Reports

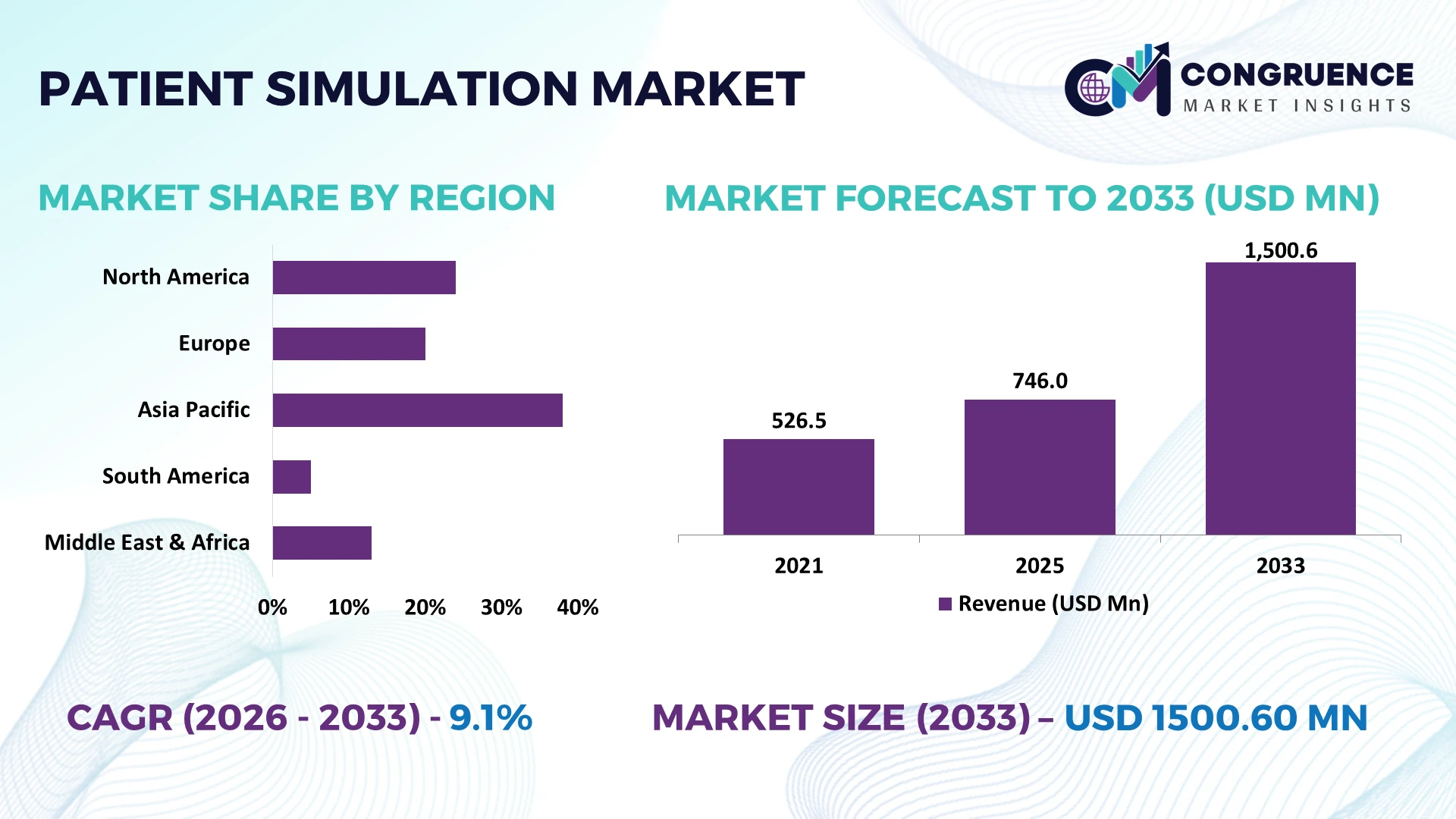

The Global Patient Simulation Market was valued at USD 745.95 Million in 2025 and is anticipated to reach a value of USD 1500.6 Million by 2033 expanding at a CAGR of 9.1% between 2026 and 2033. Growth is driven by expanding competency-based medical education, AI-enabled simulation platforms, and mandatory clinical skill validation across healthcare training institutions.

The United States leads the global Patient Simulation Market with an estimated share exceeding 38%, supported by multi-billion-dollar investments in healthcare education, more than 180 accredited medical schools, and widespread AI-enabled simulation deployment. Germany demonstrates faster integration across university hospitals through digital training initiatives, while North America maintains stronger adoption than Europe due to larger institutional funding. The 2026 expansion of healthcare workforce development programs further strengthens advanced simulation infrastructure.

Healthcare providers and technology companies should prioritize high-fidelity simulation ecosystems and digital learning partnerships in dominant regional markets to secure long-term competitive positioning.

Market Size & Growth: USD 745.95 Million (2025) is projected to reach USD 1500.6 Million by 2033 at a 9.1% CAGR, supported by AI-driven clinical education and expanding healthcare workforce development.

Top Growth Drivers: High-fidelity simulators (+31%), AI-assisted learning (+27%), and competency-based medical training (+24%) continue accelerating global market expansion.

Short-Term Forecast: By 2028, simulation-based training is expected to reduce practical assessment time by approximately 22% while improving learner proficiency by 18%.

Emerging Technologies: AI-powered virtual patients, mixed reality training, and cloud-connected simulation platforms improve assessment accuracy by nearly 30%.

Regional Leaders: North America exceeds USD 620 Million, Europe approaches USD 410 Million, and Asia-Pacific surpasses USD 330 Million through expanding digital medical education.

Consumer/End-User Trends: More than 68% of teaching hospitals increasingly integrate simulation into multidisciplinary clinical training and emergency preparedness programs.

Pilot/Case Example: In 2026, an advanced simulation deployment improved emergency response accuracy by 26% while reducing procedural errors by 19%.

Competitive Landscape: The leading supplier holds approximately 19% market share alongside major global manufacturers focused on integrated simulation ecosystems.

Regulatory & ESG Impact: Standardized competency frameworks improve certification consistency by over 20% while reducing material waste through digital simulation adoption.

Investment & Funding: More than USD 900 Million in strategic investments supports partnerships, regional expansion, and advanced healthcare education infrastructure amid supply chain localization.

Innovation & Future Outlook: AI analytics, digital twins, and interoperable simulation platforms strengthen personalized medical training and enterprise-wide clinical performance optimization.

Patient Simulation Market demand is expanding across medical schools, nursing education, military healthcare, emergency medicine, and hospital workforce training, supported by AI-enhanced scenario generation and immersive mixed reality platforms. More than 35% of newly deployed simulation systems now incorporate advanced performance analytics, while healthcare institutions increasingly prioritize localized manufacturing and resilient procurement strategies following recent global medical equipment supply-chain realignments, setting the stage for broader strategic market evaluation.

Patient simulation has become a strategic capability for healthcare systems seeking standardized clinical competency, faster workforce readiness, and lower training risk. Hospitals, universities, and defense medical organizations increasingly integrate advanced simulation into education and certification frameworks as digital healthcare infrastructure expands. The ongoing modernization of healthcare training facilities and stricter competency assessment requirements are reshaping procurement priorities, while localized manufacturing and diversified component sourcing reduce dependence on concentrated medical equipment supply chains.

High-fidelity AI-enabled simulation platforms complete scenario creation and learner assessment approximately 35% faster than conventional instructor-led systems while lowering recurring training resource consumption by nearly 25% through automated performance analytics. The United States maintains greater deployment scale across academic medical centers, whereas Japan emphasizes robotics-assisted simulation and aging-care training with higher technology integration per institution. Over the next two to three years, cloud-based simulation adoption is expected to exceed 55% among newly deployed enterprise training environments, supported by interoperable digital learning ecosystems.

A leading teaching hospital network deploying integrated simulation laboratories has improved multidisciplinary emergency preparedness while reducing repeated procedural training cycles through centralized digital assessment. In response, manufacturers are expanding software capabilities, forming partnerships with medical universities, and strengthening localized production to improve delivery resilience. Organizations that combine scalable simulation platforms with analytics-driven training workflows will secure stronger competitive positioning, operational efficiency, and long-term institutional partnerships.

Competency-based healthcare education is accelerating procurement of advanced patient simulation systems as institutions prioritize measurable clinical outcomes and standardized assessment. More than 62% of large teaching hospitals are expanding simulation-based training, while AI-assisted performance evaluation improves learner assessment consistency by nearly 28% and reduces instructor workload by approximately 24%. The United States continues integrating simulation into national workforce development initiatives, reinforcing demand for connected training infrastructure. In response, manufacturers are investing in cloud-enabled platforms, expanding strategic partnerships with medical universities, and introducing interoperable software ecosystems. A key strategic advantage lies in combining simulation hardware with analytics-driven learning platforms that increase customer retention and recurring institutional adoption.

Implementation remains constrained by high capital expenditure, interoperability challenges, and uneven digital infrastructure across healthcare institutions. Around 41% of mid-sized hospitals continue operating legacy training systems that require costly integration with modern simulation software, while implementation timelines can extend by nearly 30% due to compatibility testing. Germany and several emerging healthcare markets face procurement delays linked to specialized component availability and certification requirements. Companies are reducing operational exposure through localized assembly, standardized software interfaces, and long-term supplier agreements. Organizations capable of simplifying deployment while lowering integration complexity gain stronger scalability and procurement competitiveness.

Artificial intelligence, digital twins, and immersive mixed reality are creating new commercial opportunities beyond conventional simulation hardware. Adaptive learning algorithms improve individualized competency assessment by nearly 33%, while cloud-connected simulation environments reduce content update costs by approximately 20%. India is rapidly expanding digital medical education infrastructure through increased investment in healthcare training capacity, creating demand for scalable subscription-based simulation platforms. Companies are strengthening R&D, collaborating with software developers, and expanding ecosystem partnerships to deliver integrated education solutions. The emerging competitive advantage increasingly depends on combining intelligent analytics, remote accessibility, and continuous curriculum optimization within a unified digital platform.

Long-term market execution depends on securing skilled instructors, maintaining cybersecurity, and ensuring interoperability across increasingly connected simulation environments. Nearly 36% of healthcare organizations report shortages of certified simulation educators, while over 48% prioritize stronger cybersecurity controls for cloud-enabled training systems handling sensitive learner data. The United Kingdom continues expanding digital healthcare infrastructure, increasing expectations for secure and standardized simulation deployments. Companies must invest in workforce certification, resilient software architecture, and secure cloud infrastructure while strengthening partnerships with healthcare institutions. Organizations that successfully integrate cyber resilience with scalable training ecosystems will sustain operational consistency and preserve long-term competitive differentiation.

AI-Driven Skills Assessment Expansion AI-enabled assessment engines are reducing manual evaluation time by nearly 32% while improving competency scoring consistency by approximately 27%. Following healthcare workforce shortages, hospitals are embedding automated analytics into simulation workflows. Manufacturers are expanding cloud software capabilities and partnering with academic institutions to standardize performance measurement across distributed training environments.

Mixed Reality Training Integration Mixed reality adoption has increased by about 29%, while immersive procedure retention has improved by nearly 24% compared with conventional simulation sessions. Medical institutions in Japan are integrating extended reality into surgical education as digital infrastructure advances. Companies are restructuring product portfolios around modular software, wearable interfaces, and scalable enterprise deployment models to shorten implementation cycles.

Localized Manufacturing and Procurement Healthcare organizations are reducing dependence on imported simulation components, with localized sourcing improving delivery reliability by approximately 21% and procurement lead times falling by nearly 18%. Supply-chain diversification following recent logistics disruptions has encouraged manufacturers to establish regional assembly operations, strengthen supplier partnerships, and standardize components for faster enterprise deployment and lower operational risk.

Cloud-Connected Simulation Networks More than 57% of newly deployed enterprise simulation platforms support centralized cloud management, while collaborative multi-site training has expanded by approximately 26%. Teaching hospitals in the United States increasingly connect simulation laboratories through shared digital ecosystems, enabling standardized curricula, lower maintenance costs, and continuous software upgrades. Vendors are responding through subscription-based platforms, interoperability improvements, and long-term institutional partnerships.

Adult simulators remain the leading segment, accounting for approximately 42% of overall deployment due to their broad applicability across emergency medicine, internal medicine, critical care, and multidisciplinary clinical education. Their ability to integrate with AI-based assessment software and hospital learning management systems makes them the preferred investment for teaching hospitals and simulation centers. Pediatric simulation is the fastest-growing category, supported by increasing specialization in neonatal and pediatric critical care training, with institutional deployments rising by nearly 25%. Companies are expanding scenario libraries and introducing modular patient models to improve curriculum flexibility and reduce maintenance complexity.

Obstetric simulators continue gaining importance as healthcare providers prioritize maternal emergency preparedness, while surgical simulators benefit from growing demand for minimally invasive procedure training. Ultrasound simulation platforms are increasingly integrated into competency-based education, improving procedural confidence while reducing reliance on live patient practice. Manufacturers are expanding product portfolios through partnerships with medical educators and software developers, reflecting a clear shift toward integrated, specialty-focused simulation ecosystems with scalable digital capabilities.

Medical Training represents the largest application segment with an estimated 39% share, supported by mandatory competency development across medical schools and teaching hospitals. Standardized assessment requirements and integrated digital learning environments continue concentrating investment in this segment. Surgical Training is emerging as the fastest-growing application, driven by robotic surgery expansion, minimally invasive procedures, and simulation-first certification pathways. Training efficiency has improved by approximately 28%, while structured competency validation has reduced repeated practical sessions by nearly 20%. Vendors are scaling cloud-enabled learning platforms and expanding curriculum partnerships with healthcare institutions.

Nursing Education remains a major deployment area as workforce shortages increase demand for accelerated skills development. Emergency Care simulation continues expanding to strengthen multidisciplinary crisis response, while Clinical Assessment is becoming increasingly data-driven through automated performance analytics and standardized reporting. Companies are integrating simulation platforms with digital education ecosystems, enabling continuous learner tracking and enterprise-wide performance benchmarking across healthcare organizations.

Hospitals remain the dominant end-user, representing approximately 44% of total market demand due to continuous workforce training, accreditation requirements, and multidisciplinary clinical education. Large healthcare systems increasingly deploy integrated simulation laboratories supporting emergency response, surgical preparation, and competency validation. Simulation Centers are the fastest-growing end-user category, with annual deployment activity increasing by nearly 26% as institutions centralize advanced training resources and shared educational infrastructure. Suppliers are responding through customized enterprise platforms, flexible service agreements, and integrated analytics capabilities.

Medical Schools continue expanding simulation investments to support standardized clinical curricula, while Nursing Colleges strengthen practical learning capacity using scalable digital platforms. Military Healthcare remains strategically significant through trauma readiness and mission-specific medical preparedness programs requiring advanced procedural simulation. Companies are differentiating through institution-specific software customization, collaborative education partnerships, and subscription-based platform ecosystems, positioning themselves for sustained procurement opportunities across diverse healthcare training environments.

North America accounted for the largest market share at 39.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.8% between 2026 and 2033.

Advanced Clinical Training Infrastructure Driving Market Leadership

North America remains the largest regional market due to its mature healthcare education ecosystem, widespread deployment of high-fidelity simulation laboratories, and strong integration of digital competency assessment. The region represents nearly 40% of global installations, supported by teaching hospitals, military healthcare systems, and academic medical centers. AI-enabled simulation platforms continue replacing standalone training systems, improving learner assessment consistency and operational efficiency. Healthcare providers are expanding centralized simulation centers capable of supporting multidisciplinary education across multiple facilities. More than 65% of newly commissioned enterprise simulation environments now incorporate cloud-connected learning management capabilities, strengthening standardized workforce development. Vendors continue expanding software portfolios, service contracts, and institutional partnerships to reinforce long-term customer engagement while supporting continuous healthcare workforce modernization.

United States Market Outlook: The United States leads regional demand through its extensive network of accredited medical schools, integrated health systems, and advanced digital healthcare infrastructure. More than 180 medical schools and thousands of residency programs continue expanding simulation-based education to strengthen clinical competency and patient safety. Enterprise buyers increasingly prioritize AI-enabled assessment, cloud-connected training platforms, and specialty simulation solutions. Companies are reinforcing domestic service capabilities, expanding university collaborations, and investing in localized software development to improve implementation speed and long-term institutional support.

Healthcare Modernization Strengthening Simulation Adoption

Europe maintains a strong position through healthcare modernization initiatives, competency-based education standards, and widespread digital transformation across university hospitals. The region contributes approximately 28% of global market activity, with advanced simulation increasingly integrated into multidisciplinary medical education and clinical certification. Public healthcare investment supports expansion of centralized simulation facilities while encouraging interoperability across digital learning platforms. More than 58% of newly established training laboratories incorporate connected simulation technologies that enable standardized competency evaluation. Manufacturers are responding through localized product customization, software integration, and collaborative research partnerships designed to improve operational efficiency and institutional scalability.

Germany Market Outlook: Germany serves as the regional technology leader through its advanced hospital infrastructure, engineering expertise, and strong collaboration between healthcare providers and academic institutions. Large university medical centers continue investing in integrated simulation laboratories supporting emergency medicine, surgery, and critical care education. Approximately 60% of major teaching hospitals have expanded digital simulation capabilities, encouraging suppliers to strengthen enterprise partnerships, localized technical support, and software interoperability tailored to institutional requirements.

Rapid Healthcare Capacity Expansion Accelerates Deployment

Asia-Pacific represents the fastest-evolving regional market as healthcare capacity expansion, medical education reforms, and digital infrastructure investments reshape institutional training priorities. The region accounts for nearly 24% of global demand, supported by expanding medical schools, nursing institutions, and hospital modernization programs. Governments continue investing in workforce development, encouraging broader adoption of simulation-based competency assessment. Deployment of cloud-enabled simulation platforms has increased by approximately 30% across newly established training centers, improving educational consistency while reducing operating complexity. Manufacturers are expanding regional production, strengthening distribution partnerships, and adapting product portfolios to meet diverse institutional requirements.

China Market Outlook: China leads regional expansion through rapid healthcare infrastructure development, growing medical education capacity, and increasing domestic manufacturing capability. National investment in hospital modernization continues accelerating procurement of advanced simulation technologies across teaching hospitals and vocational medical institutions. More than 70% of newly developed provincial medical education projects include simulation-based clinical training components. Domestic manufacturers are increasing product innovation while international suppliers strengthen joint ventures and localized production to improve market responsiveness.

Institutional Modernization Supporting Clinical Training

South America is steadily expanding simulation adoption as healthcare institutions modernize professional training and strengthen clinical education quality. The region contributes close to 5% of global demand, supported by investments in university hospitals and specialized healthcare education centers. Simulation deployment increasingly focuses on emergency medicine, nursing education, and surgical preparedness where standardized competency assessment improves workforce readiness. Institutional partnerships have expanded simulation laboratory capacity by approximately 18% across leading healthcare education networks. Companies continue improving market access through distributor partnerships, localized technical services, and modular product offerings suited to varying institutional budgets while addressing infrastructure limitations.

Brazil Market Outlook: Brazil remains the largest national market due to its extensive healthcare network, expanding medical education sector, and ongoing investment in professional workforce development. Major teaching hospitals continue integrating simulation into residency and specialist training programs, while private healthcare groups increase adoption of digital assessment technologies. Approximately half of newly upgraded academic medical centers now incorporate advanced simulation facilities, encouraging suppliers to expand local service operations and long-term institutional collaborations.

Healthcare Investment Transforming Training Ecosystems

The Middle East & Africa market is advancing through healthcare infrastructure modernization, workforce localization strategies, and expanding investment in medical education. Regional governments continue prioritizing advanced clinical training to improve healthcare quality and reduce dependence on overseas education programs. Approximately 16% more healthcare institutions introduced structured simulation programs during recent modernization initiatives, while new academic hospitals increasingly incorporate integrated simulation laboratories into campus development. Technology providers are expanding regional partnerships, professional training services, and localized implementation support to strengthen long-term deployment efficiency and operational sustainability across emerging healthcare systems.

Saudi Arabia Market Outlook: Saudi Arabia leads regional development through large-scale healthcare transformation initiatives, investment in academic medical centers, and expansion of specialized healthcare workforce programs. New hospital developments increasingly integrate dedicated simulation facilities supporting multidisciplinary education and competency assessment. More than 40% of recently commissioned tertiary healthcare projects include advanced clinical simulation infrastructure. Companies are strengthening strategic partnerships with universities, expanding local technical support capabilities, and introducing enterprise-wide simulation ecosystems aligned with national healthcare modernization priorities.

The Patient Simulation Market is led by Laerdal Medical, CAE Healthcare, Gaumard Scientific, Limbs & Things, and Kyoto Kagaku, with global technology leaders competing against regional simulation manufacturers and specialized training solution providers. The top five companies collectively control approximately 61% of the market through integrated hardware, software, and clinical content ecosystems. Competition centers on simulation fidelity, AI-enabled assessment, interoperability, and deployment speed rather than pricing alone. AI-supported performance analytics improve training efficiency by nearly 30%, while cloud-enabled platforms reduce software maintenance effort by approximately 22% and modular product architectures shorten deployment cycles by around 18%. Leading vendors strengthen market positions through university partnerships, healthcare network agreements, localized manufacturing, and expansion of subscription-based software services. Regional suppliers compete through lower implementation costs and customized simulation scenarios tailored to national curricula. The competitive shift favors integrated digital ecosystems over standalone simulators, increasing pressure on vendors lacking software capabilities. Success depends on scalable platforms, clinical partnerships, rapid innovation, and seamless enterprise integration.

Laerdal Medical

CAE Healthcare

Gaumard Scientific

Limbs & Things

Kyoto Kagaku

3B Scientific

Simulab Corporation

Surgical Science

Mentice AB

VirtaMed AG

Intelligent Ultrasound Group

TruCorp

Operative Experience Inc.

Advanced patient simulation technology is shifting from standalone hardware toward connected digital ecosystems that combine artificial intelligence, cloud computing, immersive visualization, and automated competency analytics. AI-powered evaluation engines reduce instructor assessment time by approximately 32% while improving scoring consistency by nearly 28%. More than 58% of newly deployed enterprise simulation environments now integrate centralized learning management platforms, enabling standardized performance tracking across multiple training sites. This transition strengthens operational visibility and supports continuous workforce competency management.

Mixed reality, digital twins, and haptic feedback technologies are replacing conventional scenario-based training with immersive clinical experiences. Compared with legacy mannequin-only systems, integrated mixed reality platforms improve procedural retention by approximately 26% while reducing repeated practical sessions by nearly 20%. Teaching hospitals, military healthcare organizations, and large medical universities gain the greatest competitive advantage because integrated simulation ecosystems support multidisciplinary education, remote collaboration, and scalable curriculum management without proportional infrastructure expansion.

Between 2026 and 2028, predictive learning analytics, adaptive virtual patients, and interoperable simulation platforms will become core enterprise capabilities rather than premium features. Automated scenario generation is expected to shorten curriculum development cycles by roughly 25%, while broader cloud deployment will accelerate multi-site training standardization. Organizations investing early in AI-enabled simulation ecosystems, cybersecurity, and interoperable software architectures will achieve stronger operational efficiency, faster workforce readiness, and sustainable competitive differentiation as healthcare education becomes increasingly data-driven.

January 2024 Laerdal Medical introduced SimMan Critical Care in partnership with IngMar Medical, integrating the ASL 5000 breathing simulator to support advanced ventilation training across multiple care settings. The platform supports 100% compatibility with modern ventilation modes, strengthening critical care education and expanding high-fidelity simulation capabilities.

May 2024 CAE Healthcare completed its rebranding to Elevate Healthcare following its acquisition by Madison Industries, marking a strategic shift toward simulation-led healthcare education. The transition unified operations under a single brand with 100% portfolio alignment, strengthening global commercialization and enterprise-focused innovation.

February 2025 Surgical Science completed the acquisition of Intelligent Ultrasound Group, expanding its simulation portfolio with ultrasound education technologies. The transaction added ultrasound simulation capabilities into Surgical Science's existing training ecosystem, strengthening product breadth and accelerating integrated clinical education offerings.

May 2024 The Society for Simulation in Healthcare and SESAM released the Global Consensus Statement on Simulation-Based Practice in Healthcare, developed with experts representing 50 simulation societies across 67 countries. The initiative established internationally aligned recommendations, reinforcing simulation's role in healthcare quality improvement and workforce readiness. Source: (Laerdal Medical)

This report provides comprehensive coverage of the Patient Simulation Market across product types, applications, end-users, competitive positioning, technology evolution, and regional deployment trends. It evaluates Adult, Pediatric, Obstetric, Surgical, and Ultrasound simulation systems while examining adoption across Medical Training, Nursing Education, Emergency Care, Surgical Training, and Clinical Assessment. The study also assesses Hospitals, Medical Schools, Nursing Colleges, Simulation Centers, and Military Healthcare, supported by operational indicators including deployment patterns, institutional adoption, and technology integration levels.

The analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting country-level investment priorities, infrastructure development, and enterprise expansion strategies. The report reviews AI-enabled simulation, mixed reality, cloud-based learning platforms, digital assessment tools, and interoperable training ecosystems. It also benchmarks leading industry participants, identifies emerging specialty simulation opportunities, and delivers strategic intelligence supporting investment planning, market expansion, product development, partnership evaluation, and competitive positioning throughout the 2026–2033 outlook period.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 745.95 Million |

Market Revenue in 2033 | USD 1500.6 Million |

CAGR (2026 - 2033) | 9.1% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Laerdal Medical, CAE Healthcare, Gaumard Scientific, Limbs & Things, Kyoto Kagaku, 3B Scientific, Simulab Corporation, Surgical Science, Mentice AB, VirtaMed AG, Intelligent Ultrasound Group, TruCorp, Operative Experience Inc. |

Customization & Pricing | Available on Request (10% Customization is Free) |