Reports

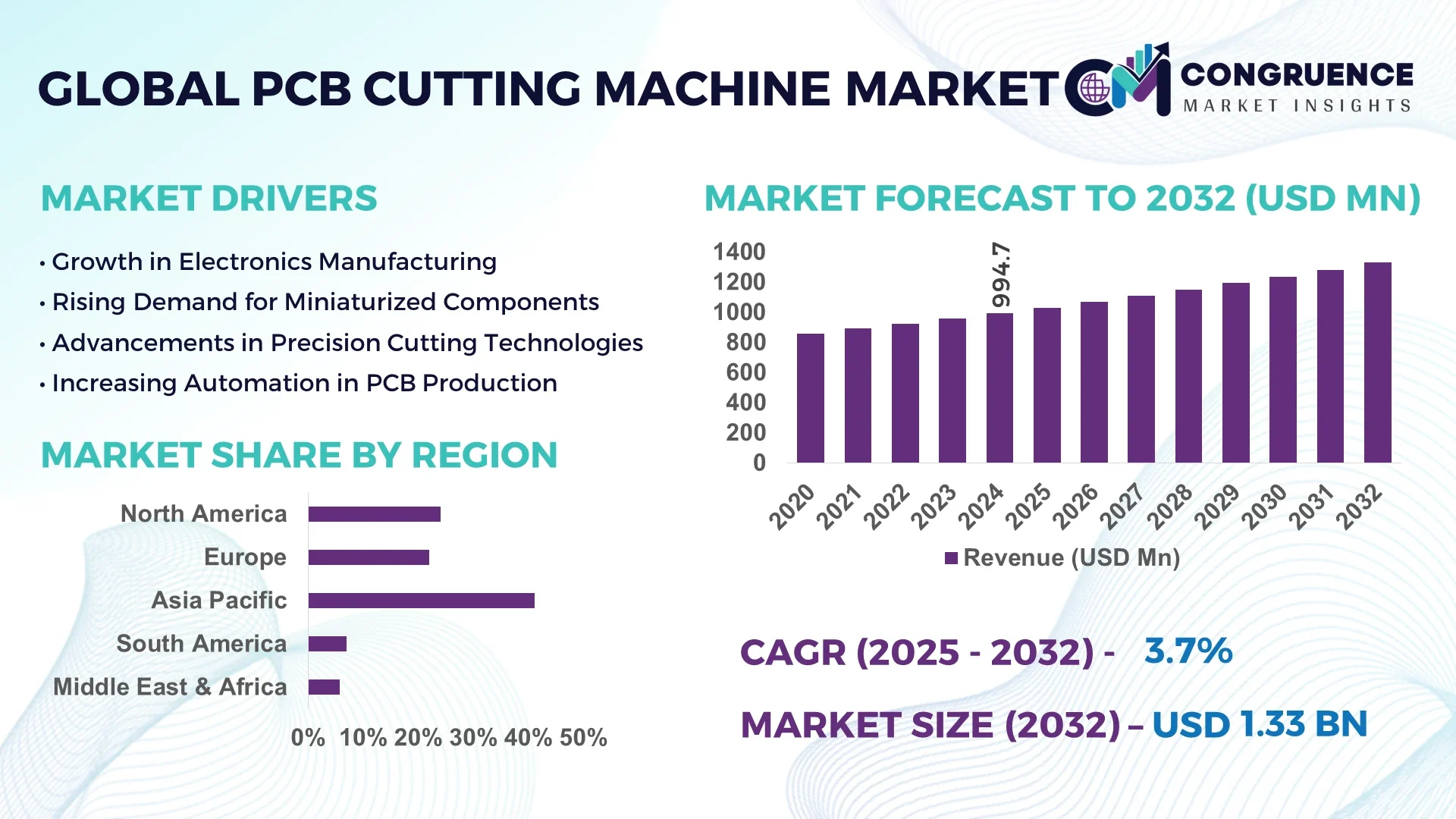

The Global PCB Cutting Machine Market was valued at USD 994.7 Million in 2024 and is anticipated to reach a value of USD 1,330.2 Million by 2032, expanding at a CAGR of 3.7% between 2025 and 2032.

China dominates the global PCB Cutting Machine Market, accounting for more than 50% of worldwide production, thanks to its strong electronics manufacturing sector and extensive automation in PCB assembly lines.

The PCB Cutting Machine Market is experiencing steady growth due to rising demand in consumer electronics, automotive electronics, and telecommunications sectors. The demand for high-precision, automated PCB cutting systems has surged, especially in industries where microelectronics and miniaturized components are critical. Laser-based PCB cutting machines are replacing traditional routing machines, offering 30% better accuracy and reducing operational defects. Automated PCB cutting machines are now integrated with inline inspection systems, improving throughput by 25% and minimizing production errors. Additionally, the surge in 5G technology and wearable devices is fueling investments in precision cutting equipment. Key manufacturers are expanding product lines to include low-vibration, dust-free PCB cutting solutions, further expanding their footprint across North America, Europe, and Asia-Pacific. The PCB Cutting Machine Market is expected to witness high-volume adoption in industries requiring fast, clean, and contactless cutting technology.

Artificial Intelligence is rapidly transforming the PCB Cutting Machine Market by integrating real-time data analysis, predictive maintenance, and autonomous calibration systems. AI-enabled PCB cutting machines optimize blade movement, reduce mechanical stress, and extend machine life by over 20%. Machine learning algorithms monitor cutting patterns and adjust cutting speed and pressure in milliseconds, enhancing cut quality by over 35%. In smart manufacturing units, AI-driven PCB cutting systems have reduced human intervention by up to 40%, allowing for faster production with minimal downtime. Computer vision integrated with AI helps detect defects on PCBs post-cutting, increasing inspection accuracy to more than 98%.

AI is also enabling seamless integration of PCB cutting machines with Industry 4.0 ecosystems. These smart systems automatically adapt to design changes and support batch-size-one manufacturing, critical for customized electronics. AI-based monitoring helps forecast tool wear and prevent breakdowns, lowering maintenance costs by up to 25%. With rising demand for precision and efficiency, AI is streamlining production and ensuring consistent quality in mass manufacturing environments. The PCB Cutting Machine Market is increasingly dependent on AI technologies to meet the evolving demands of high-speed, ultra-fine electronic production processes, making AI integration not a choice but a necessity.

“In March 2024, a major Japanese electronics manufacturer integrated an AI-powered control system into its high-speed PCB cutting machines, enabling real-time defect prediction and cutting-path optimization. The upgrade led to a 22% improvement in throughput and a 31% reduction in PCB material wastage within the first quarter of implementation.”

The PCB Cutting Machine Market is undergoing significant shifts influenced by technological innovation, automation, and the ever-expanding demand from the electronics manufacturing sector. As consumer electronics, automotive systems, and smart devices become more compact and complex, the need for advanced PCB cutting machines is surging. Automation, precision control, and AI integration are now at the forefront of market growth. In response, manufacturers are investing in high-speed laser cutting systems, robotic PCB depaneling solutions, and real-time defect detection to meet industry demands. However, the market also faces limitations such as high equipment costs and operational training challenges, which hinder adoption among small manufacturers.

The proliferation of smart devices, wearables, and IoT-based electronics has led to a significant increase in the production of compact and high-density PCBs, boosting the PCB Cutting Machine Market. Miniaturized electronics require ultra-precise and clean cutting technologies, pushing manufacturers to shift from traditional mechanical cutting to laser and router-based depaneling systems. Laser PCB cutting machines offer up to 35% higher accuracy and zero mechanical stress, which is crucial for microelectronics. As devices become smaller, multi-layered, and complex in design, the demand for dust-free, low-vibration, and high-speed cutting tools is growing rapidly. Industry-wide transitions to high-performance computing, 5G, and semiconductor packaging are further accelerating adoption rates for advanced PCB cutting machines globally.

One of the key restraints impacting the PCB Cutting Machine Market is the high capital investment required for acquiring state-of-the-art equipment. Advanced PCB laser depaneling machines, for instance, can cost 2x to 3x more than traditional routing systems, making them less accessible to small and mid-sized manufacturers. Additionally, these machines require routine calibration, laser safety protocols, and skilled technicians to operate efficiently. The lack of trained personnel limits machine optimization and increases production downtimes. For many companies, long return on investment (ROI) periods deter them from upgrading older machinery. Furthermore, maintenance of high-precision equipment involves regular parts replacement and software updates, contributing to increased operational expenses and complexity.

The growing focus on Industry 4.0 and smart manufacturing presents significant opportunities in the PCB Cutting Machine Market. IoT-integrated PCB cutting systems equipped with AI and real-time analytics are revolutionizing production lines by enabling predictive maintenance, automated adjustments, and adaptive control. Manufacturers integrating AI-powered systems have reported up to 25% reduction in cutting errors and 30% improvement in production throughput. Smart PCB cutting machines can automatically recognize board types, adjust cutting speeds, and even forecast tool wear, increasing overall efficiency. As more factories transition to connected environments, the demand for intelligent, data-driven, and remotely accessible cutting equipment is expected to soar, especially in high-volume sectors like consumer electronics and automotive PCB manufacturing.

A major challenge in the PCB Cutting Machine Market is ensuring compliance with strict safety and material-handling regulations. As cutting technologies evolve—especially with the use of laser and UV-based systems—companies must comply with health, environmental, and workplace safety norms. Laser cutting, for example, can generate harmful fumes and particulates that require advanced filtration systems, adding to equipment costs. Additionally, newer PCBs use a wide variety of materials, including flexible substrates, ceramic composites, and high-frequency laminates, which demand customized cutting parameters and tooling. Misalignment or improper configuration may damage the board or cause production loss. Adapting machines to handle diverse materials while maintaining safety and quality remains a significant operational challenge for manufacturers.

The PCB Cutting Machine Market is segmented based on machine type, application, and end-user industries. Different types of cutting machines cater to various needs depending on the complexity of the circuit, volume of production, and board material. Applications range from mobile phone manufacturing to industrial equipment production, each requiring varying degrees of cutting precision. End-users include contract electronics manufacturers, in-house OEMs, and research labs. The increasing demand for ultra-compact, multi-functional electronic products is fueling innovation across all three segments. As high-precision cutting becomes standard, especially in sectors like automotive and medical electronics, market segmentation continues to evolve with differentiated technology deployment.

The PCB Cutting Machine Market includes major types such as Laser PCB Cutting Machines, Router PCB Cutting Machines, Saw PCB Cutting Machines, Die Cutting Machines, and UV Cutting Machines. Among these, Laser PCB Cutting Machines dominate the market due to their non-contact cutting ability, superior edge quality, and adaptability to high-density, multilayered boards. Laser machines account for over 35% of total installations globally and are most prevalent in East Asia’s electronics production hubs. The fastest-growing segment is UV Cutting Machines, especially for flexible and rigid-flex PCB processing. UV machines offer high precision with minimal thermal impact, making them ideal for sensitive substrates. While Router PCB Cutting Machines continue to be popular in mid-volume manufacturing due to their affordability, Die Cutting Machines are now mostly limited to specific applications due to their lack of flexibility. Saw Cutting Machines, although reliable, are being gradually phased out in high-precision environments.

The PCB Cutting Machine Market finds application across Consumer Electronics, Automotive Electronics, Industrial Control Equipment, Medical Devices, and Telecommunication Infrastructure. Consumer Electronics remains the leading application segment, driven by high-volume production of smartphones, tablets, laptops, and wearables. This segment accounts for the highest number of machine installations, particularly in China, South Korea, and Vietnam. Automotive Electronics is the fastest-growing application area, fueled by the rise of electric vehicles (EVs), ADAS systems, and connected cars. The complexity of automotive PCBs and their safety-critical applications demand ultra-precise and reliable cutting methods. Medical Devices and Industrial Control Equipment segments are also seeing increased adoption of laser-based systems to meet stringent compliance and precision standards. Telecommunication Infrastructure applications are growing steadily, especially with the global deployment of 5G networks requiring high-performance and multilayer PCBs.

The key end-users in the PCB Cutting Machine Market are Electronics Manufacturing Services (EMS) Providers, OEMs (Original Equipment Manufacturers), Research & Development Labs, and Prototyping Studios. EMS Providers represent the largest share of the market due to their high production volumes and broad customer base across consumer electronics and industrial equipment sectors. These service providers are quick to adopt new cutting technologies like laser and UV systems to stay competitive and maintain production speed and accuracy. The fastest-growing end-user segment is OEMs, especially those involved in electric vehicles, telecom infrastructure, and medical electronics. These companies are increasingly investing in in-house cutting capabilities to improve supply chain control and product quality. R&D Labs and Prototyping Studios, while smaller in volume, require highly flexible cutting machines capable of handling diverse board types and one-off production runs. Their demand is driving innovations in software integration and machine versatility.

Asia-Pacific accounted for the largest market share at 41.2% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2025 and 2032.

Asia-Pacific’s dominance is driven by its strong base of electronics manufacturing hubs in China, Japan, South Korea, and Taiwan, where rapid PCB miniaturization and automation have led to increased adoption of high-precision cutting machines. The region benefits from a robust consumer electronics sector and supportive industrial policies. Meanwhile, North America is witnessing an accelerated shift toward domestic electronics manufacturing, especially in semiconductor packaging and electric vehicle PCBs, prompting investment in automated laser and UV cutting systems. Europe remains a key market due to its focus on green electronics and high-end automotive PCB production. The Middle East & Africa and South America are emerging as niche markets with increasing demand from medical electronics and industrial control sectors.

Rising Integration of UV Laser Systems in High-End Manufacturing

The North American PCB Cutting Machine Market is being propelled by rising investments in high-performance electronics manufacturing, especially in the U.S. and Canada. UV laser cutting machines are being widely adopted for advanced PCB applications, particularly in 5G infrastructure, aerospace, and medical device sectors. In 2024, the U.S. alone accounted for over 68% of the regional market share. Demand for precision cutting has surged with the growth of electric vehicle component production. Manufacturers are also focusing on reshoring PCB manufacturing to reduce global supply chain dependence. Additionally, several semiconductor assembly plants under construction in North America are expected to further boost the need for automated PCB cutting equipment over the coming years.

Automotive Electronics Fueling Precision PCB Cutting Demand

Europe's PCB Cutting Machine Market is being driven by the continent's robust automotive electronics industry, particularly in Germany, France, and Italy. Germany held over 32% of the regional market share in 2024, supported by the country’s leadership in electric vehicle innovation. The increasing complexity of in-vehicle electronics and ADAS components has created a strong demand for laser and router-based PCB cutting systems. Additionally, the region's growing preference for sustainable, low-emission manufacturing processes has pushed for eco-friendly machine variants with particulate filtration systems. Companies in the UK and Netherlands are also investing in smart manufacturing solutions, including AI-enabled cutting optimization to reduce material waste and improve board utilization.

Leads with Mass Electronics Manufacturing and Automation

Asia-Pacific continues to dominate the PCB Cutting Machine Market, driven by large-scale electronics manufacturing in countries like China, South Korea, Japan, and Taiwan. In 2024, China accounted for 46.7% of the region’s market share, followed by South Korea at 21.3%. The massive production of smartphones, computers, and LED lighting has fueled machine adoption in high-volume manufacturing setups. Laser-based and UV PCB cutting machines are in high demand due to the region’s transition to microelectronics and flexible circuit boards. Taiwan's semiconductor foundries and Japan's automation-driven electronics facilities are also contributing to market growth. Governments in this region are supporting machine automation through tax incentives and technology parks.

Growing Investments in Industrial Electronics and Automotive Production

South America is witnessing a gradual rise in demand for PCB Cutting Machines, largely led by Brazil and Argentina. Brazil dominated the regional market with 58.5% share in 2024, supported by increasing local manufacturing of white goods and automotive electronics. Argentina is following closely with a strong focus on industrial automation components and telecom infrastructure. Demand for laser cutting machines is gaining momentum, particularly in large OEM facilities where reliability and edge quality are critical. The region's economic incentives for domestic production are also encouraging investment in automated equipment, although the market remains price-sensitive and favors hybrid cutting technologies with flexible configurations.

Emerging Electronics Hubs Driving Entry-Level Machine Demand

The Middle East & Africa region is an emerging but promising market for PCB Cutting Machines. The UAE and South Africa are the leading countries in this region, with UAE holding 37.8% of the market share in 2024 due to its growing electronics assembly and consumer goods sector. South Africa follows with 29.4%, driven by demand in mining electronics, medical devices, and automotive components. The adoption of PCB cutting machines is being pushed by infrastructure digitization initiatives and localization of consumer electronics production. Entry-level router and laser machines dominate due to lower capital budgets. However, a shift toward more automated, dust-free machines is being observed in new facilities funded through government-backed industrial diversification projects.

China – 31.5% Market Share

China holds the highest market share due to its expansive electronics manufacturing ecosystem and large-scale PCB fabrication facilities catering to global demand.

United States – 18.7% Market Share

The U.S. ranks second, driven by significant investments in semiconductor packaging, defense electronics, and reshoring of PCB production to boost domestic supply chains.

The PCB Cutting Machine market is characterized by intense competition among key global players striving to enhance precision, productivity, and automation in their cutting systems. The market is fragmented, with several medium-sized companies competing alongside established multinational brands. Companies are heavily investing in the development of advanced blade and laser cutting technologies that ensure minimal damage to PCBs and high throughput. The demand for inline cutting solutions integrated with surface-mount technology (SMT) lines is rising significantly, prompting players to offer highly customizable and scalable machines.

Several companies have begun to emphasize the inclusion of robotic arms and AI-based fault detection features in PCB cutting equipment. Strategic partnerships and joint ventures are increasing in Asia-Pacific, especially China and Taiwan, as manufacturers aim to reduce cost pressures while maintaining international quality standards. With an increase in PCB miniaturization trends and consumer electronics innovation, players offering multi-functional and compact PCB cutting machines are witnessing strong market traction globally.

LPKF Laser & Electronics AG

ASYS Group

CAB Technology

Getech Automation

Juki Automation Systems

T-Tech Inc.

Sinmic Laser Technology Co., Ltd.

FKN Systek

Cencorp Corporation

HAKKO Corporation

Shenzhou Automation Equipment Co., Ltd.

In April 2024, LAPP launched the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

In June 2023, manufacturers began implementing AI-driven design tools in PCB prototyping, enhancing accuracy and efficiency. This integration led to a reduction in design errors by approximately 30%, streamlining the development process.

In September 2023, the industry saw a shift towards additive manufacturing techniques, allowing for the production of complex PCB designs with reduced material waste. This approach resulted in cost savings of up to 25% for manufacturers.

In December 2023, manufacturers introduced flexible PCBs, expanding applications in wearable technology and foldable devices. This innovation opened new avenues for product design and functionality.

The PCB Cutting Machine Market Report offers a detailed and comprehensive analysis of the global landscape of PCB separation technology. It encompasses various cutting methods including milling, laser cutting, punching, and V-groove systems, highlighting their role in improving production precision and throughput in printed circuit board (PCB) assembly processes. This report examines the impact of automation and smart manufacturing practices, where manufacturers are increasingly integrating robotic arms and AI-powered vision systems to enhance cut accuracy and reduce wastage in high-volume electronics production.

The market scope includes a close review of different machine configurations such as standalone and inline systems, used across industries like consumer electronics, automotive, aerospace, and telecommunications. Key geographical regions covered include North America, Europe, Asia-Pacific, South America, and Middle East & Africa, each analyzed in terms of installed capacity, number of electronics manufacturing units, and export-import trade in electronic components. The report also explores demand drivers like miniaturization of devices and the rise of high-speed internet and 5G technology, which require intricate and compact PCB designs.

Moreover, the report assesses raw material trends, cost structures, and supply chain dynamics impacting the PCB cutting ecosystem. End-user behavior, particularly in contract manufacturing and OEM sectors, is analyzed to project machine adoption trends and operational scale-up patterns across different tiers of the market.

Technological advancements in the PCB Cutting Machine market are rapidly reshaping the way printed circuit boards are handled in both prototyping and mass production environments. One of the most significant technological shifts is the adoption of laser depaneling machines over traditional mechanical routers. Laser systems offer high-precision cuts without mechanical stress, which is especially beneficial for sensitive or densely populated circuit boards used in smartphones, wearables, and automotive electronics.

Vision-based alignment systems have become more common in recent models, enabling real-time correction of alignment errors and ensuring higher product quality. Moreover, touch-screen human-machine interfaces (HMIs) are being integrated to enhance user experience and reduce training times. The integration of Internet of Things (IoT) sensors has enabled remote monitoring of equipment performance, predictive maintenance, and data analytics for operational efficiency.

The market is also witnessing a transition toward fully automatic inline cutting machines, which can be synchronized with SMT lines. These advanced systems are capable of handling high production volumes while maintaining consistent quality standards. Machines are now being equipped with dust extraction systems and anti-static features to meet the cleanliness and safety requirements of advanced electronics manufacturing. Overall, the evolution of PCB cutting technologies is geared toward reducing cycle time, enhancing cutting accuracy, and accommodating complex board layouts demanded by next-gen electronics.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 994.7 Million |

|

Market Revenue in 2032 |

USD 1,330.2 Million |

|

CAGR (2025 - 2032) |

3.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

LPKF Laser & Electronics AG, ASYS Group, CAB Technology, Getech Automation, Juki Automation Systems, T-Tech Inc., Sinmic Laser Technology Co., Ltd., FKN Systek, Cencorp Corporation, HAKKO Corporation, Shenzhou Automation Equipment Co., Ltd., MADPCB |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |