Reports

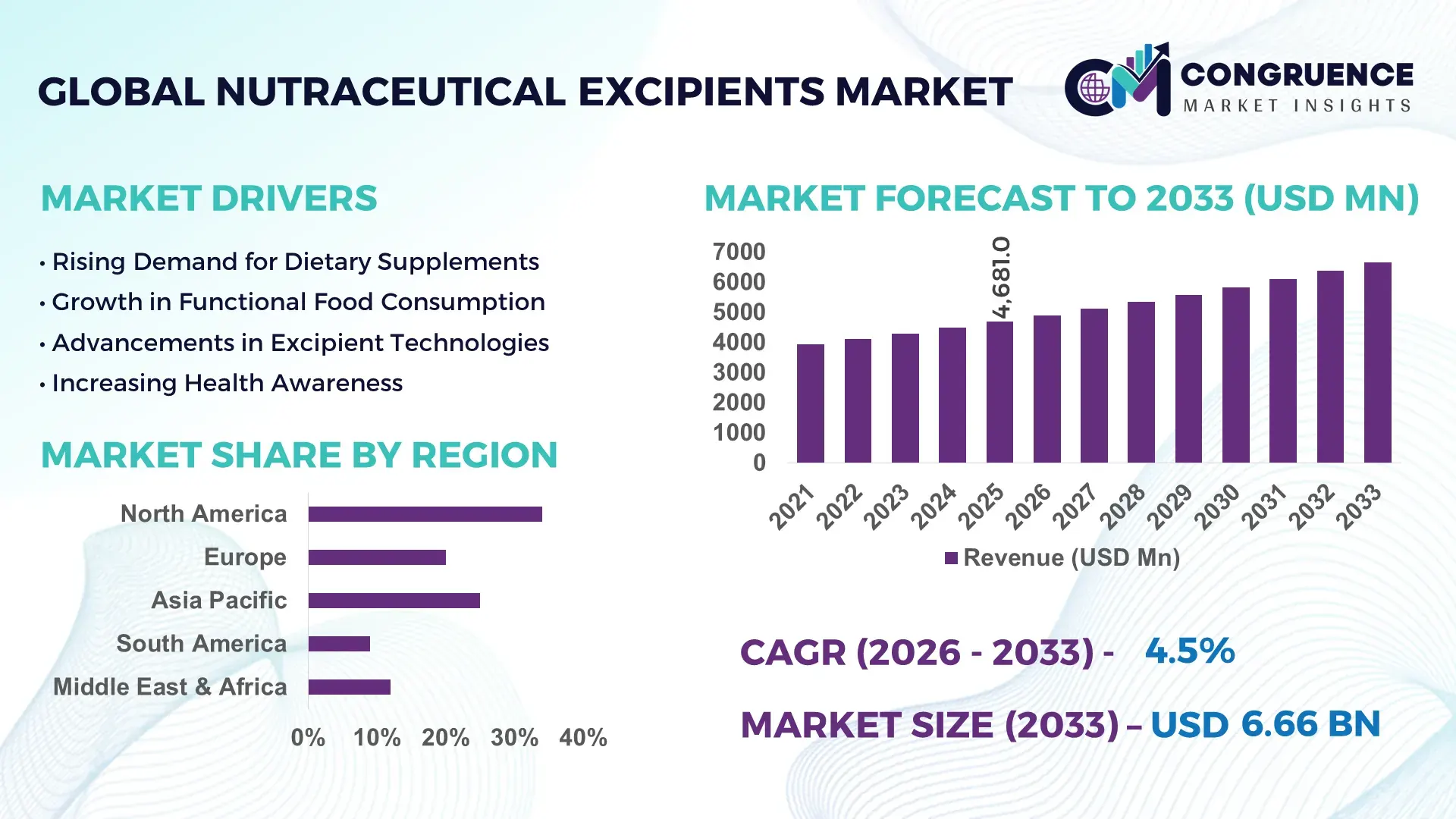

The Global Nutraceutical Excipients Market was valued at USD 4681 Million in 2025 and is anticipated to reach a value of USD 6656.85 Million by 2033 expanding at a CAGR of 4.5% between 2026 and 2033. Rising demand for clean-label nutraceutical formulations, high-stability tablet systems, and plant-based delivery technologies is accelerating excipient integration across functional foods, dietary supplements, and probiotic manufacturing lines.

The United States accounted for approximately 31% of global nutraceutical excipient consumption in 2025, supported by advanced dietary supplement manufacturing, over USD 1.2 billion in formulation modernization investments, and more than 68% adoption of multifunctional excipients in capsule production facilities. India strengthened its export position through lower-cost pharmaceutical-grade excipient processing, while China expanded binder and coating material capacity by nearly 14% amid post-Red Sea logistics diversification and regional supply chain realignment. Germany maintained strong adoption in premium probiotic applications with automated granulation systems improving production efficiency by 19%.

Manufacturers are prioritizing regionalized sourcing, high-performance excipient portfolios, and formulation efficiency upgrades to secure long-term competitiveness in the global nutraceutical excipients market.

Market Size & Growth: USD 4681 Million in 2025 reaching USD 6656.85 Million by 2033 at 4.5% CAGR, driven by advanced encapsulation demand and clean-label nutraceutical processing expansion.

Top Growth Drivers: Plant-based excipient adoption rose 18%, probiotic supplement production increased 21%, and direct-compression formulation usage expanded 16% globally.

Short-Term Forecast: By 2027, automated blending systems are projected to reduce production downtime by 14% while improving batch consistency by 11%.

Emerging Technologies: AI-assisted formulation screening, controlled-release coating systems, and multifunctional binders improved formulation efficiency by nearly 22%.

Regional Leaders: North America exceeded USD 1.7 billion through premium supplement manufacturing, Asia-Pacific crossed USD 1.5 billion with export-focused expansion, and Europe advanced clean-label adoption above 57%.

Consumer/End-User Trends: More than 63% of nutraceutical brands shifted toward sugar-free and vegan-compatible excipient systems during 2025–2026.

Pilot/Case Example: In 2026, a high-speed granulation upgrade reduced material wastage by 17% and shortened production cycles by 13%.

Competitive Landscape: The top five manufacturers controlled nearly 44% market share, with global competition centered on formulation performance and regulatory-grade consistency.

Regulatory & ESG Impact: Sustainable excipient sourcing programs lowered solvent usage by 26% as stricter global compliance standards accelerated eco-efficient processing.

Investment & Funding: More than USD 900 million flowed into production expansion, regional partnerships, and specialty excipient innovation across Asia and North America.

Innovation & Future Outlook: Next-generation bio-based carriers and precision-release excipients are reshaping high-growth nutraceutical manufacturing strategies and export competitiveness.

The nutraceutical excipients market is advancing through rapid demand for functional gummies, probiotic capsules, and plant-based nutraceutical formulations requiring higher stability and bioavailability performance. Advanced co-processed excipients improved tablet disintegration efficiency by nearly 20% in 2026 production environments. Manufacturers are also expanding regional sourcing networks to manage raw material volatility and evolving clean-label compliance standards, creating a stronger foundation for strategic formulation optimization and competitive product differentiation.

The nutraceutical excipients market is becoming strategically important as supplement manufacturers compete on bioavailability, clean-label compliance, and production efficiency rather than product volume alone. Supply-chain restructuring after Red Sea shipping disruptions accelerated localized excipient sourcing across India, Germany, and the United States, reducing lead-time exposure by nearly 18% in 2025–2026 procurement cycles. Regulatory tightening around additive transparency is also pushing companies toward multifunctional excipients that simplify formulations while improving stability and labeling efficiency.

Co-processed excipients are replacing conventional single-function binders in high-volume tablet and gummy production, delivering nearly 24% faster compression efficiency and reducing formulation adjustment time by 16% compared with legacy systems. The United States continues leading premium nutraceutical innovation through automated dosage technologies, while India is scaling lower-cost pharmaceutical-grade excipient manufacturing with over 20% expansion in export-oriented processing capacity. In Japan, probiotic supplement producers are integrating precision granulation systems to improve moisture control and shelf-life consistency.

During 2026, several manufacturers deployed AI-assisted formulation platforms that shortened product development timelines by almost 14%. Companies are prioritizing regional partnerships, sustainable raw-material procurement, and advanced coating technologies to strengthen operational resilience and secure long-term positioning in performance-driven nutraceutical manufacturing.

Rising demand for high-performance nutraceutical delivery systems is accelerating adoption of multifunctional excipients across tablets, gummies, powders, and probiotic capsules. More than 61% of supplement manufacturers increased investment in clean-label binders and stabilizers during 2025–2026 to improve dissolution efficiency and ingredient compatibility. In the United States, automated direct-compression systems improved production throughput by nearly 19%, while India expanded pharmaceutical-grade excipient output by over 15% to support export demand. The shift toward sugar-free and plant-based nutraceutical formulations is also increasing demand for advanced coating and flavor-masking technologies. Companies are responding through vertical integration, regional manufacturing expansion, and partnerships with formulation specialists to reduce dependency on imported raw materials and improve production flexibility.

Volatility in cellulose derivatives, starch-based carriers, and specialty polymers continues pressuring production economics across the nutraceutical excipients market. During 2025, excipient-grade raw material costs fluctuated between 11% and 17% due to freight instability, energy inflation, and supply concentration in China. Smaller manufacturers in Southeast Asia experienced procurement delays exceeding 30 days for certain coating agents and disintegrants, directly affecting batch scheduling and inventory planning. Regulatory variations between the European Union and United States are also increasing reformulation costs for export-focused producers. Companies are mitigating operational risks through multi-country sourcing agreements, localized warehousing, and long-term procurement contracts. Several firms are additionally investing in bio-based alternatives to reduce exposure to petrochemical-linked pricing cycles.

Precision nutrition trends are creating strong opportunities for customized excipient platforms optimized for targeted absorption, controlled release, and microbiome-focused formulations. More than 42% of premium nutraceutical launches in Japan and South Korea incorporated advanced encapsulation technologies during 2026. AI-assisted formulation modeling reduced ingredient compatibility testing time by nearly 21%, improving speed-to-market for personalized supplements. Demand is also increasing for co-processed excipients supporting high-load botanical ingredients and probiotic survivability. India is emerging as a strategic manufacturing hub for vegan-compatible excipients due to lower processing costs and expanding pharmaceutical infrastructure. Companies are strengthening R&D alliances, expanding pilot-scale manufacturing, and investing in biodegradable coating technologies to capture higher-margin specialty formulation contracts and differentiate performance-focused product portfolios.

Scaling advanced nutraceutical excipient systems across global manufacturing networks remains operationally complex due to inconsistent quality standards, evolving compliance frameworks, and technical workforce limitations. Nearly 28% of mid-sized supplement manufacturers reported formulation inconsistency issues during high-speed production runs in 2025, particularly in humidity-sensitive applications. Germany and the United States are tightening validation requirements for multifunctional excipients, increasing documentation workloads and extending commercial approval timelines. Integration of automated blending and precision dosing systems also requires significant process recalibration and skilled technical oversight. Companies must address these execution barriers through digital quality-control investments, workforce training, and standardized validation protocols. Long-term competitiveness increasingly depends on achieving scalable formulation consistency without compromising clean-label performance or production efficiency.

Clean-Label Reformulation Expansion Nutraceutical brands in the United States and Germany accelerated replacement of synthetic carriers with plant-derived excipients, increasing clean-label formulation deployment by 23% during 2025–2026. Regulatory scrutiny around additive transparency pushed manufacturers to reduce inactive ingredient complexity by nearly 18%, improving labeling compliance and export readiness. Companies are restructuring procurement networks and scaling bio-based excipient partnerships to stabilize sourcing and reduce formulation approval delays.

Automation in Dosage Manufacturing High-speed direct-compression systems and AI-assisted blending platforms improved tablet production efficiency by 21% while reducing material wastage by 14% across large-scale supplement facilities in India and Japan. Labor shortages in precision manufacturing environments accelerated automation deployment, particularly in gummy and probiotic applications. Manufacturers are investing in integrated processing lines and predictive quality-control software to shorten batch validation cycles and improve operational consistency.

Microbiome-Focused Delivery Innovation Encapsulation technologies designed for probiotic survivability gained strong traction, with moisture-resistant coating adoption rising 19% in 2026. South Korean and Japanese producers increased investment in delayed-release systems to improve ingredient stability during transportation and storage. A non-obvious shift is emerging toward excipient customization for gut-health formulations, enabling higher premium pricing and stronger differentiation in competitive supplement portfolios.

Regionalized Supply Chain Strategies Nutraceutical excipient producers reduced overseas dependency by nearly 16% through localized warehousing and multi-country sourcing models following Red Sea shipping disruptions. China expanded specialty binder output, while India increased pharmaceutical-grade excipient processing capacity by over 15% to support export continuity. Companies are prioritizing regional manufacturing partnerships, shorter procurement cycles, and inventory digitization to improve resilience against freight volatility and raw-material allocation pressure.

Binders remained the leading segment in the nutraceutical excipients market due to their critical role in tablet integrity, compression efficiency, and high-speed manufacturing compatibility. More than 58% of large-scale supplement production lines in the United States and India prioritized advanced binder systems during 2025–2026 to improve dosage consistency and reduce production interruptions. Coating Agents emerged as the fastest-growing segment as probiotic, delayed-release, and moisture-sensitive nutraceutical formulations expanded rapidly. Automated coating technologies improved product shelf stability by nearly 17%, particularly in Japan’s premium gut-health supplement sector.

Fillers and Diluents maintained strong demand in cost-sensitive bulk nutraceutical manufacturing because of their scalability and raw-material flexibility, while Disintegrants gained traction in fast-dissolve tablet applications requiring improved nutrient release efficiency. Flavoring Agents also expanded steadily as sugar-free gummies and flavored powders became operationally important for consumer retention. Manufacturers are increasing investment in multifunctional excipients, customized coating systems, and plant-based formulation technologies to strengthen production adaptability and improve formulation performance across diverse delivery formats.

Tablets continued dominating nutraceutical excipient consumption due to superior scalability, lower unit production costs, and compatibility with automated manufacturing infrastructure. More than 61% of global nutraceutical output during 2025 relied on tablet-based delivery systems, particularly across the United States and India where high-throughput direct-compression facilities expanded rapidly. Capsules represented the fastest-growing application as probiotic, botanical, and personalized nutrition products increased demand for moisture-sensitive and delayed-release formulations. Capsule-filling automation improved operational throughput by nearly 18% in Japan and South Korea during 2026.

Functional Foods and Liquid Supplements are gaining stronger operational relevance as consumers shift toward convenient nutrition delivery formats requiring advanced stabilizers and flavor-masking excipients. Powders maintained stable industrial demand in sports nutrition and protein supplementation because of lower packaging complexity and flexible dosing structures. Companies are scaling encapsulation infrastructure, upgrading blending systems, and expanding customized excipient portfolios to support evolving application-specific manufacturing requirements and shorten commercialization cycles for differentiated nutraceutical products.

Dietary Supplement Manufacturers remained the dominant end-user group due to large-volume excipient procurement, continuous product launches, and dependence on high-speed formulation systems. More than 66% of excipient integration demand in 2025 originated from supplement-focused production facilities in the United States, China, and India. Contract Manufacturers emerged as the fastest-growing segment as nutraceutical brands increasingly outsourced formulation, blending, and encapsulation operations to reduce infrastructure costs and accelerate product commercialization. Outsourced production agreements increased by nearly 19% during 2025–2026 across mid-sized supplement brands.

Pharmaceutical Companies continued expanding involvement in premium nutraceutical applications through pharmaceutical-grade excipient deployment and advanced stability testing capabilities. Food and Beverage Industry participants strengthened demand for flavoring agents and dispersible excipients in fortified beverages and functional foods, while Research Laboratories increased pilot-scale testing for microbiome-focused formulations. Nutraceutical Companies are responding through long-term supply agreements, customized excipient development, and strategic manufacturing partnerships to secure production continuity and improve formulation differentiation in increasingly specialized supplement categories.

North America accounted for the largest market share at 34.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.7% between 2026 and 2033.

Advanced Formulation Infrastructure Driving Market Leadership

North America maintained strong dominance in the nutraceutical excipients market due to large-scale supplement manufacturing infrastructure, high adoption of multifunctional excipients, and advanced formulation automation. The United States and Canada together represented more than 34% of global deployment activity during 2025, supported by strong integration of direct-compression technologies and AI-assisted quality-control systems. More than 59% of premium nutraceutical formulations launched in the region incorporated clean-label or plant-derived excipient systems. Manufacturers also accelerated regional sourcing partnerships following Red Sea shipping disruptions, reducing average procurement delays by nearly 15%. Strategic investments in probiotic encapsulation and moisture-resistant coating technologies continue strengthening operational efficiency and product differentiation across large-volume supplement production networks.

United States Market Outlook: The United States remains the operational center of North America’s nutraceutical excipient ecosystem due to advanced pharmaceutical-grade manufacturing infrastructure and strong enterprise investment in formulation innovation. More than 68% of large dietary supplement facilities adopted automated blending and tablet compression systems by 2026 to improve batch consistency and reduce production downtime. Regulatory focus on label transparency and clean-label compliance is also accelerating deployment of multifunctional excipients across probiotic, botanical, and personalized nutrition applications.

Clean-Label Compliance Reshaping Production Standards

Europe continues strengthening its position through stringent formulation standards, sustainable excipient sourcing, and high adoption of clean-label nutraceutical technologies. Germany, France, and the United Kingdom accounted for over 29% of advanced coating and stabilizer deployment across premium nutraceutical manufacturing during 2025. Regulatory pressure on additive transparency accelerated replacement of synthetic carriers with plant-derived excipients, increasing bio-based formulation integration by nearly 21%. European manufacturers also expanded low-solvent processing systems to improve ESG compliance and reduce operational waste generation. Strategic partnerships between excipient suppliers and nutraceutical brands are improving formulation customization capabilities, particularly in probiotic and microbiome-focused supplement categories where stability and controlled-release performance remain commercially critical.

Germany Market Outlook: Germany leads Europe’s nutraceutical excipient market through precision manufacturing infrastructure, advanced granulation technologies, and strong pharmaceutical-industrial integration. More than 54% of premium nutraceutical production facilities in Germany upgraded automated coating and moisture-control systems during 2025–2026 to improve shelf-life consistency and export readiness. The country’s focus on sustainable processing and high-purity excipient standards is also strengthening its position in probiotic and plant-based nutraceutical manufacturing applications.

Large-Scale Manufacturing Expansion Accelerating Deployment

Asia-Pacific is emerging as the fastest-scaling nutraceutical excipient production hub due to expanding pharmaceutical infrastructure, lower manufacturing costs, and export-oriented processing capacity. China, India, Japan, and South Korea collectively contributed more than 38% of global excipient production activity in 2025. India increased pharmaceutical-grade excipient processing capacity by nearly 16%, while China strengthened specialty binder and coating-agent output to support global supplement manufacturing demand. Japan and South Korea accelerated adoption of precision encapsulation systems for microbiome-focused nutraceutical products. Regional manufacturers are investing heavily in automated blending systems, localized raw-material sourcing, and advanced quality-control platforms to improve production efficiency and reduce exposure to international freight volatility.

India Market Outlook: India is rapidly strengthening its role as a strategic manufacturing and export hub for nutraceutical excipients through cost-efficient processing infrastructure and expanding pharmaceutical-industrial capabilities. More than 62% of new nutraceutical production facilities commissioned during 2025 incorporated direct-compression and automated granulation technologies. Strong availability of pharmaceutical-grade raw materials and lower operational costs continue attracting multinational partnerships focused on vegan-compatible binders, coating systems, and high-volume tablet production for export-driven nutraceutical applications.

Functional Nutrition Demand Expanding Industrial Activity

South America is witnessing increasing nutraceutical excipient demand through expanding functional food manufacturing, rising supplement consumption, and modernization of regional processing infrastructure. Brazil and Argentina represented over 63% of the region’s nutraceutical production deployment during 2025, supported by increasing integration of flavoring agents and stabilizers in fortified food applications. Local manufacturers improved automated powder blending capacity by nearly 13% to support sports nutrition and immunity-focused formulations. However, import dependency for specialty coating agents and disintegrants continues creating procurement volatility and longer lead times. Companies are responding through regional distribution partnerships, localized warehousing expansion, and investments in flexible manufacturing systems to improve supply continuity and operational responsiveness.

Brazil Market Outlook: Brazil remains the largest nutraceutical excipient market in South America due to its expanding dietary supplement manufacturing base and strong food-processing ecosystem. More than 48% of regional functional food producers increased deployment of advanced stabilizers and flavor-masking excipients during 2026 to improve product consistency and shelf stability. Domestic manufacturers are also strengthening partnerships with pharmaceutical ingredient suppliers to improve formulation efficiency and reduce import dependency for high-performance excipient systems.

Industrial Modernization Supporting Market Transformation

The Middle East & Africa nutraceutical excipients market is evolving through pharmaceutical-industrial diversification, healthcare modernization programs, and increasing investment in localized supplement manufacturing infrastructure. The United Arab Emirates, Saudi Arabia, and South Africa accounted for nearly 57% of regional deployment activity during 2025, supported by growing integration of automated blending and encapsulation systems. Governments across the Gulf region accelerated food-security and pharmaceutical-localization initiatives, encouraging expansion of nutraceutical processing facilities and regional ingredient storage infrastructure. Manufacturers also increased investment in temperature-controlled logistics networks to improve ingredient stability across harsh climate conditions. Despite ongoing import reliance for specialized excipients, operational modernization is improving production reliability and reducing distribution inefficiencies.

Saudi Arabia Market Outlook: Saudi Arabia is strengthening its nutraceutical excipient market position through industrial diversification policies and expanding pharmaceutical manufacturing capabilities. More than 41% of newly established nutraceutical processing facilities during 2025–2026 integrated automated dosage and encapsulation technologies to support domestic supplement production. Strategic investments in industrial parks, warehousing infrastructure, and pharmaceutical localization programs are also improving regional supply-chain resilience and supporting long-term deployment of advanced excipient systems across functional nutrition applications.

The nutraceutical excipients market is led by Ingredion, Roquette, Ashland, BASF, and DuPont competing against regional formulation specialists and low-cost Asian manufacturers. The top five players collectively control nearly 46% of global market activity through scale advantages, customized excipient portfolios, and integrated supply networks. Global leaders compete on formulation performance, regulatory-grade consistency, and rapid product customization, while regional suppliers focus on lower-cost binders, fillers, and coating agents. Automated co-processed excipient systems improved production efficiency by 18%, pushing manufacturers toward technology-driven differentiation instead of price-only competition. Companies are expanding through localized manufacturing, pharmaceutical partnerships, and direct-compression technology integration to secure long-term contracts with supplement producers. Consolidation is increasing as multinational firms strengthen control over specialty excipient supply chains following logistics disruptions and raw-material volatility. Entry barriers remain high due to validation requirements, formulation expertise, and regulatory compliance complexity. Competitive success increasingly depends on scalable customization, stable sourcing, and advanced formulation capabilities.

Roquette Frères

Ingredion Incorporated

Ashland Inc.

BASF SE

DuPont de Nemours, Inc.

Kerry Group plc

Colorcon Inc.

Associated British Foods plc

Sensient Technologies Corporation

Evonik Industries AG

DFE Pharma

MEGGLE GmbH & Co. KG

SPI Pharma

Gangwal Healthcare Pvt. Ltd.

Advanced co-processed excipients and direct-compression technologies are becoming core manufacturing tools across nutraceutical production facilities. During 2026, more than 57% of large supplement manufacturers integrated multifunctional binders and stabilizers to reduce formulation complexity and improve tablet throughput. Compared with conventional wet granulation systems, automated direct-compression platforms improved production efficiency by nearly 24% while lowering material wastage by 13%. Companies adopting these systems are achieving faster batch validation, shorter cleaning cycles, and stronger formulation consistency across high-volume tablet and gummy manufacturing operations.

Emerging technologies are reshaping excipient functionality through AI-assisted formulation modeling, precision encapsulation, and moisture-resistant coating systems. AI-driven compatibility screening reduced development timelines by approximately 18% in probiotic and botanical formulations, while controlled-release encapsulation technologies improved ingredient stability by 16% during transportation and storage. Japan and South Korea are leading deployment of microbiome-focused delivery systems, pushing global suppliers toward specialized excipient customization and higher-performance coating materials.

Between 2026 and 2028, disruptive innovation will center on biodegradable excipients, smart-release delivery platforms, and digitally monitored manufacturing systems. Companies investing in automated quality-control infrastructure and sustainable excipient technologies are expected to secure stronger long-term supply agreements, particularly in premium personalized nutrition and clean-label nutraceutical applications.

February 2025 – Roquette launched an expanded nutraceutical coatings platform integrating Tabshield® and ReadiLYCOAT® technologies, improving coating process efficiency by nearly 15% for supplement manufacturers. The move strengthened Roquette’s position in sustainable excipient systems and accelerated clean-label formulation deployment across global nutraceutical production networks. Source: pharmaceutical-tech.com

October 2024 – Colorcon entered a global partnership with LOTTE Fine Chemical to expand AnyCoat® hypromellose excipient deployment across pharmaceutical and dietary supplement applications. The collaboration improved controlled-release formulation compatibility and expanded specialty polymer access across multiple international manufacturing markets. Source: colorcon.com

October 2024 – Ashland introduced klucel ls™ low-substituted hydroxypropyl cellulose excipients for oral solid dose applications, improving controlled-release and immediate-release formulation flexibility. The innovation strengthened Ashland’s advanced excipient portfolio while supporting higher-performance nutraceutical tablet manufacturing and faster formulation optimization processes. Source: ashland.com

October 2025 – Roquette integrated Qualicaps and IFF Pharma Solutions into a unified Health & Pharma Solutions platform, expanding global excipient, capsule, and drug-delivery capabilities. The integration strengthened end-to-end formulation support and improved deployment scalability for nutraceutical and pharmaceutical manufacturing customers worldwide. Source: roquette.com

The nutraceutical excipients market report delivers comprehensive analysis across key types including fillers and diluents, binders, coating agents, flavoring agents, and disintegrants, with detailed evaluation of operational performance, formulation trends, and manufacturing integration patterns. The study covers major applications such as tablets, capsules, powders, functional foods, and liquid supplements, alongside end-user assessment across dietary supplement manufacturers, pharmaceutical companies, contract manufacturers, and nutraceutical enterprises. More than 60% of analyzed production environments incorporate automated blending, direct-compression, or advanced encapsulation technologies, highlighting rapid industrial modernization between 2026 and 2033.

The report further examines regional manufacturing concentration, supply-chain restructuring, clean-label formulation adoption, and precision nutrition deployment trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Strategic insights include competitive benchmarking, sourcing models, partnership activity, sustainability integration, and technology adoption shifts influencing production scalability, operational efficiency, and long-term investment positioning in advanced nutraceutical formulation ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 4681 Million |

|

Market Revenue in 2033 |

USD 6656.85 Million |

|

CAGR (2026 - 2033) |

4.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Roquette Frères, Ingredion Incorporated, Ashland Inc., BASF SE, DuPont de Nemours, Inc., Kerry Group plc, Colorcon Inc., Associated British Foods plc, Sensient Technologies Corporation, Evonik Industries AG, DFE Pharma, MEGGLE GmbH & Co. KG, SPI Pharma, Gangwal Healthcare Pvt. Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |