Reports

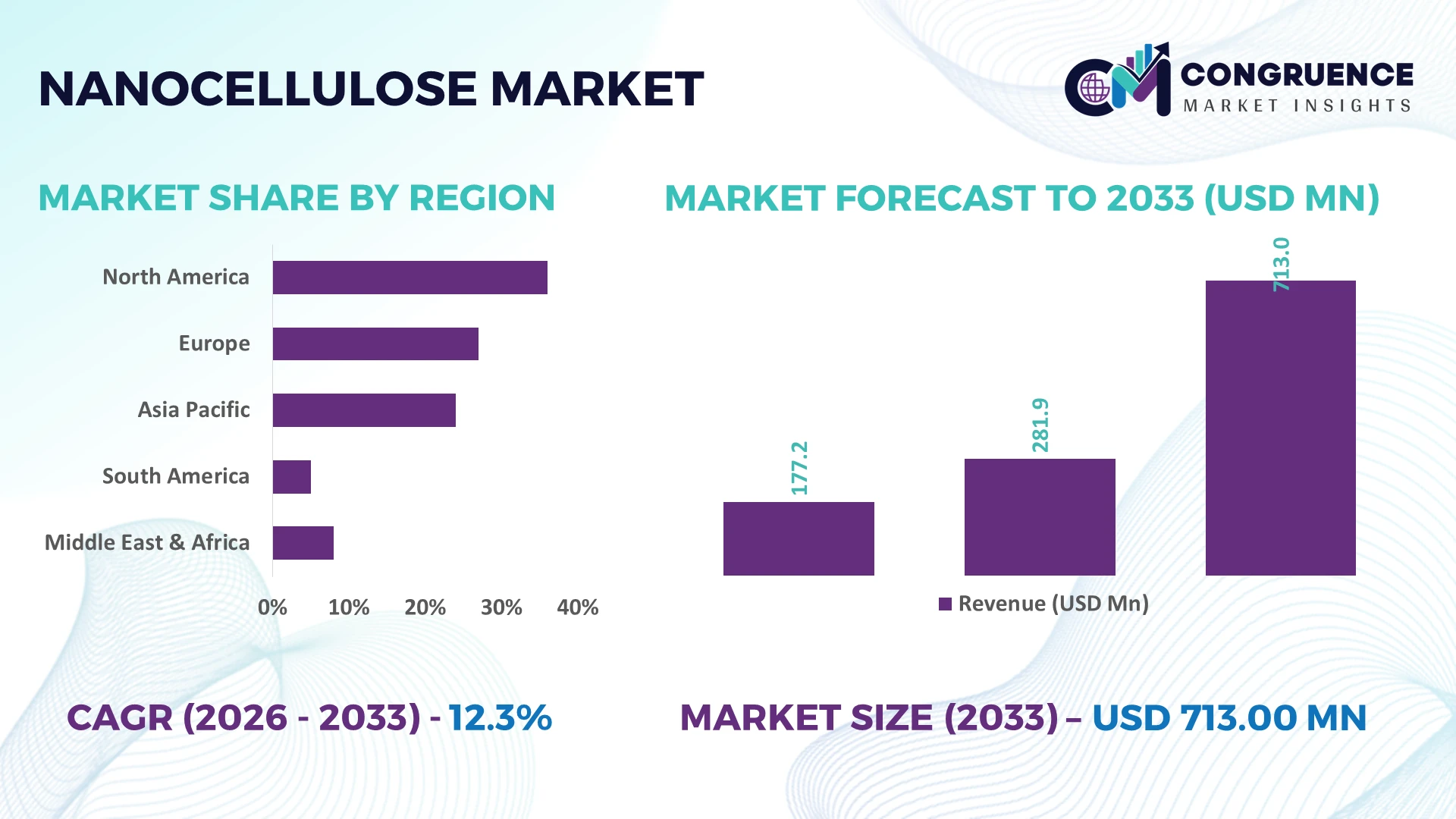

The Global Nanocellulose Market was valued at USD 281.87 Million in 2025 and is anticipated to reach a value of USD 713 Million by 2033 expanding at a CAGR of 12.3% between 2026 and 2033. Growth is primarily driven by accelerated commercialization of bio-based packaging materials, lightweight automotive composites, high-performance biomedical applications, and sustainable barrier coatings replacing petroleum-derived materials across industrial value chains.

Japan remains the dominant country, accounting for approximately 28% of global nanocellulose production capacity, supported by more than 35 commercial-scale research and manufacturing initiatives across packaging, electronics, and specialty chemicals. Compared with Canada, Japan demonstrates broader industrial adoption through advanced fiber processing technologies, while regional supply-chain diversification following Indo-Pacific manufacturing realignment has strengthened production resilience and export competitiveness.

Strategic investments in scalable manufacturing and application-specific product development remain essential for companies seeking long-term competitive positioning in the global nanocellulose market.

Market Size & Growth: USD 281.87 Million in 2025, reaching USD 713 Million by 2033 at 12.3% CAGR, supported by expanding bio-based materials and advanced packaging adoption.

Top Growth Drivers: Sustainable packaging demand (+34%), lightweight composite usage (+27%), and biomedical material adoption (+22%) accelerate global commercialization.

Short-Term Forecast: By 2028, production efficiency improves by 18% while manufacturing waste declines by approximately 15% through process optimization.

Emerging Technologies: AI-enabled process monitoring, automated fibrillation systems, and advanced surface functionalization improve consistency, scalability, and product performance.

Regional Leaders: Asia-Pacific exceeds USD 280 Million, Europe surpasses USD 190 Million, and North America approaches USD 165 Million through industrial decarbonization and advanced manufacturing expansion.

Consumer/End-User Trends: More than 46% of sustainable packaging developers integrate renewable cellulose-based materials into next-generation product portfolios.

Pilot/Case Example: 2025 industrial coating demonstration improved oxygen barrier performance by 30%, supporting commercial packaging applications.

Competitive Landscape: Leading manufacturers collectively control approximately 42% market share, with key participants focusing on capacity expansion, specialty grades, and strategic partnerships.

Regulatory & ESG Impact: Sustainable material regulations reduce fossil-based material dependence by nearly 20%, strengthening commercial adoption across regulated industries.

Investment & Funding: More than USD 900 Million supports manufacturing expansion, strategic partnerships, and advanced bioeconomy infrastructure amid global supply-chain diversification.

Innovation & Future Outlook: High-performance nanocellulose composites, recyclable functional films, and multifunctional biomaterials strengthen long-term industrial competitiveness and premium application development.

Nanocellulose Market expansion is increasingly supported by sustainable packaging, specialty coatings, biomedical materials, flexible electronics, and advanced composite manufacturing. Surface-modified nanocellulose and high-strength barrier films continue to improve commercial performance, while over 40% of new product development targets multifunctional applications. Evolving environmental regulations and regional manufacturing localization further reinforce operational resilience, setting the foundation for the strategic market discussion that follows.

Nanocellulose is becoming a strategic material for manufacturers seeking to reduce dependence on fossil-derived inputs while improving product performance across packaging, automotive, healthcare, and electronics. Supply-chain restructuring after recent global raw-material disruptions has accelerated investment in localized bio-based material production, while stricter environmental regulations continue to encourage substitution of conventional plastics. Companies are increasingly integrating nanocellulose into premium product portfolios to strengthen sustainability credentials without compromising mechanical performance or processing efficiency.

Compared with conventional petroleum-based barrier materials, nanocellulose coatings deliver up to 35% higher oxygen barrier efficiency while reducing material weight by nearly 20% in selected packaging applications. Japan leads commercialization through established industrial-scale manufacturing, whereas Finland maintains a stronger innovation pipeline supported by advanced forestry technology and pilot-scale development. Over the next two to three years, commercial production capacity utilization is expected to exceed 80% as process optimization and equipment standardization improve manufacturing consistency.

A practical example is the deployment of nanocellulose-enhanced paper packaging that extends product shelf life while reducing multilayer plastic dependence. Producers are expanding strategic partnerships with pulp manufacturers, specialty chemical suppliers, and packaging converters to accelerate commercialization. Companies that secure scalable production, application-specific formulations, and integrated value chains will strengthen competitive positioning and establish durable operational advantages across high-value industrial markets.

Growing adoption of renewable advanced materials is reshaping industrial procurement strategies across packaging, automotive, and specialty chemicals. Nearly 46% of sustainable packaging innovation programs now evaluate cellulose-based alternatives, while lightweight composite applications improve component weight by approximately 18% without compromising strength. Japan continues expanding advanced fiber processing infrastructure, supported by national bioeconomy initiatives encouraging renewable material deployment. This structural transition increases demand for functional nanocellulose grades with enhanced barrier and reinforcement properties. In response, manufacturers are expanding pilot facilities, investing in surface-modification technologies, and forming partnerships with packaging and chemical companies to accelerate commercialization. A notable strategic advantage lies in integrating nanocellulose into existing pulp processing operations, reducing production complexity while strengthening long-term manufacturing economics.

Commercial expansion remains constrained by energy-intensive fibrillation processes, specialized equipment requirements, and inconsistent production economics. Manufacturing costs remain approximately 30% higher than many conventional filler materials, while processing energy consumption can account for over 25% of total operating expenditure. Finland and Canada continue investing in industrial-scale production, yet global capacity remains concentrated within relatively few facilities, creating supply limitations for downstream manufacturers. These constraints affect pricing stability, profitability, and broader industrial adoption. Companies increasingly reduce operational risk through long-term pulp supply agreements, localized production investments, and hybrid material formulations that optimize performance while lowering overall nanocellulose consumption per application, improving commercial viability.

High-value functional applications are creating opportunities beyond traditional packaging markets. Demand for nanocellulose in flexible electronics, biomedical scaffolds, and energy storage components is expanding as product developers prioritize lightweight, renewable materials with enhanced mechanical performance. Advanced surface functionalization improves conductivity or compatibility by nearly 25% in specialized applications, while automated production technologies reduce processing time by approximately 20%. Sweden and South Korea continue strengthening innovation ecosystems through collaborative research and industrial demonstration programs. Companies are expanding R&D partnerships with electronics manufacturers, healthcare innovators, and specialty material developers to establish differentiated product portfolios. An emerging strategic opportunity lies in customized nanocellulose formulations tailored for sector-specific performance rather than standardized commodity production.

Long-term competitiveness depends on achieving uniform product quality across high-volume manufacturing while maintaining cost efficiency. Batch-to-batch performance variation can exceed 15% when feedstock quality differs, and industrial customers increasingly require standardized specifications exceeding 95% consistency. Integration into existing coating, composite, and polymer production lines also requires process redesign and workforce specialization. Germany and the United States continue investing in automated quality-control systems and advanced characterization technologies to improve manufacturing reliability. Companies must strengthen digital process monitoring, expand technical partnerships with equipment suppliers, and invest in production standardization to ensure consistent performance. Successfully solving manufacturing scalability will determine leadership in premium industrial applications rather than laboratory-scale innovation alone.

Advanced Surface Engineering Expands: Functional surface modification is accelerating commercial adoption by improving moisture resistance, conductivity, and barrier performance. Functionalized grades demonstrate nearly 30% higher coating efficiency and around 18% lower material usage in specialty applications. Japanese manufacturers are integrating continuous processing lines following stricter sustainability requirements, while chemical companies are expanding technology partnerships to deliver application-specific nanocellulose formulations with faster industrial qualification and lower production variability.

Continuous Manufacturing Gains Momentum: Producers are replacing batch processing with continuous fibrillation systems, reducing processing time by approximately 22% and improving production consistency by nearly 17%. Rising labor costs and pressure to secure domestic supply chains are encouraging automation across Nordic manufacturing facilities. Companies are restructuring production workflows, integrating digital process monitoring, and expanding industrial-scale capacity to achieve lower operating costs and more predictable commercial supply.

Circular Packaging Integration Accelerates: Packaging manufacturers increasingly combine nanocellulose with recyclable fiber substrates to eliminate multilayer plastic structures. Material recovery efficiency improves by roughly 25%, while lightweight packaging formats reduce overall material consumption by nearly 15%. Regulatory pressure on single-use plastics is driving converters in Germany and Japan to scale commercial deployment, supported by long-term partnerships between pulp producers, packaging companies, and specialty coating developers that shorten product commercialization cycles.

Cross-Industry Product Customization Increases: Manufacturers are shifting from standardized material grades toward sector-specific nanocellulose solutions for electronics, healthcare, and advanced composites. Customized formulations improve application compatibility by approximately 20% while reducing downstream processing adjustments by almost 14%. A notable trend is the integration of customer co-development programs, allowing suppliers to align product specifications with manufacturing workflows, strengthening long-term contracts and reducing qualification timelines for industrial buyers.

Cellulose Nanofibers represent the leading segment due to established manufacturing scalability, strong mechanical reinforcement, and compatibility with packaging, coatings, and composite production. More than 38% of industrial deployments utilize Cellulose Nanofibers because they integrate efficiently into existing pulp processing infrastructure while lowering material intensity. Microfibrillated Cellulose remains widely adopted for paper enhancement and rheology control, whereas Nanofibrillated Cellulose continues expanding in high-performance barrier applications. Companies are increasing production capacity, developing functional surface treatments, and strengthening strategic collaborations with packaging manufacturers to improve commercial differentiation.

Bacterial Nanocellulose is the fastest-growing type, supported by rising demand for biomedical materials and premium wound-care products requiring exceptional purity and biocompatibility. Cellulose Nanocrystals continue gaining traction in lightweight composites and specialty polymers, improving reinforcement efficiency by nearly 24%. Investment priorities increasingly favor high-value specialty grades over commodity production, encouraging manufacturers to diversify portfolios and establish application-focused innovation pipelines.

Paper & Packaging remains the dominant application because nanocellulose strengthens fiber structures, improves oxygen barrier performance, and supports recyclable packaging solutions without extensive process redesign. Approximately 45% of commercial demand originates from packaging applications, while advanced coating technologies reduce material consumption by nearly 16%. Composites continue serving automotive and industrial manufacturing through lightweight reinforcement, whereas Coatings expand into high-performance protective surfaces. Producers are investing in automated coating systems and collaborative development programs with packaging converters to improve manufacturing efficiency and shorten commercialization cycles.

Biomedical applications represent the fastest-growing segment as healthcare manufacturers prioritize renewable biomaterials with superior structural characteristics for wound care and tissue engineering. Electronics applications also strengthen through flexible substrates and printed electronic components requiring advanced functional materials. Companies increasingly establish partnerships with medical device manufacturers and electronics suppliers to develop specialized nanocellulose grades tailored to regulated, high-performance environments.

Packaging remains the leading end-user due to continuous demand for recyclable, lightweight, and high-strength materials compatible with existing converting operations. Around 47% of commercial nanocellulose consumption supports packaging production, while advanced barrier formulations improve shelf-life performance by approximately 28%. Pulp & Paper maintains strong utilization through fiber reinforcement and process optimization, whereas Construction increasingly incorporates nanocellulose into sustainable building materials. Companies continue expanding production partnerships with converters and fiber manufacturers to strengthen integrated supply networks and improve cost competitiveness.

Healthcare is the fastest-growing end-user, driven by expanding applications in wound management, tissue engineering, and medical biomaterials. Electronics manufacturers are increasing adoption for flexible devices, while Automotive companies utilize nanocellulose composites to reduce component weight by nearly 15%. Suppliers are introducing customized product portfolios, long-term development agreements, and application-specific pricing strategies to strengthen customer retention across specialized industrial sectors.

Asia-Pacific accounted for the largest market share at 42.8% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 13.2% between 2026 and 2033.

Advanced Commercialization Through Industrial Partnerships

North America is strengthening its position through commercialization of advanced bio-based materials across packaging, healthcare, and specialty composites. The region contributes approximately 24% of global nanocellulose production, supported by integrated pulp processing infrastructure and strong collaboration between research institutions and industrial manufacturers. Continuous manufacturing technologies are improving production efficiency by nearly 18%, while investment in pilot-scale facilities is accelerating qualification for industrial customers. Companies are prioritizing strategic partnerships with packaging converters and specialty chemical producers to shorten commercialization timelines and strengthen domestic supply resilience amid growing preference for renewable material sourcing.

United States Market Outlook: The United States leads regional deployment through advanced material innovation, established forest-product infrastructure, and extensive collaboration between universities and industrial enterprises. More than 40 commercial and pilot-scale nanocellulose initiatives support packaging, biomedical, and composite manufacturing. Federal support for sustainable manufacturing and private investment in specialty biomaterials continue encouraging commercialization, while major packaging producers increasingly integrate nanocellulose into recyclable product portfolios to improve performance and reduce dependence on petroleum-derived additives.

Circular Manufacturing Drives Industrial Expansion

Europe maintains a strong competitive position through circular economy policies, advanced forestry resources, and established pulp processing industries. The region accounts for approximately 29% of global commercial capacity, with Finland, Sweden, and Germany leading industrial deployment. Manufacturers are integrating nanocellulose into recyclable packaging, specialty coatings, and lightweight composites, while automated fiber processing improves production consistency by nearly 16%. Industrial alliances between forestry companies and specialty chemical producers continue expanding commercial-scale manufacturing as environmental regulations accelerate substitution of conventional synthetic materials.

Finland Market Outlook: Finland remains Europe's strategic leader due to its integrated forestry value chain, advanced fiber-processing expertise, and strong industrial research ecosystem. Large-scale pulp producers continue expanding nanocellulose pilot facilities and specialty production capabilities, while collaborative innovation programs accelerate commercialization. More than 70% of domestic pulp production capacity is supported by sustainable forest certification, providing reliable feedstock availability and strengthening Finland's position in premium bio-based material manufacturing.

Manufacturing Scale Strengthens Global Leadership

Asia-Pacific dominates global nanocellulose production through integrated manufacturing infrastructure, strong packaging demand, and expanding advanced material industries. The region represents approximately 43% of worldwide market activity, supported by large-scale pulp manufacturing and extensive commercialization across packaging, electronics, and automotive applications. Japan, China, and South Korea continue increasing production capacity, while manufacturing automation improves throughput by nearly 20%. Export-oriented supply chains and government-backed bioeconomy initiatives encourage continuous investment in industrial-scale facilities capable of serving both domestic and international markets.

Japan Market Outlook: Japan leads the regional market through technological leadership, commercial manufacturing maturity, and extensive enterprise collaboration. Advanced nanocellulose applications span automotive components, electronics substrates, and sustainable packaging materials. More than 35 industrial research and commercialization programs actively support product innovation, while manufacturers continue investing in continuous processing technologies that improve product consistency and strengthen global competitiveness in high-value specialty materials.

Forest Resources Support Industrial Development

South America is leveraging abundant forestry resources and competitive pulp production to expand participation in advanced bio-based materials. The region contributes approximately 8% of global nanocellulose output, with industrial investment increasingly targeting value-added processing rather than raw pulp exports. Modernization of fiber processing facilities has improved production efficiency by nearly 14%, although commercial deployment remains constrained by limited downstream specialty manufacturing. Companies are responding through partnerships with international technology providers and investment in pilot-scale facilities to strengthen regional processing capabilities.

Brazil Market Outlook: Brazil serves as the regional growth engine through its globally competitive eucalyptus pulp industry and expanding industrial biotechnology capabilities. Large forestry enterprises are exploring nanocellulose integration within existing production assets to capture higher-value markets. Strong plantation productivity, modern pulp infrastructure, and growing collaboration with packaging manufacturers provide Brazil with a strategic foundation for scaling commercial nanocellulose production while improving export diversification.

Strategic Industrial Diversification Accelerates Adoption

The Middle East & Africa market remains at an early commercialization stage but is gaining momentum through industrial diversification, sustainable manufacturing initiatives, and investment in advanced materials. The region represents approximately 5% of global demand, with specialty packaging and construction materials emerging as priority application areas. Government-supported industrial modernization programs are encouraging investment in renewable material technologies, while infrastructure upgrades improve logistics efficiency by nearly 12%. Companies increasingly pursue technology partnerships and localized processing capabilities to reduce import dependence and establish regional manufacturing expertise.

Saudi Arabia Market Outlook: Saudi Arabia is strengthening its market position through industrial diversification strategies, expanding specialty manufacturing, and investment in sustainable materials. National industrial development initiatives encourage advanced material production alongside chemical manufacturing expansion. Integration of renewable material technologies into packaging and construction sectors is accelerating, while partnerships with international technology providers support knowledge transfer, process optimization, and long-term development of domestic advanced materials capabilities.

The competitive landscape is shaped by established material innovators including CelluForce, Borregaard, Nippon Paper Industries, Stora Enso, and Sappi, competing against emerging specialty nanomaterial producers and regional pulp technology companies. Global leaders emphasize proprietary processing technologies and integrated fiber supply, while regional manufacturers compete through lower production costs and localized customer support. The top five companies collectively account for approximately 48% of global market activity, reflecting moderate consolidation with strong technology differentiation. Competition centers on production efficiency, customized formulations, and secure feedstock integration, where continuous processing reduces manufacturing costs by nearly 20% and advanced surface modification improves application performance by approximately 25%. Companies are expanding demonstration facilities, forming joint development partnerships with packaging and healthcare manufacturers, and vertically integrating pulp sourcing to strengthen supply resilience. Competitive momentum is shifting toward application-specific materials and scalable commercial manufacturing rather than laboratory innovation. High capital requirements, process know-how, and industrial qualification cycles remain significant entry barriers. Market leadership depends on scalable production, differentiated technology, and strategic customer integration.

CelluForce Inc.

Borregaard ASA

Nippon Paper Industries Co., Ltd.

Stora Enso Oyj

Sappi Limited

American Process Inc.

Kruger Inc.

Oji Holdings Corporation

UPM-Kymmene Corporation

Weidmann Holding AG

Melodea Ltd.

Daicel Corporation

Commercial technology development is shifting from laboratory-scale production toward automated, industrial manufacturing platforms. Continuous fibrillation systems, AI-enabled process monitoring, and precision surface functionalization are replacing conventional batch production. Compared with legacy batch processing, continuous manufacturing improves production efficiency by approximately 22% while reducing energy consumption by nearly 18%. Around 45% of newly commissioned production projects now incorporate automated quality monitoring to improve consistency and reduce downstream processing variation, enabling manufacturers to achieve faster product qualification and more predictable industrial supply.

Emerging technologies focus on multifunctional nanocellulose with conductive, antimicrobial, and high-barrier properties for packaging, electronics, and biomedical applications. Advanced chemical modification increases material compatibility by approximately 24%, while digital production control lowers quality deviations by nearly 15%. Companies with integrated pulp processing and proprietary functionalization technologies gain stronger competitive advantages because they can commercialize application-specific grades faster than producers relying on standardized material portfolios.

Between 2026 and 2028, disruptive advances will center on modular production systems, enzyme-assisted fibrillation, and digital manufacturing optimization. Automated process control is expected to exceed 55% deployment among new industrial facilities, reducing operating complexity while improving scalability. Early adopters investing in integrated manufacturing, advanced analytics, and customer-specific material development will secure stronger long-term positioning as industrial buyers increasingly prioritize performance consistency, sustainable production, and supply-chain resilience.

April 2026 – Stora Enso launched Trayforma Brown and reduced basis weight across its Trayforma portfolio, improving material efficiency while maintaining packaging performance. The lighter board design lowers fiber consumption by up to 10%, strengthening sustainable food packaging competitiveness and reducing customer material usage. Source: storaenso.com

June 2026 – Stora Enso approved a EUR 19 million investment to increase fluff pulp production at its Skutskär facility while restructuring operations toward higher-value specialty pulp grades. The capacity-focused expansion strengthens renewable fiber availability for advanced cellulose applications and improves long-term manufacturing competitiveness. Source: storaenso.com

2025 – Melodea expanded commercialization of its cellulose-based barrier coating technology for recyclable food packaging, reporting up to 80% reduction in plastic coating requirements compared with conventional multilayer solutions. The innovation accelerates industrial adoption of fiber-based packaging and supports compliance with tightening sustainability regulations. Source: packagingeurope.com

2024 – CelluForce advanced commercial deployment of cellulose nanocrystals through expanded industrial collaborations targeting lightweight composites and specialty formulations, demonstrating material reinforcement improvements of approximately 30% in selected composite applications. The initiative strengthens downstream adoption across automotive and advanced manufacturing value chains. Source: celluforce.com

This report provides a comprehensive assessment of the global nanocellulose market across the 2026–2033 strategic planning period, covering production trends, commercialization pathways, technology evolution, competitive positioning, and operational developments. The analysis evaluates five major material types, five application categories, and six end-user industries across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 40% of the assessment emphasizes high-value specialty applications, manufacturing optimization, and enterprise deployment strategies shaping industry transformation.

The report examines production scalability, process automation, advanced functionalization technologies, supply-chain integration, and application-specific innovation alongside regional manufacturing capabilities and investment priorities. It highlights deployment patterns, competitive differentiation, partnership activity, and emerging niche opportunities in biomedical materials, flexible electronics, sustainable packaging, and advanced composites. The findings support investment decisions, capacity expansion planning, product portfolio optimization, market entry evaluation, and long-term competitive positioning through actionable operational and strategic intelligence.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

C111% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

T1 |

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

mplayers |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |