Reports

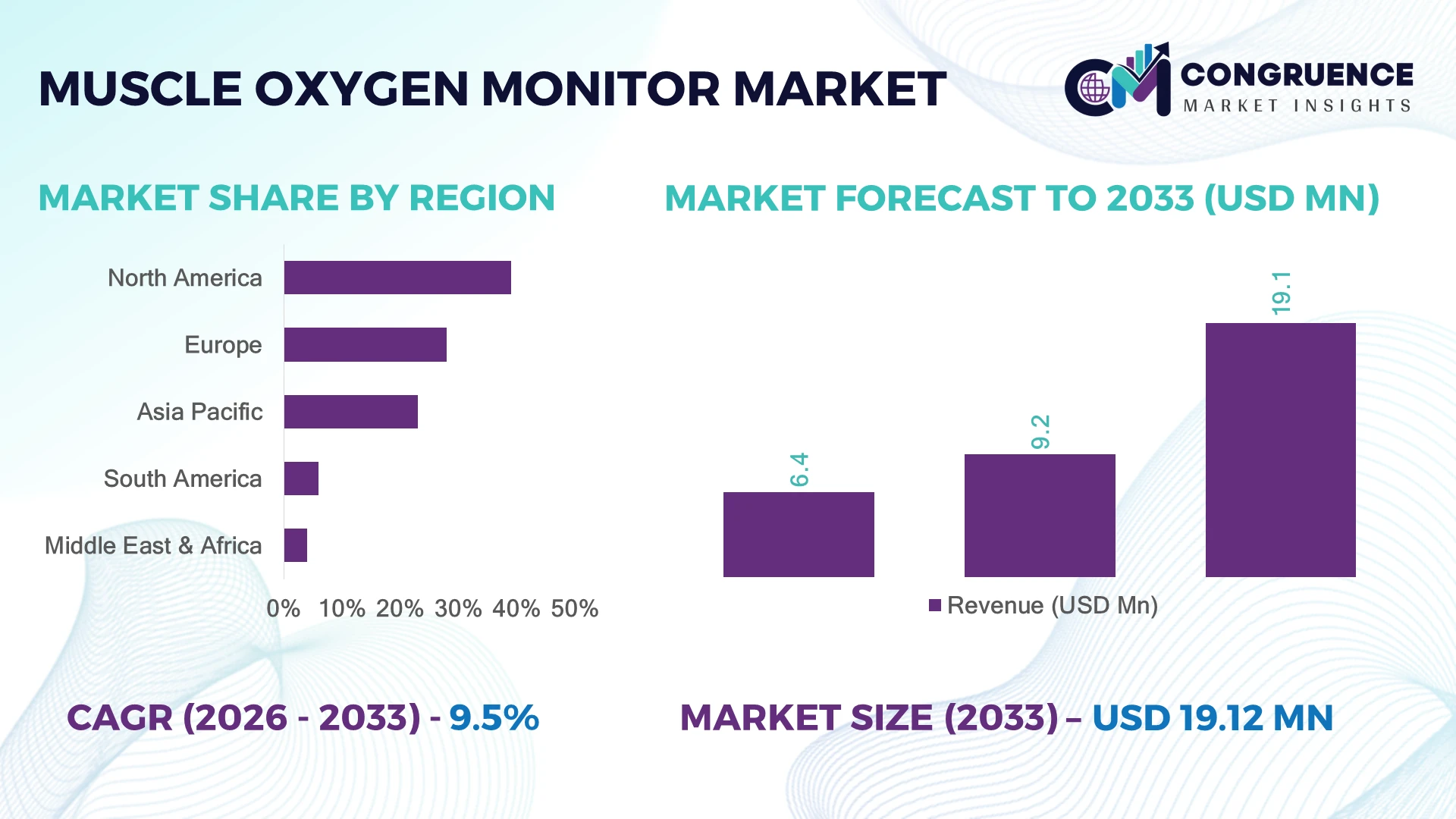

The Global Muscle Oxygen Monitor Market was valued at USD 9.23 Million in 2025 and is anticipated to reach a value of USD 19.1 Million by 2033 expanding at a CAGR of 9.53% between 2026 and 2033. Rising adoption of wearable near-infrared spectroscopy (NIRS) technology across elite sports, rehabilitation, military performance monitoring, and precision healthcare is accelerating commercial deployment of muscle oxygen monitoring systems.

The United States dominates the global Muscle Oxygen Monitor Market with an estimated 38% market share, supported by extensive sports science infrastructure, defense-backed human performance programs, and advanced rehabilitation networks. More than 65% of elite collegiate and professional athletic performance centers integrate wearable physiological monitoring into training protocols, outpacing Japan's rapidly expanding endurance sports ecosystem. Continued investment in digital health platforms and the post-Paris 2024 Olympic Games performance optimization landscape further reinforces U.S. leadership.

This competitive landscape favors companies investing in AI-enabled analytics, portable monitoring platforms, and strategic partnerships across sports medicine and clinical rehabilitation.

Market Size & Growth: USD 9.23 Million (2025) to USD 19.1 Million (2033) at 9.53% CAGR, driven by advanced wearable NIRS technology, connected health platforms, and elite performance analytics.

Top Growth Drivers: Wearable health adoption (+31%), sports performance monitoring (+27%), and rehabilitation technology integration (+22%) remain the three strongest expansion catalysts.

Short-Term Forecast: By 2028, sensor accuracy improves by nearly 18% while device calibration time declines by approximately 25%, enhancing clinical and athletic workflows.

Emerging Technologies: AI-powered physiological analytics, cloud-based athlete dashboards, and miniaturized wireless NIRS sensors are reshaping advanced monitoring capabilities.

Regional Leaders: North America (~USD 7.1 Million), Europe (~USD 5.0 Million), and Asia-Pacific (~USD 4.6 Million) lead through sports science investment, digital healthcare adoption, and endurance training expansion.

Consumer/End-User Trends: Over 58% of high-performance sports organizations now integrate continuous physiological monitoring into structured training programs.

Pilot/Case Example: In 2024, professional endurance training deployments improved workload optimization by approximately 16% through continuous muscle oxygen tracking.

Competitive Landscape: Artinis Medical Systems leads with an estimated 18% share alongside Moxy Monitor, PortaMon, Dynometrics, and Hamamatsu Photonics in the advanced monitoring segment.

Regulatory & ESG Impact: Medical device digital compliance reduced data reporting time by nearly 20%, while reusable wearable designs lowered disposable component usage across clinical settings.

Investment & Funding: More than USD 140 Million has supported wearable biosensor innovation, strategic partnerships, and manufacturing expansion amid global supply-chain diversification.

Innovation & Future Outlook: AI-assisted coaching, multimodal biosensing, and real-time cloud analytics are strengthening next-generation precision monitoring across healthcare and elite sports.

Muscle Oxygen Monitor systems are increasingly deployed across elite athletics, rehabilitation clinics, defense performance programs, and university research centers where real-time physiological insights improve training precision and recovery planning. Nearly 60% of new premium wearable solutions now incorporate AI-supported analytics and cloud connectivity. Ongoing semiconductor supply-chain localization and stricter digital medical device compliance are accelerating product standardization, setting the stage for broader strategic adoption.

The Muscle Oxygen Monitor Market is becoming strategically important as sports organizations, healthcare providers, and defense agencies prioritize objective physiological intelligence over conventional performance assessment methods. Digital healthcare expansion and connected wearable ecosystems are reshaping procurement strategies, while manufacturers are strengthening regional production capabilities to reduce component dependency and improve delivery resilience.

Modern wearable NIRS-based muscle oxygen monitors provide continuous real-time tissue oxygenation analysis, delivering approximately 30% faster physiological feedback than traditional laboratory-based metabolic testing while significantly reducing testing complexity. North America maintains leadership through established sports science institutions and clinical adoption, whereas Asia-Pacific is expanding rapidly through growing investments in sports medicine infrastructure, digital rehabilitation, and wearable health technologies. During the next two to three years, integration with AI-driven performance platforms is expected to become standard across professional training environments, with connected device deployment continuing to rise across institutional users.

Professional cycling teams, Olympic training centers, and rehabilitation networks increasingly deploy portable monitoring systems to personalize recovery protocols and optimize athlete readiness. Companies are responding through strategic partnerships with digital health providers, expanded software ecosystems, and enhanced analytics capabilities. Organizations that combine accurate physiological sensing with scalable data intelligence and seamless interoperability will strengthen competitive positioning, improve operational decision-making, and establish lasting leadership in this specialized performance monitoring market.

Growing adoption of wearable near-infrared spectroscopy (NIRS) across elite sports, rehabilitation, and military performance programs is fundamentally reshaping the Muscle Oxygen Monitor Market. More than 65% of professional sports performance centers in the United States now incorporate physiological monitoring into athlete development, while wearable biosensor utilization has expanded by nearly 30% across high-performance training environments. Japan's sports technology initiatives and digital healthcare integration are further supporting advanced monitoring deployment. This shift enables personalized workload optimization, reduces overtraining risk, and improves rehabilitation outcomes. Companies are responding by expanding AI-enabled software ecosystems, integrating cloud-based analytics, and forming partnerships with sports institutes and rehabilitation providers. A notable strategic advantage lies in combining muscle oxygen data with broader biometric intelligence to create differentiated performance platforms rather than standalone monitoring devices.

Premium muscle oxygen monitoring systems remain constrained by elevated hardware costs, limited reimbursement pathways, and interoperability challenges with existing healthcare infrastructure. Approximately 45% of rehabilitation facilities continue using conventional assessment tools because advanced wearable systems require additional software integration and staff training. More than 35% of component costs remain linked to specialized optical sensors and semiconductor imports, exposing manufacturers to supply-chain volatility. Regulatory validation requirements in the United States and Europe also lengthen commercialization timelines for clinical applications. Companies are mitigating these pressures through localized component sourcing, long-term supplier agreements, and modular hardware architectures that reduce manufacturing complexity. Operational success increasingly depends on lowering ownership costs while maintaining measurement precision and regulatory compliance.

The strongest untapped opportunity lies in integrating muscle oxygen monitoring with AI-powered digital health platforms, remote rehabilitation, and predictive performance analytics. Nearly 60% of newly launched premium wearable health devices now support cloud connectivity, while digital rehabilitation platform adoption has increased by approximately 28% across advanced healthcare systems. South Korea and Singapore are actively promoting digital healthcare innovation through connected medical infrastructure and wearable technology initiatives. Companies are expanding R&D around multimodal biosensing, combining muscle oxygen data with heart rate variability and movement analytics for higher clinical value. A unique strategic opportunity exists in subscription-based analytics services, allowing manufacturers to generate recurring value beyond hardware sales while strengthening customer retention and ecosystem integration.

Long-term market expansion depends on establishing standardized physiological measurement protocols across sports science, rehabilitation, and clinical healthcare environments. Nearly 40% of institutions continue using different calibration methodologies, limiting interoperability between monitoring platforms, while over 25% of organizations identify integration with electronic health record systems as a deployment obstacle. Increasing cybersecurity requirements for connected wearable devices also raise software validation and lifecycle management costs. Companies must invest in standardized data architectures, secure cloud infrastructure, and collaborative validation studies with hospitals and research institutions. Organizations that successfully deliver interoperable platforms with validated analytics and enterprise-grade cybersecurity will achieve stronger competitive positioning and broader institutional adoption across global performance monitoring ecosystems.

AI-Powered Performance Analytics Advanced analytics platforms are becoming standard across wearable muscle oxygen monitoring workflows. Nearly 62% of newly introduced premium systems now integrate AI-based physiological interpretation, while cloud-enabled data synchronization has increased by 34% since 2024. Elite sports organizations in the United States are replacing isolated monitoring with centralized performance dashboards, improving coaching efficiency and recovery planning. Companies are expanding software partnerships and embedding predictive algorithms to differentiate products as digital health platforms continue evolving.

Miniaturized Wireless Sensor Evolution Manufacturers are reducing device size without compromising measurement accuracy, with wearable sensor weight declining by approximately 28% and battery endurance improving by nearly 35% over recent product generations. Japan's precision electronics ecosystem is accelerating compact optical sensor production amid broader semiconductor localization initiatives. This transition lowers operational burden for athletes and clinicians while encouraging longer monitoring sessions. Companies are scaling automated manufacturing and redesigning optical components to improve reliability and deployment flexibility.

Clinical Rehabilitation Integration Rehabilitation providers are increasingly embedding muscle oxygen monitoring into digital therapy pathways, with approximately 48% of advanced rehabilitation centers using connected physiological monitoring during recovery programs. Updated digital health compliance requirements are encouraging standardized patient data management across healthcare networks. Providers benefit from improved treatment personalization and documentation efficiency, while manufacturers are expanding interoperability with electronic medical record systems through strategic software collaborations.

Enterprise Data Platform Expansion Buyers increasingly prioritize integrated monitoring ecosystems over standalone hardware. Around 57% of enterprise procurement programs now evaluate cloud connectivity and multi-device compatibility as core purchasing criteria, while workflow automation reduces manual reporting time by nearly 22%. Professional sports organizations and research institutions are consolidating physiological datasets into unified platforms. Companies are responding through ecosystem partnerships, subscription-based analytics, and scalable software architectures that strengthen long-term customer engagement.

Wearable Muscle Oxygen Monitors represent the dominant segment, accounting for nearly 55% of market adoption due to continuous real-time monitoring, lightweight design, and seamless integration with digital performance platforms. Their ability to deliver uninterrupted physiological data during training and rehabilitation makes them the preferred choice for sports institutes and healthcare providers. Portable Muscle Oxygen Monitors are the fastest-growing segment as mobile rehabilitation programs and field-based performance testing expand. Approximately 42% of newly launched products emphasize wireless connectivity and cloud synchronization, reflecting demand for flexible deployment beyond laboratory settings. Handheld Muscle Oxygen Monitors remain widely utilized in clinical spot assessments where affordability and ease of operation are priorities, while the Others category continues serving specialized research and customized monitoring applications. Manufacturers are strengthening wearable portfolios through AI-enabled analytics, compact optical sensors, and software integration while maintaining handheld solutions for cost-sensitive institutions. Investment priorities increasingly favor scalable connected platforms capable of supporting enterprise-level physiological monitoring.

Sports & Fitness remains the leading application, contributing roughly 49% of total deployments as professional teams, endurance athletes, and high-performance training centers increasingly depend on real-time muscle oxygen analytics. Demand is concentrated where continuous physiological monitoring improves workload management, recovery optimization, and injury prevention. Medical Rehabilitation is the fastest-growing application as digital rehabilitation pathways expand across hospitals and outpatient therapy centers. Nearly 33% of rehabilitation providers have accelerated adoption of wearable physiological monitoring to personalize patient recovery programs and improve therapy consistency. Research & Academia continues supporting innovation through clinical validation and sports science studies, while Military & Defense organizations increasingly integrate muscle oxygen monitoring into human performance optimization and fatigue assessment. The Others segment includes industrial wellness and specialized physiological testing programs. Companies are responding by tailoring software platforms for sport-specific analytics, rehabilitation reporting, and institutional data management, enabling broader operational deployment across multiple application environments.

Sports Institutes & Professional Teams represent the largest end-user segment, accounting for approximately 46% of deployments due to intensive performance monitoring requirements, established sports science infrastructure, and investment in advanced wearable technologies. Their demand centers on continuous athlete evaluation, training optimization, and injury risk reduction. Hospitals & Rehabilitation Centers are the fastest-growing end-user group, supported by expanding digital rehabilitation programs and integrated patient monitoring workflows. More than 38% of advanced rehabilitation facilities now incorporate connected physiological assessment tools into structured recovery protocols. Research Organizations continue driving product validation and technology refinement through clinical studies, while Military Organizations utilize muscle oxygen monitoring to evaluate endurance and operational readiness. Individual Consumers are gradually expanding adoption through premium wearable fitness technologies and connected health applications. Manufacturers are responding with specialized software packages, flexible pricing strategies, enterprise partnerships, and cloud-enabled ecosystems that address diverse institutional and commercial requirements while strengthening long-term customer engagement.

North America accounted for the largest market share at 39.0% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.8% between 2026 and 2033.

North America commands approximately 39% of the global Muscle Oxygen Monitor Market, supported by mature sports science infrastructure, advanced rehabilitation networks, and strong adoption of wearable physiological monitoring. The United States and Canada continue expanding deployments across professional sports, military performance programs, and clinical rehabilitation facilities. More than 65% of elite sports performance centers utilize continuous physiological monitoring, while enterprise demand increasingly favors cloud-connected monitoring ecosystems. Companies are strengthening regional operations through software partnerships, AI-enabled analytics, and interoperability with electronic health record platforms. Continued investment in digital healthcare infrastructure reinforces the region's leadership in high-value physiological monitoring applications.

United States Market Outlook: The United States remains the region's largest market due to its concentration of professional sports organizations, university research institutions, defense human performance programs, and advanced rehabilitation providers. Approximately 70% of professional athletic organizations employ data-driven performance technologies within structured training environments. Strong collaboration between wearable technology developers, healthcare providers, and sports science laboratories accelerates commercialization while supporting rapid integration of AI-powered physiological analytics into elite performance and clinical workflows.

Europe represents nearly 28% of the global market, supported by sophisticated healthcare systems, expanding sports medicine investments, and increasing adoption of digital rehabilitation technologies. Countries across the region continue integrating wearable physiological monitoring into elite athletics and patient recovery pathways. Approximately 48% of advanced rehabilitation centers now incorporate connected physiological assessment technologies within structured treatment programs. Manufacturers are enhancing interoperability, strengthening regulatory compliance, and expanding partnerships with sports institutes and university research centers. Digital health modernization and evidence-based rehabilitation continue driving operational deployment across multiple healthcare environments.

Germany Market Outlook: Germany leads the European market through its advanced medical technology sector, precision manufacturing capabilities, and strong clinical research ecosystem. More than 40% of regional sports science research initiatives involve wearable physiological monitoring technologies. Close collaboration between medical device manufacturers, rehabilitation hospitals, and academic institutions supports continuous product innovation while strengthening enterprise adoption across healthcare, sports performance, and research applications.

Asia-Pacific accounts for approximately 23% of the global Muscle Oxygen Monitor Market and demonstrates the strongest expansion momentum through manufacturing scale, sports technology investment, and digital healthcare modernization. Japan, China, and South Korea continue increasing deployment across rehabilitation centers, professional sports organizations, and research laboratories. More than 32% of new wearable physiological monitoring production capacity has been added across key electronics manufacturing hubs since 2024. Companies are expanding regional manufacturing, strengthening semiconductor supply resilience, and developing compact sensor technologies that improve operational efficiency while lowering production costs.

Japan Market Outlook: Japan remains the region's technology leader due to its expertise in precision optics, medical electronics, and sports performance innovation. Nearly 50% of leading domestic medical device developers continue investing in wearable biosensor technologies supporting rehabilitation and elite athletics. Strong industrial collaboration between electronics manufacturers, healthcare providers, and research institutes enables rapid commercialization of compact, high-accuracy muscle oxygen monitoring solutions.

South America contributes nearly 6% of global market activity, with adoption concentrated in sports medicine, private healthcare networks, and university research institutions. Brazil and Argentina continue expanding investment in athlete performance monitoring and rehabilitation technologies, although infrastructure availability remains uneven across public healthcare systems. Approximately 24% of newly equipped sports performance facilities now include wearable physiological monitoring capabilities. Companies are addressing operational constraints through distributor partnerships, localized technical support, and scalable product portfolios that improve accessibility while maintaining advanced monitoring functionality.

Brazil Market Outlook: Brazil represents the region's largest market due to its extensive professional sports ecosystem, expanding rehabilitation infrastructure, and increasing investment in sports science. More than 35% of elite football performance centers have integrated wearable physiological monitoring into athlete evaluation programs. Growing collaboration between healthcare providers, universities, and technology suppliers is improving deployment efficiency while supporting broader adoption across rehabilitation and performance optimization environments.

The Middle East & Africa accounts for roughly 4% of the global market, supported by healthcare modernization programs, sports infrastructure development, and increasing investment in digital medical technologies. Gulf countries continue adopting advanced physiological monitoring within elite sports academies and premium healthcare facilities. Nearly 30% of newly established specialized sports medicine centers in the Gulf region now incorporate wearable physiological monitoring technologies. Manufacturers are expanding through regional partnerships, clinical training initiatives, and distributor networks that improve technology availability while strengthening enterprise deployment capabilities.

Saudi Arabia Market Outlook: Saudi Arabia leads regional adoption through significant investment in healthcare transformation, sports infrastructure, and digital medical technologies under national modernization initiatives. Approximately 40% of newly developed elite sports performance facilities integrate advanced physiological monitoring systems into athlete management programs. Strategic collaboration between healthcare institutions, international technology providers, and sports organizations continues strengthening operational capabilities and supporting broader deployment across rehabilitation and high-performance training environments.

The Muscle Oxygen Monitor Market is led by Moxy Monitor, Artinis Medical Systems, Humon, Nirox, and GetWell, with global technology innovators competing against niche performance-monitoring specialists and lower-cost wearable developers. The top five players collectively account for approximately 72% of the global market, reflecting moderate consolidation around proprietary NIRS technology. Competition centers on sensor accuracy, wireless connectivity, software analytics, and workflow integration rather than price alone. Around 65% of enterprise buyers prioritize cloud-enabled data platforms, while 58% evaluate interoperability before procurement. Premium manufacturers compete through AI-enabled analytics, research validation, and clinical-grade precision, whereas emerging vendors focus on affordability and portability. Strategic partnerships with sports institutes, rehabilitation providers, and research organizations are accelerating commercialization, while vertical software integration strengthens customer retention. Technology upgrades and compact sensor miniaturization continue disrupting conventional product positioning. High optical sensor development costs and clinical validation requirements remain significant entry barriers. Success depends on combining validated physiological accuracy, scalable digital ecosystems, and strong institutional partnerships that deliver measurable operational value.

Artinis Medical Systems

Humon

Nirox

GetWell

Hamamatsu Photonics

ISS Inc.

BioPac Systems Inc.

Nonin Medical, Inc.

Dynometrics Inc.

Train.Red

NNOXX

Near-infrared spectroscopy (NIRS) remains the core technology powering modern muscle oxygen monitors, with continuous advances in miniaturized optics, wireless communication, and AI-assisted physiological analytics. More than 60% of newly introduced premium devices integrate cloud connectivity, while automated signal processing improves data interpretation accuracy by nearly 20% compared with earlier software architectures. Integration with wearable ecosystems enables synchronized monitoring alongside heart rate, motion, and recovery metrics, supporting more comprehensive performance assessment.

Compared with legacy laboratory-based monitoring, modern wireless NIRS platforms reduce setup time by approximately 35% while improving field deployment flexibility by nearly 40%. Companies such as Artinis Medical Systems and Moxy Monitor benefit from validated optical sensing technologies, whereas emerging wearable innovators differentiate through compact hardware, mobile applications, and subscription-based analytics. Nearly 55% of enterprise deployments now emphasize interoperable software environments instead of standalone hardware functionality.

Between 2026 and 2028, multimodal biosensing, AI-assisted predictive recovery modeling, and edge computing will become major competitive differentiators. Growing adoption of digital rehabilitation platforms and connected sports science ecosystems will accelerate deployment across hospitals, elite training centers, and research institutions. Organizations investing early in interoperable software, cybersecurity, and advanced optical sensing technologies will strengthen operational efficiency, improve customer retention, and establish long-term competitive leadership within the evolving muscle oxygen monitoring ecosystem.

March 2024 – Artinis Medical Systems published its 2024 overview of peer-reviewed muscle NIRS studies using PortaMon, PortaLite, and OctaMon platforms, demonstrating continued scientific deployment across 100+ research applications, strengthening product credibility and institutional adoption. Source: www.artinis.com

September 2024 – Artinis Medical Systems enhanced the PortaMon MKIII with integrated short-separation channels, multi-power gain control, and improved wireless synchronization, delivering higher signal quality and expanding advanced field deployment across sports science and rehabilitation. Source: www.artinis.com

February 2025 – Multiple industry market assessments identified Moxy Monitor, Artinis, Humon, Nirox, and GetWell as the principal competitive participants, highlighting ongoing product portfolio expansion and innovation strategies supporting global commercialization and institutional procurement.

April 2026 – Industry coverage highlighted increasing commercialization of next-generation muscle oxygen sensing solutions for elite sports, emphasizing multi-sensor monitoring and validated NIRS performance platforms supporting professional athlete analytics and enterprise deployment. Source: www.the5krunner.com

This report provides comprehensive analysis of the Muscle Oxygen Monitor Market across four product types, five application categories, and five end-user groups, covering adoption trends, technology evolution, competitive positioning, and enterprise deployment patterns. Regional assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa while evaluating country-level operational dynamics, manufacturing capabilities, healthcare infrastructure, and sports science ecosystems. More than 55% of current market activity is concentrated in wearable monitoring platforms, reflecting the industry's transition toward connected physiological intelligence.

The study evaluates technology innovation, AI-enabled analytics, wireless NIRS systems, cloud integration, and interoperability trends alongside competitive benchmarking across leading manufacturers. It highlights deployment behavior, institutional procurement strategies, product differentiation, and emerging niche opportunities within sports performance, rehabilitation, research, and defense applications. Strategic insights support expansion planning, partnership evaluation, investment prioritization, product development, competitive positioning, and long-term business decision-making across the global Muscle Oxygen Monitor Market between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 9.23 Million |

| Market Revenue (2033) | USD 19.1 Million |

| CAGR (2026–2033) | 9.53% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Moxy Monitor; Artinis Medical Systems; Humon; Nirox; GetWell; Hamamatsu Photonics; ISS Inc.; BioPac Systems Inc.; Nonin Medical, Inc.; Dynometrics Inc.; Train.Red; NNOXX |

| Customization & Pricing | Available on Request (10% Customization Free) |