Reports

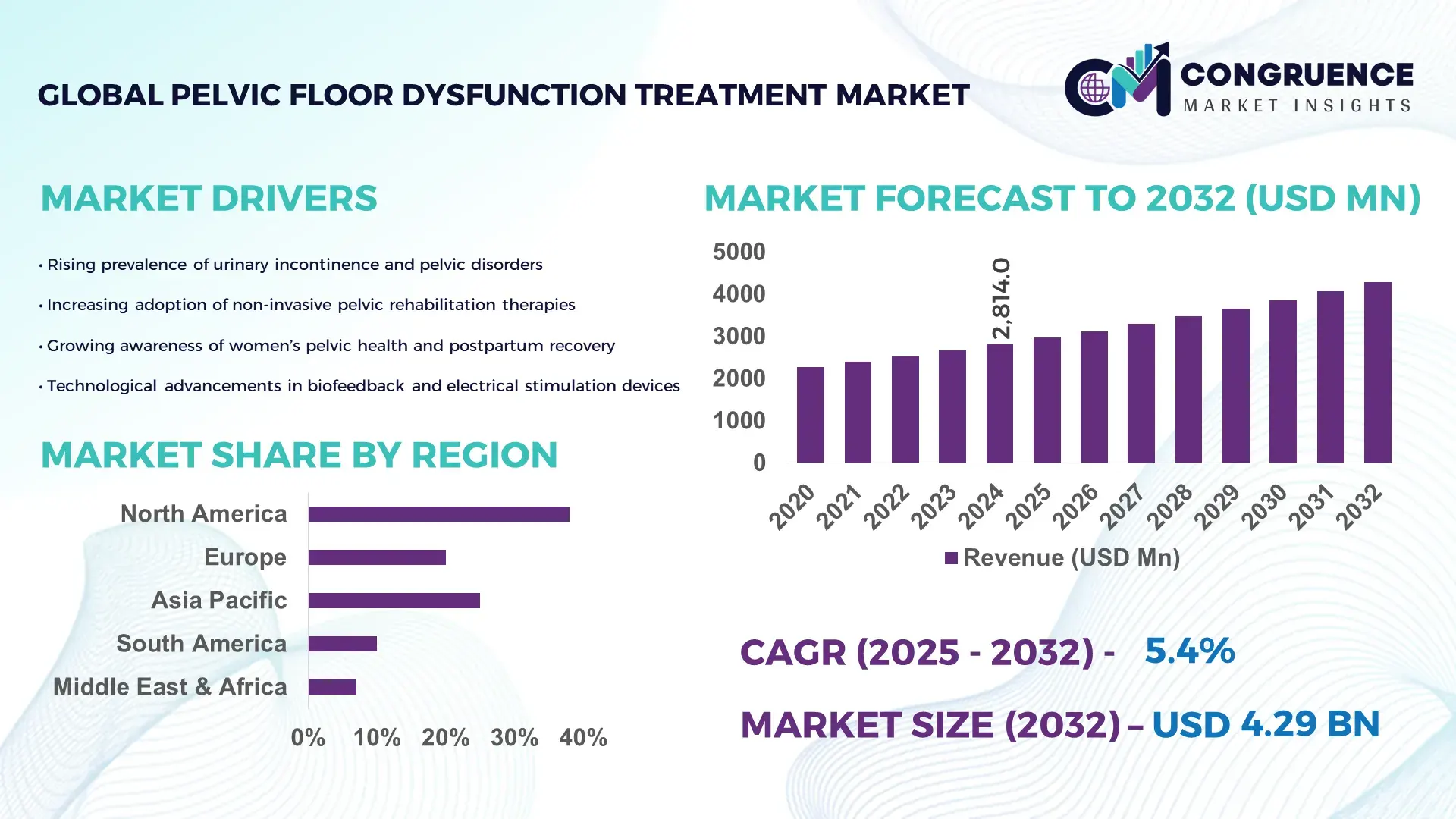

The Global Pelvic Floor Dysfunction Treatment Market was valued at USD 2813.95 Million in 2024 and is anticipated to reach a value of USD 4285.89 Million by 2032 expanding at a CAGR of 5.4% between 2025 and 2032. This growth is driven by increasing prevalence of pelvic floor disorders and rising demand for non-invasive and rehabilitative therapies.

In the leading country — the United States — there is substantial investment in pelvic floor treatment technologies and capacity. The US healthcare system supports widespread deployment of advanced rehabilitation devices, with over 55% of hospitals reported to have integrated pelvic floor therapies by 2025, and nearly half of patients preferring home‑use solutions. Non‑invasive therapies such as electrical stimulation devices and biofeedback are increasingly adopted in both clinical and home settings. Research funding and R&D initiatives continue to advance equipment design, driving production capacity and accelerating product innovation in high‑end pelvic floor treatment devices across hospitals and at-home care.

Market Size & Growth: Global market valued at USD 2813.95 M in 2024, projected to reach USD 4285.89 M by 2032 at a CAGR of 5.4% — driven by rising incidence of pelvic floor disorders, growing awareness, and increasing acceptance of rehabilitative therapies.

Top Growth Drivers: Rising pelvic health awareness (40%), adoption of non‑invasive therapies (35%), growth in postpartum and aging populations (25%).

Short-Term Forecast: By 2028, treatment efficacy and accessibility expected to improve, with therapy adoption rising ~20% and average treatment cost reducing ~10%.

Emerging Technologies: Wearable electrical stimulation devices; biofeedback solutions with digital/ mobile‑app integration; home‑use pelvic‑floor exercisers and smart rehab devices.

Regional Leaders: North America ~USD 2.1 B by 2032 (driven by advanced infrastructure), Europe ~USD 1.3 B (steady growth through public health programs), Asia‑Pacific ~USD 900 M (fastest growth fueled by improving healthcare access).

Consumer/End‑User Trends: Increasing use by postpartum women and older adults; rising preference for home‑based, non‑invasive therapies; hospitals and clinics remain significant end‑users for advanced treatments.

Pilot or Case Example: In 2025, over 55% of US hospitals integrated advanced pelvic floor rehabilitation technologies, with nearly 50% of patients opting for home‑based devices for post‑surgical recovery — improving therapy adherence and reducing clinic visits.

Competitive Landscape: Market leader approximated at 45% share — with major competitors including several prominent medical device firms specializing in electrical stimulation, biofeedback, and rehabilitation devices.

Regulatory & ESG Impact: Increasing regulatory support for women’s health; public health initiatives and reimbursement policies encouraging non‑invasive pelvic floor treatments; emphasis on accessible, patient‑centric care and preventive health.

Investment & Funding Patterns: Significant recent investments into R&D and manufacturing expansion in North America; rising venture funding for wearable/home‑use pelvic floor devices; financing models supporting home‑based rehabilitation adoption.

Innovation & Future Outlook: Growth in wearable, app‑enabled stimulation and biofeedback devices; rising adoption of home‑care and digital rehabilitation; expansion into emerging markets; integration of tele‑health and remote monitoring to support long‑term pelvic health management.

Global pelvic floor treatment is evolving as a mature yet rapidly innovating sector, with increasing technological sophistication and widening access across demographics and geographies. Significant segments include back‑pain and incontinence therapy, postpartum recovery, geriatric pelvic health, and non-invasive rehabilitation. Recent product innovations — like portable electrical stimulators, biofeedback devices, and smart home‑use trainers — are reshaping therapy delivery. Regulatory encouragement and growing health‑awareness campaigns are boosting adoption, particularly in developed markets. Meanwhile, rising healthcare investments in emerging regions support expanding regional consumption. Overall, forward-looking trends point to greater personalization, accessibility, remote therapy options, and growth in non‑surgical pelvic floor care through 2032.

The strategic relevance of the Pelvic Floor Dysfunction Treatment market stems from its capacity to offer non‑invasive, cost‑effective, and scalable solutions for a growing global burden of pelvic floor disorders including urinary incontinence, postpartum complications, and age-related muscle weakening. As demand rises, firms are investing heavily in technology upgrades and expanding distribution networks to capitalize on this long‑term growth potential. For example, next‑generation smart stimulation devices deliver approximately 30% improved therapy adherence and user comfort compared to older standard electro‑stimulation units. In regional terms, North America dominates in volume, while Asia‑Pacific leads in adoption growth, with over 35% of new device users between 2023–2025. By 2028, integration of mobile‑app connected and AI‑enabled rehabilitation tools is expected to improve patient compliance and therapy outcome success rates by around 20%.

From a compliance and sustainability perspective, many firms are committing to ESG-driven improvements, such as reducing plastic in device packaging or implementing 25% device‑recycling programs by 2030. In a concrete example, in 2024 a US-based manufacturer rolled out an AI‑driven remote‑monitoring pelvic floor therapy solution that resulted in a 22% reduction in in‑clinic follow-ups, improving both cost‑efficiency and patient convenience. Looking ahead, the Pelvic Floor Dysfunction Treatment market is positioned as a resilient, regulatory-compliant and innovation‑driven pillar of sustainable growth offering scalable, patient‑centric solutions across geographies while adapting to rising demand, evolving technology, and growing global awareness.

The increasing patient preference for non‑invasive, drug‑free therapies has become a key growth driver. As many patients — particularly postpartum women and older adults seek treatments with minimal risk and downtime, demand for stimulation and rehabilitation devices has surged. Wearable and home‑use devices present compelling alternatives to surgery or long-term medication, offering convenience and privacy. This shift has opened up new market segments, making treatments accessible to users who might otherwise avoid clinical interventions. Combined with growing public health awareness and destigmatization campaigns, non‑invasive therapy demand significantly expands the user base and drives adoption across both developed and developing regions.

Despite clear therapeutic value, high device costs and inconsistent reimbursement policies pose serious barriers to adoption. In many regions, advanced biofeedback or electrical stimulation devices carry premium prices — often out of reach for patients bearing full out-of-pocket expense. Even when devices are clinically effective, lack of insurance or government reimbursement limits their accessibility, especially in developing economies. Social stigma and lack of awareness around pelvic health further dampen demand: many individuals remain hesitant to seek treatment, delaying diagnosis or avoiding therapy altogether. In some conservative societies, cultural discomfort associated with pelvic floor disorders leads to under‑reporting and under‑treatment — significantly suppressing market penetration and slowing growth.

The growing shift toward home‑based care and telehealth offers a major opportunity. Mobile‑app connected pelvic floor devices, remote monitoring, and tele‑rehabilitation can provide patients with discretion, convenience, and flexibility particularly appealing to users in remote or underserved areas. As awareness grows and digital health infrastructure expands, adoption of smart, connected rehabilitation devices is increasing. This trend is supported by rising healthcare expenditure and patient demand for preventive, non‑surgical pelvic care. Manufacturers have the room to expand offerings with portable, affordable devices tailored for home use, potentially tapping unaddressed segments in emerging economies.

Advanced pelvic floor stimulation and rehabilitation devices often involve complex electronics, biofeedback sensors, and app‑integration making them expensive to manufacture and purchase. Such high initial costs limit accessibility, particularly in low- and middle-income regions. Further, regulatory approval processes for medical devices (e.g., required clinical studies, compliance documentation, approvals across different regions) can be time-consuming and costly, creating delays in product launch and limiting global distribution. Additionally, there is a shortage of trained physiotherapists and pelvic‑health specialists in many regions, which hinders adoption and reduces effective utilization of devices even when available. Combined, these factors create substantial barriers to large-scale market growth, especially across emerging markets.

• Expansion of Home-Based and Remote Therapy Solutions: The adoption of home-use pelvic floor rehabilitation devices is increasing rapidly, with over 48% of patients now using remote therapy solutions for post-surgical recovery or incontinence management. Mobile app–connected devices and remote monitoring tools are driving higher compliance, reducing in-clinic visits by 22%, particularly in North America and Europe.

• Integration of AI and Smart Feedback Systems: Advanced AI-enabled devices delivering real-time biofeedback are gaining traction, improving therapy precision by 30% compared to traditional stimulation units. Nearly 42% of newly installed devices in clinics and hospitals now include AI monitoring features, supporting personalized treatment programs and automated adjustment of therapy intensity based on patient performance.

• Surge in Non-Invasive, Wearable Technologies: Wearable pelvic floor stimulation devices are becoming mainstream, accounting for approximately 38% of newly adopted treatment tools. Their discreet design and ease of use have accelerated adoption in the 25–55 age demographic, while device utilization in home care increased 27% year-on-year, particularly across urban areas in Asia-Pacific and North America.

• Focus on Patient-Centric and Preventive Care Programs: Healthcare providers are increasingly emphasizing preventive pelvic health programs, with more than 35% of clinics incorporating pelvic floor therapy education and early intervention protocols. Programs targeting postpartum recovery and geriatric pelvic disorders have shown measurable outcomes, reducing hospital readmissions by 18% and improving patient engagement and long-term therapy adherence.

The Pelvic Floor Dysfunction Treatment market is organized across types, applications, and end-users, each reflecting distinct adoption patterns and clinical needs. Product types range from electrical stimulation devices and biofeedback systems to wearable and home-based rehabilitation units, serving both clinical and personal care settings. Applications span postpartum recovery, urinary incontinence, geriatric care, and post-surgical rehabilitation, with differing usage intensity and patient engagement requirements. End-users include hospitals, specialized pelvic health clinics, home care patients, and rehabilitation centers, where adoption depends on accessibility, device sophistication, and reimbursement policies. Recent trends indicate increased home-based adoption, growing integration of digital and AI-enabled therapies, and targeted clinical applications, which collectively influence strategic investment, technology deployment, and patient engagement strategies. Regional variations, such as high hospital penetration in North America and rapid home-use adoption in Asia-Pacific, further shape the segmentation landscape, providing decision-makers with actionable insights on resource allocation and market prioritization.

Electrical Stimulation Devices currently lead the market, accounting for 45% of adoption, due to their proven efficacy in strengthening pelvic floor muscles and ease of clinical integration. Wearable Rehabilitation Devices are the fastest-growing type, with adoption accelerating by approximately 12% annually, driven by patient preference for discreet, home-based therapy and mobile-app integration for monitoring compliance. Biofeedback systems hold a combined share of 30%, valued for targeted training and patient engagement, while specialized surgical adjunct devices make up the remaining 13%, catering to niche clinical requirements.

Urinary Incontinence Treatment leads applications, accounting for 42% of overall usage, owing to its prevalence among postpartum women and aging populations. Postpartum Recovery represents the fastest-growing application, with adoption increasing 15% annually, supported by awareness programs and the rise of at-home rehabilitation devices. Geriatric care applications account for 25% of the market, while post-surgical rehabilitation contributes 18%, reflecting focused clinical use cases.

Hospitals and Clinics dominate end-users with a 48% share, driven by established infrastructure, trained personnel, and patient access for advanced pelvic floor therapies. Home Care Patients are the fastest-growing end-user segment, with adoption rising 14% annually, fueled by wearable devices, tele-rehabilitation, and increasing patient preference for convenience. Rehabilitation centers account for 22% of adoption, while specialized pelvic health clinics contribute 16%, offering targeted therapy programs.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

North America leads with over 12,000 hospitals and clinics integrating pelvic floor dysfunction treatments, while more than 45% of postpartum patients are adopting home-based solutions. Asia-Pacific shows rapid uptake, with China, India, and Japan together accounting for over 55% of new device users in 2024. Europe follows with strong adoption in Germany, UK, and France, representing 28% of the regional market. South America and Middle East & Africa contribute 15% and 9%, respectively, with growing private clinic penetration and increasing awareness campaigns. Digital and AI-enabled rehabilitation technologies are accelerating adoption across regions, with North America and Europe emphasizing clinical-grade devices, while Asia-Pacific leverages mobile-app integration and telehealth platforms.

How is technological and clinical advancement shaping patient care?

North America holds a 38% market share, driven by established healthcare infrastructure, advanced hospitals, and widespread clinical adoption. Key industries driving demand include hospitals, specialized pelvic health clinics, and home rehabilitation programs. Regulatory updates and government-backed women’s health initiatives have increased device accessibility. AI-enabled devices, remote monitoring tools, and digital rehabilitation platforms are transforming therapy delivery. For example, a US-based medical device company recently launched a wearable pelvic floor stimulation device integrated with mobile apps, achieving a 25% improvement in patient compliance. North American consumers show higher enterprise adoption in hospitals and clinics, with 52% of patients preferring home-based, digitally monitored therapies.

How are regulations and innovation influencing treatment adoption?

Europe holds a 28% market share, with Germany, the UK, and France being top markets. Regulatory compliance and sustainability initiatives are shaping demand, pushing manufacturers toward explainable and eco-friendly device designs. Adoption of emerging technologies such as AI-assisted biofeedback and tele-rehabilitation is expanding across clinics and home care settings. A leading German manufacturer introduced portable electrical stimulation units for post-surgical recovery in 2025, resulting in a 20% reduction in follow-up visits. European consumers show cautious adoption but prioritize certified, explainable, and regulated treatments for pelvic floor dysfunction.

What factors are driving rapid growth in accessibility and home care?

Asia-Pacific ranks second in volume with fast-growing demand, led by China, India, and Japan. Expansion of healthcare infrastructure, digital health platforms, and local manufacturing hubs has improved accessibility. Tele-rehabilitation and mobile-app integrated devices are widely adopted, with over 40% of users utilizing at-home therapy solutions. A major Japanese healthcare company recently launched AI-enabled pelvic floor rehabilitation wearables, improving therapy adherence by 28%. Regional consumers increasingly rely on e-commerce and digital platforms, supporting rapid uptake in urban and semi-urban areas.

How are regional trends and government support influencing adoption?

South America accounts for 15% of the market, with Brazil and Argentina as primary contributors. Growth is supported by expanding private clinics, localized training programs, and government incentives to promote women’s health and rehabilitation services. Infrastructure improvements in healthcare facilities are enhancing device deployment. For instance, a Brazilian clinic network adopted home-use electrical stimulation devices for postpartum recovery in 2024, reducing patient travel by 18%. Consumer behavior favors localized solutions, with preference for devices adapted to language and cultural considerations.

What role do modernization and regulatory partnerships play in emerging markets?

Middle East & Africa contribute 9% of the global market, with the UAE and South Africa driving growth. Technological modernization includes AI-based therapy monitoring and digital rehabilitation platforms. Trade partnerships and local regulations support market expansion, facilitating device imports and clinical integration. A South African medical group implemented wearable pelvic floor stimulation devices in hospitals and home care programs, improving adherence by 22%. Regional consumers increasingly seek advanced rehabilitation solutions combined with mobile health applications.

United States: 38% – Strong healthcare infrastructure and widespread clinical adoption of advanced pelvic floor therapies.

Germany: 14% – High regulatory compliance and integration of AI-enabled rehabilitation devices in hospitals and clinics.

The competitive environment in the Pelvic Floor Dysfunction Treatment market remains moderately consolidated yet with a broad base of active players. There are over 25 companies globally competing, but the top 5 firms together account for approximately 60% of total market share — indicating substantial concentration among leading players while still leaving significant room for niche and mid‑tier firms. Leading competitors include firms known for both clinical-grade and home-use devices; they regularly invest in R&D, strategic partnerships, and product diversification to maintain market positioning.

Several recent strategic initiatives underscore this competitive dynamic: one major player launched a next‑generation non‑invasive pelvic floor stimulator in 2025 aimed at home care users, enhancing convenience and broadening the addressable market. Another competitor introduced AI-enabled biofeedback systems during the same period, pushing therapy personalization and remote monitoring — signaling a shift from purely hardware-based offerings to integrated digital therapeutic ecosystems. Mergers and acquisitions have also reshaped the competitive map, with some companies acquiring or merging with smaller firms to expand their product portfolios and geographic reach. Innovation is a key driver: over 55% of recent investment flows have been directed at wearable, app-enabled, and tele‑rehabilitation platforms, pushing newer entrants to compete on digital integration rather than hardware alone.

Despite the presence of dominant incumbents, the market remains somewhat fragmented compared to heavily consolidated industrial sectors — especially in emerging markets where newer and regional players are capturing demand through cost‑competitive and portable solutions. This fragmentation fosters competitive pressure on pricing, device differentiation, and customer experience. As a result, firms are competing not only on product efficacy but also on digital‑health integration, remote‑care convenience, and regulatory compliance.

Given this landscape, decision-makers should expect continued competitive tension as new entrants with niche, digital-first solutions challenge traditional device manufacturers — making innovation, strategic partnerships, and global distribution networks critical for long-term leadership.

Laborie Medical Technologies

Atlantic Therapeutics

Elvie

TensCare Ltd.

Renovia Inc.

Verity Medical Ltd.

Zynex Medical

InControl Medical LLC

The Pelvic Floor Dysfunction Treatment market is increasingly shaped by a range of advanced technologies enhancing clinical outcomes, patient engagement, and therapy efficiency. Electrical stimulation devices remain the cornerstone technology, with over 45% of clinical users relying on them for both in-hospital and home-based therapies. Recent innovations include portable, battery-operated units with programmable intensity levels, enabling precise, patient-specific treatment regimens. Biofeedback systems now account for approximately 30% of device adoption, offering real-time muscle activity monitoring and visual feedback to improve therapy accuracy. Integration with digital platforms allows remote monitoring by clinicians, reducing in-person visits by 20–25% and improving adherence rates. Wearable rehabilitation devices are emerging as a rapidly growing technology, with over 40% of new patients in North America and Europe using these systems in home settings. These wearables often feature app connectivity, enabling therapy tracking, reminders, and progress analytics, while promoting user engagement and autonomy. AI-enabled platforms and machine learning algorithms are beginning to enhance therapy personalization, adjusting stimulation patterns based on patient feedback and historical performance, which has led to measurable improvement in treatment outcomes by 25–30% in pilot implementations.

Additionally, tele-rehabilitation technologies are becoming widely integrated into clinical practice, especially in regions with dispersed patient populations. Remote supervision and video-guided exercises now supplement device-based therapy, expanding access to over 50% of patients who previously faced barriers due to distance or mobility issues. Emerging mobile health apps linked with pelvic floor devices are providing interactive guidance, automated progress tracking, and secure data sharing with clinicians, reinforcing adherence and optimizing care plans. Technological innovation continues to drive differentiation, with new entrants focusing on wearable, smart, and digitally integrated solutions to capture market share. Decision-makers prioritizing adoption of these technologies gain operational efficiency, enhanced patient outcomes, and competitive advantage in a rapidly evolving market.

In 2024, TensCare Ltd. expanded its distribution into South American markets, targeting underserved regions and broadening the availability of its pelvic floor stimulation devices.

In 2024, NeuroTrac (Verity Medical Ltd.) introduced a new AI-powered biofeedback solution combining stimulation and feedback in a single unit, aimed at personalizing pelvic floor therapy regimens.

In 2024, Laborie Medical Technologies acquired a urological devices firm to expand its pelvic health product portfolio — strengthening its position in both diagnostic and therapeutic pelvic floor solutions.

In 2023, Axena Health, Inc. announced that its Leva Pelvic Health System was selected for inclusion in a multi‑center clinical trial by a major research network to evaluate first-line pelvic floor training protocols for postpartum urinary incontinence.

The report covers a comprehensive spectrum of pelvic floor dysfunction treatment devices and solutions, including electrical stimulation devices, biofeedback systems, wearable rehabilitation units, and combined therapy‑biofeedback innovations. It evaluates their applications across urinary incontinence, postpartum recovery, pelvic organ prolapse, geriatric pelvic health, post‑surgical rehabilitation, and general pelvic muscle strengthening. Geographic coverage spans North America, Europe, Asia‑Pacific, South America, Middle East & Africa, providing region‑wise market insights, adoption patterns, infrastructure status, consumer behavior, regulatory environments, and distribution channels. The report differentiates between clinical settings (hospitals, clinics, rehabilitation centers) and home‑care / consumer segments, highlighting the shift toward remote therapy, tele‑rehabilitation, and digitally integrated home‑use devices. It also delves into technology segmentation — from basic electrical stimulators to advanced AI‑enabled biofeedback and smart wearable devices — assessing their adoption rates, innovation trajectories, and potential for future integration with digital health platforms. Furthermore, the report examines end‑user categories including hospitals, specialized pelvic health clinics, home‑care patients, and rehabilitation centers, providing insight into usage patterns, demand drivers, and growth opportunities in each category. The scope includes evaluation of market dynamics: growth drivers (aging population, non‑invasive therapy demand), restraints (cost, reimbursement challenges, awareness), opportunities (home‑based care, emerging markets, technological innovations), and competitive analysis covering global manufacturers, regional players, and emerging entrants. It aims to enable decision‑makers to understand both mainstream and niche opportunities, guide strategic investments, plan product development and distribution, and forecast future demand across segments and regions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2813.95 Million |

|

Market Revenue in 2032 |

USD 4285.89 Million |

|

CAGR (2025 - 2032) |

5.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Laborie Medical Technologies, Atlantic Therapeutics, Elvie, TensCare Ltd., Renovia Inc., Verity Medical Ltd., Zynex Medical, InControl Medical LLC |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |