Reports

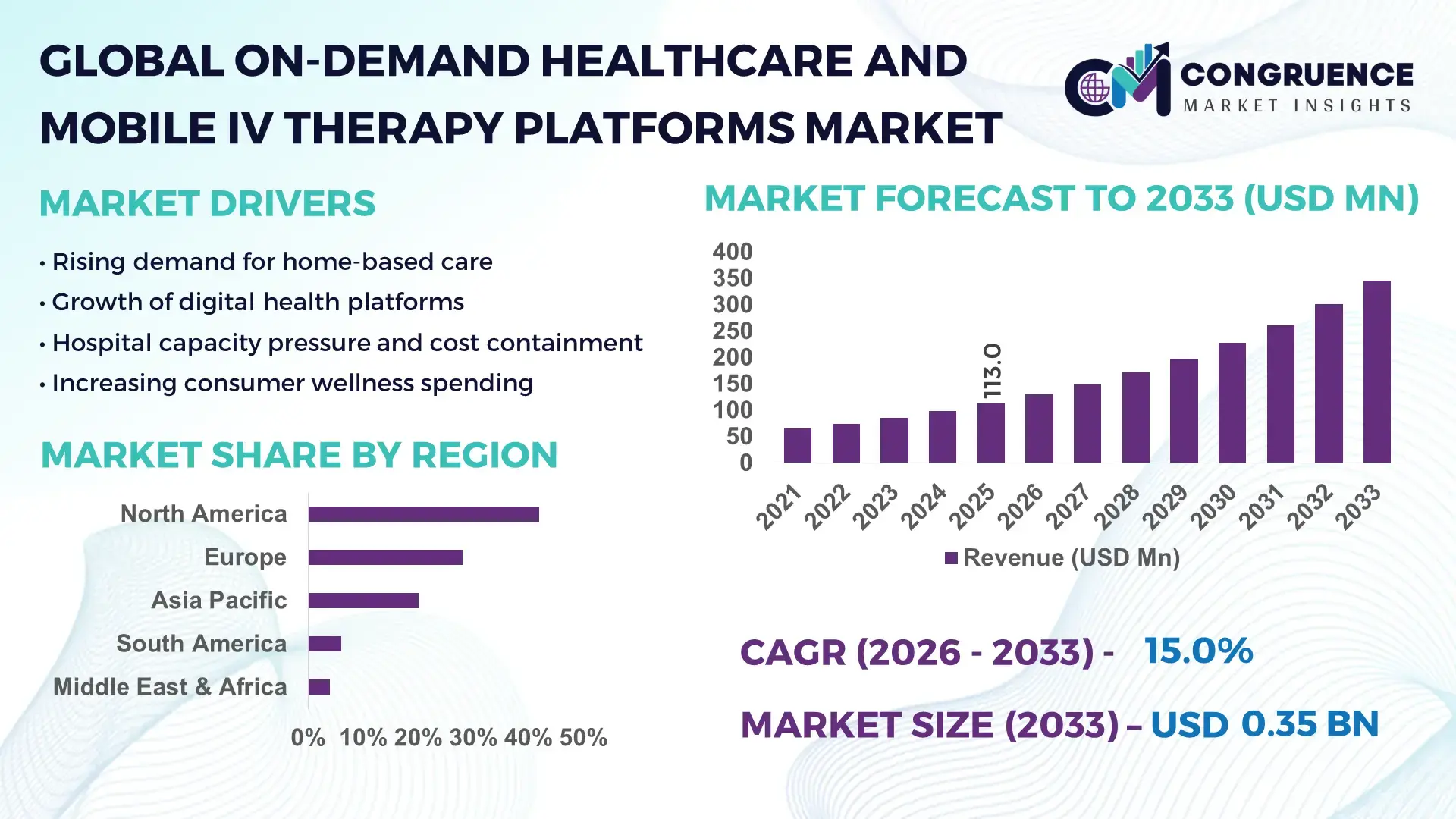

The Global On-Demand Healthcare and Mobile IV Therapy Platforms Market was valued at USD 113.0 Million in 2025 and is anticipated to reach USD 345.7 Million by 2033, expanding at a CAGR of 15% between 2026 and 2033, according to an analysis by Congruence Market Insights—driven by the rapid shift toward home-based, technology-enabled clinical delivery models that reduce hospital congestion and patient wait times.

The United States has built extensive nationwide dispatch capacity with more than 2,500 licensed mobile infusion vehicles integrated with digital triage platforms and pharmacy fulfillment hubs. Annual private investment in mobile care infrastructure exceeds USD 600 million, supporting 24/7 nurse networks, cold-chain logistics, and portable infusion devices. Over 320 hospitals now partner with third-party on-demand providers for overflow care, while employers across 18 states fund mobile IV benefits for roughly 1.2 million insured workers. Continuous monitoring wearables and AI routing systems are embedded in over 70% of leading service fleets, enabling real-time vitals tracking and predictive staffing.

Market Size & Growth: USD 113.0 Mn (2025) → USD 345.7 Mn (2033); ~15% CAGR, supported by rising preference for at-home clinical care.

Top Growth Drivers: telehealth integration 42%, hospital-to-home shift 37%, chronic-care demand 34%.

Short-Term Forecast: By 2028, average response time is projected to fall by 28% through AI dispatch.

Emerging Technologies: AI triage, portable smart pumps, remote vitals analytics, and blockchain medical records.

Regional Leaders (2033): North America ~USD 145 Mn (enterprise contracts), Europe ~USD 110 Mn (public–private pilots), Asia-Pacific ~USD 90 Mn (urban app adoption).

Consumer Trends: Higher uptake among working adults, post-surgery patients, and wellness users seeking rapid hydration.

Pilot Example (2024): A multi-city U.S. program cut ER diversion rates by 22% using mobile IV teams.

Competitive Landscape: Leading provider holds ~18% share; key players include ShiftMed, Remedy, Revitalize IV, and MedArrive.

Regulatory & ESG Impact: Stricter home-care standards and reduced patient travel emissions are accelerating adoption.

Investment Patterns: Over USD 480 Mn raised in the last three years, with growing insurer partnerships.

Innovation Outlook: Integration with wearables, autonomous routing, and pharmacy micro-fulfillment hubs.

On-demand platforms are increasingly anchored in home care (38%), corporate wellness (27%), and post-acute recovery (21%), while urgent care and travel medicine make up the remainder. Smart infusion pumps with automated dosing are being deployed in nearly 60% of new vehicles, and cloud EHR integration now covers 65% of providers. Regulators are tightening nurse-to-patient ratios and cold-chain protocols, while urban adoption in North America and Western Europe outpaces rural areas by roughly 1.8×. Growth is further propelled by insurance reimbursement pilots, same-day pharmacy fulfillment, and hybrid telehealth-mobile workflows.

The strategic relevance of the On-Demand Healthcare and Mobile IV Therapy Platforms Market lies in its ability to redesign care delivery around speed, cost efficiency, and patient convenience while relieving overstretched hospital systems. Health systems globally are shifting from centralized treatment to distributed, tech-enabled care networks that combine tele-triage, mobile clinicians, and data-driven decisioning. In many metropolitan areas, mobile-first care is now treated as an extension of hospital capacity rather than a niche wellness service.

From a performance standpoint, AI-based triage and routing delivers 30–35% faster clinician dispatch compared to traditional call-center scheduling, reducing idle time and improving utilization of nursing resources. Smart infusion pumps with automated dosing and digital audit trails cut medication errors by 18–22% versus older manual drip systems, strengthening clinical safety and compliance.

Regionally, North America dominates in service volume, driven by dense urban logistics networks, while Europe leads in structured adoption, with roughly 32% of large healthcare providers formally integrating third-party mobile IV partners into care pathways. In Asia-Pacific, rapid smartphone penetration and super-app ecosystems are accelerating app-based bookings, particularly in Japan, Singapore, and South Korea.

In the short term (by 2028), predictive workforce planning powered by machine learning is expected to reduce missed appointments and scheduling inefficiencies by 25%, while remote patient monitoring integration should lower avoidable ER visits by 15–20% for participating patients.

On the ESG front, firms are committing to measurable sustainability goals such as a 25% reduction in patient travel emissions by 2030 through home-based care and electric vehicle fleets. Many providers are also targeting 40% recyclable packaging for IV kits by 2029.

A micro-scenario illustrates impact: In 2024, a multi-state U.S. mobile provider deployed AI routing and achieved a 27% reduction in average response time and a 19% drop in nurse overtime hours, improving both patient outcomes and operating efficiency.

Looking ahead, the market is positioned as a pillar of resilient, compliant, and sustainable healthcare delivery—blending clinical rigor with digital agility to build a more accessible, decentralized, and patient-centric care ecosystem.

The On-Demand Healthcare and Mobile IV Therapy Platforms Market is shaped by converging trends in digital health, home-based care, and logistics innovation. Rising hospital crowding, workforce shortages, and consumer demand for convenience are accelerating the shift from facility-centric to mobile-first clinical models. Telehealth triage is increasingly used as a gateway to mobile services, enabling rapid assessment before dispatch. Simultaneously, insurers and employers are piloting reimbursement and benefit programs that legitimize mobile IV as part of standard care. Technological advances—smart pumps, wearable monitoring, and AI routing—are improving safety, efficiency, and scalability. Regulatory oversight is tightening around nurse licensure, medication handling, and cold-chain compliance, raising operational standards. Urban density favors rapid deployment, while rural expansion depends on partnerships with local clinics and pharmacies. Competition is intensifying as healthcare providers, logistics firms, and tech platforms enter the space, pushing innovation, consolidation, and service differentiation.

The acceleration of home-based care is a primary growth driver for the market. Aging populations and chronic disease prevalence are increasing the need for convenient, non-hospital treatment options. In the U.S., nearly 60% of post-acute patients now prefer recovery at home rather than in facilities, creating consistent demand for mobile infusion and monitoring services. Hospitals are diverting lower-acuity cases to mobile providers to free up beds, with some systems redirecting 15–25% of non-critical visits to home care pathways. Employers are also incorporating mobile IV and urgent care into wellness benefits, covering more than 1 million workers across multiple states. Technological enablers—portable infusion pumps, remote vitals tracking, and secure EHR integration—have reduced clinical risk, making home treatment more acceptable to regulators and insurers. Moreover, shorter response times and same-day service are improving patient satisfaction scores, which are increasingly tied to reimbursement metrics. As trust in remote clinical delivery strengthens, utilization rates continue to climb across urban and suburban markets.

Regulatory fragmentation across states and countries constrains rapid scaling of mobile IV services. Licensing requirements for nurses vary widely, forcing providers to maintain multiple state-specific compliance frameworks and increasing administrative costs. Medication handling rules—particularly for controlled substances—impose strict cold-chain, documentation, and storage protocols that add logistical complexity to mobile operations. Some jurisdictions still classify mobile IV as a non-essential wellness service, limiting insurance reimbursement and slowing adoption among mainstream healthcare systems. Data privacy regulations such as HIPAA in the U.S. and GDPR in Europe require robust cybersecurity investments, which smaller providers struggle to afford. Additionally, lack of standardized clinical guidelines for mobile infusion creates hesitancy among hospitals to formalize partnerships. Vehicle regulations, zoning restrictions for medical parking, and cross-border nurse credentialing further complicate expansion. These regulatory barriers raise operating costs, limit geographic reach, and slow market penetration despite strong underlying demand.

Deep integration with telehealth platforms creates significant growth opportunities by enabling seamless end-to-end care pathways. Virtual consultations can triage patients in minutes, determining whether mobile IV is appropriate before dispatch, which improves resource allocation and reduces unnecessary visits. Major telehealth providers are beginning to partner with mobile care networks, expanding access to millions of existing users. In urban centers, hybrid telehealth–mobile models are reducing emergency department utilization by up to 20% for non-critical cases. Integration also allows real-time data sharing between clinicians, pharmacies, and insurers, streamlining authorization and reimbursement. Wearable devices connected to telehealth dashboards can trigger automated mobile responses when vitals cross predefined thresholds. Furthermore, partnerships with retail pharmacies enable rapid medication fulfillment and last-mile delivery, shortening service timelines. As health systems pursue value-based care, telehealth-linked mobile services offer measurable improvements in patient outcomes, adherence, and cost efficiency.

Persistent shortages of qualified nurses and paramedical staff pose a major operational challenge. Competition with hospitals and clinics drives up wages, while mobile work requires additional training in autonomous field operations and digital documentation. Staffing constraints can lead to service delays, particularly during peak demand periods such as weekends or flu seasons. Logistics costs further strain profitability, as providers must maintain specialized vehicles, medical equipment, cold-chain storage, and real-time tracking systems. Fuel, maintenance, and insurance expenses are rising, especially in urban markets with heavy traffic. Coordinating pharmacy fulfillment, clinician scheduling, and route optimization adds complexity to operations. Rural and semi-urban areas present additional hurdles due to longer travel times and lower patient density, making service economically less viable. Without scale, smaller providers struggle to balance quality, speed, and cost, limiting market expansion despite strong consumer interest.

Faster response through AI-enabled dispatch (20–30% improvement): Leading providers are deploying machine-learning routing systems that cut average arrival times from 90 minutes to 60–70 minutes, while improving vehicle utilization rates to 78–82%. Real-time traffic analytics and predictive demand models are reducing missed appointments and idle time, particularly in dense urban corridors.

Smart infusion devices reducing clinical risk by 18–22%: Next-generation portable pumps with automated dosing, barcode verification, and digital audit trails are now used in roughly 60% of new mobile fleets. These systems lower medication errors, shorten setup time by 15–18%, and generate instant compliance records for insurers and regulators.

Expansion of insurer-backed mobile care pilots (coverage up 35%): More than 25 U.S. health plans are testing reimbursement for mobile IV and urgent care, increasing eligible patient pools by 30–35% since 2023. Early results show 12–17% lower costs versus traditional ER visits for low-acuity cases.

Rise in Modular and Prefabricated Construction for mobile infrastructure: Modular outfitting of medical vehicles and micro-clinics is reshaping deployment speed in the market. Around 55% of new mobile projects report cost benefits from prefabricated interiors, standardized cabinets, and pre-installed equipment bays. Off-site automated fabrication of wiring, plumbing, and storage modules has reduced vehicle build time by 25–30% and labor hours by 20–22%, accelerating fleet rollouts across Europe and North America.

The On-Demand Healthcare and Mobile IV Therapy Platforms Market is structured around three core lenses—type, application, and end-user—that together explain how services are delivered, where they are deployed, and who ultimately consumes them. By type, the market spans clinical service models, digital coordination platforms, and equipment-enabled mobile delivery, reflecting a blend of medical and technology capabilities. Application segmentation is driven by acuity levels ranging from wellness hydration to post-acute recovery and urgent care diversion, with rising integration into chronic disease management pathways. End-user segmentation highlights a clear shift from purely consumer wellness toward institutional adoption by hospitals, insurers, and employers. Urban density, digital readiness, and reimbursement frameworks strongly influence regional deployment patterns, while interoperability with electronic health records increasingly shapes platform design. Overall, segmentation reveals a market moving from fragmented pilots to standardized, scalable care networks that align mobile clinical delivery with mainstream healthcare systems.

The market is broadly segmented into Platform-Led Services, Clinician-Led Mobile Care, and Equipment-First Mobile Systems, with Platform-Led Services emerging as the leading type. Platform-led models currently account for 44% of total market usage, driven by AI-based dispatch, real-time logistics, and integrated tele-triage that reduce response times and improve workforce utilization. In contrast, Clinician-Led Mobile Care represents about 28%, relying more heavily on nurse autonomy and local partnerships rather than centralized digital orchestration. However, Equipment-First Mobile Systems are the fastest-growing type at roughly 17% CAGR, propelled by the rapid adoption of smart infusion pumps, portable diagnostics, and wearable monitoring devices that allow safer, protocol-driven care outside hospitals.

Clinician-led models remain critical in rural and semi-urban areas where local trust and relationships matter more than digital scale, while Equipment-First systems are gaining traction in urban centers due to precision dosing and automated compliance records. The remaining segment—hybrid models that blend platform coordination with clinician discretion—collectively accounts for about 28% of the market, serving as a bridge between fully automated and fully human-driven care.

Applications in this market span Wellness Hydration, Post-Acute Recovery, Urgent Care Diversion, Chronic Disease Support, and Travel/Occupational Care. Post-Acute Recovery is the leading application at 40% share, as hospitals increasingly rely on mobile IV services to manage pain control, hydration, and medication delivery after discharge, reducing readmission risk and freeing inpatient beds. Urgent Care Diversion holds around 26%, serving low-acuity cases that would otherwise visit emergency departments.

The fastest-growing application is Chronic Disease Support at about 18% CAGR, driven by rising prevalence of conditions requiring periodic infusion, remote monitoring, and home-based clinical oversight. Wellness Hydration remains popular among working professionals and athletes but is gradually becoming more clinically standardized. Travel and occupational care together represent roughly 14% of the market, supported by corporate wellness programs and onsite medical services at large facilities.

Consumer adoption is accelerating: in 2025, over 36% of urban households reported using at least one on-demand mobile healthcare service, while 58% of working adults expressed higher trust in providers that combine telehealth triage with in-home treatment. Meanwhile, 41% of U.S. hospitals are piloting mobile care partnerships to manage overflow and reduce ER congestion.

Hospitals and health systems are the leading end-user segment at 38% share, as they increasingly contract mobile providers to manage post-discharge care, reduce readmissions, and handle low-acuity cases outside emergency departments. Corporate employers represent about 24%, using mobile IV and urgent care benefits to reduce employee downtime and improve productivity.

The fastest-growing end-user group is insurance providers at approximately 19% CAGR, fueled by pilots that demonstrate cost savings versus traditional ER visits and by value-based care models that reward home-based treatment. Individual consumers account for around 20%, primarily for wellness hydration and travel-related care, while government and community health programs together contribute roughly 18%, especially in disaster response and underserved regions.

Industry adoption is deepening: 44% of large hospital networks now use some form of mobile care partnership, and 39% of Fortune 500 firms offer telehealth-linked mobile services in their benefits packages. Among younger consumers, 62% of Gen Z and Millennials prefer brands that provide app-based scheduling with real-time clinician tracking.

North America accounted for the largest market share at 42% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 17% between 2026 and 2033.

The global landscape is increasingly shaped by urban density, digital health readiness, and reimbursement frameworks that determine how quickly mobile clinical models can scale. In 2025, North America led with over 2,500 active mobile IV fleets, 320+ hospital partnerships, and more than 1.2 million employer-covered users across 18 states. Europe followed with roughly 28% of global volume, driven by public–private pilots, standardized nurse credentialing, and sustainability mandates that prioritize home-based care over facility visits. Asia-Pacific represented about 20% of deployments but showed the steepest expansion as super-app ecosystems, telehealth penetration, and pharmacy-led logistics networks accelerated last-mile care. South America contributed approximately 6%, concentrated in Brazil and Argentina where urban telemedicine adoption is rising alongside private insurance coverage. The Middle East & Africa held around 4%, anchored by UAE smart-health initiatives and mining/oil-field medical logistics in South Africa, with rapid digital modernization boosting mobile readiness across Gulf cities.

North America remains the most mature market with roughly 42% share in 2025, supported by dense urban logistics, advanced reimbursement pilots, and deep integration between hospitals, insurers, and mobile providers. Health systems across the U.S. and Canada increasingly rely on mobile IV teams to manage post-acute care, divert low-acuity ER visits, and reduce readmissions, with more than 320 hospitals formally partnering with third-party platforms. Employer-sponsored wellness programs cover over 1.2 million workers, making corporate benefits a major demand driver alongside chronic disease management and post-surgical recovery. Regulatory momentum is also favorable: multiple U.S. states have clarified scope-of-practice rules for mobile nurses, while federal interoperability standards have accelerated real-time EHR data exchange. Technologically, AI dispatch, wearable monitoring, and smart infusion pumps are now standard in 70%+ of leading fleets, cutting setup times by nearly 15–18% and improving clinical safety. Local players such as MedArrive have expanded multi-state networks that combine tele-triage with mobile visits, while ShiftMed has invested heavily in digital workforce coordination. Consumer behavior skews toward higher enterprise adoption, particularly in healthcare and finance, where employers prioritize rapid, app-based clinical access to minimize productivity losses.

Europe holds about 28% of global volume in 2025, with Germany, the UK, and France as leading markets. Germany’s strong hospital digitization agenda and the UK’s NHS-backed home-care pilots have normalized mobile infusion for post-acute recovery and chronic care. France has emphasized integration with community pharmacies and district nurses, expanding last-mile reach into semi-urban areas. Regulatory bodies such as the European Medicines Agency (EMA) and national health authorities are tightening cold-chain and data-privacy standards, pushing providers toward explainable AI, auditable digital records, and greener logistics. Sustainability initiatives—electric medical vehicles, recyclable IV packaging, and reduced patient travel—are reshaping fleet design and procurement. Emerging technologies include portable diagnostics, remote vitals analytics, and standardized smart pumps that sync directly with hospital EHRs. Local players like Doctolib in France are experimenting with telehealth-to-home clinical pathways, while UK-based home-care networks are integrating pharmacy fulfillment into mobile workflows. European consumers are more compliance-driven than convenience-driven; regulatory pressure creates demand for transparent, explainable digital care platforms, and patients show higher trust when clinical data governance is visible.

Asia-Pacific ranks as the fastest-expanding region by volume, now representing roughly 20% of global deployments, with China, India, and Japan as top consuming countries. Rapid smartphone penetration, dense urban populations, and pharmacy-led logistics networks are accelerating mobile clinical models. In China, hospital overcrowding has pushed private platforms to deploy city-based mobile teams linked to digital triage apps. India’s growth is concentrated in Tier-1 cities where teleconsultation and pharmacy delivery are converging into hybrid care models. Infrastructure trends include modular outfitting of medical vans, shared micro-fulfillment hubs, and integration with e-pharmacy ecosystems. Innovation hubs in Singapore, Tokyo, and Shenzhen are piloting AI routing, wearable monitoring, and cloud-based medical records tailored for mobile care. Local players such as Ping An Good Doctor and Practo are expanding telehealth-to-home services, while Japanese providers are standardizing portable infusion devices for aging populations. Fleet density in major metros has increased by over 30% since 2023, reducing average response times to under 70 minutes. Consumer behavior is highly app-centric: growth is driven by e-commerce habits and mobile AI apps, with users expecting same-day scheduling, real-time tracking, and digital payment integration.

South America accounts for about 6% of the global market, led by Brazil and Argentina. Brazil dominates regional activity due to its large private healthcare system, growing telemedicine adoption, and expanding pharmacy delivery networks in São Paulo and Rio de Janeiro. Argentina follows with rising urban mobile services tied to private insurers and employer wellness programs. Infrastructure development—particularly in cold-chain logistics and digital patient records—is gradually enabling safer mobile IV operations. Government incentives for digital health modernization in Brazil have improved interoperability between hospitals and mobile providers, while Argentina is exploring reimbursement pilots for home-based care. Energy and mining sectors in Chile and Peru are also creating demand for onsite medical services at remote sites, where mobile IV capabilities reduce emergency evacuations. Local players such as Brasil’s Docway are integrating teleconsultations with mobile clinician dispatch. Consumer behavior reflects strong demand for media and language-localized digital platforms, with patients favoring Portuguese and Spanish interfaces, video-based triage, and WhatsApp-style scheduling.

The Middle East & Africa region represents roughly 4% of global activity, with the UAE and South Africa as key growth markets. In the Gulf, demand is fueled by smart-city initiatives, luxury wellness services, and large-scale events that require rapid medical response. Oil and gas operations in Saudi Arabia and Qatar are adopting mobile clinical units for remote workforce safety and emergency preparedness. Technological modernization is advancing through cloud-based medical records, AI routing, and wearable monitoring integrated with national digital health platforms. The UAE’s Ministry of Health has supported pilot programs that standardize mobile care protocols, while free-trade zones in Dubai are attracting foreign mobile health providers. In South Africa, mining and construction industries rely on mobile medical units to serve remote sites, while urban telehealth partnerships are expanding access in Johannesburg and Cape Town. Fleet electrification and solar-powered cold storage are emerging sustainability trends. Consumer behavior varies widely: in the Gulf, affluent users favor premium concierge-style mobile care, while in Africa demand is more cost-sensitive and oriented toward employer-sponsored onsite services and community health outreach.

United States — 38% Market Share: Strong hospital partnerships, advanced digital health infrastructure, and insurer-backed pilots accelerate nationwide scaling.

Germany — 14% Market Share: Rigorous regulatory standards, high healthcare digitization, and well-developed home-care networks drive consistent adoption.

The On-Demand Healthcare and Mobile IV Therapy Platforms Market is highly fragmented, with an estimated 110–130 active providers globally ranging from local boutique IV services to multi-state mobile care networks and digital health platforms. Competition is driven less by price and more by speed of response, clinical safety, network coverage, and interoperability with hospitals and insurers. The top five players collectively account for roughly 30–35% of the market, while hundreds of regional operators serve city-level or state-level niches, creating a long-tail structure with continuous entry and consolidation.

Strategic positioning revolves around three models: (1) platform-led networks that optimize dispatch with AI and logistics analytics; (2) clinician-first providers emphasizing nursing quality and partnerships with hospitals; and (3) equipment-centric firms that differentiate through smart infusion devices and remote monitoring. Over the last 24 months, competition has intensified through partnerships with insurers (value-based care pilots), hospital system contracts, and retail-pharmacy alliances for same-day medication fulfillment.

M&A activity is rising as digital health firms acquire mobile providers to add “care at home” capabilities to telehealth ecosystems. Fleet modernization—electric vehicles, modular interiors, and IoT-enabled cold storage—has become a key differentiator. At the same time, cybersecurity investments and real-time EHR integration are emerging as table stakes. Innovation is shifting from basic hydration services toward complex care (antibiotics, biologics, post-surgical infusions, and remote monitoring bundles), raising clinical barriers to entry and favoring scaled players with standardized protocols.

MedArrive

Revitalize IV

IVme Wellness

Remedy IV

Thrive IV

The I.V. Doc

Mobile IV Nurses

Drip Hydration

Masimo

Philips

Doctolib

Practo

Technology is rapidly transforming mobile clinical delivery from a logistics service into a data-driven care network. AI-powered dispatch systems now combine demand forecasting, traffic analytics, and clinician availability to cut average response times by roughly 20–30% in major metros while lifting fleet utilization above 80%. These platforms integrate with hospital EHRs, enabling real-time chart updates, automated documentation, and audit-ready records that reduce administrative burden and compliance risk.

On the clinical side, smart infusion pumps with barcode medication verification, automated dosing limits, and digital logs are becoming standard in more than 60% of new mobile fleets. These devices are paired with wearable biosensors that stream continuous vitals (heart rate, oxygen saturation, temperature) to cloud dashboards, allowing remote oversight and early intervention. Predictive analytics flag deterioration before symptoms escalate, supporting safer home-based care.

Tele-triage and virtual assessment platforms are increasingly used as the entry point to mobile services, filtering inappropriate cases and routing only clinically suitable patients to field teams. This reduces unnecessary visits and improves workforce efficiency. Meanwhile, IoT-enabled cold-chain containers track temperature and tampering in real time, ensuring medication integrity during transport.

Fleet technology is also evolving: electric medical vehicles, modular interiors, and quick-swap equipment bays are shortening deployment cycles and lowering operating costs. In parallel, drone logistics pilots are emerging for last-mile delivery of medications and supplies to remote sites, cutting delivery times from hours to minutes in select corridors.

Connectivity upgrades—5G, edge computing, and secure APIs—are enabling high-resolution data streaming from vehicles to command centers. Cybersecurity frameworks aligned with HIPAA/GDPR are being embedded into platform architecture. Finally, digital consent tools, automated billing workflows, and insurer portals are accelerating reimbursement cycles and reducing claims friction, making technology a core competitive lever.

• In June 2025, DispatchHealth completed its merger with Medically Home, forming one of the largest hospital-at-home and complex care delivery platforms. The combined organization now operates in more than 20 U.S. states, supports over 50 enterprise customers, and delivers everything from emergency-alternative care to hospital-level services and transitional care in patients’ homes. Source: www.dispatchhealth.com

• In October 2025, DocGo acquired virtual care provider SteadyMD and expanded its telehealth-to-mobile care footprint across all 50 U.S. states. The integration adds SteadyMD’s nationwide clinician network and real-time matching technology, expected to serve over 3 million patients in 2025, enhancing DocGo’s combined mobile and virtual healthcare services. Source: www.docgo.com

• In November 2025, DocGo announced the upcoming launch of Longitudinal Care Services with a major California health plan, combining mobile clinical visits and telehealth tools to support preventative and chronic care for roughly 10,000 underserved plan members beginning Q4 2025. Source: www.docgo.com

• In 2025, Zipline expanded its global healthcare logistics operations through partnerships that scale autonomous medical supply delivery via drones. The U.S. State Department committed up to $150 million to Zipline to expand medical drone delivery services across five African countries (Rwanda, Ghana, Nigeria, Kenya, and Côte d’Ivoire), representing a first-of-its-kind performance-linked aid model that could support up to $400 million in new business. Source: www.axios.com

This report covers the full ecosystem of on-demand, home-based, and mobile clinical delivery models that combine digital coordination platforms with in-person medical services and portable medical technologies. The scope spans service types (platform-led networks, clinician-led care, and equipment-centric models), applications (wellness hydration, post-acute recovery, urgent care diversion, chronic disease support, occupational care, and travel medicine), and end-users (hospitals, insurers, employers, individual consumers, and public health agencies).

Geographically, the report analyzes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing differences in regulatory frameworks, reimbursement models, urban density, and digital health maturity. Urban markets are examined separately from rural and remote settings due to distinct logistics and economics. Country-level deep dives include the United States, Germany, the United Kingdom, France, China, India, Japan, Brazil, Argentina, the UAE, and South Africa.

Technologically, the scope includes AI dispatch systems, tele-triage platforms, smart infusion pumps, wearable biosensors, IoT cold-chain logistics, electric medical fleets, and drone delivery pilots, along with cybersecurity and interoperability standards. The report also evaluates integration with hospital EHRs, pharmacy networks, and insurer portals.

Industry focus areas include hospital overflow management, value-based care pilots, employer wellness programs, disaster response, and remote site medical support (e.g., mining and oil & gas). Emerging niches such as home biologics administration, antibiotic infusions, and post-surgical monitoring are assessed alongside traditional hydration services.

Operational aspects—fleet design, modular medical vans, clinician staffing models, and supply-chain resiliency—are analyzed to highlight scalability constraints and investment priorities. Finally, the report maps regulatory compliance, data governance, and sustainability initiatives (EV fleets, recyclable packaging, reduced patient travel) that are reshaping market strategy and long-term adoption.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 113.0 Million |

| Market Revenue (2033) | USD 345.7 Million |

| CAGR (2026–2033) | 15% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | DispatchHealth, DocGo, Zipline, MedArrive, Revitalize IV, IVme Wellness, Remedy IV, Thrive IV, The I.V. Doc, Mobile IV Nurses, Drip Hydration, Masimo, Philips, Doctolib, Practo |

| Customization & Pricing | Available on Request (10% Customization Free) |