Reports

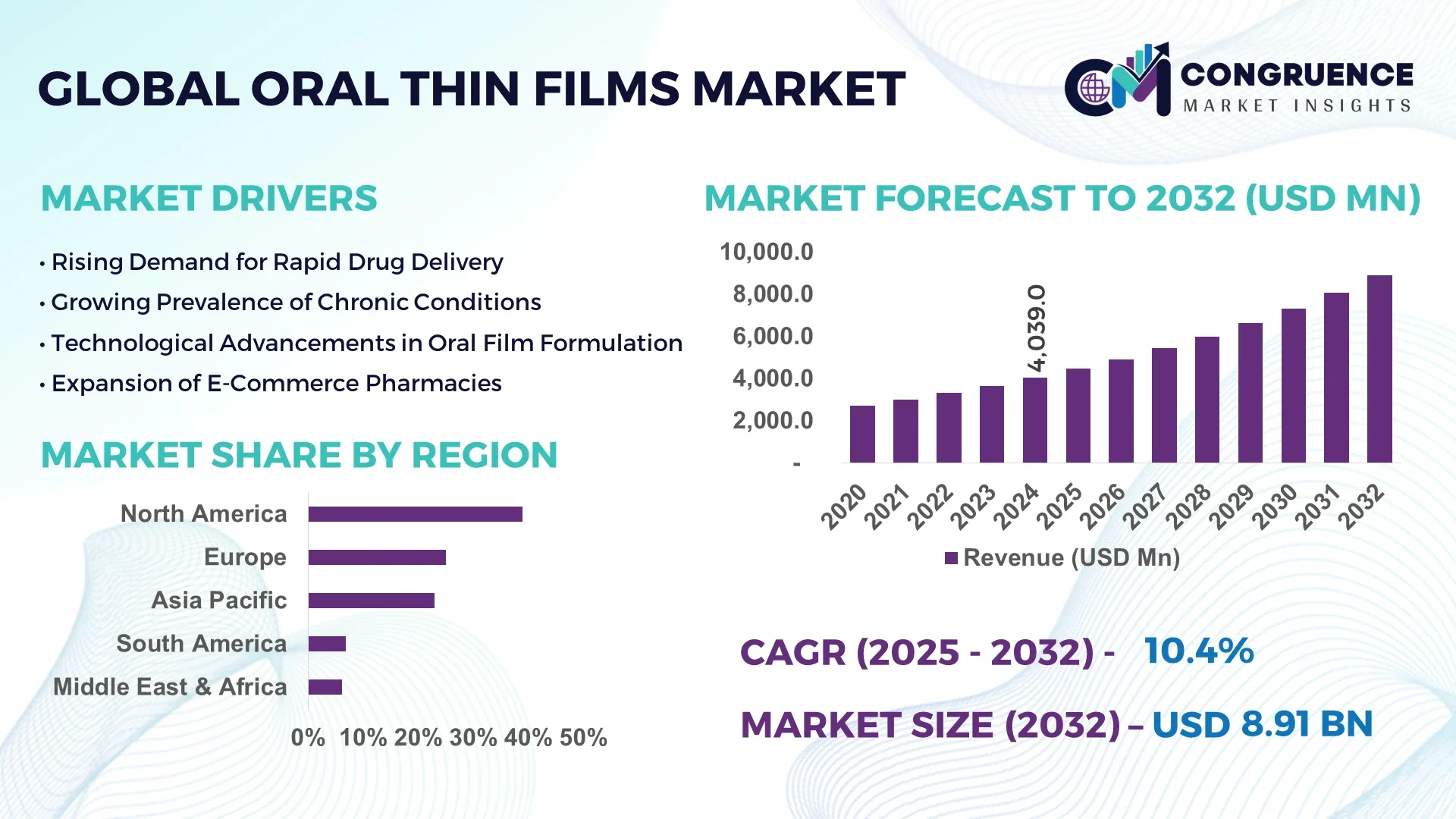

The Global Oral Thin Films Market was valued at USD 4,038.98 Million in 2024 and is anticipated to reach a value of USD 8,913.01 Million by 2032, expanding at a CAGR of 10.4% between 2025 and 2032.

In the United States, oral thin films are increasingly being utilized in the treatment of various chronic conditions, including pain management and opioid dependence. The market is driven by innovations in drug delivery systems, leading to improved patient compliance and rapid market expansion.

Oral thin films are rapidly gaining popularity due to their patient-friendly design, offering a convenient and effective alternative to traditional dosage forms like tablets and capsules. These films dissolve quickly in the mouth, allowing for rapid absorption of active ingredients through the oral mucosa, which can lead to faster onset of action. They are commonly used in applications such as pain management, neurological disorders, and opioid dependence treatment. With growing consumer demand for more efficient, easy-to-consume medications, oral thin films are revolutionizing the pharmaceutical landscape. Their potential for improved bioavailability, reduced side effects, and ease of use has attracted significant attention, making it a dominant player in the global pharmaceutical market.

Artificial Intelligence (AI) is making significant strides in transforming the Oral Thin Films market by enhancing the development and production of these films. AI algorithms are being used to accelerate the formulation process, ensuring that oral thin films are optimized for faster dissolution, better stability, and higher bioavailability. Additionally, AI is being applied in personalized medicine, where AI systems predict which formulations will be most effective for individual patients based on genetic data and health conditions. This allows pharmaceutical companies to create tailored solutions for pain management, neurological disorders, and other medical conditions, increasing the efficacy of treatments delivered via oral thin films. Moreover, AI tools are being employed in the manufacturing process to improve the quality control of oral thin films, reducing the chances of defects and increasing efficiency.

In the research and development phase, AI-driven simulations help to predict how different compositions will behave under various conditions, speeding up the process of formulation and improving the reliability of the final product. AI-powered data analytics are also crucial in the monitoring of patient responses to oral thin films, allowing healthcare providers to adjust doses or formulations in real-time for optimal patient outcomes. As AI continues to evolve, its role in oral thin films is set to grow even further, streamlining the production process, enhancing personalized treatment options, and ensuring higher standards of care for patients.

“In 2024, a leading oral thin film manufacturer integrated AI into their R&D phase, resulting in the development of a faster-dissolving oral film for migraine relief, improving patient satisfaction and medication adherence.”

Oral thin films are emerging as a preferred drug delivery system due to their ease of use, rapid absorption, and patient compliance. With a growing demand for more efficient and patient-friendly alternatives to traditional pill forms, oral thin films provide a solution to many challenges in pharmaceutical consumption. Their ability to rapidly dissolve and deliver drugs through the oral mucosa significantly reduces time to onset of action. The shift towards more effective delivery mechanisms is evident, with oral thin films being increasingly used in treatments for pain, neurological disorders, and opioid dependence.

The high cost of production for oral thin films is a significant restraint in the market. The specialized materials required for these films, along with advanced manufacturing processes, lead to higher costs compared to conventional drug delivery systems. Additionally, the need for sophisticated technologies and equipment for scaling production can deter smaller manufacturers from entering the market. As oral thin films require precise formulations and quality control measures, these costs contribute to price barriers that can limit their widespread adoption, particularly in developing regions.

The increasing demand for personalized medicines presents a significant opportunity for the oral thin films market. As pharmaceutical companies move towards more customized therapies tailored to individual genetic profiles and health conditions, oral thin films offer a practical solution for targeted drug delivery. These films can be designed to dissolve at specific rates or release drugs at precise intervals, making them ideal for personalized treatments. This trend is particularly noticeable in chronic disease management, where individualized treatment options are gaining traction.

Despite the growing potential of oral thin films, regulatory hurdles remain a challenge for market growth. The approval process for these drug delivery systems is often complex and time-consuming due to the need for rigorous testing to ensure safety and efficacy. Regulatory agencies such as the FDA have stringent guidelines for new drug delivery systems, and navigating these requirements can be costly and slow. This challenge is particularly evident for new market entrants, who face additional hurdles in meeting the standards set by health authorities across various regions.

• Rise in Demand for Patient-Centric Drug Delivery: The trend toward more patient-friendly, efficient drug delivery systems is contributing to the growth of the oral thin films market. Oral thin films offer a unique advantage over traditional tablets or capsules due to their quick dissolution and ease of use. This has led to increased adoption of these films in various therapeutic areas such as pain management, central nervous system disorders, and addiction treatment. Patients are increasingly seeking non-invasive, easy-to-consume alternatives, and oral thin films meet this demand effectively.

• Technological Advancements in Formulation: Advances in drug formulation technologies are driving growth in the oral thin films market. Companies are focusing on improving the stability and bioavailability of drugs through innovative technologies, such as nanoencapsulation and the use of dissolving polymers. This has significantly enhanced the efficacy of oral thin films, especially in areas like analgesics, where rapid action is required. Manufacturers are also exploring ways to incorporate multiple drugs into a single film for enhanced convenience.

• Focus on Cost-Effective Manufacturing: As demand for oral thin films rises, pharmaceutical manufacturers are increasingly adopting cost-effective manufacturing techniques. This includes the use of roll-to-roll processing technology, which allows for high-volume production at lower costs. These advancements are expected to make oral thin films more accessible to a broader consumer base, including in emerging markets. The growing emphasis on reducing production costs without compromising quality is a major factor that is shaping the market’s future.

• Regulatory Approvals and Expanding Product Portfolio: Regulatory bodies across the globe are beginning to approve a wider range of oral thin film products. As the market becomes more regulated, pharmaceutical companies are capitalizing on these approvals to introduce a broader range of oral thin film products. This is particularly evident in the approval of over-the-counter oral thin films for pain relief and other common ailments. These regulatory milestones are helping the market mature and gain traction globally, paving the way for further innovation and expansion.

The Oral Thin Films market is segmented by type, application, and end-user. Each segment plays a critical role in shaping the dynamics of the market. The key types include sublingual films, buccal films, and other film types, which vary in their method of dissolution and intended use. In terms of applications, oral thin films are used for a wide range of therapeutic purposes such as pain management, addiction treatment, and the treatment of neurological disorders. The market is also segmented by end-users, which include hospitals, clinics, and individual consumers. Understanding these segments helps to identify the leading and fastest-growing areas of the market, allowing for targeted strategies and investment opportunities.

The oral thin films market is divided into sublingual films, buccal films, and other film types. Sublingual films are the leading segment, capturing a significant share of the market due to their ability to dissolve quickly under the tongue, enabling fast absorption into the bloodstream. These films are primarily used for pain relief, including opioid dependence treatments, making them the most popular type in the market. Buccal films, which dissolve between the gum and cheek, are also growing rapidly, especially for drugs targeting chronic diseases and neurological conditions. The fastest-growing segment within the oral thin films market is multi-layer films, which are designed to provide controlled-release formulations. These films combine multiple active ingredients, enhancing their therapeutic potential by allowing the controlled delivery of drugs over time.

The oral thin films market is applied in several therapeutic areas, including pain management, opioid dependence, neurological disorders, mental health, and cancer treatments. The pain management segment is the largest and fastest-growing segment, driven by the increasing prevalence of chronic pain conditions such as arthritis and migraines. Oral thin films provide an efficient and fast-acting alternative to traditional painkillers. Opioid dependence is another key area where oral thin films are gaining popularity. They provide a non-invasive, easy-to-administer solution for individuals undergoing addiction treatment. The neurological disorders segment, including treatments for Alzheimer's and Parkinson's, is seeing significant growth due to the increasing demand for targeted drug delivery systems. Mental health treatments and cancer therapies are also expected to expand, as oral thin films provide an effective method for drug delivery with minimal side effects.

The oral thin films market serves multiple end-users, including hospitals, clinics, pharmacies, and individual consumers. Hospitals are the largest end-user segment, as they utilize oral thin films in pain management and treatment for addiction, especially in emergency settings. Clinics are rapidly adopting oral thin films for their convenience and ease of administration, particularly in outpatient care for chronic diseases. Pharmacies are seeing increasing demand for over-the-counter oral thin film products, including those for pain relief and oral health. The individual consumer segment is also growing as people seek over-the-counter, easy-to-use medications for common ailments. As more products become available, the individual consumer segment is expected to experience rapid expansion, particularly in the wake of growing consumer awareness and self-medication trends.

North America accounted for the largest market share at 39% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12% between 2025 and 2032.

The demand for oral thin films in North America is driven by increasing patient preferences for convenient drug delivery systems, especially in the U.S., where pain management and opioid dependence treatments are prevalent. However, Asia-Pacific's market is growing rapidly due to rising healthcare needs in emerging markets like India and China, where affordable, efficient, and non-invasive treatments are becoming increasingly sought after. These regions are focusing on adopting new drug delivery systems to cater to large populations with unmet healthcare needs.

Leading the Charge in Oral Thin Films Innovation

North America remains a dominant market for oral thin films, with the U.S. accounting for the largest share. The growing popularity of oral thin films is driven by their convenience, fast-acting properties, and ability to bypass the gastrointestinal tract, making them highly sought after for pain relief, addiction treatment, and more. Over-the-counter oral thin films for common ailments, like mouth ulcers and headache relief, are gaining traction across the region. The focus on regulatory approvals and advancements in drug formulation technology also supports the expansion of the market. The increasing prevalence of chronic diseases and aging population further boosts the demand for these films in the healthcare system.

A Hub for Advanced Drug Delivery Systems

Europe is witnessing significant growth in the oral thin films market, driven by innovations in drug delivery and an increasing demand for alternative treatments. Countries like Germany and the UK are at the forefront of market expansion due to the growing preference for non-invasive treatments and faster drug absorption methods. Europe’s regulatory environment is also favorable, with several approvals for oral thin film-based products, especially for pain relief and opioid dependence. Additionally, advancements in personalized medicine are spurring the demand for more tailored treatment options, and oral thin films provide an effective solution. As the healthcare sector in Europe focuses on improving patient compliance, oral thin films offer a promising method for achieving better therapeutic outcomes.

Rapid Growth and Increasing Adoption of Oral Thin Films

Asia-Pacific is expected to be the fastest-growing region in the oral thin films market, driven by increasing healthcare demands in emerging markets like China and India. The market growth in the region is supported by factors such as the rising burden of chronic diseases, increasing healthcare awareness, and the adoption of new drug delivery systems. The demand for oral thin films is rising rapidly due to their convenience, which is important in countries with large rural populations where access to healthcare can be limited. Local pharmaceutical companies are focusing on producing affordable oral thin film products to meet the needs of a growing middle class. Furthermore, improvements in healthcare infrastructure are helping drive market expansion.

Expanding Horizons for Convenient Medication Solutions

South America is gradually adopting oral thin films due to increasing awareness of advanced drug delivery systems. Countries like Brazil and Argentina are seeing a steady rise in the demand for oral thin films, driven by the rising prevalence of chronic diseases such as diabetes, hypertension, and pain-related conditions. Healthcare infrastructure improvements and the growing need for cost-effective treatments are further fueling the market. Over-the-counter oral thin films are becoming increasingly popular for minor ailments, creating a strong potential for market growth. Local manufacturers are entering the market with affordable solutions to cater to a large, underserved population seeking effective treatments.

Emerging Markets and Rising Healthcare Demand

The Middle East & Africa market for oral thin films is expanding as healthcare systems in countries like South Africa and Saudi Arabia continue to improve. There is increasing awareness about the benefits of oral thin films, particularly for pain relief and opioid dependency treatments. The growing demand for efficient drug delivery systems is contributing to the expansion of this market, especially in areas where oral administration is preferred due to cultural factors. Investments in healthcare infrastructure and the rising burden of chronic diseases are expected to further boost market growth. Local production of oral thin films is also growing as manufacturers look to offer cost-effective solutions to cater to diverse consumer needs across the region.

United States holds the highest market share at 32%. The dominance is due to the increasing adoption of advanced drug delivery systems and the growing healthcare infrastructure.

Germany holds the second-largest market share at 18%. The country’s strong pharmaceutical industry and significant investments in research and development contribute to its market leadership.

The global Oral Thin Films Market is highly competitive, with several key players constantly innovating and introducing new products to meet the growing demand for non-invasive drug delivery solutions. The market is characterized by the presence of both established pharmaceutical companies and emerging players. Key players focus on enhancing product offerings with advancements in drug formulation, improving patient compliance, and expanding their product portfolios. Companies are also investing in research and development to develop more efficient, fast-dissolving oral thin films for various therapeutic areas, including pain management, addiction treatment, and over-the-counter medications. The industry is also witnessing strategic collaborations and partnerships, particularly between pharmaceutical companies and contract manufacturing organizations, to meet the rising demand for oral thin films. Furthermore, companies are increasing their production capacity to cater to the growing demand in both developed and emerging markets. The ongoing trend toward healthcare system advancements and improving drug accessibility is also shaping the competitive landscape.

IntelGenx Technologies Corp.

LTS Lohmann Therapie-Systeme AG

Zuellig Pharma

Novartis AG

Indivior PLC

Medytox

Tetra Bio-Pharma

Pharmascience Inc.

The Oral Thin Films Market has witnessed significant technological advancements in recent years, primarily aimed at improving the efficacy, patient compliance, and convenience of drug delivery. The development of mucoadhesive films has gained considerable traction, allowing for better retention on mucosal surfaces, enhancing drug absorption and providing prolonged therapeutic effects. Additionally, innovations in film-forming technologies, such as solvent casting and hot-melt extrusion, are enabling more efficient production processes and increasing the versatility of oral thin films in various therapeutic areas.

New formulations using active pharmaceutical ingredients (APIs) are being introduced, offering targeted delivery for pain management, sleep disorders, and smoking cessation. With these innovations, oral thin films are becoming an attractive alternative to traditional drug delivery methods like tablets and injections. Furthermore, the integration of nanotechnology in the development of oral thin films is enhancing the bioavailability and dissolution rates of drugs. The continuous improvement of drug stability and taste-masking technologies is also contributing to increased patient satisfaction and compliance. As patient-centric drug delivery systems gain prominence, these technological advancements are expected to drive the future growth of the oral thin films market.

In January 2024, Awakn Life Sciencescompleted its investigation study AWKN-002 for the dissociative effect of a proprietary and patent-pending S-ketamine formulation administered sublingually via an oral thin film indicated for alcohol-use disorders.

In February 2024, CD Formulation, a pharmaceutical and biotechnology company, introduced Oral Thin Film Technology, a groundbreaking drug delivery system set to transform medication administration. This user-friendly method involves placing a thin film strip in the oral cavity, where it rapidly dissolves, delivering medication directly into the bloodstream.

In March 2024, Redwood Scientific Technologies Inc.announced an initiation plan to build oral thin manufacturing in the U.S. This initiative aims to make the company self-reliant by minimizing dependency on foreign-sourced pharmaceutical goods.

In May 2024, BIALintroduced KYNMOBI, the first and only sublingual film approved for the intermittent treatment of OFF episodes, addressing a critical unmet need for patients facing unpredictable symptoms.

The Oral Thin Films Market report provides a comprehensive analysis of the current and future landscape of oral thin films in various applications, including pharmaceutical, nutraceutical, and cosmetic industries. This report explores critical factors influencing the market, such as the technological advancements in drug delivery systems, increased demand for convenient dosage forms, and the growing trend of self-medication. Oral thin films are increasingly being recognized for their ability to improve bioavailability and provide faster onset of action compared to traditional solid dosage forms.

The market scope includes detailed insights into the leading regions, including North America, Europe, and Asia-Pacific, where oral thin films are gaining traction due to their ease of use and effectiveness in drug delivery. With the rising prevalence of chronic diseases, particularly in developing countries, the demand for oral thin films is expected to grow as patients seek more user-friendly methods of administering medication. Additionally, the report delves into the regulatory landscape, which plays a crucial role in the adoption of new products in the market.

Furthermore, the report examines key players in the oral thin films market, highlighting their strategic initiatives such as partnerships, product launches, and technological innovations. The study offers an in-depth look at market segmentation based on type, application, and end-user insights, providing a clear understanding of the opportunities and challenges in the market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 4038.98 Million |

|

Market Revenue in 2032 |

USD 8913.01 Million |

|

CAGR (2025 - 2032) |

10.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IntelGenx Technologies Corp., LTS Lohmann Therapie-Systeme AG, IntelGenx Technologies Corp., LTS Lohmann Therapie-Systeme AG, Zuellig Pharma, Novartis AG, Indivior PLC, IntelGenx Technologies Corp., LTS Lohmann Therapie-Systeme AG, Zuellig Pharma, Novartis AG, Indivior PLC, Medytox, Tetra Bio-Pharma, Pharmascience Inc., Medytox, Tetra Bio-Pharma, Pharmascience Inc., Zuellig Pharma, Novartis AG, Indivior PLC, IntelGenx Technologies Corp., LTS Lohmann Therapie-Systeme AG, Zuellig Pharma, Novartis AG, Indivior PLC, Medytox, Tetra Bio-Pharma, Pharmascience Inc., Medytox, Tetra Bio-Pharma, Pharmascience Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |