Reports

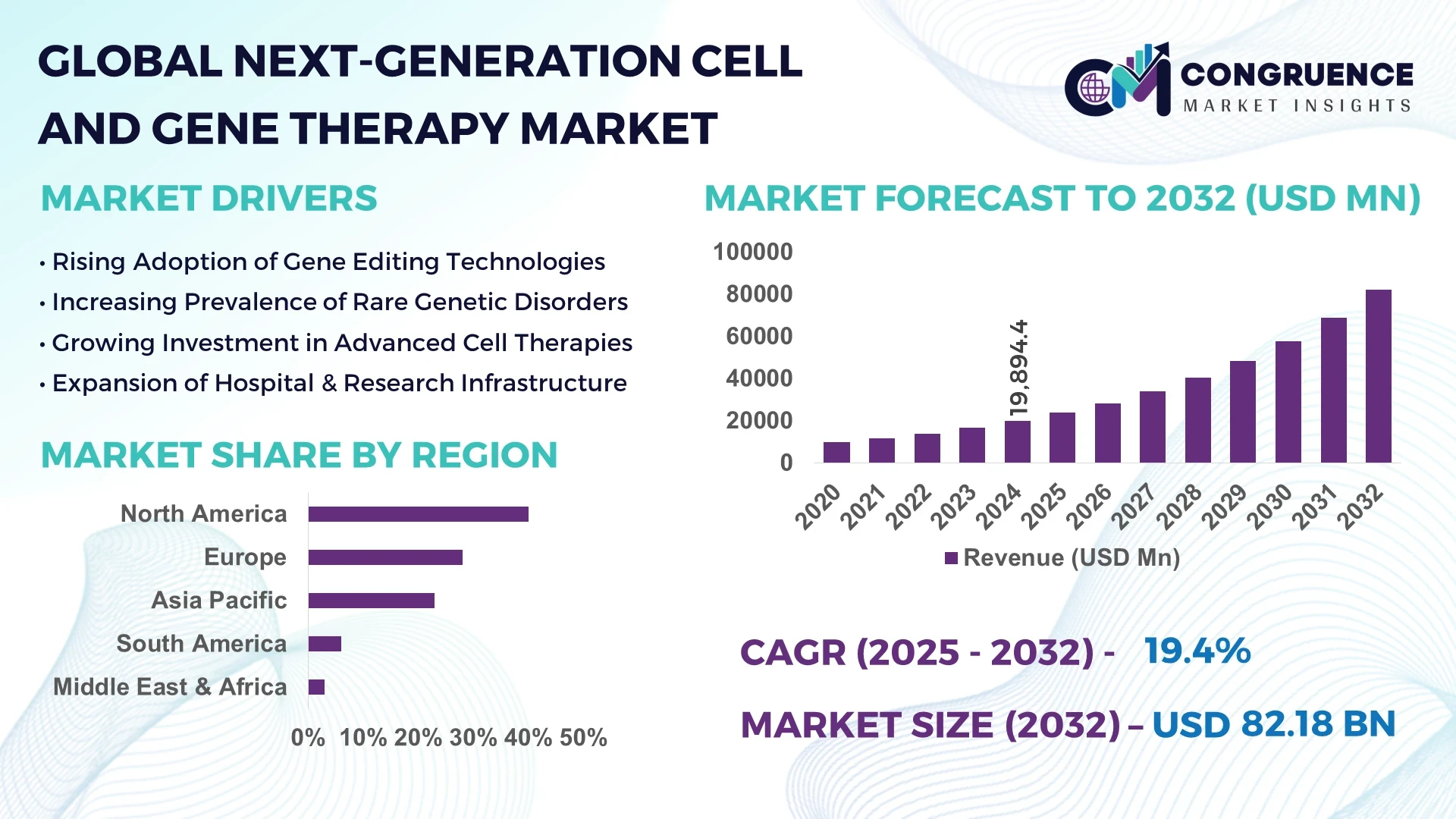

The Global Next-Generation Cell And Gene Therapy Market was valued at USD 19,894.4 Million in 2024 and is anticipated to reach USD 82,179.9 Million by 2032, expanding at a CAGR of 19.4% between 2025 and 2032.

The United States maintains a strong position in this market, with extensive biomanufacturing capacity, advanced clinical trial networks, and sustained government funding in regenerative medicine. The country has also established specialized innovation hubs that accelerate pre-clinical and translational research for cell and gene-based therapies.

The Next-Generation Cell And Gene Therapy Market is undergoing rapid expansion across oncology, rare genetic disorders, cardiovascular conditions, and neurology. Breakthroughs in CAR-T and CRISPR-based technologies are reshaping therapeutic strategies, while regulatory bodies are introducing accelerated approval pathways to support innovation. Increased adoption of allogeneic cell therapies, advancements in viral and non-viral delivery systems, and greater focus on scalable manufacturing are driving industrial growth. Furthermore, the global demand for precision medicine and personalized treatment models is fostering new partnerships among pharmaceutical firms, biotechnology start-ups, and research institutions. Regional consumption patterns indicate strong demand in North America and Europe, while Asia-Pacific is emerging as a high-potential hub due to growing clinical infrastructure and government investment in biotech.

Artificial intelligence is significantly reshaping the Next-Generation Cell And Gene Therapy Market by optimizing drug discovery, accelerating biomarker identification, and streamlining clinical trial design. AI-driven algorithms enhance genomic data analysis, allowing researchers to detect mutations and gene variations with greater accuracy and speed. This has improved the selection process for patient cohorts, reducing trial delays and minimizing attrition rates. In manufacturing, AI models are being integrated into process automation systems, enabling real-time monitoring of cell culture conditions and ensuring consistent quality in large-scale production.

AI also plays a crucial role in predicting therapeutic responses and adverse effects, helping clinicians personalize treatment plans. Machine learning tools are increasingly being used to simulate complex biological pathways, supporting the development of safer and more effective therapies. The integration of digital twins in bioprocessing has allowed companies to test production variables virtually before implementation, lowering costs and reducing experimental errors. With continuous advancements in predictive analytics, AI is bridging the gap between laboratory research and clinical application, making cell and gene therapies more accessible and efficient for patients worldwide.

"In March 2025, researchers applied an AI-driven deep learning framework to optimize adeno-associated virus (AAV) vector design, achieving a 27% increase in transduction efficiency for gene therapies targeting neuromuscular disorders. This measurable outcome demonstrated AI’s ability to enhance therapeutic delivery systems in clinical-grade applications."

The Next-Generation Cell And Gene Therapy Market is shaped by a complex interplay of technological progress, regulatory support, and shifting healthcare priorities. Advancements in CRISPR gene editing, CAR-T cell platforms, and allogeneic therapies are enhancing scalability and reducing production times. Governments are implementing supportive frameworks to accelerate approvals, while strategic partnerships among pharmaceutical giants and biotech start-ups are intensifying innovation. At the same time, global healthcare systems are under pressure to integrate these advanced therapies despite high treatment costs and infrastructure challenges, creating both opportunities and risks for market participants.

Rapid progress in CRISPR-Cas9 and CAR-T cell technologies is a primary driver in the Next-Generation Cell And Gene Therapy Market. These innovations have significantly improved precision in genetic modification and boosted therapeutic outcomes in oncology and rare genetic disorders. For example, CRISPR tools now enable targeted edits in under 24 hours, improving research efficiency and reducing development bottlenecks. CAR-T therapies have shown remarkable remission rates in hematological cancers, expanding adoption across multiple treatment centers worldwide. The growing integration of these advanced platforms is pushing the boundaries of personalized and regenerative medicine.

The Next-Generation Cell And Gene Therapy Market faces substantial challenges due to elevated production expenses and the requirement for highly specialized facilities. Manufacturing costs per patient can exceed USD 300,000, restricting accessibility and limiting scalability for healthcare systems. Cold chain logistics, contamination risks, and stringent regulatory compliance further complicate distribution. Additionally, developing nations struggle with inadequate infrastructure to support advanced cell processing and storage, slowing global adoption. These constraints highlight the pressing need for cost-effective biomanufacturing and scalable supply chain solutions.

Personalized treatments and rare disease therapies present a major growth avenue in the Next-Generation Cell And Gene Therapy Market. Over 7,000 rare diseases have been identified globally, yet fewer than 10% have approved therapies. Recent breakthroughs in targeted delivery systems and next-generation vectors are enabling more tailored treatments, especially in neurology and metabolic disorders. With increasing regulatory incentives and orphan drug designations, biotech firms are investing heavily in rare disease pipelines. This opportunity is further reinforced by patient advocacy initiatives and rising demand for precision healthcare solutions.

A major challenge for the Next-Generation Cell And Gene Therapy Market is navigating stringent regulatory frameworks and lengthy approval processes. Despite accelerated pathways in certain regions, many therapies face delays due to complex safety evaluations, post-treatment monitoring requirements, and evolving ethical considerations. The need for long-term efficacy and safety data extends timelines, creating uncertainty for developers and investors. Additionally, inconsistencies in regulatory guidelines across countries complicate global commercialization strategies, hindering market harmonization.

Adoption of Allogeneic Cell Therapies

The shift from autologous to allogeneic therapies is transforming the Next-Generation Cell And Gene Therapy Market. Allogeneic platforms reduce treatment times from weeks to days, with several trials reporting positive efficacy in oncology and rare genetic diseases.

Integration of Digital Twins in Bioprocessing

Digital twin technology is gaining momentum, allowing companies to simulate production conditions virtually. This has cut process development timelines by nearly 30%, driving efficiency in large-scale biomanufacturing.

Rise of Non-Viral Delivery Systems

Non-viral vectors are emerging as safer and more scalable alternatives to viral systems. Nanoparticle and lipid-based carriers have shown enhanced delivery rates while reducing immune response risks in clinical applications.

Growth of Cross-Border Collaborations

International collaborations are accelerating innovation in the Next-Generation Cell And Gene Therapy Market. Joint ventures between biotech firms in the US, Europe, and Asia-Pacific are expediting access to specialized platforms and expanding trial diversity.

The Next-Generation Cell And Gene Therapy Market is segmented by type, application, and end-user, reflecting the diversity of therapeutic platforms and industrial adoption. Types include CAR-T therapies, CRISPR-based therapies, viral vector technologies, and non-viral delivery methods. Applications span oncology, rare genetic disorders, cardiovascular diseases, neurology, and others. End-users range from hospitals and specialty clinics to academic research centers and pharmaceutical manufacturers. This segmentation highlights the varied demand base and underscores the importance of innovation in driving adoption across multiple healthcare landscapes.

CAR-T therapies dominate the Next-Generation Cell And Gene Therapy Market due to their proven success in hematological cancers and increasing expansion into solid tumors. These therapies have achieved remission rates exceeding 70% in specific leukemia cases, making them highly sought-after. CRISPR-based therapies are the fastest-growing segment, fueled by their versatility in editing genetic material with precision, supporting applications in both inherited disorders and oncology. Viral vector technologies remain central to the market as delivery vehicles for many therapies, though challenges with immune response are driving demand for alternatives. Non-viral delivery methods, particularly lipid nanoparticles, are gaining traction due to scalability and reduced safety risks. Other emerging types, such as engineered stem cell therapies, contribute to the broader innovation landscape.

Oncology represents the leading application area in the Next-Generation Cell And Gene Therapy Market, driven by the success of CAR-T and gene-edited treatments in leukemia, lymphoma, and multiple myeloma. These therapies offer high remission rates and new hope for patients resistant to conventional treatment. Rare genetic disorders form the fastest-growing application, with rising investment in therapies for conditions such as spinal muscular atrophy and hemophilia. Cardiovascular diseases and neurology are emerging as significant areas of focus, supported by ongoing clinical trials exploring regenerative approaches. Other applications, including metabolic and ophthalmic disorders, are contributing to niche growth, highlighting the expanding therapeutic potential of next-generation platforms.

Hospitals and specialty clinics are the dominant end-users in the Next-Generation Cell And Gene Therapy Market, as they provide direct patient access and advanced treatment infrastructure. These institutions handle the majority of CAR-T and gene therapy administrations globally. Academic and research institutes represent the fastest-growing segment, benefiting from increased funding, advanced laboratory infrastructure, and active participation in early-stage clinical trials. Pharmaceutical and biotechnology companies play a vital role as enablers, focusing on large-scale production, regulatory approval, and commercialization. Collectively, these end-users form an interconnected ecosystem that supports innovation, delivery, and expansion of advanced therapies across regions.

North America accounted for the largest market share at 40% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 22% between 2025 and 2032.

North America leads thanks to its advanced manufacturing infrastructure, vast clinical trial network, and extensive R&D investments in innovation clusters. By contrast, Asia-Pacific is rapidly advancing with new therapy hubs, local CDMO expansions, and regulatory pathways supporting biopharmaceutical innovation. Western Europe remains a significant contributor, driven by precision medicine initiatives and regulatory harmonization. In emerging markets such as Latin America and the Middle East & Africa, expanding healthcare infrastructure and strategic international partnerships are enabling gradual adoption. These regional disparities highlight where capital, technology, and regulatory adaptability intersect to shape market growth globally.

Leading Edge Manufacturing and Innovation Ecosystem

North America held approximately 40% market share in 2024, underpinned by strong clinical infrastructure and biomanufacturing capacity. Key demand originates from oncology, rare genetic disorders, and regenerative medicine segments. Regulatory updates—such as streamlined FDA pathways for advanced therapies—and expanding government support for manufacturing scale-up have fortified the ecosystem. Technology trends include automated, modular bioprocessing platforms and closed-loop manufacturing systems enabling scalable, high-quality production. Collaboration between research institutions and industrial partners is accelerating innovation in vector design, automated cell expansion, and gene editing tools, reinforcing North America’s leadership in next-generation strategic therapy deployment.

Advancing Regulatory Alignment and Sustainable Innovation

Europe accounted for about 28% market share in 2024, with innovation hubs in Germany, France, and the UK leading adoption. The European Medicines Agency continues to refine frameworks supporting conditional approvals and tissue/gene therapy guidance. Sustainability agendas are promoting greener manufacturing processes, aligned with cell and gene therapy innovation. Emerging technologies—including real-world evidence platforms, AI-enhanced vector design, and regional production alliances—are reshaping the market. Collaborative networks between pharma and academic centers are fostering regional trial acceleration and distribution models to meet patient needs across national boundaries.

Rapid Expansion Driven by Innovation Hubs and Cost-Efficient Trials

Asia-Pacific ranked second in market volume in 2024, with China, Japan, and India leading consumption. Manufacturing and clinical trial infrastructure are expanding rapidly across emerging biotech hubs in Shanghai, Seoul, and Bangalore. These hubs benefit from government incentives, lower-capital CDMOs, and international licensing partnerships. Innovative platforms optimized for CRISPR-based gene editing, CAR-T cell therapies, and in-situ vector production are being deployed. Additionally, regional clinical trial efficiencies and growing oncology patient populations are driving accelerated adoption. Asia-Pacific’s technological modernization signifies its evolution from manufacturing base to science-driven innovation region in the next-generation therapy landscape.

Building Capacity Through Emerging Biotech Partnerships

South America accounted for approximately 6% market share in 2024, anchored by activity in Brazil and Argentina. Growth is supported by local biotech clusters, academic research centers, and expanding manufacturing pilot sites. Infrastructure improvements in cleanroom facilities and regulatory harmonization are encouraging strategic collaborations. Government policies providing tax breaks and public-private partnerships are facilitating capacity building. A growing focus on affordability and local access is also guiding market development, with interest in allogeneic and off-the-shelf therapies that facilitate scalable deployment.

Strategic Investments Fueling Healthcare Modernization

The Middle East & Africa held roughly 3% market share in 2024, with emerging activity in the UAE and South Africa. Regional development funds are supporting centers focused on oncology cell therapies and gene editing research. Governments are aligning regulatory pathways with international standards to attract global biotech players. Sophisticated manufacturing facilities are being introduced, some leveraging modular or automated cell therapy platforms. Strategic trade partnerships with global CDMOs are enabling technology transfer and workforce training, positioning the region for gradual market expansion.

United States – 32% market share

Leadership driven by cutting-edge manufacturing capacity, extensive clinical pipelines, and advanced research infrastructure.

China – 18% market share

Strong growth supported by expansive biotech investment, innovation clusters, and efficient clinical trial frameworks.

The Next-Generation Cell and Gene Therapy market is shaped by over 120 active global and regional players, including biotech leaders, CDMOs, and academic spinouts. Competition centers around capabilities in vector design, scalable bioprocessing, and CAR-T/autologous therapy platforms. Many firms are pursuing strategic alliances—ranging from manufacturing partnerships to co-development agreements—to accelerate pipeline expansion. Industry trends show acceleration in automation, AI-augmented manufacturing, and modular facility deployment. Players differentiate by end-to-end service offerings or specialty platforms, and by investing in regional production hubs to reduce time-to-clinic. The competitive environment is also influenced by emerging players focusing on allogeneic, off-the-shelf formats, compelling traditional incumbents to explore modularization, digital diagnostics, and next-gen payload strategies. This dynamic landscape places innovation, service scope, and agility at the core of competitive positioning.

Novartis AG

Gilead Sciences, Inc. (Kite)

Bristol-Myers Squibb

Adaptimmune Therapeutics

Cellares Corporation

Thermo Fisher Scientific

Lonza Group

Fujifilm Diosynth Biotechnologies

Catalent, Inc.

Vertex Pharmaceuticals

Next-generation cell and gene therapies are being revolutionized by converging technologies in manufacturing, delivery, and design. Automated, modular manufacturing systems—such as robotic “smart factories”—are enabling efficient production at scale, lowering labor costs and reducing variability. CRISPR-enhanced payload engineering is optimizing gene-editing precision, while AI-driven vector design algorithms accelerate capsid selection, minimizing off-target effects. Allogeneic platforms and off-the-shelf models are transforming autologous constraints, enabling scalable manufacturing and broader patient access.

Digital solutions, including analytics-enabled bioprocess control, real-time in-line monitoring, and cloud-integrated batch tracking systems, are enhancing quality assurance, compliance, and throughput. Delivery innovations—like novel viral and nonviral vehicles—are expanding therapeutic reach into hard-to-access tissues. In parallel, advanced cell processing technologies, including microfluidic expansion and closed-system bioreactors, are increasing yield and reducing contamination risk. Altogether, these technologies are collectively transforming the therapeutic landscape by improving scalability, safety, and affordability—key imperatives for decision-makers navigating the evolving next-generation cell and gene therapy domain.

In December 2023, the FDA approved Casgevy, the first CRISPR/Cas9-based gene therapy for sickle cell disease and beta-thalassemia, marking a landmark milestone for gene editing in clinical care.

In February 2024, Lifileucel (Amtagvi), the first tumor-derived T cell immunotherapy, received FDA approval for treating unresectable metastatic melanoma.

In September 2024, Cellares announced the opening of its first “smart factory” in New Jersey, capable of producing over 40,000 cell therapy batches annually via automated robotics.

In August 2024, Adaptimmune received FDA accelerated approval for Tecelra (afamitresgene autoleucel), the first TCR gene therapy targeting a solid tumor (synovial sarcoma).

The report presents a comprehensive framework covering product types—such as CAR-T, TCR therapies, viral vector gene editing, allogeneic/off-the-shelf models—and their tailored manufacturing processes. It evaluates applications across oncology, rare genetic disorders, autoimmune and regenerative medicine. End-user segments include pharma innovators, biotech firms, contract manufacturing organizations, and academic translational centers.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa, addressing regional manufacturing capacity, clinical trial density, and regulatory landscape nuances. It examines trends in automation, AI-enabled payload design, modular biomanufacturing, and digital quality systems. Strategic dimensions include partnerships, facility expansions, and regulatory approvals.

Given the fast-evolving nature of the field, the report also highlights future-oriented segments such as next-gen allogeneic therapies, CRISPR-based gene editing, and AI-integrated production platforms—serving as a strategic compass for decision-makers focusing on investment, product development, and infrastructure scaling in next-generation cell and gene therapy.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 19894.4 Million |

|

Market Revenue in 2032 |

USD 82179.9 Million |

|

CAGR (2025 - 2032) |

19.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Novartis AG, Gilead Sciences, Inc. (Kite), Bristol-Myers Squibb, Adaptimmune Therapeutics, Cellares Corporation, Thermo Fisher Scientific, Lonza Group, Fujifilm Diosynth Biotechnologies, Catalent, Inc., Vertex Pharmaceuticals |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |