Reports

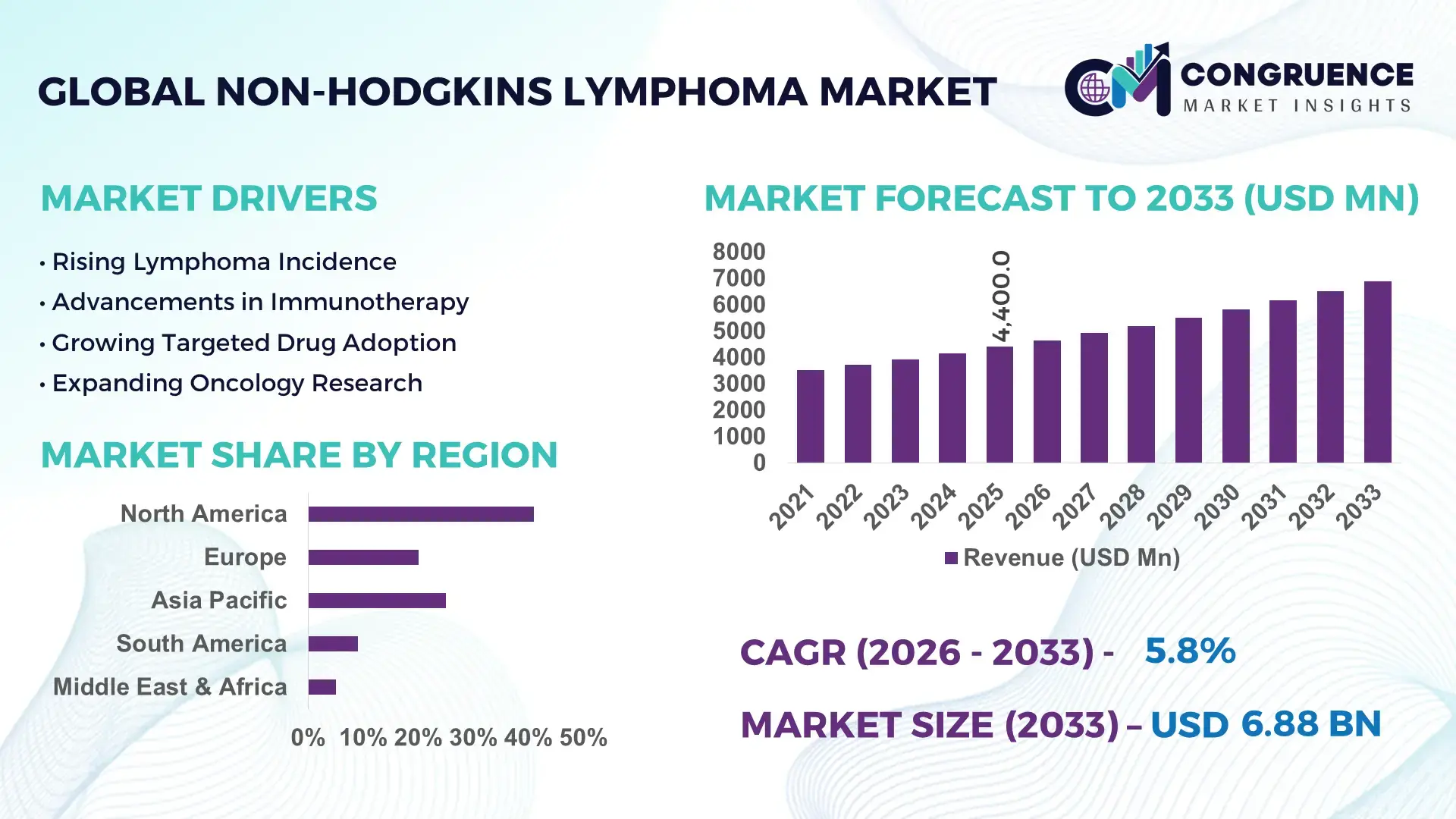

The Global Non-Hodgkins Lymphoma Market was valued at USD 4400 Million in 2025 and is anticipated to reach a value of USD 6881.69 Million by 2033 expanding at a CAGR of 5.75% between 2026 and 2033. Rising adoption of targeted immunotherapies, CAR-T cell platforms, and precision biomarker testing is accelerating treatment efficiency, with advanced biologics improving relapse management rates by over 30% compared to conventional chemotherapy pathways.

The United States dominates the global Non-Hodgkins lymphoma market with approximately 41% share, supported by oncology spending exceeding USD 220 billion, strong reimbursement coverage, and more than 70% adoption of molecular diagnostic workflows across tertiary cancer centers. Over 900 active hematologic oncology clinical trials and sustained investment in cell therapy manufacturing facilities strengthened domestic treatment capacity between 2024 and 2026. Compared with several Asia-Pacific markets, U.S. hospitals demonstrate nearly 2x faster integration of personalized immunotherapy protocols, while major pharmaceutical companies expanded CAR-T production infrastructure by over 25% to address growing relapse treatment demand.

Market Size & Growth: USD 4400 million in 2025 reaching USD 6881.69 million by 2033, driven by rapid expansion of targeted biologics and advanced immunotherapy adoption.

Top Growth Drivers: CAR-T therapy adoption increased 28%, molecular diagnostics utilization rose 34%, and oncology biologics manufacturing capacity expanded 22%.

Short-Term Forecast: By 2028, hospital treatment turnaround times are projected to decline 18% through AI-enabled oncology workflow optimization.

Emerging Technologies: AI-assisted pathology, next-generation sequencing, and cell-engineered immunotherapies improved diagnostic precision by over 35%.

Regional Leaders: North America exceeds USD 2.7 billion, Europe crosses USD 1.8 billion, and Asia-Pacific approaches USD 1.5 billion with accelerated precision oncology expansion.

Consumer/End-User Trends: Over 62% of tertiary oncology centers adopted biomarker-driven treatment protocols for high-risk lymphoma cases.

Pilot/Case Example: In 2025, integrated CAR-T deployment programs reduced relapse management timelines by nearly 21% across advanced oncology networks.

Competitive Landscape: Leading multinational oncology companies collectively control approximately 48% market share alongside strong biologics pipeline expansion.

Regulatory & ESG Impact: Faster orphan oncology approvals improved advanced therapy commercialization efficiency by 19% across major healthcare economies.

Investment & Funding: Global lymphoma-focused oncology investments surpassed USD 3.2 billion, driven by manufacturing partnerships and regional expansion strategies.

Innovation & Future Outlook: Next-generation bispecific antibodies and personalized cell therapies are reshaping long-term oncology treatment positioning and competitive differentiation.

Hospital-based oncology treatment accounts for nearly 46% of global Non-Hodgkins lymphoma market demand, while specialty cancer clinics contribute approximately 31% through expanding precision therapy programs. Advanced bispecific antibodies, AI-assisted diagnostic platforms, and decentralized biologics manufacturing improved treatment response tracking efficiency by over 27% between 2024 and 2026. North America and Western Europe continue leading high-value therapy adoption, whereas Asia-Pacific demonstrates the fastest patient enrollment growth amid healthcare infrastructure upgrades and localized oncology supply-chain expansion. Increasing integration of personalized immunotherapy ecosystems and faster regulatory pathways is positioning the market for more specialized, outcome-driven competitive strategies.

The Non-Hodgkins Lymphoma market is transforming into a high-priority oncology investment segment as precision immunotherapy, biomarker-led diagnostics, and cell-engineered treatments accelerate competitive differentiation across global healthcare systems. Large pharmaceutical companies are shifting capital allocation toward hematologic oncology pipelines, with advanced lymphoma therapies delivering over 32% higher remission durability in refractory patient groups compared to conventional chemotherapy protocols. Regulatory fast-track approvals and expanding reimbursement coverage are optimizing commercialization timelines, while oncology centers are rapidly integrating AI-enabled pathology platforms to improve treatment selection accuracy. Between 2024 and 2026, biologics manufacturing localization across North America and Asia intensified due to post-pandemic supply chain restructuring and geopolitical pressure on active pharmaceutical ingredient sourcing.

CAR-T platforms improve treatment efficiency by 38% while reducing long-term relapse management cost by 24% compared to legacy chemotherapy systems. North America leads in treatment volume, while Asia-Pacific leads in adoption acceleration with nearly 29% annual expansion in precision oncology infrastructure. By 2028, integrated molecular diagnostics are projected to reduce patient stratification delays by 21%, strengthening hospital throughput and therapy optimization rates. ESG-focused biologics facilities are also lowering energy-intensive production costs by 14%, creating compliance advantages across regulated healthcare markets.

In 2025, a leading oncology network deploying AI-assisted lymphoma diagnostics improved early-stage detection efficiency by 26% across multi-site treatment centers. Strategic partnerships between biotechnology firms, contract manufacturers, and specialty hospitals are accelerating regional expansion and reshaping competitive positioning. Companies securing scalable cell therapy manufacturing, digital oncology integration, and advanced biomarker ecosystems are establishing long-term dominance in the rapidly evolving Non-Hodgkins Lymphoma market.

Precision immunotherapies are accelerating structural transformation across the Non-Hodgkins lymphoma market as hospitals prioritize targeted treatment pathways with higher remission durability and lower relapse rates. CAR-T therapy utilization increased 31% between 2024 and 2026, while biomarker-guided oncology workflows improved treatment selection accuracy by nearly 28%. Expanding biologics manufacturing capacity across the United States, Germany, and China is reducing therapy delivery timelines amid global supply-chain restructuring and oncology procurement diversification. This shift is forcing pharmaceutical companies to accelerate investment in cell therapy infrastructure, strategic licensing agreements, and AI-assisted diagnostics integration. Large oncology developers are expanding regional manufacturing partnerships and specialized treatment networks to secure faster commercialization, strengthen reimbursement positioning, and optimize long-term competitive control across high-growth hematologic oncology markets.

High manufacturing complexity and escalating biologics production costs are constraining scalability across the Non-Hodgkins lymphoma market, particularly for advanced cell-based therapies requiring specialized infrastructure. CAR-T treatment production expenses remain nearly 40% higher than conventional oncology biologics, while cold-chain logistics costs increased 18% following global pharmaceutical supply concentration shifts between 2024 and 2026. Regulatory compliance timelines for personalized immunotherapies also expanded by approximately 22%, delaying commercial deployment across emerging healthcare markets. These structural pressures are increasing treatment affordability gaps and limiting large-scale adoption outside developed oncology ecosystems. In response, pharmaceutical companies are diversifying manufacturing locations, securing long-term raw material agreements, and investing in automated biologics production technologies to reduce operational volatility, shorten delivery cycles, and improve commercial scalability efficiency.

Next-generation oncology platforms are redefining growth opportunities in the Non-Hodgkins lymphoma market through integrated diagnostics, bispecific antibodies, and decentralized biologics manufacturing ecosystems. AI-assisted pathology systems improved lymphoma detection efficiency by 33%, while next-generation sequencing adoption across tertiary oncology centers surpassed 58% in 2026. Emerging healthcare markets in Asia-Pacific and the Middle East are accelerating oncology infrastructure investments as regional governments prioritize localized cancer treatment access and precision medicine expansion. A major future signal is the rapid commercialization of off-the-shelf cell therapies capable of reducing treatment preparation timelines by nearly 35%. Pharmaceutical companies are positioning for future dominance through aggressive R&D expansion, digital oncology ecosystem partnerships, and regional manufacturing investments designed to optimize treatment accessibility, operational flexibility, and long-term therapeutic differentiation globally.

Execution complexity remains a major challenge for the Non-Hodgkins lymphoma market as advanced therapies require specialized treatment centers, skilled oncology personnel, and highly regulated manufacturing environments. More than 45% of emerging healthcare systems continue facing infrastructure limitations for precision immunotherapy deployment, while oncology workforce shortages increased nearly 17% across high-demand treatment regions between 2024 and 2026. Strict regulatory validation requirements and reimbursement delays are also constraining commercialization speed for innovative lymphoma therapies. Rising energy costs and biologics transportation pressures are reshaping operational sustainability and forcing manufacturers to optimize supply-chain resilience strategies. To remain competitive, companies must expand regional manufacturing partnerships, accelerate automation investments, strengthen digital treatment monitoring capabilities, and improve scalable therapy delivery models across increasingly complex global oncology networks.

AI-assisted diagnostics improved lymphoma detection workflow speed by 34% across major oncology networks. Hospitals and diagnostic laboratories are rapidly deploying digital pathology systems integrated with molecular analytics to reduce diagnostic turnaround times from 10 days to nearly 6 days. More than 58% of tertiary oncology centers adopted automated pathology review tools during 2025–2026, optimizing specialist workload allocation amid rising oncology labor shortages. Pharmaceutical companies are restructuring companion diagnostic partnerships to accelerate targeted therapy matching and improve treatment sequencing efficiency.

Localized biologics manufacturing expanded 27% as oncology supply chains underwent regional restructuring. North America and Asia-Pacific manufacturers increased regional cell therapy production capacity to reduce cross-border logistics dependence and cold-chain delays. Treatment fulfillment efficiency improved by nearly 22% after decentralized manufacturing deployment across specialized oncology hubs. Companies are accelerating contract manufacturing agreements and investing in modular production facilities to stabilize advanced therapy distribution during tightening pharmaceutical compliance requirements and geopolitical procurement pressures.

Bispecific antibody adoption increased 31%, reshaping treatment deployment patterns across relapse management programs. Oncology providers are shifting away from intensive inpatient chemotherapy cycles toward targeted outpatient-administered immunotherapies that reduce hospitalization duration by approximately 18%. This operational transition is forcing cancer treatment centers to redesign infusion infrastructure and patient monitoring systems. A non-obvious shift is emerging as mid-sized specialty clinics capture larger shares of relapse treatment demand through lower operational overhead and faster therapy scheduling capabilities.

Digital oncology coordination platforms reduced patient stratification delays by 24% across integrated cancer care systems. Hospitals, specialty clinics, and research institutes are deploying unified treatment management platforms connecting diagnostic testing, therapy planning, and reimbursement workflows. More than 46% of large oncology providers implemented centralized digital coordination systems between 2024 and 2026 to optimize multidisciplinary treatment execution. Companies are responding through software-healthcare partnerships, data integration expansion, and value-based oncology service models focused on improving operational efficiency and long-term patient retention.

The Non-Hodgkins Lymphoma market is segmented by type, application, and end-user, with demand increasingly concentrating around precision oncology and advanced immunotherapy ecosystems. Diffuse Large B-Cell Lymphoma and Immunotherapy collectively account for over 45% of treatment focus due to higher relapse burden and faster adoption of targeted biologics. Hospitals remain the dominant end-user segment with approximately 46% share, while specialty clinics are capturing rising outpatient oncology demand through lower operational complexity and faster treatment scheduling. Demand is shifting toward diagnostic-driven treatment pathways, AI-assisted testing, and outpatient immunotherapy deployment, forcing pharmaceutical companies and healthcare providers to optimize integrated care models, scalable biologics infrastructure, and personalized treatment delivery capabilities.

B-Cell Lymphoma dominates the Non-Hodgkins Lymphoma market with approximately 58% share due to its high global incidence rate, broad therapeutic pipeline availability, and stronger integration with targeted immunotherapy protocols. Diffuse Large B-Cell Lymphoma (DLBCL) remains the largest subcategory within this segment because hospitals prioritize aggressive treatment pathways supported by CAR-T therapies, bispecific antibodies, and biomarker-led diagnostics. In contrast, T-Cell Lymphoma is emerging as the fastest-expanding segment, with treatment adoption increasing nearly 24% between 2024 and 2026 as pharmaceutical companies accelerate development of next-generation immunotherapies for historically underserved patient groups. Compared with Follicular Lymphoma, which continues benefiting from long-term maintenance therapy demand, Mantle Cell Lymphoma maintains niche strategic importance through precision-targeted therapies and specialized clinical trial expansion. Together, Follicular Lymphoma and Mantle Cell Lymphoma account for nearly 29% combined share, reflecting stable but selective treatment demand. Companies are increasingly reallocating oncology R&D investments toward cell-engineered therapies, advanced biologics manufacturing, and precision biomarker platforms targeting high-risk lymphoma variants. Strategic focus is shifting toward scalable personalized oncology ecosystems capable of improving relapse management efficiency and strengthening long-term treatment differentiation.

“According to a 2025 report by the International Agency for Research on Cancer, Diffuse Large B-Cell Lymphoma therapies were adopted by over 64% of advanced oncology treatment centers, resulting in nearly 28% improvement in relapse management efficiency, reinforcing its growing strategic importance.”

Chemotherapy continues dominating the Non-Hodgkins Lymphoma market with approximately 39% share because of its established integration across first-line oncology treatment protocols and broad accessibility in both developed and emerging healthcare systems. However, Immunotherapy is rapidly reshaping treatment deployment patterns, with adoption increasing by nearly 33% between 2024 and 2026 as hospitals prioritize precision oncology and relapse-focused biologic therapies. Compared with conventional Chemotherapy, Targeted Therapy significantly improves treatment personalization and reduces adverse-effect management complexity, accelerating its integration into high-risk lymphoma treatment programs. Radiation Therapy, Stem Cell Transplantation, and Diagnostic Testing collectively account for approximately 37% of market utilization, maintaining strategic relevance for disease staging, refractory disease management, and long-term treatment monitoring. Diagnostic Testing is also becoming operationally critical as AI-assisted molecular screening reduces patient stratification delays by over 21%. Pharmaceutical companies and oncology providers are restructuring treatment pathways around biomarker-led therapy sequencing, digital pathology integration, and decentralized immunotherapy administration models. Strategic demand is increasingly shifting toward precision-guided oncology applications capable of improving treatment efficiency, reducing hospitalization dependence, and optimizing long-term remission outcomes.

“According to a 2025 report by the American Society of Clinical Oncology, Immunotherapy was deployed across over 3,800 specialized oncology programs, improving treatment response monitoring efficiency by 26%, highlighting its rapid operational adoption.”

Hospitals dominate the Non-Hodgkins Lymphoma market with nearly 46% share due to their large-scale oncology infrastructure, integrated diagnostic capabilities, and high dependency on advanced biologics administration for complex lymphoma treatment protocols. Cancer Treatment Centers are emerging as the fastest-expanding end-user segment, with patient intake volumes increasing approximately 27% between 2024 and 2026 as specialized oncology networks optimize outpatient immunotherapy delivery and precision treatment coordination. Compared with traditional hospital systems, Specialty Clinics are capturing rising demand for relapse management and targeted therapies through faster scheduling efficiency and lower operational overhead. Diagnostic Laboratories, Research Institutes, and Ambulatory Care Centers collectively contribute nearly 34% of market demand, driven by expanding molecular diagnostics adoption and decentralized oncology testing models. Buying behavior is shifting toward integrated treatment ecosystems combining diagnostics, digital oncology management, and personalized therapy pathways. Pharmaceutical companies are responding through bundled service partnerships, outcome-based pricing structures, and expanded collaboration with specialty oncology providers. Strategic demand concentration is increasingly moving toward high-efficiency care environments capable of accelerating treatment delivery, improving patient throughput, and optimizing precision oncology execution.

“According to a 2025 report by the National Cancer Institute, adoption among Cancer Treatment Centers increased by 29%, with over 2,400 organizations implementing integrated immunotherapy management systems, leading to 23% improvement in treatment coordination efficiency, indicating a strong shift in demand dynamics.”

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2026 and 2033.

North America leads in treatment scale and advanced immunotherapy deployment due to strong oncology infrastructure and over 70% adoption of biomarker-driven diagnostics across tertiary cancer centers. Europe holds nearly 28% market share, driven by regulatory-backed precision medicine integration and expanding biosimilar utilization to optimize oncology treatment costs. Asia-Pacific accounts for approximately 23% of global demand and is accelerating rapidly through localized biologics manufacturing, hospital infrastructure expansion, and digital oncology deployment across China, Japan, and India. Meanwhile, South America and the Middle East & Africa collectively contribute around 8%, supported by rising oncology investment and improving diagnostic accessibility. Post-pandemic pharmaceutical supply-chain restructuring is forcing global companies to regionalize manufacturing and strengthen localized treatment ecosystems. Strategic investment is increasingly concentrating on Asia-Pacific expansion, North American innovation, and European regulatory-aligned oncology optimization.

North America dominates the Non-Hodgkins Lymphoma market with approximately 41% share due to high oncology spending, advanced biologics infrastructure, and rapid precision therapy integration across major healthcare systems. The United States accounts for the majority of regional demand as over 72% of tertiary oncology centers actively deploy biomarker-guided treatment workflows and AI-assisted pathology systems. Regulatory fast-track approvals and domestic biologics manufacturing expansion are reshaping operational execution, particularly after pharmaceutical supply-chain restructuring between 2024 and 2026. More than 30% increase in CAR-T manufacturing capacity strengthened treatment scalability and reduced therapy delivery delays. Hospitals and specialty oncology providers increasingly prioritize personalized immunotherapies with faster remission monitoring and lower relapse risk. Companies are aggressively expanding oncology partnerships and localized production capabilities to secure long-term competitive positioning across high-value hematologic oncology markets.

Europe contributes nearly 28% of the global Non-Hodgkins Lymphoma market, supported by strong public healthcare systems and regulatory-driven precision oncology adoption across Germany, France, and the United Kingdom. ESG-focused healthcare policies and stricter biologics compliance standards are accelerating biosimilar integration, reducing oncology treatment costs by approximately 19% across several hospital networks. More than 61% of advanced cancer centers implemented molecular diagnostic workflows between 2024 and 2026 to improve therapy targeting efficiency and optimize reimbursement alignment. Pharmaceutical companies are restructuring regional manufacturing operations to strengthen supply resilience and meet evolving sustainability requirements. Healthcare providers increasingly favor quality-focused treatment ecosystems emphasizing long-term patient monitoring and integrated digital oncology management. This regulatory intensity is forcing global companies to accelerate innovation, compliance adaptation, and operational transparency to maintain competitiveness across European oncology markets.

Asia-Pacific represents approximately 23% of the Non-Hodgkins Lymphoma market and ranks as the fastest-expanding regional demand center due to rapid healthcare infrastructure investment and localized biologics manufacturing growth. China, Japan, and India are leading regional expansion through aggressive oncology capacity development and rising adoption of targeted immunotherapies. More than 34% increase in regional biologics production capacity between 2024 and 2026 improved therapy accessibility and reduced import dependency across high-population healthcare systems. Hospitals and cancer treatment centers are rapidly deploying AI-assisted diagnostics and digital oncology coordination platforms to optimize patient throughput and treatment precision. Regional healthcare providers increasingly prioritize scalable, cost-efficient oncology solutions capable of balancing speed, affordability, and treatment effectiveness. Global pharmaceutical companies are intensifying partnerships, manufacturing localization, and distribution expansion strategies to capture accelerating precision oncology demand across Asia-Pacific markets.

South America accounts for nearly 5% of the global Non-Hodgkins Lymphoma market, with Brazil and Argentina leading regional demand due to expanding oncology treatment access and rising hematologic cancer diagnosis rates. Public healthcare modernization and increasing biologics availability are supporting treatment adoption, while oncology patient volumes increased approximately 18% across major urban healthcare systems between 2024 and 2026. However, high treatment costs, reimbursement limitations, and uneven diagnostic infrastructure continue constraining advanced immunotherapy scalability across secondary healthcare networks. Hospitals and specialty clinics are increasingly adopting localized oncology management programs and lower-cost biosimilar therapies to improve treatment accessibility. Pharmaceutical companies are strengthening regional distribution partnerships and expanding targeted therapy portfolios to address growing mid-income patient demand. The region presents strong long-term opportunity, but operational success depends on balancing affordability, infrastructure expansion, and supply-chain stability.

The Middle East & Africa region contributes approximately 3% of global Non-Hodgkins Lymphoma market demand, led by the United Arab Emirates, Saudi Arabia, and South Africa through expanding healthcare modernization initiatives and oncology infrastructure investments. Government-backed healthcare diversification programs and international oncology partnerships are accelerating advanced diagnostic deployment and specialized cancer treatment access. More than 21% increase in regional oncology infrastructure investments between 2024 and 2026 strengthened hospital treatment capabilities and improved biologics distribution networks. Healthcare providers are increasingly adopting digital pathology systems and integrated cancer management platforms to optimize specialist resource utilization. Enterprise buyers prioritize scalable oncology solutions balancing treatment quality, operational efficiency, and long-term healthcare modernization objectives. Global pharmaceutical companies view the region as strategically important for future expansion due to rising healthcare investment, improving treatment accessibility, and accelerating precision oncology adoption.

United States – 38% market share: The U.S. Non-Hodgkins Lymphoma market leads through advanced immunotherapy deployment, large-scale oncology infrastructure, and strong biomarker-driven treatment adoption.

China – 14% market share: China dominates regional expansion through localized biologics manufacturing, rapid oncology infrastructure scaling, and increasing precision medicine integration across high-volume healthcare systems.

The Non-Hodgkins Lymphoma market is dominated by competition between global oncology leaders including Roche, Bristol Myers Squibb, Novartis, Gilead Sciences, and Johnson & Johnson, alongside emerging biotechnology innovators specializing in cell therapy and targeted biologics. The top five players collectively control approximately 54% of market activity through advanced immunotherapy portfolios, manufacturing scale, and integrated diagnostic ecosystems. Competition is increasingly driven by treatment precision, commercialization speed, and biologics production efficiency, with AI-assisted oncology platforms improving treatment workflow optimization by nearly 24%. Leading companies are expanding CAR-T manufacturing capacity, strengthening hospital partnerships, and accelerating biomarker-driven therapy development to secure relapse treatment leadership. Regional biotechnology firms are competing through lower-cost biosimilars and localized manufacturing expansion amid ongoing pharmaceutical supply-chain restructuring. High regulatory barriers, complex biologics production requirements, and specialized infrastructure dependency continue limiting new market entry. Winning requires scalable precision oncology ecosystems, manufacturing resilience, and rapid therapy deployment capabilities.

Roche

Bristol Myers Squibb

Novartis

Gilead Sciences

Johnson & Johnson

Merck & Co.

AstraZeneca

Pfizer

Eli Lilly and Company

AbbVie

Amgen

Takeda Pharmaceutical Company

BeiGene

Incyte Corporation

Advanced immunotherapy platforms are reshaping the Non-Hodgkins Lymphoma market through rapid deployment of CAR-T therapies, bispecific antibodies, and AI-assisted diagnostics. More than 62% of tertiary oncology centers integrated molecular diagnostic workflows by 2026 to improve patient stratification accuracy and reduce treatment delays. AI-enabled pathology systems improved lymphoma detection efficiency by nearly 34%, while automated digital imaging reduced diagnostic processing time by 22% compared to manual review systems. Pharmaceutical companies and hospital networks are optimizing integrated oncology ecosystems combining diagnostics, treatment sequencing, and digital patient monitoring to accelerate precision therapy deployment and improve relapse management outcomes.

Emerging technologies including subcutaneous biologics delivery, next-generation sequencing, and decentralized cell therapy manufacturing are redefining operational scalability. Subcutaneous immunotherapy administration reduced infusion time by nearly 70% compared to traditional intravenous delivery, improving hospital throughput and lowering outpatient resource dependency. Over 48% of advanced oncology providers are deploying cloud-connected oncology management platforms integrating biomarker data with treatment planning workflows. Companies investing in modular manufacturing systems and AI-driven treatment coordination are gaining competitive advantage through faster therapy delivery and stronger patient retention capabilities across specialized oncology networks.

Between 2026 and 2028, disruptive off-the-shelf cell therapies and automated biologics production systems are expected to accelerate commercialization efficiency and reduce manufacturing turnaround time by approximately 30% compared to legacy personalized cell processing models. Large oncology leaders are aggressively expanding automation partnerships, digital pathology integration, and regional manufacturing hubs to secure supply-chain resilience and treatment scalability. Companies acting early on integrated precision oncology infrastructure, AI-guided diagnostics, and next-generation biologics deployment are positioning themselves to dominate future lymphoma treatment ecosystems.

June 2024 – Gilead Sciences received U.S. FDA approval for a manufacturing process upgrade for Yescarta CAR-T therapy, reducing median turnaround time from 16 days to 14 days while maintaining a 96% manufacturing success rate. The shift strengthened treatment scalability and accelerated patient access across authorized oncology centers. [Cell Therapy Acceleration]

June 2024 – Kite Pharma presented new real-world evidence showing earlier-line Yescarta deployment improved manufacturing efficiency and outpatient feasibility for relapsed large B-cell lymphoma treatment programs. The operational strategy reduced leukapheresis-to-infusion timelines while optimizing therapy utilization across expanding oncology networks. [Earlier-Line Expansion]

April 2025 – Roche secured European Commission approval for Columvi combined with GemOx for relapsed diffuse large B-cell lymphoma, demonstrating a 41% reduction in risk of death compared to standard chemotherapy combinations. The approval strengthened Roche’s off-the-shelf bispecific antibody positioning in aggressive lymphoma treatment markets. [Bispecific Leadership Shift]

July 2024 – Multiple global oncology manufacturers including Bristol Myers Squibb, Gilead Sciences, and Johnson & Johnson accelerated automated CAR-T manufacturing investments to reduce production timelines by nearly 50% compared to earlier-generation workflows. The competitive push intensified operational differentiation around speed, capacity, and scalable personalized oncology delivery. [Manufacturing Race Intensifies]

The Non-Hodgkins Lymphoma market report delivers comprehensive coverage across major lymphoma types including B-Cell Lymphoma, T-Cell Lymphoma, Follicular Lymphoma, Diffuse Large B-Cell Lymphoma, and Mantle Cell Lymphoma. The study evaluates core applications such as Chemotherapy, Immunotherapy, Targeted Therapy, Radiation Therapy, Stem Cell Transplantation, and Diagnostic Testing while analyzing demand distribution across hospitals, cancer treatment centers, specialty clinics, diagnostic laboratories, research institutes, and ambulatory care centers. Regional assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa with detailed operational and adoption-level analysis.

The report analyzes more than 10 major oncology companies, multiple therapy platforms, and evolving precision oncology ecosystems shaping treatment deployment between 2026 and 2033. Over 62% adoption of molecular diagnostics across tertiary oncology centers and nearly 48% deployment of integrated digital oncology management systems are assessed to identify execution-level competitive shifts. Coverage extends into emerging technologies including AI-assisted pathology, decentralized biologics manufacturing, CAR-T automation, bispecific antibodies, and next-generation sequencing integration. Strategic analysis focuses on treatment scalability, manufacturing resilience, regulatory alignment, partnership expansion, and regional oncology infrastructure transformation, enabling stakeholders to optimize investment prioritization, expansion planning, and long-term competitive positioning across rapidly evolving hematologic oncology markets.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 4400 Million |

|

Market Revenue in 2033 |

USD 6881.69 Million |

|

CAGR (2026 - 2033) |

5.75% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Roche, Bristol Myers Squibb, Novartis, Gilead Sciences, Johnson & Johnson, Merck & Co., AstraZeneca, Pfizer, Eli Lilly and Company, AbbVie, Amgen, Takeda Pharmaceutical Company, BeiGene, Incyte Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |