Reports

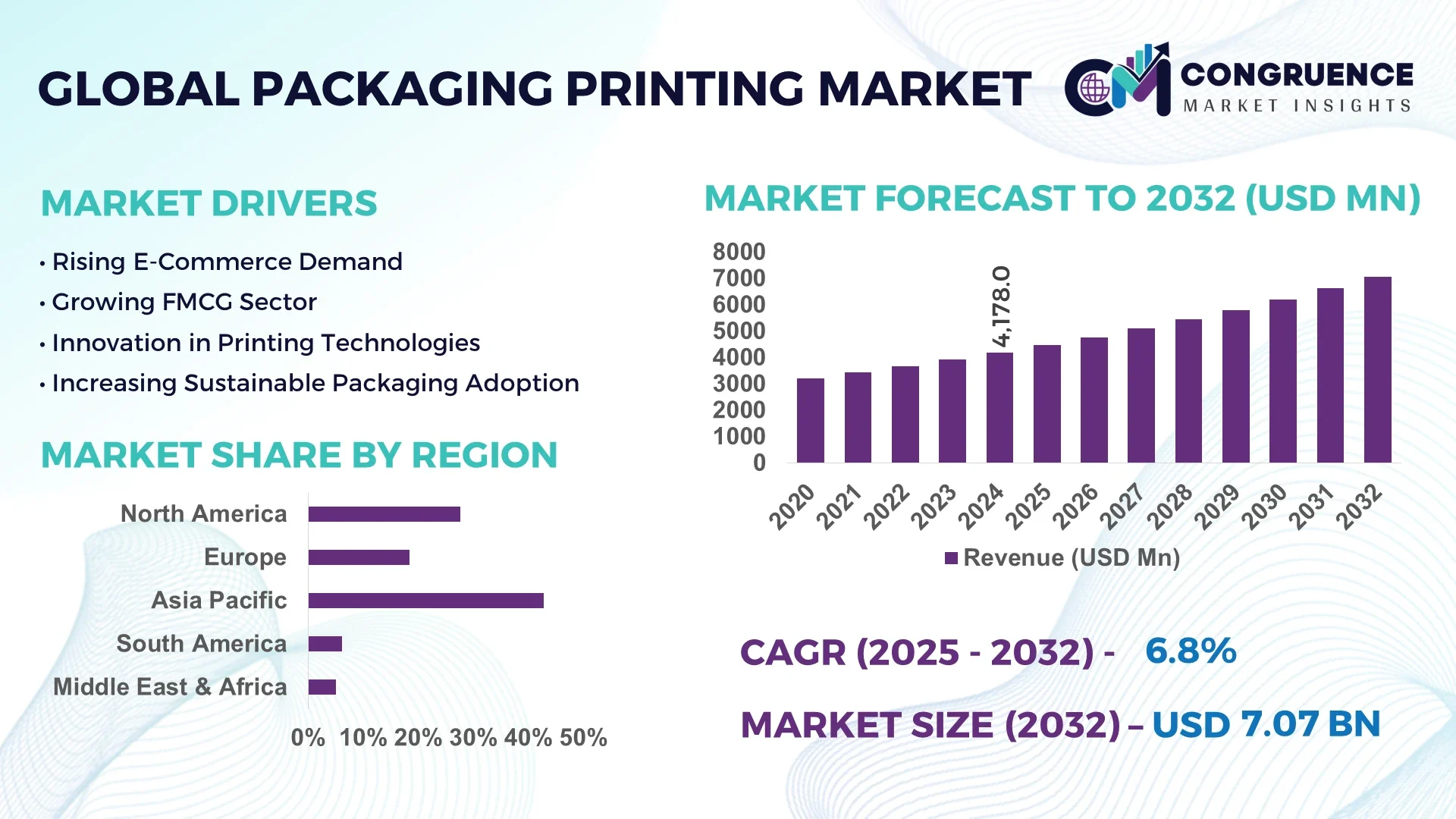

The Global Packaging Printing Market was valued at USD 4,178.0 Million in 2024 and is anticipated to reach USD 7,071.9 Million by 2032, expanding at a CAGR of 6.8% between 2025 and 2032. This growth is primarily attributed to increasing demand for high-quality, visually appealing, and sustainable packaging solutions across industries such as food & beverage, healthcare, and personal care.

China dominates the global packaging printing market, supported by its large-scale industrial production, advanced flexographic and digital printing infrastructure, and extensive packaging manufacturing capacity exceeding 45 million tons annually. The country has seen significant investment in eco-friendly ink formulations, 3D printing integration, and smart packaging technology, with over USD 2.3 billion allocated to R&D initiatives in 2023. Additionally, consumer adoption of digitally printed flexible packaging reached nearly 62%, driven by e-commerce growth, rapid urbanization, and sustainability goals.

Market Size & Growth: The market is valued at USD 4,178.0 Million in 2024 and projected to reach USD 7,071.9 Million by 2032, growing at a CAGR of 6.8%, driven by technological upgrades and rising demand for premium packaging.

Top Growth Drivers: 48% adoption of digital printing, 35% efficiency improvement in flexographic systems, and 42% growth in sustainable packaging demand.

Short-Term Forecast: By 2028, production efficiency is expected to improve by 33% with automation and AI-based print quality control.

Emerging Technologies: Widespread adoption of hybrid printing systems, AI-enabled defect detection, and UV-curable ink technologies.

Regional Leaders: Asia Pacific (USD 2,740 Million by 2032), North America (USD 1,850 Million by 2032), and Europe (USD 1,640 Million by 2032), each showing unique adoption trends in digital and sustainable printing.

Consumer/End-User Trends: Rapid uptake in FMCG and e-commerce packaging, with over 58% consumers preferring printed recyclable materials.

Pilot or Case Example: In 2024, a European printing consortium achieved 27% downtime reduction through digital workflow automation.

Competitive Landscape: HP Inc. leads with approximately 12% market share, followed by Amcor Plc, Mondi Group, Quad/Graphics, and Sonoco Products Company.

Regulatory & ESG Impact: Stricter packaging waste directives and incentives for biodegradable inks are accelerating adoption of low-VOC solutions.

Investment & Funding Patterns: Over USD 5.1 billion invested in 2023 toward smart printing and green ink technology development.

Innovation & Future Outlook: Integration of IoT-enabled printers and AI-based print analytics will redefine operational efficiency and sustainability by 2030.

The packaging printing sector is experiencing continuous innovation across digital, flexographic, and gravure printing processes. Recent advances in biodegradable substrates, water-based inks, and smart labeling are transforming end-user applications in healthcare, food packaging, and logistics. Increasing regulatory pressures and sustainability benchmarks continue to shape product development, regional adoption, and long-term growth potential.

The strategic relevance of the Packaging Printing Market lies in its ability to integrate sustainability, customization, and automation within industrial and consumer packaging ecosystems. As global trade and e-commerce accelerate, packaging printing enables brand differentiation, traceability, and regulatory compliance. Measurable performance improvements are emerging from digital transformation — AI-based digital presses deliver 30% higher throughput compared to legacy offset systems, optimizing time-to-market for short-run packaging.

Regionally, Asia Pacific dominates in volume, while Europe leads in technology adoption with 68% of enterprises integrating smart printing solutions. By 2027, predictive analytics in print management is expected to reduce operational waste by 28% and improve print material utilization efficiency. Firms are actively aligning with ESG commitments, targeting 40% recycling rate improvement by 2030 under sustainable printing mandates.

In 2024, Japan achieved a 25% energy consumption reduction through deployment of hybrid UV-curable presses and ink recovery systems. Strategic pathways increasingly include automation of print workflows, digital twin modeling, and use of blockchain for supply-chain traceability. By integrating AI, IoT, and green chemistry, the market positions itself as a pillar of operational resilience, regulatory compliance, and sustainable economic growth over the next decade.

The Packaging Printing Market is characterized by dynamic technological evolution, rising consumer expectations, and stringent environmental standards. Industry trends are shaped by the convergence of digital printing, eco-friendly inks, and flexible packaging materials. Rapid urbanization, growth in food delivery services, and the expansion of global e-commerce networks are creating sustained demand for customized and durable printed packaging solutions. Moreover, innovation in 3D and variable-data printing is enhancing supply chain efficiency and product personalization.

The exponential growth of e-commerce and fast-moving consumer goods (FMCG) sectors has significantly increased demand for high-quality printed packaging. In 2024, online retail packaging volume surged by 29%, requiring durable, branded, and sustainable packaging solutions. FMCG companies are investing heavily in digitally printed, quick-turnaround packaging formats to enhance shelf appeal and logistics traceability. The need for customized short-run packaging and real-time labeling systems has strengthened demand for digital and flexographic technologies, resulting in improved production speed and reduced waste.

Fluctuations in raw material costs, particularly paper, inks, and plastics, have imposed financial pressure on printing service providers. In 2024, ink cost volatility increased by 18%, driven by global supply chain disruptions. Additionally, stricter environmental regulations, such as solvent usage restrictions and waste management mandates, require continuous technological upgrades. Compliance with these evolving standards increases operational costs and delays product development, limiting the pace of innovation and market expansion in small- and mid-scale printing enterprises.

The accelerating transition to sustainable and intelligent packaging solutions presents a major opportunity for market growth. By 2026, over 70% of global brand owners are expected to adopt recyclable or compostable packaging materials. Smart packaging equipped with QR codes and RFID tagging is expanding rapidly, especially in the food and pharmaceutical sectors, enhancing traceability and consumer engagement. This creates a strong need for advanced digital printing technologies capable of high-resolution and variable data printing on eco-friendly substrates.

Integrating advanced digital printing technologies with legacy production systems remains a significant challenge for the industry. Approximately 40% of manufacturers report operational inefficiencies due to compatibility issues between old equipment and new digital workflows. High capital investment requirements and the need for skilled labor further slow technology adoption. This limits the scalability of automation initiatives, particularly among small and medium enterprises striving to modernize production lines.

Adoption of Digital and Hybrid Printing Systems: In 2024, digital and hybrid printing accounted for over 47% of new installations, reflecting a major shift toward shorter production runs and on-demand printing. These systems deliver up to 35% reduction in setup time and improve print accuracy, supporting brand agility in dynamic markets.

Sustainability-Driven Ink Innovation: Water-based and bio-ink formulations are gaining prominence, with adoption up 41% in 2024. Manufacturers report a 25% reduction in carbon emissions through use of low-VOC inks, aligning with circular economy objectives and regional sustainability policies.

AI-Powered Workflow Optimization: Artificial intelligence in prepress and print management enhanced production efficiency by 32% and reduced error rates by 22%. AI-driven inspection systems now control over 50% of global print lines, ensuring consistent color accuracy and quality assurance.

Smart Packaging Integration: Smart labels and printed sensors reached 38% market penetration in high-end consumer goods packaging. Embedded NFC and QR technologies improved logistics visibility by 27%, helping companies enhance customer engagement and compliance with evolving traceability regulations.

The Packaging Printing Market is segmented by type, application, and end-user, each contributing uniquely to the industry’s overall structure. The market encompasses flexographic, digital, gravure, and offset printing technologies, catering to varied substrate and performance requirements. Applications range from food & beverage and healthcare packaging to industrial and personal care sectors, each emphasizing brand differentiation and regulatory compliance. End-users include manufacturers, FMCG companies, and logistics providers adopting digitalized printing workflows to enhance traceability and sustainability. Continuous advancements in smart printing, automation, and eco-friendly ink formulations are reshaping market segmentation, driving specialization across printing technologies and end-user categories.

Flexographic printing currently dominates the global packaging printing market, accounting for approximately 38% of adoption in 2024. This dominance is attributed to its cost-effectiveness, versatility in printing on diverse substrates, and high-speed production capabilities, making it ideal for large-scale packaging operations. Digital printing represents the fastest-growing type, expanding at a CAGR of 7.9%, fueled by increasing demand for short-run, variable data printing and customization for consumer-focused products. Gravure printing holds around 22% share, primarily in high-quality image packaging, while offset and screen printing collectively contribute to a combined 26% share, serving niche segments such as rigid containers and premium labels.

The food & beverage sector leads the application segment, representing approximately 46% of total usage in 2024, due to stringent safety standards, high-volume packaging demand, and rising consumer preference for visually distinctive, branded packaging. The healthcare packaging segment follows with around 24%, driven by pharmaceutical labeling, dosage tracking, and counterfeit prevention measures. Meanwhile, the personal care and cosmetics application is the fastest-growing segment, expanding at a CAGR of 8.2%, as brands increasingly leverage high-resolution digital printing for small-batch and sustainable packaging solutions. Other application areas, including industrial goods and e-commerce packaging, collectively account for a 30% combined share, reflecting growth in shipping-ready and protective packaging materials. In 2024, over 58% of global FMCG enterprises reported adopting digitally printed packaging for enhanced traceability and brand differentiation. Additionally, 41% of consumers preferred products with eco-labeled packaging that communicates sustainability credentials.

Manufacturing and FMCG companies lead the end-user segment, accounting for approximately 44% of total market adoption in 2024, driven by high output volumes and demand for printed flexible packaging. The e-commerce and logistics sector is the fastest-growing end-user, projected to grow at a CAGR of 8.7%, due to rapid global online retail expansion and the need for durable, custom-printed, and trackable shipping materials. The healthcare and pharmaceutical industries hold around 21% share, leveraging printed packaging for regulatory compliance, authentication, and patient safety, while other sectors such as agriculture and automotive together represent a 35% combined share of total adoption. In 2024, more than 37% of global e-commerce firms integrated digitally printed packaging for brand personalization and improved consumer engagement, while 49% of healthcare product manufacturers employed variable data printing to enhance traceability.

Asia Pacific accounted for the largest market share at 42.8% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2025 and 2032.

The Asia-Pacific region’s dominance is primarily driven by the massive packaging demand from China, India, and Japan, which together represent over 60% of the region’s consumption volume. Strong manufacturing infrastructure, rising e-commerce shipments exceeding 12 billion parcels annually, and the rapid shift toward flexible and digital printing technologies contribute significantly to the regional growth. North America, driven by premium packaging trends and sustainability initiatives, continues to adopt innovative ink formulations and smart labeling technologies. Meanwhile, Europe, with around 28.5% of the global share, remains a mature yet innovation-driven market emphasizing recyclability and carbon-neutral packaging solutions. South America and the Middle East & Africa collectively account for around 10% of global revenue, supported by gradual industrialization and expanding consumer goods manufacturing bases.

North America holds approximately 27.6% of the global packaging printing market in 2024, supported by strong demand from the food & beverage, healthcare, and consumer goods industries. The U.S. and Canada have seen accelerated adoption of digital and flexographic printing, driven by the push toward short-run, customizable packaging. Regulatory updates under the U.S. Sustainable Packaging Act have encouraged the use of recyclable inks and bio-based materials. Local players such as Quad Graphics Inc. are investing in high-speed digital presses and data-driven personalization to enhance supply chain agility. The region’s enterprises exhibit strong digital adoption, particularly in healthcare and retail, with over 65% of packaging companies leveraging digital workflows. North American consumers increasingly favor brands with sustainable packaging, reflecting heightened environmental awareness and preference for premium-quality printed labels.

Europe represents approximately 28.5% of the global packaging printing market in 2024, with key markets including Germany, the United Kingdom, France, and Italy. The region’s strong regulatory framework—supported by the European Packaging and Packaging Waste Directive—has accelerated the transition to eco-friendly inks and recyclable materials. Countries such as Germany and France are spearheading digital printing adoption in luxury packaging and personal care sectors. European players like Smurfit Kappa Group are expanding sustainable corrugated printing lines using water-based inks and automated finishing systems. Consumer behavior in the region emphasizes eco-conscious purchasing, driving up demand for traceable, low-emission packaging. Furthermore, over 70% of manufacturers are integrating smart codes and RFID tagging for improved supply chain transparency, reflecting the region’s commitment to digital transformation within sustainable frameworks.

Asia Pacific dominates the global packaging printing market, accounting for 42.8% of total share in 2024. Countries such as China, India, and Japan are at the forefront, with China alone contributing over 50% of regional demand due to its vast FMCG, e-commerce, and electronics sectors. Rapid industrialization, rising disposable incomes, and expanding urban populations are fueling the adoption of high-quality printed packaging. Japan’s innovation in digital inkjet technologies and India’s booming corrugated printing industry further enhance regional competitiveness. Companies such as Huhtamaki PPL in India are investing in smart packaging solutions integrating QR-based consumer engagement. Consumer behavior across Asia Pacific shows a strong inclination toward visually appealing, affordable, and eco-friendly packaging, especially in e-commerce, where mobile-driven purchases dominate.

South America holds around 6.2% of the global packaging printing market in 2024, led by Brazil and Argentina as the major contributors. The regional market is witnessing increasing adoption of flexible and digital printing methods as local manufacturers cater to the food, beverage, and cosmetics sectors. Government trade initiatives such as Brazil’s packaging sustainability roadmap are promoting biodegradable and recyclable packaging practices. Infrastructure expansion in logistics and printing capabilities has strengthened local competitiveness. Regional players, including Klabin S.A., are advancing in paper-based packaging solutions with enhanced print quality and lower carbon footprints. Consumer behavior in South America is increasingly influenced by brand visibility, eco-awareness, and localized language printing, supporting demand for customized, high-quality packaging across urban markets.

The Middle East & Africa account for nearly 5.0% of the global packaging printing market in 2024, with strong demand emerging from UAE, Saudi Arabia, and South Africa. The region’s economic diversification into non-oil industries—particularly FMCG, pharmaceuticals, and construction—is accelerating demand for printed packaging materials. Investments in advanced flexographic and digital technologies are on the rise, especially within industrial printing parks in the UAE. Local companies such as Saudi Printing & Packaging Company are expanding capacity for flexible packaging and smart labeling solutions. Regulatory frameworks encouraging recyclable materials and trade partnerships under the African Continental Free Trade Area (AfCFTA) are further bolstering growth. Regional consumers favor visually striking and durable packaging, aligning with the trend of premiumization in retail and food sectors.

China – 28.4% Market Share: Dominance driven by high production capacity, large-scale FMCG exports, and strong e-commerce packaging demand.

United States – 22.6% Market Share: Leadership supported by advanced digital printing infrastructure and rapid adoption of sustainable packaging materials across major industries.

The Packaging Printing Market exhibits a moderately fragmented competitive environment with over 350 active global players operating across different segments. The top five companies—Amcor plc, Mondi Group, Smurfit Kappa, Sonoco Products, and Toppan Printing—together hold approximately 48% of the global market, highlighting significant competition among leading and mid-tier players. Strategic initiatives such as partnerships, technology licensing agreements, and in-house R&D expansions are shaping market dynamics, with companies collectively investing over USD 3.7 billion in digital printing, sustainable inks, and automation technologies in 2024.

Innovation trends are strongly influencing competitive positioning. For instance, over 62% of packaging firms worldwide are integrating automated inspection systems, AI-based color management, and workflow optimization tools to improve throughput and reduce material waste by up to 22%. In addition, companies are increasingly focusing on biodegradable substrates and high-speed flexographic presses, with adoption rates of eco-friendly inks rising to 45% globally. Market players are also expanding their geographic reach, with over 38% of investments in 2024 targeting emerging regions in Asia-Pacific, South America, and Middle East & Africa, further intensifying competition.

Smurfit Kappa Group plc

Toppan Printing Co., Ltd.

Quad/Graphics, Inc.

Printpack

Sealed Air Corporation

Halaman Printing and Packaging Corp

Blue Label Packaging Company

Technological advancements in the Packaging Printing Market are revolutionizing production efficiency and product differentiation. Digital printing adoption has surged, with over 40% of new packaging lines in 2024 integrating inkjet or electrophotography systems for high-resolution and short-run applications. Automation is now utilized in approximately 55% of large-scale production facilities, enabling predictive maintenance, real-time quality control, and a 15–20% reduction in downtime.

Sustainability-driven technology has also gained momentum. Eco-friendly ink adoption, including UV-curable and water-based inks, increased to 45% of the market, while bio-based substrates now constitute 18% of total packaging materials in select regions. Smart packaging solutions incorporating RFID tags and QR codes are implemented in over 30% of consumer goods products to enhance traceability and engagement.

Emerging trends include 3D printed packaging prototypes, reducing material waste by up to 25%, and AI-assisted workflow management, which optimizes production lines to handle over 2,500 print jobs per month in high-volume plants. These technologies are reshaping operational efficiency, sustainability, and customization, allowing companies to respond effectively to evolving consumer and regulatory demands.

In March 2024, Amcor unveiled a high-speed digital printing facility in the U.S., capable of producing over 500 million digitally printed flexible packs annually, integrating AI-based color management and reducing material waste by 20%. Source: www.amcor.com

In September 2023, Mondi opened a new flexographic packaging plant in Germany, increasing output capacity by 15,000 tons annually and employing fully automated inspection systems to ensure 99.7% print accuracy. Source: www.mondigroup.com

In February 2024, Smurfit Kappa initiated production of 100% recyclable corrugated boards in the UK, supplying over 200 million packaging units to FMCG and e-commerce sectors. Source: www.smurfitkappa.com

In December 2023, Toppan deployed AI-based defect detection across its Japanese facilities, resulting in a 17% reduction in rejected packaging units and improving overall production efficiency. Source: www.toppan.com

The Packaging Printing Market Report provides an extensive overview of industry segments, including printing technologies, ink types, substrate materials, applications, and geographic coverage. The report evaluates flexographic, gravure, offset, and digital printing technologies, emphasizing their applications in food & beverage, healthcare, personal care, e-commerce, and industrial sectors. Ink types analyzed include solvent-based, water-based, UV-curable, and bio-inks, along with emerging innovations in hybrid and smart printing systems.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting production volumes, consumption trends, infrastructure development, regulatory frameworks, and adoption of technological advancements in each region. Additionally, the report identifies emerging and niche segments, including smart packaging, eco-friendly substrates, and high-speed automated presses, providing insights into production efficiency and sustainability initiatives.

By consolidating market insights across technology, application, end-user, and regional trends, the report equips stakeholders with actionable intelligence to make informed strategic, operational, and investment decisions. It highlights opportunities for innovation, competitive positioning, and sustainable growth within the global packaging printing ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 4,178.0 Million |

| Market Revenue (2032) | USD 7,071.9 Million |

| CAGR (2025–2032) | 6.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Amcor plc, Mondi Group, Sonoco Products Company, Smurfit Kappa Group plc, Toppan Printing Co., Ltd., Quad/Graphics, Inc., Printpack, Sealed Air Corporation, Halaman Printing and Packaging Corp, Blue Label Packaging Company |

| Customization & Pricing | Available on Request (10% Customization is Free) |