Reports

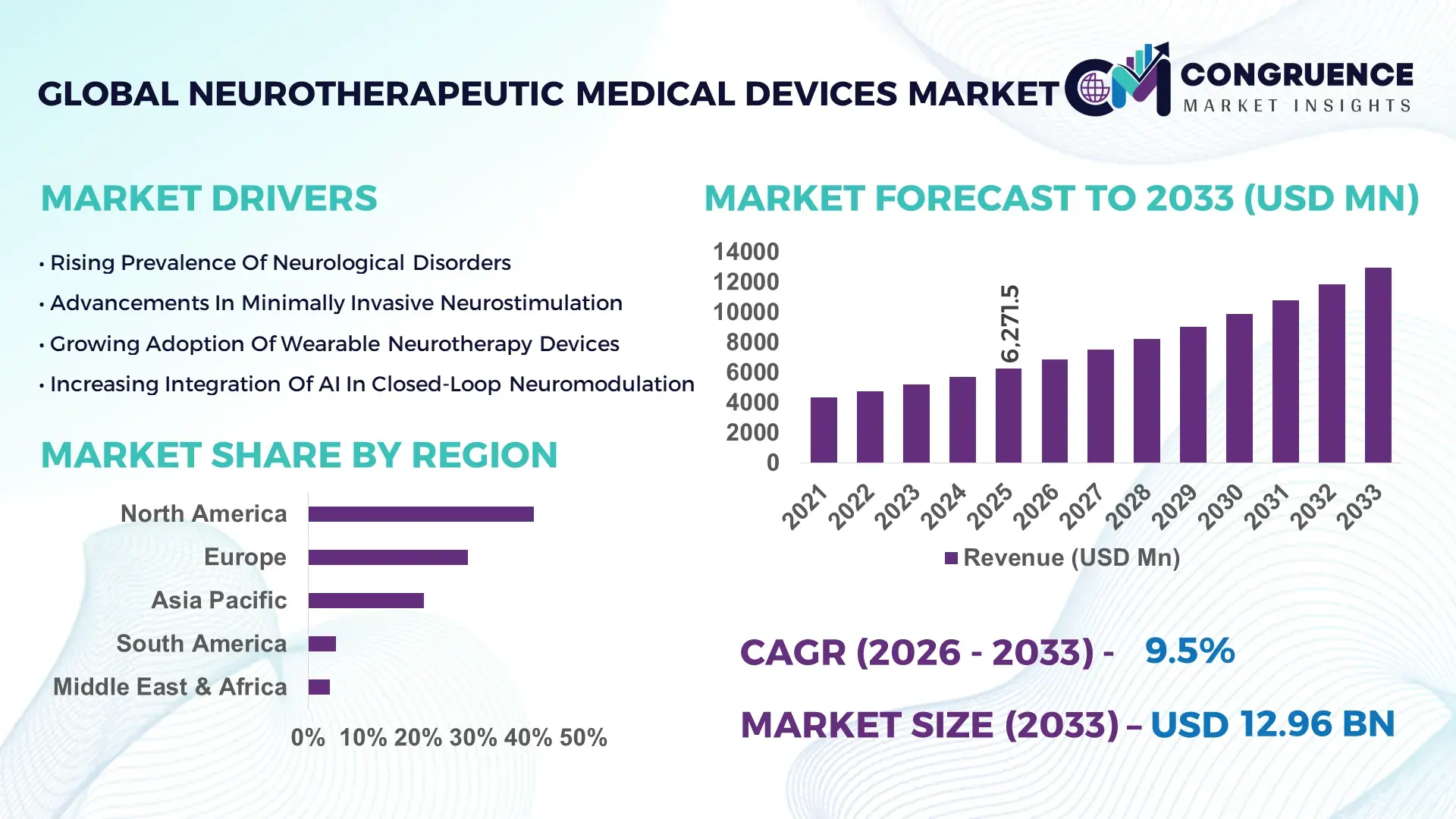

The Global Neurotherapeutic Medical Devices Market was valued at USD 6,271.5 Million in 2025 and is anticipated to reach a value of USD 12,962.4 Million by 2033 expanding at a CAGR of 9.5% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by rising neurological disorder prevalence and rapid innovation in minimally invasive neuromodulation technologies.

The United States leads the Neurotherapeutic Medical Devices market with advanced manufacturing capacity exceeding 1.8 million implantable neurostimulation units annually. Over 900 specialized neurology centers perform device-based therapies such as deep brain stimulation (DBS), vagus nerve stimulation (VNS), and spinal cord stimulation (SCS). Federal research funding for neuroscience innovation surpassed USD 3 billion in 2025, accelerating AI-integrated neurostimulation platforms and next-generation closed-loop systems. More than 65% of large U.S. hospitals have adopted at least one implantable neurotherapeutic solution, while over 40% of new product launches globally originate from U.S.-based manufacturers focused on precision neuro-modulation and wearable neurotherapy systems.

Market Size & Growth: USD 6,271.5 Million in 2025, projected to reach USD 12,962.4 Million by 2033 at 9.5% CAGR, driven by increasing Parkinson’s, epilepsy, and chronic pain cases.

Top Growth Drivers: 32% rise in neurodegenerative diagnoses, 28% increase in minimally invasive procedures, 24% improvement in therapy efficacy through closed-loop stimulation.

Short-Term Forecast: By 2028, AI-enabled neuromodulation is expected to improve patient response rates by 18%.

Emerging Technologies: Closed-loop deep brain stimulation, AI-powered signal mapping, and non-invasive transcranial magnetic stimulation platforms.

Regional Leaders: North America projected at USD 5.4 Billion by 2033; Europe at USD 3.6 Billion; Asia-Pacific at USD 2.9 Billion with strong hospital infrastructure expansion.

Consumer/End-User Trends: Over 52% of tertiary hospitals prioritize implantable neurostimulators; outpatient neurology centers adoption increased 21% in 2025.

Pilot Example: In 2025, a major neurology institute achieved 22% reduction in seizure frequency using adaptive DBS.

Competitive Landscape: Market leader holds approximately 26% share, followed by key multinational medical device manufacturers.

Regulatory & ESG Impact: Enhanced device safety frameworks and 15% reduction in electronic component waste through sustainable manufacturing.

Investment Patterns: Over USD 1.2 Billion invested in neurotechnology startups during 2025.

Innovation Outlook: Integration of AI diagnostics with implantable devices and wireless charging systems shaping future growth.

Cardiology, pain management, and movement disorder treatments collectively account for over 68% of Neurotherapeutic Medical Devices utilization. Implantable stimulators represent nearly 55% of procedures, while non-invasive therapies are expanding rapidly. Regulatory approvals for closed-loop stimulation systems increased 19% in 2025. Asia-Pacific consumption is rising due to aging populations, while Europe emphasizes value-based care models supporting cost-efficient neuromodulation therapies.

The Neurotherapeutic Medical Devices market plays a critical strategic role in modern healthcare systems by addressing the growing burden of neurological disorders affecting more than 3 billion people globally. Healthcare providers increasingly prioritize device-based interventions due to improved clinical outcomes and reduced pharmaceutical dependency. Closed-loop deep brain stimulation delivers 25% improvement compared to conventional open-loop stimulation in symptom control for Parkinson’s patients, highlighting measurable therapeutic advantages.

North America dominates in procedure volume, while Europe leads in adoption with over 58% of large public hospitals implementing advanced neuromodulation platforms. By 2028, AI-assisted neuro-signal mapping is expected to reduce programming time by 20%, improving hospital efficiency and patient throughput. Firms are committing to ESG improvements such as 18% reduction in device-related electronic waste by 2030 through recyclable components and energy-efficient manufacturing.

In 2025, a U.S.-based neuromodulation company achieved a 19% improvement in chronic pain management outcomes through AI-guided stimulation calibration. Strategic pathways include expansion into wearable neurotherapy devices, integration with digital health platforms, and broader outpatient procedure accessibility. As healthcare systems transition toward value-based treatment models, the Neurotherapeutic Medical Devices market is positioned as a cornerstone of precision medicine, resilience, regulatory compliance, and sustainable long-term growth.

The Neurotherapeutic Medical Devices market dynamics are shaped by technological advancements, rising neurological disease incidence, regulatory modernization, and expanding healthcare infrastructure. Increasing life expectancy contributes to higher prevalence of Parkinson’s disease, epilepsy, chronic pain disorders, and depression requiring device-based interventions. Implantable neuromodulation procedures have grown by nearly 17% over the past two years, reflecting clinical preference for minimally invasive solutions.

Healthcare systems emphasize cost-effective therapies that reduce hospitalization rates. Advanced devices featuring real-time neural feedback and wireless programmability enhance therapeutic precision. Regulatory pathways have accelerated approvals for adaptive stimulation technologies, reducing commercialization timelines by approximately 15%. Emerging markets are investing heavily in tertiary neurology care centers, supporting device penetration growth. However, high upfront costs and surgical complexity remain important operational considerations influencing adoption rates across developing regions.

Neurological disorders affect nearly 15% of the global population, with Parkinson’s disease cases projected to surpass 12 million by 2030. Chronic pain impacts over 20% of adults worldwide, increasing demand for spinal cord stimulation systems. Implantable neurostimulation therapies demonstrate up to 50% reduction in symptom severity for selected patient groups, improving quality-of-life metrics.

Hospitals report a 23% rise in neuromodulation procedures since 2023, supported by improved reimbursement structures. Growing awareness of non-pharmacological treatment alternatives further supports device adoption. Increasing elderly population segments, particularly those aged above 65 years, represent more than 40% of neurotherapeutic device recipients, strengthening consistent procedural growth.

Advanced Neurotherapeutic Medical Devices involve implantation procedures costing between USD 20,000 and USD 40,000 per patient, creating financial barriers in emerging markets. Limited reimbursement coverage in certain regions reduces accessibility for lower-income populations. Surgical risks and device replacement cycles every 5–10 years increase long-term treatment expenses.

Approximately 27% of developing-country hospitals lack specialized neurosurgical facilities required for implantation. Training requirements for neurosurgeons and neurologists further restrict expansion. Device-related complications, although rare at under 5%, can influence clinical hesitancy and insurance scrutiny, moderating broader market penetration.

AI-enabled Neurotherapeutic Medical Devices offer real-time neural signal adaptation, improving treatment accuracy by 20% compared to manual programming. Closed-loop systems adjust stimulation parameters dynamically, enhancing seizure control and chronic pain management outcomes. Tele-neurology integration enables remote device calibration, reducing follow-up visits by 18%.

Emerging wearable neurotherapy solutions expand outpatient treatment possibilities, potentially lowering procedural costs by 15%. Asia-Pacific investments in advanced neurology centers increased 24% in 2025, creating untapped growth potential. Expanding indications into depression, Alzheimer’s disease, and post-stroke rehabilitation further diversify clinical applications.

Stringent regulatory frameworks require extensive clinical validation, extending approval timelines by 12–18 months. Complex device architectures integrating AI algorithms demand rigorous cybersecurity protocols. Nearly 22% of device manufacturers report extended product development cycles due to compliance requirements.

Interoperability with hospital digital systems presents additional integration challenges. Variability in global regulatory standards increases costs for multinational manufacturers. Furthermore, supply chain disruptions for specialized electronic components can delay production schedules, impacting delivery timelines across major healthcare markets.

• Expansion of Closed-Loop Neurostimulation: Closed-loop systems now account for approximately 34% of new deep brain stimulation implants, delivering 25% improved symptom stability compared to earlier-generation models. Adaptive stimulation algorithms reduce adverse event rates by nearly 12%, enhancing long-term patient outcomes.

• Growth in Minimally Invasive Implant Techniques: Minimally invasive neurosurgical approaches have reduced average hospital stays by 18% and lowered post-operative complication rates by 10%. Over 60% of tertiary hospitals have adopted image-guided robotic assistance systems for precision implantation.

• Surge in Non-Invasive Neuromodulation Devices: Transcranial magnetic stimulation adoption increased by 21% in 2025, particularly for treatment-resistant depression. Outpatient therapy sessions expanded by 16%, reflecting broader clinical acceptance and improved reimbursement coverage.

• Integration with Digital Health Ecosystems: Approximately 48% of newly launched Neurotherapeutic Medical Devices feature wireless connectivity for remote monitoring. AI-driven analytics platforms enhance therapy personalization, improving response rates by 17% and reducing follow-up adjustments by 14%.

The Neurotherapeutic Medical Devices market is segmented by type, application, and end-user to reflect diverse clinical use cases. Implantable devices dominate advanced neurological interventions, while non-invasive systems address outpatient therapy needs. Applications span Parkinson’s disease, epilepsy, chronic pain, depression, and movement disorders.

Tertiary hospitals and specialized neurology centers represent the primary end-users, accounting for more than half of procedural volume. Ambulatory surgical centers are expanding adoption due to reduced inpatient dependency. Technological innovation and increasing neurological disease burden drive segmentation evolution, enabling targeted treatment strategies and optimized healthcare resource allocation.

Implantable neurostimulation devices hold approximately 58% of the Neurotherapeutic Medical Devices market due to their effectiveness in chronic neurological conditions. Deep brain stimulators account for 28% adoption, while spinal cord stimulators represent 20%. However, non-invasive neurostimulation systems are the fastest-growing segment, expanding at 12.8% CAGR, driven by outpatient accessibility and reduced surgical risks.

Wearable neurotherapy devices and transcranial magnetic stimulation systems collectively account for 24% of market volume. Hybrid AI-enabled closed-loop devices represent nearly 18% and continue gaining clinical acceptance.

In 2025, a leading neuromodulation manufacturer reported successful deployment of adaptive deep brain stimulation in over 5,000 Parkinson’s patients, demonstrating significant symptom reduction across multi-center trials.

Parkinson’s disease remains the leading application, accounting for approximately 31% of Neurotherapeutic Medical Devices usage. Chronic pain follows at 27%, while epilepsy treatments represent 18%. Depression and movement disorders collectively account for 15%. However, post-stroke rehabilitation is expanding fastest at 11.6% CAGR due to increased awareness and technological refinement.

In 2025, more than 42% of U.S. hospitals reported implementing advanced neurostimulation platforms for chronic pain therapy. Over 38% of tertiary care centers globally piloted AI-integrated neuromodulation systems for personalized treatment adjustments.

In 2025, a major neurology research institute deployed AI-powered neurostimulation therapy across 150 patients, achieving measurable seizure reduction improvements in clinical settings.

Hospitals dominate the Neurotherapeutic Medical Devices market with approximately 54% share, supported by specialized neurosurgical capabilities. Neurology specialty clinics account for 26%, while ambulatory surgical centers represent 14%. However, outpatient rehabilitation centers are the fastest-growing segment at 13.4% CAGR due to demand for non-invasive therapies.

Nearly 47% of tertiary hospitals globally invested in AI-enabled neurotherapy devices in 2025. Around 35% of specialty clinics expanded device programming capabilities to enhance patient-specific therapy optimization.

In 2025, a leading global healthcare network implemented AI-guided neurostimulation systems across 20 facilities, improving treatment efficiency and reducing patient adjustment visits by 18%.

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.8% between 2026 and 2033.

North America generated procedure volumes exceeding 320,000 neuromodulation implantations in 2025, supported by over 1,200 advanced neurology centers and strong reimbursement coverage for deep brain stimulation and spinal cord stimulation therapies. Europe represented approximately 29% of the Neurotherapeutic Medical Devices market, driven by more than 850 specialized neuroscience hospitals across Germany, the UK, and France.

Asia-Pacific accounted for nearly 21% of total device installations, with China and Japan collectively performing over 110,000 neurostimulation procedures annually. Government-backed investments in tertiary hospitals increased by 18% in 2025 across key Asian economies. South America contributed 5% share, primarily from Brazil and Argentina, where neurological treatment access expanded by 14% through public-private partnerships. The Middle East & Africa held 4%, supported by rising demand in the UAE and South Africa, where advanced neurosurgical units increased by 12% year-over-year.

How Is Advanced Clinical Infrastructure Strengthening Regional Leadership in Neurotherapeutic Medical Devices?

North America holds approximately 41% share of the Neurotherapeutic Medical Devices market, supported by high healthcare expenditure exceeding USD 12,000 per capita annually in leading economies. Neurology, pain management, and movement disorder clinics are primary demand drivers, with chronic pain affecting nearly 20% of adults. Over 65% of tertiary hospitals utilize implantable neurostimulation systems.

Regulatory modernization has accelerated device approvals by nearly 15% in recent years, enabling faster commercialization of adaptive closed-loop systems. Digital health integration allows remote device programming in over 48% of newly implanted units. A leading regional manufacturer expanded its AI-enabled spinal cord stimulation platform in 2025, enhancing signal precision and reducing programming sessions by 17%. Consumer behavior reflects strong preference for minimally invasive, outpatient neuromodulation therapies, particularly within advanced healthcare networks.

Why Is Regulatory Innovation Driving Adoption of Advanced Neurotherapeutic Medical Devices?

Europe represents around 29% of the Neurotherapeutic Medical Devices market, with Germany, the UK, and France accounting for over 60% of regional installations. More than 800 neurology centers provide device-based therapies, and over 55% of university hospitals employ deep brain stimulation programs. Sustainability-focused regulatory bodies emphasize device safety and traceability, increasing compliance standards by 20% in recent years.

Adoption of AI-guided neuro-mapping technologies has increased 22% across Western Europe. A prominent European manufacturer introduced next-generation rechargeable implantable stimulators in 2025, extending battery life by 25% and reducing replacement surgeries. Regional healthcare systems prioritize cost-effective, evidence-based neuromodulation therapies, reflecting patient preference for long-term symptom stability and transparent clinical validation.

What Is Accelerating Rapid Clinical Expansion Across Emerging Neuroscience Hubs?

Asia-Pacific ranks third in total market volume, contributing approximately 21% of global Neurotherapeutic Medical Devices installations. China, Japan, and India collectively account for over 70% of regional demand. Neurological disorder prevalence in populations aged above 60 years has risen by 19%, stimulating hospital investment in advanced neurosurgical units.

More than 500 tertiary hospitals across China have established neuromodulation departments. Japan remains a leader in precision robotics-assisted implantation, while India recorded a 23% rise in spinal cord stimulation procedures in 2025. Regional innovation hubs focus on cost-efficient device manufacturing and AI-based neural analytics. Patients increasingly favor wearable and non-invasive neurotherapy devices, with outpatient adoption increasing by 16% annually.

How Are Public-Private Healthcare Investments Supporting Device Adoption Growth?

South America accounts for approximately 5% of the Neurotherapeutic Medical Devices market, with Brazil representing nearly 60% of regional procedure volume. Argentina and Chile are expanding neurology center capacity, increasing implantation rates by 14% in 2025. Infrastructure modernization programs support advanced neurosurgical capabilities in over 120 hospitals.

Government-backed reimbursement reforms improved patient access to implantable neurostimulators by 11%. A regional medical device distributor introduced AI-enabled programming software, reducing therapy calibration time by 15%. Consumer behavior trends indicate rising awareness of chronic pain management alternatives and increased acceptance of minimally invasive neuromodulation treatments.

How Is Healthcare Modernization Expanding Advanced Neuromodulation Therapies?

The Middle East & Africa region contributes nearly 4% of the Neurotherapeutic Medical Devices market. The UAE and Saudi Arabia collectively account for over 55% of regional installations, supported by investment exceeding USD 2 billion in specialized neuroscience facilities over the past three years. South Africa remains a leading African adopter, with implantation procedures rising by 13% in 2025.

Technological modernization initiatives include robotic-assisted neurosurgery and digital patient monitoring platforms adopted in 40% of major urban hospitals. Trade partnerships facilitate advanced device imports, improving availability. Patient preference trends show increasing demand for advanced neurological care and long-term chronic pain management solutions.

United States – 38% share: Dominates the Neurotherapeutic Medical Devices market due to high procedural volumes, advanced manufacturing capacity, and robust reimbursement frameworks.

Germany – 12% share: Strong clinical infrastructure and early adoption of AI-integrated neuromodulation technologies support sustained Neurotherapeutic Medical Devices demand.

The Neurotherapeutic Medical Devices market is moderately consolidated, with the top five companies collectively accounting for approximately 63% of global share. Over 45 active manufacturers compete across implantable and non-invasive neuromodulation segments. Market leaders emphasize product differentiation through AI-enabled adaptive stimulation, rechargeable battery systems, and minimally invasive implantation tools.

Strategic initiatives include 18% increase in R&D expenditure across leading players during 2025, multiple cross-border partnerships for distribution expansion, and at least 6 notable acquisitions in neurotechnology startups within two years. Closed-loop stimulation platforms represent nearly 34% of new product launches. Competitive positioning focuses on expanding indications for depression, Alzheimer’s disease, and post-stroke rehabilitation. Barriers to entry remain high due to regulatory requirements, clinical validation complexity, and capital-intensive manufacturing processes.

LivaNova PLC

Nevro Corp.

NeuroPace, Inc.

Synapse Biomedical Inc.

Soterix Medical Inc.

Aleva Neurotherapeutics SA

Cochlear Limited

Natus Medical Incorporated

B. Braun Melsungen AG

Integra LifeSciences Holdings Corporation

Zynex, Inc.

Technological innovation within the Neurotherapeutic Medical Devices market centers on precision neuromodulation, artificial intelligence integration, and minimally invasive implantation systems. Closed-loop stimulation platforms now account for nearly 34% of advanced implants, enabling real-time neural signal monitoring and adaptive therapy adjustment. AI-based neural mapping reduces device calibration time by up to 20%, enhancing clinical efficiency.

Rechargeable battery technology has extended implant lifespan by 25%, decreasing replacement surgeries. Wireless programming capabilities are integrated into over 48% of newly launched devices, supporting remote patient monitoring. Robotic-assisted implantation systems improve electrode placement accuracy by 15%, minimizing post-operative complications.

Non-invasive technologies such as transcranial magnetic stimulation have expanded outpatient usage by 21% in 2025. Integration with digital health ecosystems enables cloud-based data analytics and predictive symptom modeling. Cybersecurity enhancements, including encrypted communication protocols, protect patient data in over 90% of connected devices. Emerging research focuses on bioelectronic medicine, targeting inflammatory and metabolic disorders through neural pathway modulation, expanding the therapeutic scope of advanced neurotherapeutic solutions.

• In January 2025, Medtronic announced expanded global rollout of its Percept™ RC deep brain stimulation system featuring BrainSense™ technology, enabling chronic brain sensing and personalized therapy adjustments for Parkinson’s patients. Source: www.medtronic.com

• In April 2025, Boston Scientific reported positive clinical data for its WaveWriter Alpha™ spinal cord stimulation system, demonstrating improved chronic pain management outcomes and enhanced patient programming efficiency. Source: www.bostonscientific.com

• In March 2024, Abbott received regulatory approval for expanded indications of its Infinity™ DBS system, supporting adaptive stimulation therapy with directional leads for movement disorders. Source: www.abbott.com

• In September 2024, Nevro Corp. launched next-generation high-frequency spinal cord stimulation software upgrades improving therapy customization and remote programming capabilities across multiple clinical centers. Source: www.nevro.com

The Neurotherapeutic Medical Devices Market Report provides comprehensive coverage across device types, including implantable neurostimulators, deep brain stimulation systems, spinal cord stimulators, vagus nerve stimulators, and non-invasive neuromodulation technologies. The analysis spans key applications such as Parkinson’s disease, epilepsy, chronic pain, depression, movement disorders, and post-stroke rehabilitation, collectively representing over 85% of therapeutic demand.

Geographically, the report evaluates North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, covering more than 25 major countries with detailed assessment of procedure volumes, hospital adoption rates, and regulatory frameworks. Over 45 active manufacturers and 60+ product variants are evaluated based on technological sophistication, battery longevity, AI integration capabilities, and digital connectivity features.

The report further examines end-user segments including hospitals, specialty neurology clinics, ambulatory surgical centers, and rehabilitation facilities. Technology insights cover robotic-assisted implantation, closed-loop adaptive stimulation, wireless programming systems, and cybersecurity integration. Strategic factors such as reimbursement trends, sustainability initiatives, manufacturing expansion, and cross-border partnerships are analyzed to provide decision-makers with actionable intelligence for investment, expansion, and competitive positioning within the Neurotherapeutic Medical Devices market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 6,271.5 Million |

|

Market Revenue in 2033 |

USD 12,962.4 Million |

|

CAGR (2026 - 2033) |

9.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Medtronic plc, Boston Scientific Corporation, Abbott Laboratories, LivaNova PLC, Nevro Corp., NeuroPace, Inc., Synapse Biomedical Inc., Soterix Medical Inc., Aleva Neurotherapeutics SA, Cochlear Limited, Natus Medical Incorporated, B. Braun Melsungen AG, Integra LifeSciences Holdings Corporation, Zynex, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |