnfabrik; Coltene Group; Shofu Dental; Amann Girrbach; 3Shape; Align Technology |

| Customization & Pricing | Available on Request (10% Customization Free) |