Reports

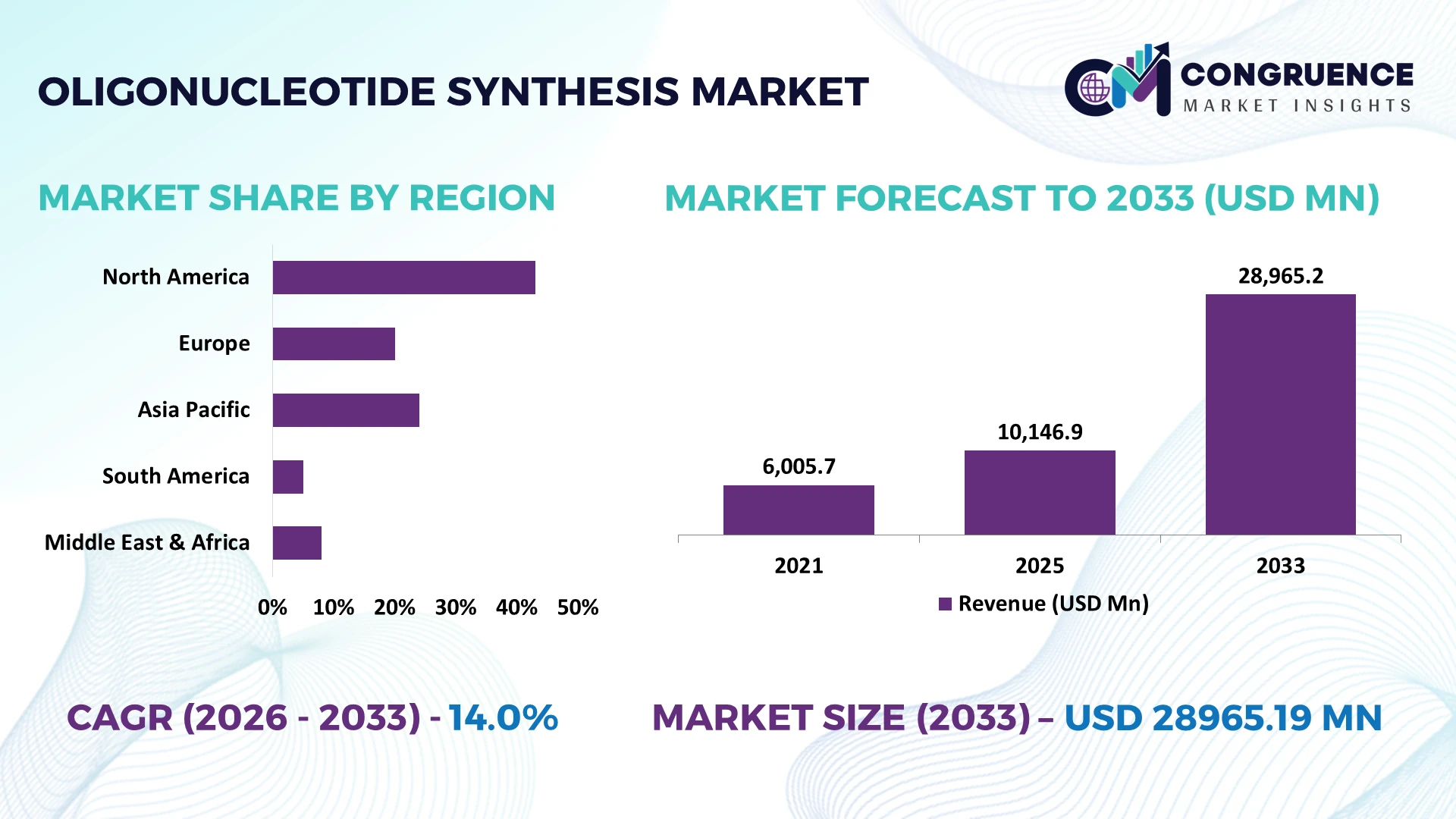

The Global Oligonucleotide Synthesis Market was valued at USD 10146.89 Million in 2025 and is anticipated to reach a value of USD 28965.19 Million by 2033 expanding at a CAGR of 14.01% between 2026 and 2033. Growth is being accelerated by expanding RNA therapeutics pipelines, precision medicine programs, automated high-throughput synthesis platforms, and increasing GMP-grade oligonucleotide manufacturing for clinical and commercial applications.

The United States leads the global oligonucleotide synthesis market with approximately 39% of global manufacturing capacity, supported by multi-billion-dollar investments in biotechnology, advanced genomic research, and pharmaceutical innovation. Compared with Germany, which accounts for nearly 9% of production capacity, the U.S. benefits from stronger clinical trial activity and broader adoption of automated synthesis systems exceeding 70% across leading facilities. Ongoing biotechnology supply-chain localization initiatives following global healthcare resilience programs further reinforce production stability and long-term competitiveness.

Organizations expanding manufacturing capacity, securing regional supply networks, and investing in advanced synthesis automation are positioned to strengthen competitive advantage in the evolving global oligonucleotide synthesis market.

Market Size & Growth: USD 10146.89 Million (2025) to USD 28965.19 Million (2033) at 14.01% CAGR, driven by expanding RNA therapeutics and automated synthesis technologies.

Top Growth Drivers: Therapeutic pipeline expansion (+28%), automated synthesis adoption (+35%), and GMP manufacturing investments (+24%) accelerate global market momentum.

Short-Term Forecast: By 2028, automated production is expected to improve synthesis efficiency by 30% while reducing manufacturing turnaround time by nearly 20%.

Emerging Technologies: AI-driven sequence optimization, robotic synthesis platforms, and advanced purification systems improve yield, scalability, and process consistency.

Regional Leaders: North America exceeds USD 11 Billion, Europe approaches USD 7 Billion, and Asia-Pacific surpasses USD 8 Billion through expanding biotechnology manufacturing and regional capacity investments.

Consumer/End-User Trends: More than 65% of demand originates from pharmaceutical and biotechnology companies developing gene therapies and precision medicine products.

Pilot/Case Example: A 2025 automated synthesis deployment improved batch productivity by approximately 27% while reducing process deviations by 18%.

Competitive Landscape: Leading manufacturers collectively control nearly 45% market share, with Thermo Fisher Scientific, Danaher, Merck KGaA, Eurofins Genomics, and LGC Biosearch Technologies maintaining strong positions.

Regulatory & ESG Impact: Sustainable solvent optimization lowers chemical waste by nearly 22%, while stricter quality compliance strengthens global manufacturing reliability.

Investment & Funding: More than USD 3 Billion in strategic investments supports manufacturing expansion, partnerships, and regional supply-chain diversification.

Innovation & Future Outlook: Next-generation enzymatic synthesis, digital manufacturing, and continuous production platforms accelerate commercialization and strengthen long-term industry competitiveness.

The Oligonucleotide Synthesis Market is advancing through rising demand from gene editing, RNA therapeutics, molecular diagnostics, and personalized medicine programs. Automated synthesis and high-purity manufacturing technologies now improve production efficiency by nearly 30%, while regional manufacturing expansion strengthens supply resilience amid evolving regulatory expectations. These developments reinforce long-term commercialization opportunities and set the foundation for the strategic market analysis that follows.

The Oligonucleotide Synthesis Market has become strategically important as pharmaceutical companies, contract development organizations, and biotechnology firms accelerate investments in RNA therapeutics, gene editing, and molecular diagnostics. Supply-chain restructuring since the pandemic has shifted procurement toward localized GMP manufacturing and dual-source strategies, reducing dependence on single-country production while improving resilience for clinical and commercial programs.

Modern automated synthesis platforms generate up to 35% higher throughput while reducing reagent consumption by nearly 20% compared with conventional batch-oriented systems, enabling lower production costs and greater batch consistency. The United States remains the largest innovation hub through advanced biopharmaceutical manufacturing, whereas Singapore is expanding rapidly by combining government-backed biotechnology infrastructure with faster deployment of high-value manufacturing assets. Over the next two to three years, automated synthesis is expected to account for more than 60% of new production line installations, supported by increasing digital quality management and process monitoring.

A practical example is the deployment of continuous oligonucleotide manufacturing integrated with automated purification, enabling faster release cycles and improved production flexibility for therapeutic developers. Companies are responding through strategic partnerships, manufacturing expansion, and digital process investments that strengthen supply reliability. Organizations capable of combining scalable production, regulatory compliance, and advanced automation will secure stronger competitive positioning across the global oligonucleotide synthesis value chain.

Rapid expansion of RNA therapeutics, antisense drugs, and gene-editing research is reshaping manufacturing priorities across the oligonucleotide synthesis market. More than 65% of advanced development programs now require high-purity synthetic oligonucleotides, while automated production platforms improve manufacturing throughput by approximately 30% and reduce batch variability by nearly 25%. The United States continues expanding domestic biopharmaceutical manufacturing to strengthen critical healthcare supply chains, encouraging new production investments. In response, leading companies are increasing GMP manufacturing capacity, integrating digital quality control, and forming strategic partnerships with pharmaceutical innovators. This structural transition improves manufacturing resilience while creating faster commercialization pathways for high-value therapeutic applications.

Production economics remain constrained by expensive specialty reagents, complex purification requirements, and dependence on high-quality phosphoramidite supply chains. Raw materials represent nearly 40% of manufacturing costs in many facilities, while quality-control activities can account for approximately 20% of total production time. Supply disruptions affecting specialty chemicals have increased procurement complexity for manufacturers operating global production networks. Companies are responding by localizing critical material sourcing, securing long-term supplier agreements, and qualifying alternative vendors to reduce operational exposure. Organizations with diversified procurement strategies achieve greater manufacturing continuity and improved cost stability despite ongoing supply-chain uncertainty.

Enzymatic oligonucleotide synthesis is creating new opportunities by reducing chemical waste while improving sequence accuracy for complex therapeutic applications. Early industrial deployments demonstrate reagent consumption reductions approaching 30% and shorter manufacturing workflows exceeding 20% compared with traditional chemical synthesis. Japan and South Korea are expanding investments in advanced biomanufacturing infrastructure alongside AI-enabled process optimization, accelerating commercialization readiness. Companies are strengthening competitive positioning through collaborative R&D, technology licensing, and automation partnerships that combine digital manufacturing with continuous production. This transition opens high-value opportunities in personalized medicine, next-generation diagnostics, and decentralized manufacturing ecosystems.

Scaling commercial oligonucleotide manufacturing requires sophisticated automation, validated digital systems, and highly specialized technical expertise. More than 45% of advanced production facilities report recruitment challenges for experienced bioprocess professionals, while digital validation requirements can extend implementation timelines by nearly 25%. Maintaining consistent quality across multi-site manufacturing networks has become increasingly complex as therapeutic portfolios diversify. Companies are investing in workforce development, digital manufacturing platforms, and standardized production protocols while expanding collaborations with specialized technology providers. Successfully integrating talent, infrastructure, and intelligent manufacturing systems will determine long-term operational competitiveness and sustainable industry leadership.

Automated Production Line Expansion Automated synthesis platforms now process nearly 35% more sequences per production cycle while reducing manual intervention by about 45%. Rising labor costs and stricter GMP expectations are accelerating workflow automation, enabling shorter turnaround times. Companies are scaling robotic production lines and integrating digital quality monitoring to improve manufacturing consistency.

Localized Manufacturing Networks More than 40% of new capacity additions are being established closer to major pharmaceutical hubs as supply-chain resilience becomes a strategic priority. The United States and Singapore continue expanding advanced manufacturing infrastructure, reducing logistics risks and improving delivery reliability. Manufacturers are restructuring procurement models through regional partnerships and multi-site production strategies.

Higher-Purity Product Demand Clinical-stage applications now account for over 60% of demand for high-purity oligonucleotides, while advanced purification technologies improve batch acceptance rates by nearly 25%. Increasing regulatory scrutiny is driving investments in process validation and analytical testing. Companies are upgrading purification workflows and expanding GMP-certified facilities to support commercial-scale production.

Digital Process Intelligence Adoption AI-assisted sequence optimization and real-time manufacturing analytics improve synthesis efficiency by approximately 20% while reducing production deviations by nearly 18%. A non-obvious shift is the growing use of predictive maintenance to minimize equipment downtime. Enterprises are partnering with digital technology providers to strengthen operational visibility, quality assurance, and manufacturing flexibility.

DNA Oligonucleotides remain the dominant segment, accounting for approximately 41% of market demand due to their extensive use in PCR, sequencing, molecular diagnostics, and gene analysis. Their established manufacturing workflows, high synthesis accuracy, and lower production complexity make them the preferred choice for research laboratories and commercial manufacturers. Modified Oligonucleotides continue gaining traction as therapeutic developers prioritize enhanced stability and targeted delivery, while RNA Oligonucleotides benefit from expanding RNA-based therapeutic pipelines. Companies are increasing investments in automated synthesis and purification technologies to improve quality while reducing production variability by nearly 22%.

Custom Oligonucleotides represent the fastest-growing segment as pharmaceutical companies increasingly require sequence-specific products for precision medicine and clinical development. Demand for customized synthesis has expanded by approximately 30% over recent years, encouraging manufacturers to broaden design capabilities and shorten delivery timelines. Strategic collaborations between synthesis providers and biotechnology firms are strengthening product portfolios, while continuous manufacturing technologies improve scalability. Investment priorities are increasingly shifting toward flexible production platforms capable of supporting diverse therapeutic and research applications.

Therapeutics account for approximately 38% of total application demand as oligonucleotides become central to RNA therapeutics, antisense medicines, and gene-editing programs. Expanding clinical pipelines and regulatory approvals continue increasing manufacturing requirements for high-purity products. Research & Development remains a mature application supporting innovation, while Diagnostics maintains strong demand through molecular testing. Drug Discovery and Genomic Studies continue expanding as pharmaceutical companies integrate genomic information into early-stage development. Manufacturers are increasing automated production capacity, improving batch consistency by nearly 25%, and strengthening analytical validation capabilities.

Drug Discovery is the fastest-growing application as AI-assisted target identification and high-throughput screening accelerate preclinical workflows. Deployment efficiency has improved by nearly 20% through integrated synthesis platforms and digital laboratory automation. Companies are expanding partnerships with biotechnology firms and contract research organizations to provide customized synthesis services, creating stronger long-term customer relationships. These operational changes are shifting investment toward integrated development ecosystems supporting rapid therapeutic innovation.

Pharmaceutical Companies represent the largest end-user segment with an estimated 44% market share, supported by large-scale therapeutic development, commercial manufacturing, and extensive clinical pipelines. Their demand is driven by advanced production requirements, regulatory compliance, and long-term manufacturing contracts. Biotechnology Companies constitute the fastest-growing customer group as venture-backed innovation and specialized therapeutic programs increase outsourcing requirements. Research Institutes continue generating stable demand for genomic studies, while Diagnostic Laboratories expand procurement alongside growing molecular testing volumes. Manufacturers are responding through customized production agreements, dedicated GMP capacity, and integrated technical support.

Biotechnology Companies are increasing purchasing volumes by approximately 28% as precision medicine programs expand globally. Companies are strengthening relationships through strategic partnerships, flexible pricing models, and rapid production scheduling tailored to early-stage developers. Diagnostic Laboratories continue adopting higher-throughput products to improve testing efficiency, while Research Institutes emphasize customized oligonucleotide solutions for advanced genomic research. Competitive positioning increasingly depends on manufacturing flexibility, quality assurance, and application-specific product customization.

North America accounted for the largest market share at 41.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 15.8% CAGR between 2026 and 2033.

Advanced Biopharmaceutical Manufacturing Strengthens Market Leadership

North America remains the leading regional market due to its mature biotechnology ecosystem, advanced pharmaceutical manufacturing infrastructure, and strong concentration of genomic research activities. The region contributes approximately 42% of global demand, supported by widespread deployment of GMP-certified synthesis facilities and extensive clinical development programs. More than 65% of commercial oligonucleotide manufacturing capacity is concentrated within established biotechnology clusters, enabling rapid production scaling and regulatory compliance. Investments in automated synthesis platforms and digital quality management continue improving manufacturing efficiency, while strategic collaborations between pharmaceutical companies and contract development organizations strengthen supply resilience. The region also benefits from integrated research, manufacturing, and commercialization capabilities that accelerate therapeutic development and improve production flexibility.

United States Market Outlook: The United States remains the region's operational center, supported by extensive pharmaceutical manufacturing infrastructure, world-leading biotechnology clusters, and strong genomic research investment. More than 70% of North America's advanced oligonucleotide production capacity is located in the country, supported by expanding GMP manufacturing facilities and automation deployment. Companies continue strengthening domestic manufacturing networks through capacity expansion, technology integration, and long-term supply partnerships, reinforcing the country's leadership in commercial-scale oligonucleotide production.

Regulatory Excellence Drives Manufacturing Modernization

Europe maintains a strong competitive position through advanced pharmaceutical manufacturing, harmonized regulatory frameworks, and increasing investments in precision medicine. The region represents approximately 28% of global market activity, supported by expanding biologics production and integrated research collaborations. More than 55% of newly commissioned manufacturing projects emphasize digital quality assurance and sustainable production technologies, improving operational consistency. Enterprise partnerships between biotechnology innovators and specialized manufacturing providers continue enhancing production flexibility while strengthening regional supply security. Ongoing investments in analytical technologies and modern manufacturing infrastructure further support commercialization of complex oligonucleotide products.

Germany Market Outlook: Germany leads the European market through its highly developed pharmaceutical manufacturing base, advanced biotechnology capabilities, and strong industrial automation expertise. The country accounts for nearly 24% of Europe's production capacity and continues expanding investments in high-quality nucleic acid manufacturing. Integrated research institutions, engineering expertise, and advanced production technologies enable manufacturers to improve operational efficiency while supporting growing therapeutic and diagnostic development programs.

Manufacturing Expansion Accelerates Regional Competitiveness

Asia-Pacific is emerging as the fastest-expanding regional market through rapid biotechnology investment, expanding pharmaceutical manufacturing, and increasing contract development activity. The region accounts for approximately 23% of global production while benefiting from cost-efficient manufacturing infrastructure and skilled technical workforces. More than 40% of recent manufacturing facility expansions have been announced across key biotechnology hubs, strengthening regional production capacity. Companies continue establishing localized supply networks and automation-enabled facilities to improve production efficiency and support global pharmaceutical demand. Government-backed biotechnology initiatives further accelerate manufacturing modernization and technology adoption.

China Market Outlook: China has become the region's largest manufacturing and investment center through continuous expansion of biotechnology parks, pharmaceutical production facilities, and genomic research programs. More than 45% of Asia-Pacific's new oligonucleotide manufacturing investments are directed toward Chinese facilities. Domestic manufacturers continue increasing production capacity, integrating automated synthesis technologies, and expanding international partnerships to strengthen export competitiveness and support global therapeutic supply requirements.

Healthcare Expansion Supports Market Development

South America continues strengthening its market position through expanding healthcare infrastructure, increasing biotechnology research, and growing pharmaceutical manufacturing capabilities. The region contributes approximately 5% of global demand, with investments increasingly directed toward molecular diagnostics and advanced laboratory capabilities. Public-private partnerships are supporting laboratory modernization, while specialized manufacturing and research facilities continue expanding. Although import dependence remains significant, regional enterprises are improving operational resilience through local distribution partnerships and technology transfer agreements. These developments gradually strengthen supply continuity while supporting future therapeutic manufacturing capabilities.

Brazil Market Outlook: Brazil remains the region's primary biotechnology and pharmaceutical market due to its expanding industrial base and established research institutions. The country represents more than 45% of South America's pharmaceutical manufacturing activity and continues investing in advanced laboratory infrastructure. Collaboration between domestic manufacturers and international biotechnology companies supports technology adoption, improves production capability, and strengthens local access to advanced oligonucleotide products.

Strategic Healthcare Investments Expand Market Capacity

The Middle East & Africa market is progressing through sustained healthcare modernization, biotechnology investment, and laboratory infrastructure development. The region accounts for approximately 3% of global market activity while increasing investment in genomic medicine, precision diagnostics, and specialized pharmaceutical capabilities. More than 30% of newly established life science facilities emphasize molecular testing and advanced laboratory technologies. Governments and private enterprises continue supporting biotechnology partnerships and healthcare infrastructure upgrades, creating stronger foundations for future manufacturing and research capabilities. Strategic investment remains focused on reducing import dependence while expanding regional technical expertise.

Saudi Arabia Market Outlook: Saudi Arabia leads regional development through national healthcare transformation initiatives, biotechnology investment programs, and expanding life science infrastructure. The country continues increasing deployment of advanced genomic laboratories and pharmaceutical manufacturing capabilities, supported by strategic public and private investment. Growing collaboration with international biotechnology companies strengthens technology transfer, workforce development, and operational readiness, positioning Saudi Arabia as the leading biotechnology hub within the Middle East and Africa.

The competitive landscape is led by Thermo Fisher Scientific, Merck KGaA, Eurofins Genomics, LGC Biosearch Technologies, and Integrated DNA Technologies, with specialized biotechnology manufacturers challenging established global suppliers through customized synthesis capabilities. The top five players collectively control approximately 48% of the market, while regional manufacturers compete aggressively on delivery speed and flexible production rather than scale. Competition increasingly centers on synthesis accuracy, turnaround time, supply-chain resilience, and therapeutic-grade manufacturing, with automated platforms improving production efficiency by nearly 30% and digital quality systems reducing batch deviations by approximately 20%. Leading companies are expanding GMP facilities, forming long-term pharmaceutical partnerships, integrating purification technologies, and strengthening vertical control over critical raw materials. The competitive shift favors automation-enabled manufacturers capable of delivering customized products at commercial scale while maintaining regulatory consistency. High capital requirements, process validation complexity, and specialized technical expertise remain significant entry barriers. Winning requires scalable manufacturing, reliable quality systems, rapid customization, resilient supply networks, and continuous technology advancement.

Thermo Fisher Scientific

Merck KGaA

Eurofins Genomics

Integrated DNA Technologies (IDT)

LGC Biosearch Technologies

GenScript Biotech Corporation

Bioneer Corporation

Synbio Technologies

Microsynth AG

Bio-Synthesis Inc.

TriLink BioTechnologies

ATDBio Ltd.

Macrogen Inc.

GeneCust

Conventional phosphoramidite chemistry continues to dominate commercial production, but automated high-throughput synthesis systems have transformed manufacturing performance. Modern robotic platforms increase production throughput by nearly 35% while reducing manual process intervention by approximately 45% compared with legacy batch workflows. More than 60% of newly commissioned production lines now incorporate automated reagent handling, inline monitoring, and digital quality control, enabling higher batch consistency and shorter production cycles. Pharmaceutical manufacturers benefit through improved scheduling, reduced operational variability, and faster fulfillment of clinical and commercial orders.

Emerging technologies are reshaping product quality and manufacturing flexibility. AI-assisted sequence optimization reduces design iterations by nearly 20%, while advanced purification technologies improve final product purity and increase batch acceptance rates by approximately 25%. Enzymatic oligonucleotide synthesis is gaining industrial attention because it lowers reagent consumption and minimizes chemical waste compared with conventional synthesis. Technology providers and contract manufacturers are integrating cloud-based manufacturing execution systems with predictive analytics to optimize equipment utilization and strengthen process traceability across distributed production facilities.

Between 2026 and 2028, continuous manufacturing, digital twins, and intelligent process control will become defining competitive technologies. Early adopters integrating automated synthesis, predictive maintenance, and real-time release testing are expected to improve overall manufacturing efficiency by nearly 30% while reducing operational costs by approximately 15%. Global manufacturers with scalable digital infrastructure, advanced analytical capabilities, and flexible production networks will achieve stronger supply reliability, faster commercialization, and superior responsiveness to expanding therapeutic and diagnostic demand.

January 2025 TriLink BioTechnologies (Maravai LifeSciences) acquired the assets of Molecular Assemblies, adding Fully Enzymatic Synthesis technology to strengthen long-sequence oligonucleotide manufacturing capabilities. The platform demonstrated 95% average coupling efficiency, supporting next-generation therapeutic production and manufacturing scalability. Source: Maravai LifeSciences

December 2024 Co-Dx and CoSara Diagnostics inaugurated an oligonucleotide synthesis facility in Vadodara, India under the Make in India initiative. The new facility expands domestic manufacturing capacity for molecular diagnostics while strengthening regional supply-chain resilience and reducing import dependence.

August 2025 Cohance Lifesciences announced an investment of INR 230 million to establish a cGMP oligonucleotide building block manufacturing facility in Hyderabad. The expansion strengthens India's pharmaceutical manufacturing ecosystem and increases local availability of critical inputs for nucleic acid therapeutics.

February 2026 Tsingke Biotech partnered with iGeneTech Bioscience to expand high-throughput oligonucleotide synthesis capabilities for synthetic biology and gene-editing applications. The collaboration targets significantly higher processing capacity through advanced automated workflows, improving manufacturing efficiency and research support.

This report provides comprehensive coverage of the global oligonucleotide synthesis market across DNA Oligonucleotides, RNA Oligonucleotides, Modified Oligonucleotides, and Custom Oligonucleotides, with detailed assessment of Research & Development, Therapeutics, Diagnostics, Drug Discovery, and Genomic Studies. It evaluates demand across pharmaceutical companies, biotechnology companies, research institutes, and diagnostic laboratories while examining market performance across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The analysis covers more than 10 leading industry participants alongside emerging technology innovators.

The report evaluates manufacturing automation, enzymatic synthesis, advanced purification technologies, AI-enabled process optimization, and digital quality management. It highlights deployment trends, production expansion, supply-chain localization, partnership strategies, and technology adoption influencing competitive positioning between 2026 and 2033. Strategic insights support investment prioritization, capacity expansion, product portfolio optimization, regional market entry, risk assessment, and long-term business planning by identifying operational opportunities, evolving customer demand, competitive differentiation, and emerging application areas across the global oligonucleotide synthesis value chain.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 10146.89 Million |

Market Revenue in 2033 | USD 28965.19 Million |

CAGR (2026 - 2033) | 14.01% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Thermo Fisher Scientific, Merck KGaA, Eurofins Genomics, Integrated DNA Technologies (IDT), LGC Biosearch Technologies, GenScript Biotech Corporation, Bioneer Corporation, Synbio Technologies, Microsynth AG, Bio-Synthesis Inc., TriLink BioTechnologies, ATDBio Ltd., Macrogen Inc., GeneCust |

Customization & Pricing | Available on Request (10% Customization is Free) |