Reports

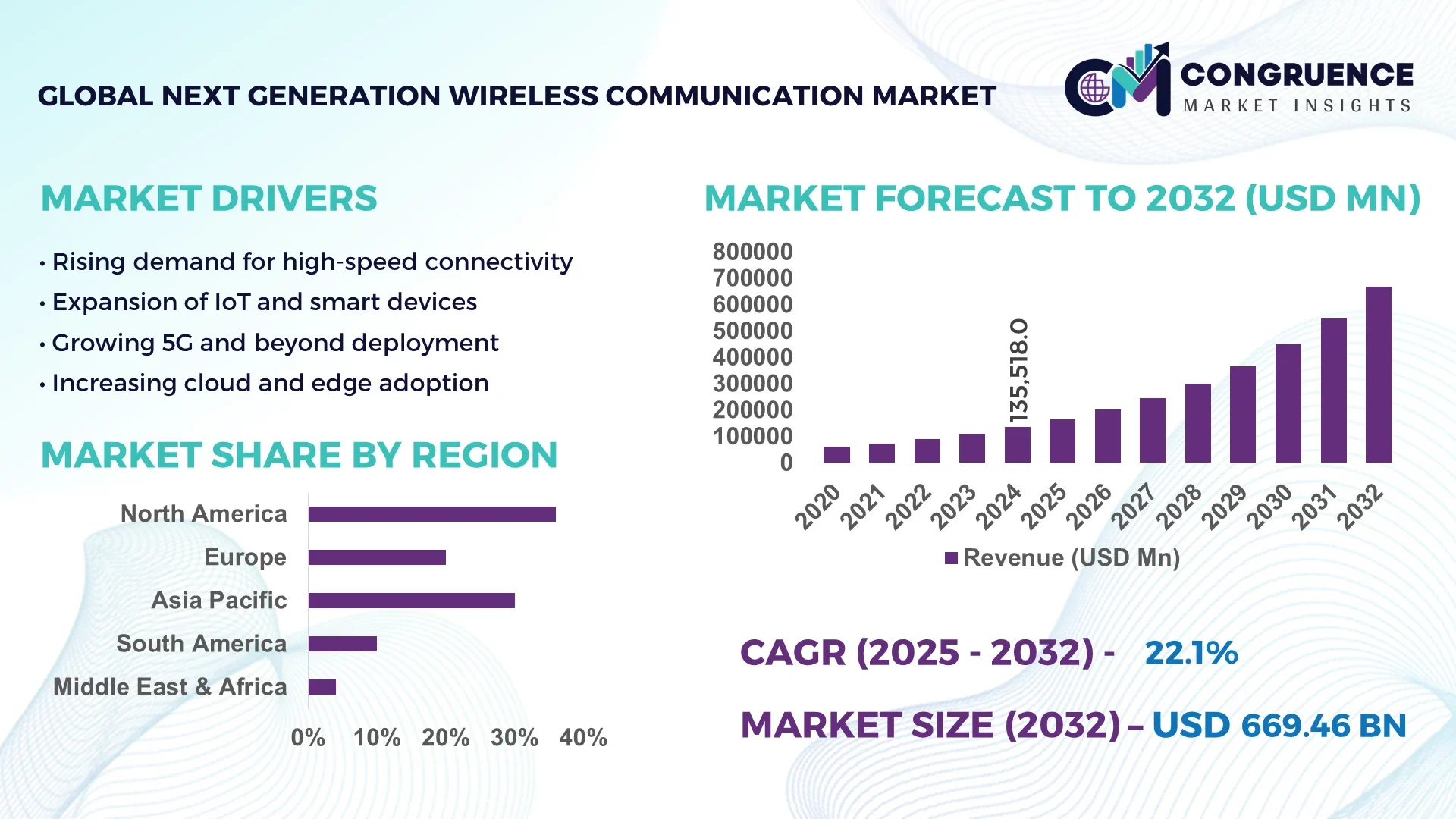

The Global Next Generation Wireless Communication Market was valued at USD 135518 Million in 2024 and is anticipated to reach a value of USD 669460 Million by 2032 expanding at a CAGR of 22.1% between 2025 and 2032.

In this landscape, a leading country plays a pivotal role through substantial production capacity, major investment in infrastructure and R&D, deployment of advanced testbeds across diverse environments such as urban, industrial, and rural zones, and continuous technological advancement in areas like beamforming, sub terahertz experimentation, and energy efficient networking components.

Key industry sectors driving demand include telecommunications service providers, automotive applications such as vehicle to everything connectivity, industrial automation supporting smart manufacturing, consumer electronics like XR devices, and aerospace and satellite systems. Recent technological and product innovations include AI powered adaptive beam shaping using metasurfaces to steer signals around obstacles, transformer assisted millimeter wave channel state feedback for more reliable high speed 5G and 6G links, and AI native air interface modems capable of learning new waveforms and modulation strategies in real time. Regulatory, environmental, and economic drivers comprise evolving spectrum policies for sub THz and NTN access, sustainability targets encouraging energy efficient designs, and macroeconomic stimulus for digital infrastructure. Regional consumption patterns reveal rapid uptake in urban and suburban regions, particularly in Asia Pacific and North America, where demand from smart city deployments and automotive sectors is robust. Growth factors include increased spectrum availability, convergence of communication and sensing functions, and supportive public private partnerships. Emerging trends include semantic communication focusing on conveying meaning rather than raw data, convergence of satellite based 5G for remote inclusion, and momentum toward 6G architectures offering pervasive, intelligent, and context aware connectivity for mission critical applications.

Artificial intelligence is fundamentally reshaping the Next Generation Wireless Communication Market by enabling unprecedented levels of network intelligence, performance optimization, and adaptive automation. AI driven orchestration and management across network layers from edge to core empower operators to deliver reliably ultra low latency, high throughput services while reducing manual intervention. AI improves operational performance by streamlining traffic prediction, load balancing, self organizing networks, and real time anomaly detection. AI empowered control enables predictive maintenance, dynamically adapting to shifting radio conditions and user mobility. AI powered network optimization is pivotal to 5G Advanced and emerging 6G networks, facilitating smarter resource allocation, spectral efficiency, and highly customized network slicing that meets diverse application requirements across industries.

Concrete advances include AI powered transformer assisted channel state information feedback systems for millimeter wave massive MIMO, which mitigate rapid mobility induced signal degradation by predicting and correcting errors in real time, ensuring faster and more reliable next generation wireless links. Meanwhile, AI driven air interface systems now employ deep learning at both transmitters and receivers, dynamically learning new waveforms and modulation techniques to enhance RAN efficiency and spectrum utilization. Edge computing combined with AI enables deep reinforcement learning mediated optimization in Open RAN and MEC architectures, delivering efficient computation offloading, energy savings, and improved QoS. The deliberate integration of AI across the network stack is transforming the Next Generation Wireless Communication Market by enhancing automation, reliability, security, and efficiency. Industry leaders increasingly rely on AI to support rapidly rising demand for immersive XR services, autonomous systems, and industrial IoT, ensuring networks are intelligent, responsive, and scalable in real time.

“2024 Researchers at Incheon National University published a transformer assisted parametric CSI feedback method in IEEE Transactions on Wireless Communications, using AI to predict and correct millimeter wave channel aging in massive MIMO systems. The AI powered method significantly improved the reliability and speed of high mobility next generation wireless links in real world scenarios.”

The Next Generation Wireless Communication Market is undergoing rapid transformation driven by the convergence of advanced technologies, regulatory frameworks, and evolving consumer demands. Increasing adoption of 5G Advanced and ongoing development toward 6G networks are redefining connectivity through ultra low latency, enhanced bandwidth, and context aware communication. The market is strongly influenced by the rising integration of AI, machine learning, and edge computing, which enable automated, efficient, and resilient network operations. Industry insights indicate strong momentum across industrial automation, automotive connectivity, and immersive media applications, reflecting broad cross sector reliance on robust wireless solutions. Additionally, governments and enterprises are actively investing in spectrum allocation, sustainable infrastructure, and satellite connectivity, creating favorable conditions for expansion. These dynamics collectively position the market for accelerated innovation and broader adoption across developed and emerging regions.

The demand for ultra low latency communication is a major driver in the Next Generation Wireless Communication Market as industries increasingly adopt smart factories and industrial IoT. For example, applications such as predictive maintenance, robotic process automation, and digital twin modeling require latency levels below one millisecond to function seamlessly. The adoption of private 5G and the testing of 6G prototypes have enhanced real time control systems, enabling more precise and reliable machine to machine communication. This growth is supported by ongoing industrial investments in automation, with manufacturing hubs across Asia Pacific and Europe deploying next generation wireless solutions to optimize efficiency and reduce downtime. Such advancements are ensuring scalability and reliability in highly demanding operational environments.

One of the key restraints in the Next Generation Wireless Communication Market is spectrum scarcity combined with the significant cost of infrastructure development. As demand for advanced wireless networks grows, operators are under pressure to secure additional frequency bands, including millimeter wave and sub terahertz ranges, which are limited and heavily regulated. Building dense small cell networks and integrating AI powered architectures demand substantial capital expenditure, which poses barriers for smaller service providers. Furthermore, energy costs associated with high performance infrastructure increase operational burdens. These factors collectively delay large scale deployments in certain regions and create disparities in accessibility between urban and rural zones, slowing overall market adoption despite strong demand.

The integration of satellite technology with terrestrial networks presents a significant opportunity in the Next Generation Wireless Communication Market. Emerging non terrestrial networks (NTN) are enabling seamless coverage in remote and underserved areas, supporting global connectivity goals. With satellite constellations being launched for direct to device services, industries such as maritime, aviation, and defense are set to benefit from uninterrupted, secure communication. In addition, this integration enhances disaster recovery capabilities and supports nationwide digital transformation programs. For businesses, satellite linked wireless systems ensure continuous operations across geographically dispersed assets, reducing downtime and enabling data intensive applications even in isolated regions. This opportunity is expanding the market’s reach beyond urban centers into truly global, inclusive connectivity.

Security and privacy risks present a critical challenge in the Next Generation Wireless Communication Market as AI integration deepens within core and edge networks. The use of AI algorithms for network orchestration, predictive analysis, and automated decision making exposes communication infrastructures to cyber vulnerabilities. Attack surfaces expand as billions of IoT devices connect through next generation networks, increasing the risk of data breaches and unauthorized access. Safeguarding sensitive industrial, governmental, and consumer data requires robust encryption, zero trust frameworks, and continuous monitoring, all of which demand high investment and skilled expertise. Balancing the push for innovation with stringent cybersecurity standards remains a pressing difficulty for operators, regulators, and enterprises adopting next generation wireless technologies.

Adoption of Terahertz Frequency Research for 6G Development: The transition toward terahertz frequency research is a defining trend in the Next Generation Wireless Communication Market. Laboratory trials and field experiments are demonstrating data rates exceeding 100 Gbps over short distances, unlocking capabilities for immersive XR and holographic applications. Several nations are allocating research funds to accelerate terahertz technology, which is expected to support ultra high capacity wireless backhaul and advanced sensing functionalities. This trend is shaping the foundation for 6G commercialization and influencing equipment design, spectrum planning, and regulatory adjustments across multiple regions.

Expansion of Open RAN and Virtualized Network Architectures: The rapid adoption of Open RAN solutions is transforming network deployment strategies in the Next Generation Wireless Communication Market. Operators are increasingly deploying software defined and virtualized platforms that allow vendor interoperability and cost effective rollouts. By 2025, trials indicate that large scale operators are achieving up to 30% savings in capital expenditures by shifting toward cloud native, AI optimized architectures. This trend not only reduces dependency on single vendors but also accelerates the deployment of tailored wireless networks to serve enterprise specific requirements such as private 5G and industrial IoT connectivity.

Integration of Non Terrestrial Networks for Global Coverage: A significant market trend is the integration of non terrestrial networks with terrestrial infrastructures to deliver uninterrupted connectivity. Satellite constellations in low earth orbit are now offering direct to device services, enabling global access without additional ground infrastructure. The Next Generation Wireless Communication Market is seeing strong adoption across maritime, aviation, and defense sectors where reliable coverage is essential. This integration also enhances disaster recovery communication and supports governments’ objectives of digital inclusion, bridging the connectivity gap in remote regions while expanding opportunities for cross sector applications.

Emergence of Semantic and AI Native Communication Systems: The development of semantic communication, where transmitted data focuses on meaning rather than raw content, is gaining traction in the Next Generation Wireless Communication Market. AI native systems are being deployed to interpret, compress, and optimize messages dynamically, reducing bandwidth usage while maintaining accuracy. Trials in 2024 demonstrated bandwidth savings of over 60% in machine to machine communication scenarios using semantic models. This evolution is particularly impactful in industrial IoT and smart city deployments, where millions of connected devices generate continuous streams of data that must be efficiently managed.

The Next Generation Wireless Communication Market is segmented by type, application, and end-user, reflecting diverse adoption patterns across industries. By type, segments such as 5G Advanced, 6G prototypes, millimeter wave, sub terahertz solutions, and satellite integrated systems are shaping the technological base. Applications span industrial automation, autonomous vehicles, consumer electronics, healthcare, aerospace, and immersive media, each contributing uniquely to overall demand. End-user insights highlight adoption across telecom operators, enterprises, government agencies, and defense organizations, driven by varying infrastructure priorities and investment scales. These segmentation insights reflect how different technologies and user groups are shaping the evolution of next generation connectivity globally.

In the Next Generation Wireless Communication Market, 5G Advanced remains the leading type, driven by its widespread deployment across urban centers and industrial clusters. Its maturity and ability to support ultra reliable low latency communication and massive IoT connections have positioned it as the backbone of current wireless strategies. The fastest growing type is 6G prototypes, supported by rapid global R&D investment and experimental testbeds that demonstrate terahertz level transmission speeds and AI integrated functionalities. Satellite integrated systems are emerging as a niche but highly significant type, particularly for industries requiring seamless coverage across remote regions such as aviation and maritime. Millimeter wave and sub terahertz systems are also gaining ground, serving as critical enablers for high bandwidth and short range applications, including factory automation and immersive XR experiences. Together, these types illustrate a layered market evolution where established and experimental technologies coexist to address diverse connectivity demands.

Industrial automation is the leading application in the Next Generation Wireless Communication Market, as factories, logistics hubs, and production lines rely on low latency, reliable networks for predictive maintenance, robotics, and smart manufacturing. Autonomous vehicles are the fastest growing application, with vehicle to everything communication demanding ultra reliable and high speed wireless links for navigation, safety, and infotainment. Consumer electronics, particularly AR and VR devices, are also significant, benefiting from bandwidth intensive and low latency communication to support immersive user experiences. Aerospace and satellite communication continue to play a strategic role, with demand rising for defense grade secure systems and commercial inflight connectivity. Healthcare is another notable application, where remote surgeries and real time monitoring require resilient networks to ensure accuracy and patient safety. The breadth of these applications underscores the central role of next generation wireless systems in supporting advanced industries and critical infrastructure.

Telecom operators remain the leading end-users in the Next Generation Wireless Communication Market, as they are at the forefront of deploying infrastructure, spectrum management, and delivering connectivity services to consumers and enterprises. Enterprises represent the fastest growing end-user segment, particularly in manufacturing, logistics, and financial services, where private 5G and AI driven wireless solutions are enabling operational efficiency and digital transformation. Government agencies are also major participants, investing in smart city projects, nationwide coverage programs, and digital inclusion initiatives. Defense organizations maintain a steady role, leveraging next generation wireless systems for secure communication, surveillance, and tactical operations. Consumer adoption, while indirect, further drives the market as demand for XR experiences, mobile applications, and IoT devices expands. Collectively, these end-users define the trajectory of wireless communication by shaping investment priorities, regulatory landscapes, and technology integration strategies across global markets.

North America accounted for the largest market share at 36% in 2024 however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 25.3% between 2025 and 2032.

Growth in the Next Generation Wireless Communication Market is shaped by varied regional dynamics, including technological maturity, regulatory frameworks, and sector-specific adoption patterns. Established markets are driving large-scale infrastructure rollouts, while emerging economies are accelerating adoption through nationwide digitalization programs and rising consumer demand for connected services. Regional differences in spectrum allocation, investment intensity, and industry participation highlight the global diversity in market expansion.

Advanced Infrastructure Rollouts Supporting Industrial Connectivity

North America held a market share of 36% in 2024, reflecting its established leadership in the Next Generation Wireless Communication Market. Key industries driving demand include automotive, aerospace, and industrial automation, supported by strong adoption of private 5G and early 6G research programs. Regulatory bodies have introduced spectrum reallocations to enhance connectivity for enterprises and consumers, enabling faster adoption of high-capacity networks. Government support for nationwide broadband expansion and investments in Open RAN solutions are accelerating deployment. Notable digital transformation trends include adoption of AI-enabled network orchestration, seamless integration of edge computing, and growing demand for immersive XR platforms, positioning the region as a pioneer in advanced wireless communication.

Commitment to Green Connectivity and Digital Sovereignty

Europe accounted for approximately 27% market share in 2024 within the Next Generation Wireless Communication Market, with Germany, the UK, and France leading adoption. The European Union’s regulatory bodies have emphasized sustainability and green connectivity, driving energy-efficient wireless solutions across industries. Initiatives such as carbon-neutral data centers and stricter emissions targets are influencing equipment design and deployment strategies. Technological adoption is accelerating, with industries embracing private 5G for smart factories and early pilots of 6G across research hubs. Key European markets are also prioritizing digital sovereignty, fostering secure supply chains and interoperable network architectures to ensure resilience against global disruptions.

Innovation Hubs Accelerating Mass Adoption of Next Generation Networks

Asia Pacific is the fastest-growing region in the Next Generation Wireless Communication Market, holding 25% of market volume in 2024 and advancing rapidly with strong infrastructure expansion. China, Japan, and India are the top consuming countries, each investing heavily in nationwide wireless rollouts and industrial digitalization. Manufacturing clusters in China and India are adopting ultra-reliable low-latency networks to drive Industry 4.0. Japan’s innovation hubs are testing terahertz communication and AI-powered wireless platforms to support 6G advancements. The region’s expanding population of connected devices, coupled with government-backed programs for smart cities and digital inclusion, is accelerating the adoption of high-performance wireless communication systems.

Rising Connectivity Investments in Emerging Economies

South America contributed about 6% market share in 2024 to the Next Generation Wireless Communication Market, with Brazil and Argentina leading deployments. Infrastructure upgrades in metropolitan areas and expanding energy and mining sectors are creating strong demand for advanced wireless solutions. Governments are introducing tax incentives and trade policies to encourage foreign investment in digital infrastructure projects. Brazil’s adoption of private 5G in industrial corridors is advancing operational efficiency, while Argentina is focusing on enhancing urban connectivity to support digital businesses. This regional growth is characterized by targeted modernization programs and integration of next generation networks into critical sectors.

Strategic Investments in Smart Cities and Energy Connectivity

The Middle East and Africa accounted for 6% market share in 2024 within the Next Generation Wireless Communication Market, with UAE and South Africa emerging as major growth countries. Regional demand trends are driven by oil and gas, construction, and smart city projects, where high-capacity and resilient communication networks are essential. Governments are forming partnerships to accelerate 5G and early-stage 6G deployments, supported by regulations that encourage international investment. Technological modernization trends include AI-driven network optimization, smart grid integration, and next-gen connectivity for logistics and ports. Strategic projects in energy and urban development are positioning the region as a growing participant in global wireless innovation.

United States – 24% market share: Dominance supported by advanced infrastructure deployment, high enterprise adoption of private 5G, and strong federal investment in wireless R&D.

China – 20% market share: Leadership driven by large-scale manufacturing demand, rapid smart city projects, and aggressive investment in 6G research and terahertz technology.

The competitive environment in the Next Generation Wireless Communication Market is characterized by the presence of over 120 active global and regional competitors, ranging from telecom giants to specialized technology innovators. Leading players are positioning themselves through strategic investments in 5G Advanced and early 6G research, aiming to secure technological leadership and long-term market influence. The landscape is marked by frequent partnerships between network operators, equipment manufacturers, and software providers to accelerate Open RAN adoption, expand spectrum utilization, and integrate AI-driven optimization tools. Recent years have witnessed a surge in product launches targeting enterprise connectivity, industrial IoT, and XR applications, alongside mergers and acquisitions designed to strengthen intellectual property portfolios and expand global reach. Innovation trends such as terahertz communication, semantic transmission, and AI-native air-interface systems are shaping the competitive frontier, compelling companies to differentiate through R&D intensity, ecosystem collaborations, and the ability to provide sustainable, energy-efficient wireless solutions. This dynamic competition underscores the strategic importance of technological agility, regulatory compliance, and diversified service offerings in sustaining market leadership.

Ericsson

Nokia Corporation

Huawei Technologies Co., Ltd.

Samsung Electronics Co., Ltd.

ZTE Corporation

Qualcomm Incorporated

Intel Corporation

Cisco Systems, Inc.

NEC Corporation

Fujitsu Limited

Keysight Technologies

MediaTek Inc.

Telefonaktiebolaget LM Ericsson

Juniper Networks, Inc.

Ciena Corporation

The Next Generation Wireless Communication Market is being shaped by a wave of advanced technologies that are driving innovation, efficiency, and expanded applications across industries. Among the most significant is the development of terahertz (THz) communication, which enables data rates exceeding 100 Gbps for short-range transmission, paving the way for holographic communications, advanced industrial automation, and immersive XR services. Millimeter wave technology continues to play a critical role, with deployment expanding across dense urban environments where high capacity and low latency are essential.

Artificial intelligence and machine learning are deeply embedded into wireless systems, powering predictive maintenance, adaptive beamforming, and dynamic spectrum allocation. These advancements allow networks to anticipate demand fluctuations and self-optimize, reducing latency and improving efficiency. Non-terrestrial networks (NTN) are another transformative technology, integrating satellite and aerial platforms to provide seamless connectivity in remote regions. In 2024, multiple low-earth orbit satellite constellations began testing direct-to-device connectivity, signaling a future of global accessibility without reliance on ground-based infrastructure.

Energy efficiency and sustainability are also emerging as key technology drivers. Intelligent power-saving protocols and green hardware design are reducing the carbon footprint of large-scale wireless systems. Open RAN and virtualized network architectures are further reshaping the ecosystem by promoting vendor interoperability, reducing costs, and enabling rapid innovation. Together, these technologies underscore the evolution toward 6G systems, which are expected to combine ultra-high speed, semantic communication, and integrated sensing capabilities for truly ubiquitous, intelligent connectivity.

• In March 2023, Samsung Electronics successfully tested 6G terahertz spectrum transmission over 120 meters indoors, achieving data speeds beyond 100 Gbps, marking a significant milestone for ultra-fast wireless connectivity and laying groundwork for future commercial 6G deployments.

• In October 2023, Nokia deployed its first commercial 5G-Advanced private wireless network with AI-enabled optimization for a European manufacturing hub, enabling sub-5 millisecond latency and supporting real-time robotics and automated guided vehicles.

• In May 2024, Huawei unveiled its AI-native 5.5G core network designed to support 10 Gbps downlink speeds and one-millisecond latency, with trials demonstrating enhanced reliability for industrial IoT and autonomous mobility applications.

• In July 2024, Ericsson launched an integrated non-terrestrial network solution supporting direct-to-device connectivity via low-earth orbit satellites, ensuring global coverage for maritime, aviation, and defense communication with seamless handover across terrestrial and satellite links.

The scope of the Next Generation Wireless Communication Market Report encompasses a comprehensive analysis of technologies, applications, geographic regions, and end-user industries shaping the evolution of advanced connectivity. The report covers all key segments, including 5G-Advanced, emerging 6G prototypes, millimeter wave systems, sub-terahertz solutions, and non-terrestrial networks. Each segment is analyzed in terms of adoption trends, technical innovation, and industry relevance, with special attention to the convergence of AI, edge computing, and cloud-native network architectures. Applications evaluated include industrial automation, autonomous vehicles, healthcare, aerospace, consumer electronics, smart cities, and immersive XR platforms, reflecting the market’s wide-ranging impact on both critical infrastructure and consumer-driven sectors. End-user insights highlight telecom operators, enterprises, governments, and defense organizations, each with distinct investment strategies and adoption patterns.

Geographically, the report provides in-depth analysis of North America, Europe, Asia Pacific, South America, and the Middle East & Africa, capturing regional growth dynamics, regulatory frameworks, and investment priorities. It further highlights niche opportunities such as semantic communication systems, green communication technologies, and satellite-integrated connectivity. Overall, the report’s scope delivers a structured view of the market’s competitive, technological, and regional landscape, offering business decision-makers a detailed yet holistic understanding of current developments and emerging opportunities across the global Next Generation Wireless Communication ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 135518 Million |

|

Market Revenue in 2032 |

USD 669460 Million |

|

CAGR (2025 - 2032) |

22.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Ericsson, Nokia Corporation, Huawei Technologies Co., Ltd., Samsung Electronics Co., Ltd., ZTE Corporation, Qualcomm Incorporated, Intel Corporation, Cisco Systems, Inc., NEC Corporation, Fujitsu Limited, Keysight Technologies, MediaTek Inc., Telefonaktiebolaget LM Ericsson, Juniper Networks, Inc., Ciena Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |