Reports

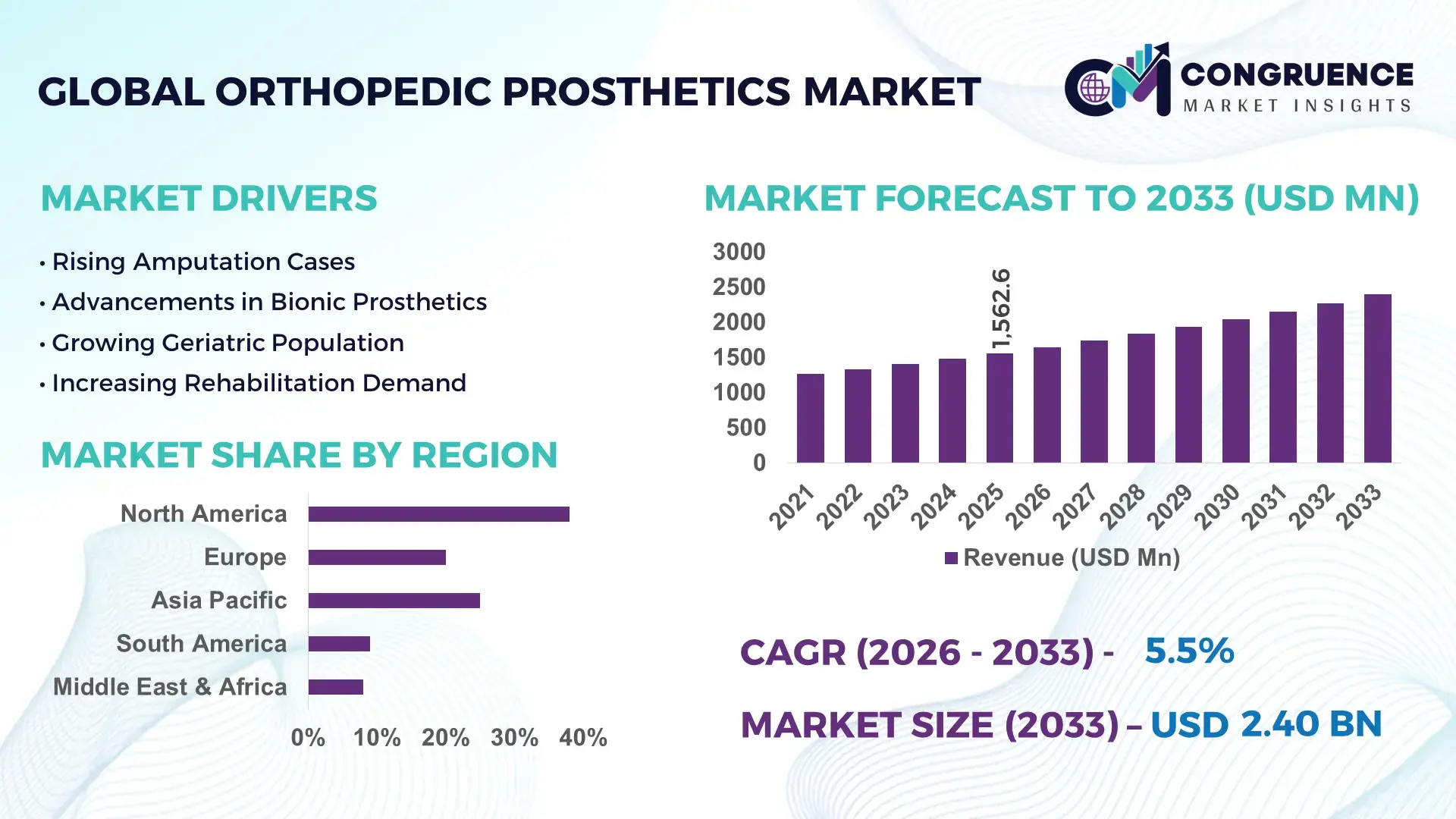

The Global Orthopedic Prosthetics Market was valued at USD 1562.57 Million in 2025 and is anticipated to reach a value of USD 2398.06 Million by 2033 expanding at a CAGR of 5.5% between 2026 and 2033. Advanced microprocessor-controlled prosthetics, lightweight carbon-fiber composites, and AI-enabled gait analysis systems are accelerating replacement cycles, with digitally customized limb solutions reducing fitting time by nearly 28% compared to conventional socket-based methods.

The United States continues to dominate the global orthopedic prosthetics landscape with nearly 34% market share, supported by annual orthopedic device investments exceeding USD 5 billion and a high concentration of rehabilitation centers integrating robotic mobility platforms. More than 62% of premium lower-limb prosthetic fittings in the country now incorporate sensor-enabled alignment systems, compared to below 40% adoption across several Asia-Pacific markets. Germany remains a high-value European manufacturing hub with precision-engineered prosthetic component exports rising by 14% in 2025, while Japan leads in elderly mobility adoption through advanced mechatronic prosthetics for aging populations. Compared with traditional prosthetic fabrication, additive-manufactured components lower production waste by approximately 22% and improve patient-specific fitting accuracy.

Market Size & Growth: Global orthopedic prosthetics market reached USD 1562.57 million in 2025 and advances toward USD 2398.06 million by 2033, driven by AI-assisted fitting systems and lightweight composite adoption.

Top Growth Drivers: Microprocessor knee demand increased 19%, 3D-printed prosthetic adoption expanded 24%, and rehabilitation robotics integration rose 17% globally.

Short-Term Forecast: By 2028, digital prosthetic scanning reduces patient fitting turnaround time by 31% while material wastage declines 22%.

Emerging Technologies: AI gait analytics, smart sensor integration, and carbon-fiber additive manufacturing improve prosthetic durability by 18% and mobility response accuracy by 26%.

Regional Leaders: North America exceeds USD 820 million with robotic rehabilitation expansion, Europe crosses USD 610 million through reimbursement upgrades, and Asia-Pacific approaches USD 540 million driven by elderly mobility demand.

Consumer/End-User Trends: Nearly 58% of advanced lower-limb prosthetic users prefer sensor-enabled adaptive devices with app-based performance tracking.

Pilot/Case Example: In 2025, a digitally integrated rehabilitation network reduced prosthetic adjustment visits by 33% using AI-powered alignment monitoring.

Competitive Landscape: Leading manufacturers control approximately 41% combined share, with innovation led by advanced biomechanical engineering and customized prosthetic platforms.

Regulatory & ESG Impact: Sustainable composite initiatives lowered production scrap volumes by 20%, while stricter device compliance accelerated certified digital prosthetic deployment across Europe.

Investment & Funding: Global orthopedic mobility investments surpassed USD 1.4 billion between 2024 and 2026, supported by manufacturing expansion and rehabilitation technology partnerships.

Innovation & Future Outlook: Neural-interface prosthetics, cloud-connected monitoring platforms, and regionalized supply chain models are reshaping next-generation orthopedic mobility strategies.

Orthopedic rehabilitation centers account for nearly 46% of total prosthetic demand, followed by trauma recovery applications at 29% and diabetic limb-loss management at approximately 18%. Advanced sensor-integrated prosthetics and 3D-printed socket systems are improving mobility precision and reducing patient recalibration frequency by over 25%. North America and Western Europe continue leading high-value adoption, while Asia-Pacific experiences rapid expansion through aging population support programs and localized manufacturing investments. Regulatory standardization for smart medical devices and ongoing supply chain regionalization are accelerating procurement modernization, positioning digitally connected prosthetic ecosystems as the next strategic growth frontier.

The orthopedic prosthetics market is transforming into a strategic healthcare technology segment where mobility restoration, digital rehabilitation, and precision engineering are accelerating competitive differentiation. Hospitals and rehabilitation networks are prioritizing smart prosthetic ecosystems as patient retention and long-term care efficiency become measurable performance indicators. Supply chain regionalization and stricter medical-device traceability rules are forcing manufacturers to redesign sourcing and production strategies across North America and Europe. AI-assisted prosthetic alignment systems now reduce calibration time by 34% while improving patient mobility accuracy by 27% compared to legacy mechanical fitting systems, creating a direct operational advantage for integrated rehabilitation providers.

Asia-Pacific leads in procedural volume due to expanding trauma-care infrastructure and aging demographics, while North America leads in adoption and innovation with nearly 61% penetration of sensor-enabled lower-limb prosthetics in premium rehabilitation facilities. Over the next three years, digital scanning and additive manufacturing workflows are expected to reduce prosthetic production cycles by 30% and lower customization costs by 18%. Manufacturers implementing recyclable composite materials and energy-efficient fabrication systems are securing ESG-linked procurement advantages and reducing material waste by approximately 21%. In 2025, a robotic rehabilitation deployment across a multi-center orthopedic network improved patient gait recovery rates by 29% within six months.

Capital allocation is rapidly shifting toward neural-interface mobility systems, cloud-connected prosthetic monitoring, and localized manufacturing hubs to optimize supply continuity and post-treatment analytics. Companies expanding rehabilitation software partnerships and AI-driven customization capabilities are strengthening recurring service models while accelerating clinical integration. The next competitive frontier will be defined by how effectively manufacturers combine intelligent prosthetic performance, scalable production efficiency, and regulatory-ready digital ecosystems into a unified mobility platform strategy.

Rising integration of AI-enabled prosthetics, robotic rehabilitation platforms, and lightweight composite materials is accelerating orthopedic prosthetics demand across trauma recovery and elderly mobility segments. Nearly 58% of premium lower-limb devices now incorporate sensor-assisted gait optimization, while digital scanning reduces fitting turnaround time by 31%. Post-2024 supply chain restructuring across North America and Europe pushed manufacturers toward regional production hubs, improving component availability and shortening delivery cycles by 18%. This structural shift is forcing healthcare providers to prioritize digitally integrated rehabilitation ecosystems that optimize patient retention and treatment efficiency. In response, companies are expanding additive manufacturing capacity, accelerating rehabilitation software partnerships, and increasing investment in smart prosthetic platforms to secure long-term procurement contracts and clinical differentiation globally.

Orthopedic prosthetics manufacturers face increasing pressure from semiconductor dependency, carbon-fiber material volatility, and tightening medical-device compliance standards. More than 46% of advanced prosthetic sensor components remain concentrated within limited supplier networks, exposing production systems to logistics disruptions and pricing instability. Regulatory approval timelines for AI-integrated prosthetic systems expanded by nearly 22% between 2024 and 2026, delaying commercialization and increasing validation costs. Infrastructure gaps across developing rehabilitation markets further constrain scalable deployment of premium prosthetic technologies. These limitations are directly impacting operating margins, inventory planning, and product launch schedules. To mitigate risk, manufacturers are diversifying sourcing strategies, securing long-term material contracts, and investing in modular prosthetic architectures that reduce dependence on highly specialized imported electronic components.

Smart prosthetic ecosystems integrating AI analytics, cloud-connected monitoring, and additive manufacturing are reshaping competitive positioning across the orthopedic prosthetics industry. Digitally customized prosthetics improve mobility precision by 26% while lowering refitting requirements by nearly 20%, creating measurable operational savings for rehabilitation centers. Emerging healthcare infrastructure investments across Southeast Asia, Latin America, and the Middle East are expanding advanced prosthetic access, with rehabilitation facility capacity increasing by 24% in several urban healthcare corridors. Neural-interface prosthetics and adaptive sensor technologies are emerging as high-value innovation pathways with faster patient responsiveness and stronger clinical outcomes. Companies are accelerating R&D spending, building localized manufacturing ecosystems, and forming rehabilitation technology partnerships to secure first-mover advantage in next-generation orthopedic mobility solutions and long-term service integration.

Scaling advanced orthopedic prosthetics remains challenging due to infrastructure limitations, skilled clinician shortages, and inconsistent reimbursement frameworks across major healthcare systems. Nearly 39% of rehabilitation facilities in emerging economies lack digital gait analysis capabilities required for high-performance smart prosthetic integration. Rising electronic component costs increased advanced prosthetic assembly expenses by approximately 17% between 2024 and 2026, constraining affordability and procurement expansion. Healthcare providers also face growing pressure to demonstrate long-term patient outcome consistency under stricter regulatory performance benchmarks. These execution barriers are reshaping competitive dynamics by favoring manufacturers with integrated service ecosystems and localized technical support networks. To remain competitive, companies must strengthen clinician training, expand rehabilitation partnerships, and invest aggressively in scalable digital prosthetic infrastructure and compliance-ready manufacturing systems.

Digital fitting adoption surged 32% across rehabilitation networks in 2025, reshaping prosthetic customization workflows. Clinics are replacing manual casting with AI-assisted scanning systems that reduce fitting errors by 27% and shorten patient processing cycles by 30%. Companies are restructuring fabrication operations around centralized digital modeling hubs to optimize throughput and lower material waste. Rising clinician shortages are further accelerating automated fitting deployment.

Sensor-enabled prosthetic integration expanded by 29%, forcing manufacturers to prioritize connected mobility platforms. Real-time gait analytics and cloud-based performance monitoring are now embedded into premium lower-limb systems, improving mobility calibration accuracy by 24%. Companies are scaling software partnerships and subscription-based monitoring services to strengthen recurring revenue models while optimizing post-treatment engagement and maintenance tracking across rehabilitation ecosystems.

Regional manufacturing localization increased 21% as supply chain disruptions reshaped production strategies. North American and European manufacturers are shifting component sourcing closer to assembly facilities following semiconductor delays and logistics instability linked to Red Sea trade disruptions. This operational transition reduced average delivery timelines by 18% while improving inventory predictability. Companies are expanding modular production systems to balance resilience with customization flexibility.

Myoelectric prosthetic deployment rose 26% within specialized mobility programs, redefining premium product positioning. Advanced upper-limb systems integrating muscle-signal responsiveness improved movement precision by 22% compared with conventional mechanical alternatives. Rehabilitation providers are prioritizing high-performance prosthetics for sports recovery and military rehabilitation segments, while manufacturers are optimizing lightweight materials and battery efficiency to strengthen long-duration usability and competitive differentiation.

The orthopedic prosthetics market is segmented by type, application, and end-user, with lower limb prosthetics and mobility assistance applications dominating overall demand due to rising trauma recovery and elderly mobility requirements. Hospitals and rehabilitation centers collectively account for nearly 61% of procurement activity as digitally integrated rehabilitation systems gain adoption. Demand is shifting toward microprocessor-controlled and myoelectric prosthetics, which recorded adoption growth above 20% through enhanced mobility precision and real-time gait optimization. Pediatric and geriatric care segments are also expanding steadily as healthcare systems prioritize long-term mobility support. Companies are repositioning manufacturing, customization, and rehabilitation partnerships to capture higher-value, technology-driven prosthetic deployment opportunities globally.

Lower Limb Prosthetics dominate the orthopedic prosthetics market with approximately 44% share, driven by high procedural volumes linked to diabetes-related amputations, trauma recovery, and elderly mobility requirements. Their structural dominance comes from broader rehabilitation applicability, scalable manufacturing, and faster integration with sensor-assisted gait systems. Microprocessor-Controlled Prosthetics represent the fastest-growing segment, with adoption increasing by nearly 23% due to improved mobility responsiveness, real-time balance correction, and reduced rehabilitation time. Compared with Conventional Prosthetics, advanced microprocessor systems improve walking efficiency by nearly 28% while reducing adjustment frequency significantly, reshaping premium product demand. Myoelectric Prosthetics are accelerating in upper-limb rehabilitation programs where precision control and muscle-signal responsiveness are becoming competitive differentiators. Upper Limb Prosthetics, Myoelectric Prosthetics, and Conventional Prosthetics collectively account for nearly 56% of market demand, maintaining relevance across cost-sensitive and specialized rehabilitation settings. Companies are expanding smart prosthetic production lines, investing in lightweight materials, and prioritizing AI-integrated mobility systems, while conventional product portfolios are increasingly repositioned toward emerging markets and public healthcare procurement programs.

Mobility Assistance remains the leading application segment with nearly 38% share, supported by rising demand for long-term movement restoration across elderly and trauma-affected populations. High dependency on lower-limb prosthetic integration and continuous rehabilitation support has concentrated usage within this segment. Geriatric Care is emerging as the fastest-growing application area, recording adoption growth above 21% due to aging demographics, improved reimbursement alignment, and increasing deployment of sensor-enabled mobility systems. Compared with Trauma Recovery, which remains operationally mature through hospital-led rehabilitation programs, Geriatric Care is shifting demand toward lightweight, adaptive prosthetics designed for long-duration usability and remote mobility monitoring. Rehabilitation Therapy, Sports Injury Recovery, Pediatric Care, and Trauma Recovery collectively contribute more than 62% of total application demand, supported by expanding rehabilitation infrastructure and digital therapy integration. Companies are scaling rehabilitation partnerships, optimizing prosthetic customization for activity-specific recovery, and repositioning premium mobility platforms toward specialized patient segments where performance tracking and mobility precision are becoming decisive procurement factors.

Hospitals dominate the orthopedic prosthetics market with approximately 36% share due to high surgical procedure volumes, integrated rehabilitation pathways, and stronger purchasing capacity for advanced prosthetic systems. Their demand concentration is reinforced by centralized trauma recovery programs and increasing adoption of AI-assisted mobility technologies. Rehabilitation Centers represent the fastest-growing end-user segment, expanding by nearly 22% as post-surgical recovery models shift toward long-duration mobility optimization and digital gait monitoring. Compared with Prosthetic Clinics, which remain focused on personalized fitting and outpatient customization, Rehabilitation Centers are capturing broader demand through integrated therapy ecosystems and continuous patient monitoring capabilities. Prosthetic Clinics, Ambulatory Surgical Centers, Orthopedic Centers, and Military Healthcare Facilities collectively account for nearly 64% of market activity, with military programs increasingly prioritizing high-performance myoelectric and microprocessor-enabled systems for mobility restoration. Companies are responding through bundled rehabilitation partnerships, outcome-based pricing models, and localized technical support expansion. Procurement behavior is increasingly favoring scalable smart prosthetic platforms that combine customization efficiency, rehabilitation analytics, and long-term clinical performance optimization.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

North America continues leading demand concentration through advanced rehabilitation infrastructure, high adoption of sensor-enabled prosthetics, and strong reimbursement alignment, with nearly 61% of premium lower-limb systems integrating AI-assisted gait technologies. Europe accounts for approximately 29% share and leads in regulatory-driven innovation, particularly in sustainable prosthetic materials and digitally compliant rehabilitation systems. Asia-Pacific contributes nearly 24% of global demand while accelerating production scale through localized manufacturing expansion across China, Japan, and India. Regionalized supply chain restructuring after global logistics disruptions is reshaping procurement strategies and reducing delivery timelines by almost 18%. Companies are increasingly focusing investment on Asia-Pacific production hubs while maintaining innovation and premium rehabilitation deployment across North America and Europe.

North America holds nearly 38% of global orthopedic prosthetics demand, supported by advanced trauma-care infrastructure, rising diabetic amputation cases, and rapid deployment of AI-assisted rehabilitation systems. More than 61% of premium prosthetic fittings now integrate sensor-enabled gait optimization, while digital scanning platforms reduce fitting turnaround time by approximately 30%. Tightening reimbursement performance standards and ongoing supply chain localization are forcing manufacturers to expand regional assembly operations and strengthen rehabilitation partnerships. Hospitals and rehabilitation centers increasingly prefer connected prosthetic ecosystems that combine mobility analytics with long-term monitoring capabilities. Several manufacturers expanded smart prosthetic production capacity by over 20% during 2025 to address rising clinical demand. The region remains a priority investment destination due to strong purchasing power, rapid technology adoption, and integrated rehabilitation networks.

Europe represents approximately 29% of the orthopedic prosthetics market, with Germany, the United Kingdom, and France leading high-value rehabilitation deployment. Regulatory pressure surrounding sustainable medical manufacturing and digital device traceability is reshaping procurement priorities across healthcare systems. More than 44% of rehabilitation providers now prioritize recyclable composite prosthetics and digitally monitored mobility platforms to improve compliance efficiency and reduce long-term maintenance costs. AI-assisted fitting systems reduced prosthetic recalibration frequency by nearly 21% across several orthopedic networks, accelerating operational optimization. Companies are expanding localized additive manufacturing facilities and restructuring supplier relationships to align with stricter European medical-device standards. Enterprise buyers increasingly favor premium, compliance-ready prosthetic systems over lower-cost imports, forcing manufacturers to innovate rapidly around durability, sustainability, and digitally integrated rehabilitation performance.

Asia-Pacific ranks as the fastest-expanding orthopedic prosthetics market, contributing nearly 24% of global demand through rising trauma-care procedures, aging populations, and accelerating rehabilitation infrastructure investment. China, Japan, and India are leading regional deployment through localized production ecosystems and lower manufacturing costs. More than 36% of component assembly operations shifted toward Asia-Pacific facilities between 2024 and 2026 as manufacturers optimized supply resilience and production scalability. Rehabilitation centers across urban healthcare networks increased digital prosthetic fitting adoption by approximately 28%, improving patient throughput and customization efficiency. Cost-sensitive buyers continue prioritizing scalable, lightweight prosthetics with faster delivery timelines, forcing companies to expand regional fabrication capacity and modular production systems. Asia-Pacific remains strategically critical for large-scale manufacturing, export positioning, and long-term patient volume expansion.

South America accounts for nearly 6% of the orthopedic prosthetics market, with Brazil and Argentina leading regional rehabilitation demand through expanding trauma-care and diabetic mobility programs. Public healthcare budget limitations and uneven rehabilitation infrastructure continue constraining premium prosthetic adoption across several secondary urban markets. However, localized prosthetic assembly increased by nearly 19% during 2025 as manufacturers responded to import cost pressure and delivery delays. Rehabilitation providers are increasingly adopting mid-range modular prosthetics that balance affordability with improved mobility performance. More than 32% of procurement contracts now prioritize locally serviceable prosthetic systems to reduce maintenance costs and downtime. Companies expanding regional partnerships and localized customization capabilities are gaining stronger market access, although pricing sensitivity and reimbursement inconsistencies continue creating operational risk across broader expansion strategies.

The Middle East & Africa region contributes approximately 3% of global orthopedic prosthetics demand, led by Saudi Arabia, the UAE, and South Africa through healthcare modernization and rehabilitation infrastructure expansion. Rising workplace injuries linked to construction, industrial activity, and transportation sectors are strengthening demand for advanced mobility restoration systems. Government-backed healthcare investment programs increased rehabilitation technology deployment by nearly 23% between 2024 and 2026, while digital prosthetic fitting adoption expanded steadily across private orthopedic centers. Enterprise buyers increasingly prioritize durable, low-maintenance prosthetic systems suited for long-term mobility rehabilitation and climate-intensive operating conditions. Manufacturers are forming regional distribution partnerships and expanding localized servicing networks to improve accessibility and reduce support delays. The region is emerging as a strategic expansion market driven by infrastructure investment, healthcare transformation, and rehabilitation capacity development.

United States – Holds approximately 34% share of the orthopedic prosthetics market due to advanced rehabilitation infrastructure, high smart prosthetic adoption, and strong clinical integration capabilities.

Germany – Accounts for nearly 11% share of the orthopedic prosthetics market, supported by precision prosthetic manufacturing, regulatory-driven innovation, and strong orthopedic technology deployment across rehabilitation networks.

The orthopedic prosthetics market is dominated by global mobility technology leaders competing against regional customization specialists and cost-focused manufacturers. Össur, Ottobock, Hanger Inc., Blatchford, and Fillauer collectively control nearly 41% of premium prosthetic deployment, competing primarily through AI-assisted mobility systems, lightweight material engineering, and integrated rehabilitation partnerships. Technology-focused players are reshaping competition by improving prosthetic fitting efficiency by approximately 30% and reducing recalibration frequency by nearly 24% through sensor-enabled gait analytics. Regional manufacturers compete aggressively on pricing and localized servicing, particularly across Asia-Pacific and South America. Companies are accelerating vertical integration, additive manufacturing expansion, and digital rehabilitation ecosystem partnerships to optimize supply resilience and recurring service revenue. The competitive shift is increasingly favoring firms controlling smart prosthetic software integration and localized production infrastructure. High regulatory compliance costs and advanced component dependency remain major entry barriers. Winning requires scalable customization, rehabilitation integration, and operational speed across regional healthcare systems.

Ottobock

Össur

Hanger Inc.

Blatchford

Fillauer

WillowWood Global LLC

Steeper Group

Proteor

Endolite

College Park Industries

Naked Prosthetics

Ortho Europe

Aether Biomedical

Mobius Bionics

AI-assisted gait analytics, sensor-enabled alignment systems, and digital socket scanning technologies are currently reshaping orthopedic prosthetics manufacturing and rehabilitation workflows. Nearly 58% of premium lower-limb prosthetic deployments now integrate real-time motion sensors to optimize balance correction and mobility response. Digital fitting platforms reduce prosthetic calibration time by approximately 31% while improving fitting precision by 27% compared with manual casting methods. Rehabilitation providers are integrating cloud-connected monitoring systems to optimize long-term patient tracking and reduce repeat adjustment visits. Companies scaling digital rehabilitation ecosystems are securing operational advantages through faster customization cycles and stronger recurring service integration.

Emerging technologies between 2026 and 2028 are centered on microprocessor-controlled prosthetics, myoelectric systems, and additive manufacturing integration. Advanced carbon-fiber 3D printing reduces material waste by nearly 22% while accelerating component production speed by 26% compared with conventional fabrication systems. More than 36% of large orthopedic manufacturers are expanding localized additive manufacturing capacity to strengthen supply resilience and reduce delivery delays. Myoelectric upper-limb systems are also gaining momentum through improved muscle-signal responsiveness and lightweight battery optimization, particularly across military rehabilitation and sports recovery programs.

Disruptive innovation is increasingly shifting toward neural-interface prosthetics, adaptive AI mobility systems, and wearable human-machine integration platforms. Neurotechnology-enabled prosthetics improve movement responsiveness by approximately 34% compared with legacy mechanical systems, redefining premium mobility performance. Global technology leaders and rehabilitation-focused manufacturers benefit most from this transition because integrated software ecosystems, digital rehabilitation analytics, and localized smart manufacturing are becoming decisive competitive differentiators. Companies delaying intelligent prosthetic integration risk losing procurement preference as healthcare systems prioritize scalable, connected, and performance-measured mobility solutions.

April 2025 – Ottobock invested in Phantom Neuro’s neurotechnology platform to accelerate development of intuitive prosthetic control systems through a USD 19 million Series A financing round. The partnership strengthens neural-interface prosthetic commercialization and expands AI-driven mobility innovation capabilities across advanced rehabilitation ecosystems. [Neural Control Expansion] Source: Ottobock Corporate Newsroom

May 2025 – Blatchford announced a £15 million investment in a new Operations Centre of Excellence in Basingstoke to expand advanced prosthetic manufacturing capacity and streamline innovation deployment. The facility is expected to improve operational scalability and strengthen supply responsiveness for high-demand mobility technologies. [Manufacturing Scale Upgrade] Source: Blatchford Mobility News

August 2025 – Ottobock launched multiple strategic prosthetic and exoskeleton technologies while reporting a 30.5% increase in operational profitability driven by innovation efficiency and product integration. The company accelerated investments in neurotechnology, intelligent prosthetics, and human-machine interface systems to strengthen premium mobility leadership. [Human-Machine Integration] Source: Ottobock Company Newsroom

April 2024 – Össur partnered with the Challenged Athletes Foundation to distribute 115 advanced prosthetic sports feet and knees across mobility programs nationwide. The initiative expanded high-performance prosthetic accessibility and reinforced demand for activity-specific rehabilitation technologies within sports recovery and adaptive mobility segments. [Adaptive Mobility Deployment]

The Orthopedic Prosthetics Market report delivers comprehensive analysis across product types, applications, end-users, regional performance, and advanced mobility technologies shaping global rehabilitation systems between 2026 and 2033. The report evaluates Upper Limb Prosthetics, Lower Limb Prosthetics, Microprocessor-Controlled Prosthetics, Myoelectric Prosthetics, and Conventional Prosthetics alongside key application areas including mobility assistance, trauma recovery, pediatric care, and geriatric rehabilitation. End-user assessment covers hospitals, rehabilitation centers, prosthetic clinics, orthopedic centers, ambulatory surgical centers, and military healthcare facilities across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The study analyzes more than 10 major industry participants and tracks operational shifts linked to AI-assisted fitting systems, sensor-enabled gait analytics, additive manufacturing, and neural-interface prosthetic technologies. Nearly 58% of premium prosthetic deployments now incorporate digital mobility optimization features, while additive manufacturing adoption has improved fabrication efficiency by approximately 26%. The report also evaluates regionalized production strategies, rehabilitation infrastructure modernization, and evolving procurement behavior influencing market positioning.

Strategically, the report supports investment planning, competitive benchmarking, product expansion, and supply chain optimization through detailed segmentation insights, technology adoption analysis, and regional demand mapping. It highlights emerging smart prosthetic ecosystems and digitally connected rehabilitation platforms that are redefining operational scalability and long-term competitive advantage across the global orthopedic prosthetics industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1562.57 Million |

|

Market Revenue in 2033 |

USD 2398.06 Million |

|

CAGR (2026 - 2033) |

5.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Ottobock, Össur, Hanger Inc., Blatchford, Fillauer, WillowWood Global LLC, Steeper Group, Proteor, Endolite, College Park Industries, Naked Prosthetics, Ortho Europe, Aether Biomedical, Mobius Bionics |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |