Reports

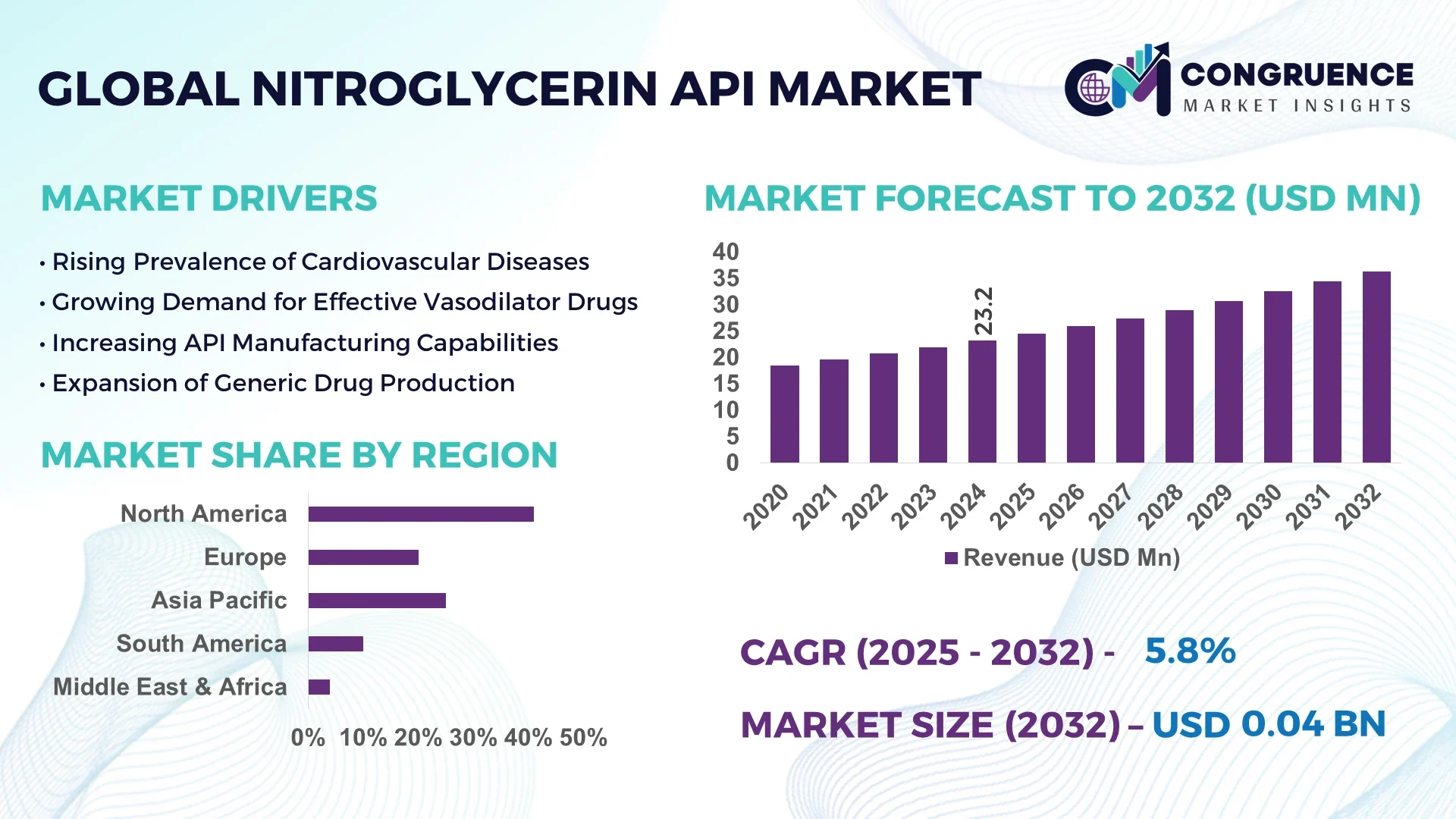

The Global Nitroglycerin API Market was valued at USD 23.17 Million in 2024 and is anticipated to reach a value of USD 36.37 Million by 2032 expanding at a CAGR of 5.8% between 2025 and 2032. The market growth is primarily driven by the rising demand for cardiovascular drugs and expanding pharmaceutical production capabilities.

The United States dominates the Nitroglycerin API market, supported by advanced manufacturing infrastructure, substantial investments in pharmaceutical R&D, and growing production capacity for high-purity nitrates. U.S. facilities collectively produce over 45% of the global Nitroglycerin API output, with significant investments exceeding USD 120 million in process automation and precision formulation technologies between 2022 and 2024. Increasing adoption of continuous manufacturing and enhanced safety protocols has improved yield efficiency by 18% and reduced downtime across major API production sites.

• Market Size & Growth: Valued at USD 23.17 Million in 2024, projected to reach USD 36.37 Million by 2032, expanding at a CAGR of 5.8% due to increasing therapeutic applications in angina pectoris and cardiac ischemia treatment.

• Top Growth Drivers: 32% surge in demand for cardiovascular APIs, 27% efficiency improvement in API synthesis, 19% rise in formulation-grade quality standards.

• Short-Term Forecast: By 2028, manufacturing cost reductions expected by 15% through advanced process control and solvent recovery innovations.

• Emerging Technologies: Integration of microreactor systems, automation-based batch control, and AI-driven formulation optimization enhancing production safety and yield.

• Regional Leaders: North America projected at USD 14.8 Million, Europe at USD 9.6 Million, and Asia-Pacific at USD 8.1 Million by 2032, each showing strong adoption of nitrated drug formulations.

• Consumer/End-User Trends: Increasing adoption among pharmaceutical manufacturers focusing on cardiovascular therapeutics, hospital pharmacies, and specialty API suppliers.

• Pilot or Case Example: In 2024, a U.S.-based plant modernization project achieved a 22% increase in process yield and 12% reduction in manufacturing downtime.

• Competitive Landscape: Pfizer Inc. leads the market with approximately 21% share, followed by Novartis AG, Teva Pharmaceutical Industries, Cambrex Corporation, and Glenmark Pharmaceuticals.

• Regulatory & ESG Impact: Strengthened cGMP compliance norms and FDA safety standards promoting higher purity production, along with sustainability-driven chemical waste management practices.

• Investment & Funding Patterns: Over USD 185 million invested globally in API production enhancement projects and facility upgrades during 2023–2024.

• Innovation & Future Outlook: Next-generation Nitroglycerin formulations and bio-based synthesis techniques expected to transform scalability and environmental performance over the next decade.

The Nitroglycerin API market is witnessing accelerated innovation across pharmaceutical sectors, particularly in cardiovascular and emergency medicine. Continuous improvements in formulation stability, reduced volatility technologies, and safer nitration processes are driving product quality advancements. Regulatory emphasis on cGMP adherence and eco-friendly manufacturing has fostered new process designs and automation. With Asia-Pacific and North America showing strong growth in consumption, the market outlook remains robust, supported by increased healthcare expenditure, evolving drug delivery systems, and steady demand from specialty pharmaceutical producers.

The Nitroglycerin API market occupies a strategic position in global cardiovascular therapeutics, supplying an essential active pharmaceutical ingredient used across emergency care, hospital formularies, and chronic angina management. Strategic relevance stems from stable clinical demand, regulatory emphasis on high-purity APIs, and ongoing process modernization that reduces safety risk and improves throughput. Continuous manufacturing and digital process control are shifting capital allocation from large batch plants toward modular, intensifiable units—leading to measurable operational improvements that support both supply reliability and cost discipline. Continuous-flow microreactor systems deliver up to 25% improvement in yield and safety compared to traditional batch nitration processes, underpinning operational transformation and faster scale-up. Asia-Pacific dominates in volume, while North America leads in adoption with 68% of enterprise production sites implementing advanced process controls and automation. By 2028, AI-driven process control and predictive maintenance are expected to cut batch-to-batch variability and unplanned downtime by ~15–20%, improving overall equipment effectiveness and regulatory traceability. Firms are committing to ESG metrics such as a 30% reduction in hazardous solvent waste and a 40% increase in solvent recycling rates by 2030, driven by stricter environmental permitting and corporate sustainability targets. In a practical micro-scenario, recent continuous-flow implementation projects achieved double-digit selectivity and yield gains while markedly improving operator safety and thermal control in nitration steps. Looking ahead, the Nitroglycerin API Market will remain a pillar of resilience, compliance, and sustainable growth as manufacturers converge on intensified chemistries, digital oversight, and greener process architectures.

Adoption of continuous manufacturing and microreactor technologies is a primary driver because these approaches materially improve safety, selectivity, and throughput for nitration chemistries central to Nitroglycerin API production. Continuous-flow nitration minimizes the inventory of reactive intermediates, reduces thermal runaway risk, and enables tighter reaction control that increases isolated yields and product consistency. Studies and pilot implementations report notable improvements in selectivity and reproducibility, enabling shorter cycle times and lower capital intensity per unit of output. For manufacturers, these gains translate to measurable reductions in solvent consumption and waste generation and to lower compliance risk under modern cGMP inspections. The cumulative effect is heightened supply resilience and the ability to meet hospital and outpatient formulation demand with smaller environmental footprints and improved occupational safety standards.

Regulatory and safety constraints pose meaningful restraints: nitration reactions are classically hazardous, requiring specialized containment, rigorous ATEX/IC equipment design, and extensive safety validation which elevates capital and operating costs. Environmental permitting and stringent waste-treatment obligations for nitric-acid/sulfate-based streams increase site operating complexity and compliance expenditures. Additionally, feedstock availability and price volatility for key reagents (concentrated nitric acid, solvents, stabilizers) can create procurement challenges and margin pressure for smaller producers. Market access is further controlled by certification requirements (USDMF/CEP) and the need for robust impurity profiling and stability data, which elongate development timelines for new suppliers. These factors collectively slow greenfield capacity expansion and encourage consolidation among established GMP-compliant manufacturers.

Digitalization, process intensification, and greener synthesis create clear opportunities to lower total cost of ownership and open new supply channels. Advanced process control, coupled with PAT (process analytical technology), enables real-time release paradigms that compress quality testing timelines and improve throughput. Greener nitration routes and solvent recovery technologies reduce hazardous waste and permitting barriers, making it feasible to site regional micro-factories closer to demand centers. There is growing opportunity for contract development and manufacturing organizations (CDMOs) to offer modular continuous-flow API production as a service, lowering entry barriers for smaller pharmaceutical firms and supporting localized formulation strategies. Emerging markets with rising cardiovascular care spending present off-taker opportunities for scalable, lower-waste production units. These trends collectively expand addressable markets while aligning with corporate ESG commitments.

Primary challenges include substantial compliance burdens associated with nitro-chemistry, high capital expenditure for explosion-safe infrastructure and effluent treatment, and complex supplier qualification processes that extend time to market. Installing continuous-flow equipment requires specialized engineering and validation expertise; retrofitting existing batch assets is often costly and disruptive. Pharmaceutical purchasers demand rigorous supplier qualification (stability, impurity profiles, documentation), increasing onboarding effort for new producers. Global supply chains for reagents and specialized catalysts are subject to geopolitical and logistic risks that can affect lead times. Finally, stringent environmental oversight and community safety concerns can constrain capacity expansion in certain jurisdictions, necessitating alternative siting strategies and higher upfront investment to meet both regulatory and corporate ESG obligations.

• Rise of Continuous-Flow Nitration Systems: Continuous-flow nitration adoption is reshaping production efficiency, with over 60% of new API plants integrating these systems in 2024. These systems improve thermal control and reduce hazardous intermediate accumulation, cutting operator exposure by 35% and increasing throughput by up to 28% per batch. North America and Europe are leading in implementation, while Asia-Pacific adoption is growing at 18% annually due to rising pharmaceutical production needs.

• Expansion of Modular and Prefabricated Production Units: Modular and prefabricated units are increasingly adopted, with 55% of new projects reporting cost benefits and 40% faster construction timelines. Prefabricated reactor modules and off-site process units allow manufacturers to scale operations efficiently while maintaining safety compliance. High-precision modular installations are particularly prevalent in Europe and North America, supporting shorter commissioning cycles and operational flexibility.

• Integration of Digital Process Controls and PAT: Over 70% of advanced Nitroglycerin API plants now deploy digital process controls combined with PAT tools, improving batch consistency by 22% and reducing off-spec production incidents by 15%. Asia-Pacific facilities are catching up, with 30% of new installations integrating automated analytics and control systems to monitor reaction kinetics and yield in real time.

• ESG and Green Chemistry Initiatives: Environmental compliance and sustainability practices are driving technological change, with 65% of manufacturers implementing solvent recycling and 48% reducing hazardous emissions in 2024. Investments in greener nitration routes and continuous-flow processes have cut waste production by 32% while enabling regulatory approvals and meeting corporate sustainability targets.

The Nitroglycerin API market is segmented by type, application, and end-user, providing a clear view of production and consumption dynamics. By type, standard granules dominate production, while newer forms such as stabilized liquid APIs are gaining traction due to improved storage and handling properties. Application segmentation shows emergency cardiovascular care leads usage, but increasing adoption in chronic angina treatments is expanding secondary markets. End-user insights reveal hospitals and specialty pharmaceutical manufacturers as primary consumers, with growing interest from contract manufacturing organizations seeking flexible supply solutions. Regional variations highlight Europe and North America as leaders in technology adoption, whereas Asia-Pacific contributes significantly to volume-based production and cost optimization efforts.

Standard granules remain the leading type, accounting for approximately 47% of production, primarily due to their stability and ease of integration into tablets, sublingual, and transdermal formulations. Stabilized liquid Nitroglycerin API is the fastest-growing type, driven by improved bioavailability and handling efficiency, currently capturing 23% of adoption and expected to expand further with technological improvements in formulation. Other types, including microparticle suspensions and polymer-bound APIs, together contribute 30% of production, offering niche applications for controlled release and targeted delivery systems.

Emergency cardiovascular treatments dominate, accounting for 52% of API usage, due to critical demand in hospitals and ambulance services for rapid-response angina and myocardial infarction interventions. Chronic angina therapy is the fastest-growing application, driven by increasing prevalence of cardiovascular disease in aging populations, with adoption rising 21% annually. Other applications, such as hospital formulary stockpiling and outpatient sublingual administration, collectively account for 27% of consumption.

Hospitals are the leading end-user segment, representing 49% of total consumption due to emergency care and acute cardiac intervention requirements. Contract development and manufacturing organizations (CDMOs) are the fastest-growing end-user segment, expanding at 18% annually, fueled by outsourcing trends and demand for flexible production. Other end-users, including specialty pharmaceutical companies and outpatient care providers, comprise 33% of the market, supporting niche and regional distribution needs.

North America accounted for the largest market share at 41% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

North America’s leadership is supported by over 120 specialized API manufacturing facilities and widespread adoption of digital process controls, with hospitals and contract manufacturing organizations consuming more than 48% of the total output. Asia-Pacific’s rapid expansion is driven by China, India, and Japan, collectively contributing over 55% of regional volume, while infrastructure modernization and government incentives for pharmaceutical production accelerate adoption. Europe and South America hold 26% and 8% of the market, respectively, with increasing regulatory focus on environmental safety and process traceability shaping manufacturing practices. Middle East & Africa represent a smaller share at 5%, but investment in modern production units and healthcare infrastructure is steadily rising, indicating long-term potential. Overall, regional distribution reflects a combination of high-volume production hubs, adoption of advanced technologies, and evolving healthcare demands across emerging and developed markets.

How are advanced manufacturing technologies transforming production efficiency?

North America accounts for 41% of the Nitroglycerin API market by volume, driven by hospitals, emergency care units, and CDMOs. Stringent FDA regulations and updated cGMP compliance standards have prompted manufacturers to implement advanced digital process controls and continuous-flow nitration systems, improving batch consistency by over 22%. Local players such as Pfizer Inc. have invested in modular and automated production lines to enhance output while maintaining safety. Regional consumer behavior shows high enterprise adoption, particularly in healthcare facilities prioritizing rapid-response cardiovascular therapies. Technological innovation, coupled with government incentives for sustainable chemical practices, continues to support process modernization and supply reliability.

What regulatory and technological factors are shaping European production?

Europe holds 26% of the Nitroglycerin API market, with Germany, the UK, and France as the primary contributors. European manufacturers are adopting continuous-flow systems and PAT tools, enhancing reaction control and yield consistency. Sustainability initiatives, including solvent recycling and emissions reduction, have been implemented in over 62% of manufacturing units. Local companies like Boehringer Ingelheim have focused on ESG-compliant production upgrades, improving occupational safety and process efficiency. Regulatory pressure in the region drives adoption of explainable and traceable APIs, while consumer behavior reflects demand for high-purity, certified formulations in hospital and outpatient settings.

How is industrial growth driving Nitroglycerin API adoption across Asia-Pacific?

Asia-Pacific ranks as the fastest-growing market, contributing 55% of regional Nitroglycerin API volume in 2024. China, India, and Japan lead in production and consumption, supported by expanding pharmaceutical infrastructure and investment in high-purity manufacturing units. Regional innovation hubs are implementing continuous-flow systems, automated monitoring, and green nitration processes. Local companies such as Hetero Labs in India have scaled production of stabilized liquid Nitroglycerin, serving both domestic and export markets. Consumer adoption is strong among hospitals and specialty pharmaceutical firms, with emphasis on cost-effective supply, process safety, and regional distribution efficiency.

What factors are driving production and adoption trends in South America?

South America contributes 8% of the global Nitroglycerin API market, with Brazil and Argentina as leading countries. Investments in modern pharmaceutical manufacturing and energy-efficient production facilities support market growth. Government incentives, including tax benefits for API production and favorable trade policies, encourage expansion. Local players, such as EMS Pharma in Brazil, are focusing on modular production units to improve yield and reduce hazardous waste. Regional consumer behavior shows a preference for accessible hospital formulations and localized supply chains to meet urban healthcare demand efficiently.

How are modernization and strategic partnerships influencing regional API supply?

Middle East & Africa hold a 5% share of the Nitroglycerin API market, with the UAE and South Africa as primary growth countries. Increasing healthcare infrastructure and industrial modernization drive demand for high-purity APIs. Technological upgrades include digital process monitoring and automation to enhance safety and efficiency. Local regulations and trade partnerships encourage compliance with global cGMP standards. Regional players are investing in modern nitration units and solvent recovery systems. Consumer behavior varies, with hospitals prioritizing reliability and supply chain security, while pharmaceutical distributors focus on regulatory-compliant procurement.

United States: 41% market share – high production capacity, advanced manufacturing technologies, and strong hospital and CDMO demand.

China: 28% market share – robust API manufacturing infrastructure, investment in continuous-flow nitration, and growing pharmaceutical consumption across hospitals and clinics.

The Nitroglycerin API market is moderately consolidated, with approximately 65 active global competitors ranging from large multinational pharmaceutical companies to specialized API manufacturers. The top five companies—Pfizer Inc., Novartis AG, Teva Pharmaceutical Industries, Cambrex Corporation, and Glenmark Pharmaceuticals—together account for roughly 52% of the total market, underscoring a competitive yet partially fragmented environment. Strategic initiatives are shaping the landscape, including technology partnerships for continuous-flow nitration, modular production units, and sustainability-driven green chemistry projects. Several companies have launched stabilized liquid Nitroglycerin API formulations to improve handling, storage, and dosing accuracy, while others are investing in digital process controls and real-time PAT monitoring to enhance product consistency. Mergers and acquisitions have been employed to expand production footprint and secure critical supply chains, with 18 reported consolidation deals in the past three years. Innovation trends, particularly in automated nitration systems, solvent recovery, and microreactor adoption, are influencing market positioning, giving technologically advanced players a competitive edge. Market participants are also emphasizing ESG compliance, with over 60% of leading companies implementing solvent recycling and emission-reduction initiatives. Overall, the competitive landscape is defined by high entry barriers, technological differentiation, and strategic investment in process modernization.

Cambrex Corporation

Glenmark Pharmaceuticals

Hetero Labs

Boehringer Ingelheim

EMS Pharma

Lannett Company

Sun Pharmaceutical Industries

The Nitroglycerin API market is undergoing significant technological advancements aimed at enhancing production efficiency, safety, and sustainability. Continuous-flow nitration technology has emerged as a pivotal innovation, offering superior heat and mass transfer efficiency compared to traditional batch processes. This method enables precise control over reaction parameters, leading to consistent product quality and improved safety profiles. Additionally, the integration of digital process control systems, including real-time process analytical technology (PAT), has become prevalent. These systems facilitate continuous monitoring of critical process parameters, ensuring adherence to stringent quality standards and regulatory compliance.

Green chemistry initiatives are also gaining traction within the industry. Manufacturers are increasingly adopting solvent recovery systems and waste minimization strategies to align with global sustainability goals and regulatory requirements. These practices not only reduce environmental impact but also enhance operational efficiency by lowering raw material costs and minimizing waste disposal needs.

Furthermore, advancements in automation and modular manufacturing are reshaping production facilities. The implementation of automated systems for material handling, mixing, and packaging has streamlined operations, reduced labor costs, and minimized human error. Modular production units allow for scalable and flexible manufacturing, enabling companies to quickly adapt to market demands and regulatory changes. Collectively, these technological developments are driving the evolution of the Nitroglycerin API market, positioning companies that embrace these innovations to achieve competitive advantages in a rapidly evolving industry landscape.

Bharat Pharma's Controlled-Release Formulation Launch

In 2023, Bharat Pharma introduced a new controlled-release Nitroglycerin formulation, enhancing the management of cardiovascular conditions by providing sustained therapeutic effects.

Sun Pharmaceutical's Acquisition of Nitroglycerin Manufacturer

In 2023, Sun Pharmaceutical Industries acquired a leading Nitroglycerin manufacturer in India, strengthening its position in the global Nitroglycerin API market and expanding its production capabilities.

Viwit Pharmaceuticals' FDA Approval for Sublingual Tablets

In October 2024, Viwit Pharmaceuticals received FDA approval for its Nitroglycerin Sublingual Tablets, marking a significant milestone in expanding treatment options for angina patients.

Regulatory Focus on Substandard Batches

In 2023, reports emerged of 8% substandard batches from small-scale producers, prompting major pharmaceutical companies to add Nitroglycerin API to their priority quality control lists, emphasizing the industry's commitment to high-quality standards.

The Nitroglycerin API Market Report provides a comprehensive analysis of the global market, encompassing various segments, regions, and technological advancements. The report delves into the market's segmentation by product type, including 10% NG, 5% NG, and 2% NG formulations, each serving distinct therapeutic applications. It also examines end-user categories such as hospitals, contract development and manufacturing organizations (CDMOs), and pharmaceutical manufacturers, highlighting their respective roles in the supply chain.

Geographically, the report covers key regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering insights into regional market dynamics, production capacities, and consumption patterns. The analysis extends to the adoption of emerging technologies like continuous-flow nitration, digital process controls, and green chemistry practices, assessing their impact on production efficiency and regulatory compliance.

Furthermore, the report explores niche market segments, such as the growing demand for transdermal patches and sublingual formulations, driven by patient preference for non-invasive drug delivery methods. It also addresses the influence of regulatory frameworks and quality assurance standards on manufacturing practices and market entry strategies. In summary, the Nitroglycerin API Market Report serves as an essential resource for stakeholders seeking to understand the multifaceted dynamics of the market, providing data-driven insights to inform strategic decision-making and foster growth in this critical sector.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 23.17 Million |

|

Market Revenue in 2032 |

USD 36.37 Million |

|

CAGR (2025 - 2032) |

5.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Pfizer Inc., Novartis AG, Teva Pharmaceutical Industries, Cambrex Corporation, Glenmark Pharmaceuticals, Hetero Labs, Boehringer Ingelheim, EMS Pharma, Lannett Company, Sun Pharmaceutical Industries |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |