Reports

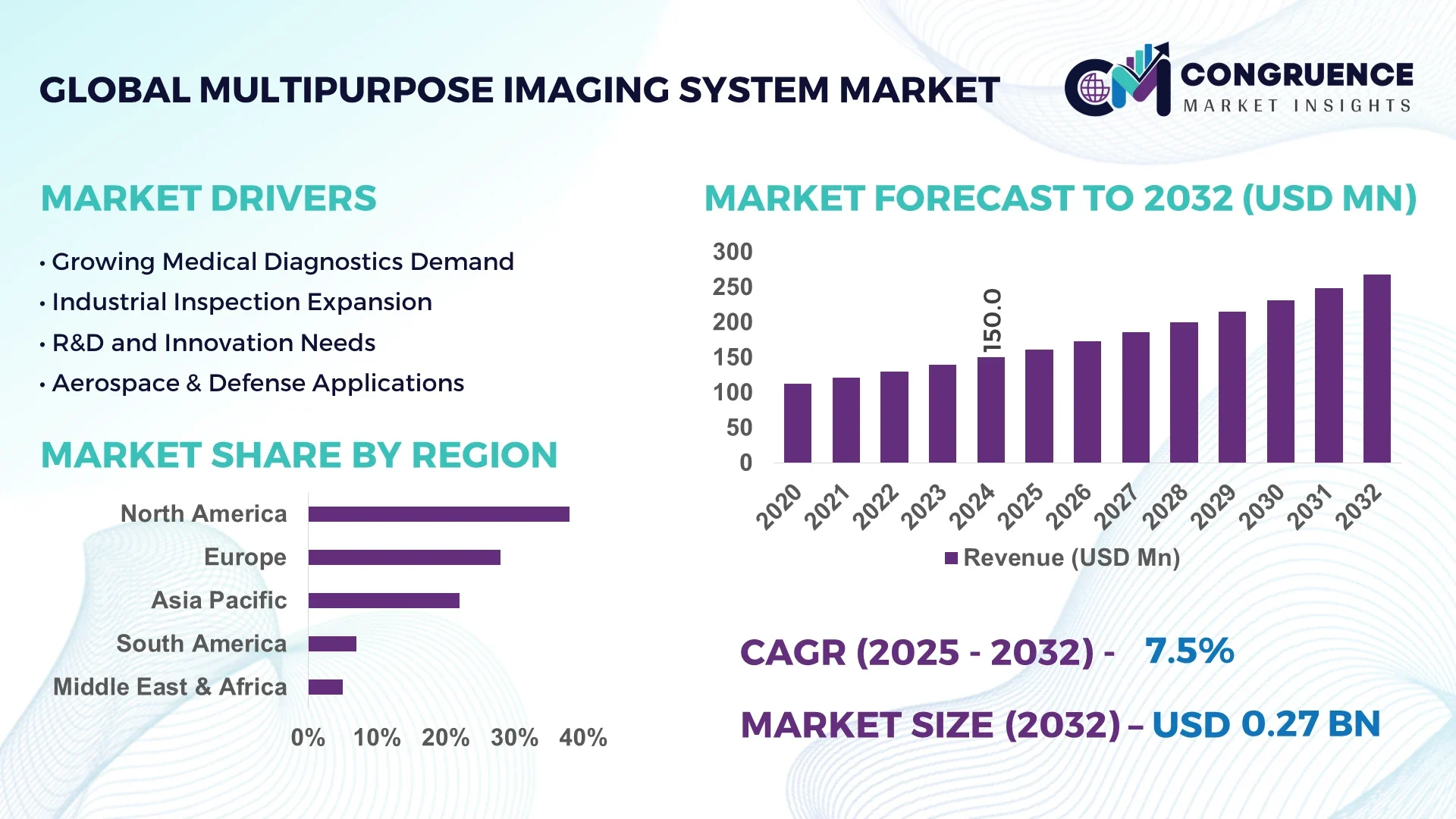

The Global Multipurpose Imaging System Market was valued at USD 150.0 Million in 2024 and is anticipated to reach a value of USD 267.5 Million by 2032, expanding at a CAGR of 7.5% between 2025 and 2032. This growth is primarily driven by advancements in imaging technologies and the increasing demand for multifunctional diagnostic tools across various medical applications.

In the United States, the adoption of multipurpose imaging systems is particularly robust, with a significant concentration of installations in hospitals and imaging centers. Approximately 65% of healthcare facilities in the U.S. have integrated these systems into their diagnostic workflows. The U.S. also leads in research and development investments, contributing to continuous technological innovations in the field.

Market Size & Growth: Valued at USD 150.0 Million in 2024; projected to reach USD 267.5 Million by 2032, expanding at a CAGR of 7.5%.

Top Growth Drivers: Technological advancements (45%), increasing healthcare expenditure (35%), and rising prevalence of chronic diseases (20%).

Short-Term Forecast: By 2028, the integration of AI in imaging systems is expected to improve diagnostic accuracy by 30%.

Emerging Technologies: AI-enhanced imaging, portable imaging devices, and 3D imaging technologies.

Regional Leaders: North America (USD 1.2 Billion), Europe (USD 900 Million), Asia-Pacific (USD 700 Million) by 2032.

Consumer/End-User Trends: Hospitals and imaging centers are the primary adopters, with a growing trend towards outpatient diagnostics.

Pilot or Case Example: In 2023, a U.S.-based hospital network implemented AI-driven imaging systems, resulting in a 25% reduction in diagnostic time.

Competitive Landscape: GE Healthcare (25%), Siemens Healthineers (20%), Philips Healthcare (15%), Canon Medical Systems (10%), and Fujifilm Holdings (10%).

Regulatory & ESG Impact: Compliance with FDA regulations and a focus on sustainable manufacturing practices are influencing market dynamics.

Investment & Funding Patterns: Recent investments include USD 500 Million in R&D for AI-based imaging technologies.

Innovation & Future Outlook: The market is moving towards fully integrated imaging solutions with real-time data analytics capabilities.

The multipurpose imaging system market is characterized by rapid technological advancements, leading to more efficient and accurate diagnostic tools. Key industry sectors such as hospitals, imaging centers, and research institutions are increasingly adopting these systems to enhance patient care. Regulatory standards and environmental considerations are shaping product development and manufacturing processes. Regional consumption patterns indicate a shift towards outpatient diagnostics, with emerging markets showing significant growth potential. Looking ahead, the integration of AI and machine learning is expected to further revolutionize the field, offering improved diagnostic capabilities and operational efficiencies.

The strategic relevance of the multipurpose imaging system market lies in its ability to provide comprehensive diagnostic solutions across various medical disciplines. By 2026, the integration of AI technologies is expected to reduce diagnostic errors by 20%, enhancing patient outcomes and operational efficiency. Regionally, North America leads in volume, while Europe demonstrates a higher adoption rate, with 75% of healthcare facilities utilizing advanced imaging systems. In the short term, the focus is on developing portable and cost-effective imaging solutions to increase accessibility. By 2028, the adoption of cloud-based imaging platforms is anticipated to improve data sharing and collaboration among healthcare providers by 40%. Companies are also committing to sustainability goals, aiming for a 30% reduction in carbon emissions from manufacturing processes by 2030. For instance, in 2023, a leading imaging system manufacturer achieved a 15% reduction in energy consumption through process optimization. Looking forward, the multipurpose imaging system market is poised to be a cornerstone of resilient, compliant, and sustainable healthcare infrastructure, driven by continuous innovation and strategic investments.

The multipurpose imaging system market is experiencing robust growth, driven by technological advancements and increasing demand for multifunctional diagnostic tools. Key factors influencing the market include the integration of artificial intelligence for enhanced imaging capabilities, the shift towards outpatient diagnostics, and the need for cost-effective healthcare solutions. Additionally, regulatory standards and environmental considerations are shaping product development and manufacturing processes. These dynamics are contributing to the evolution of the market, with a focus on improving patient outcomes and operational efficiencies.

Advancements in artificial intelligence (AI) are significantly enhancing the capabilities of multipurpose imaging systems. AI algorithms are being integrated to improve image quality, automate image analysis, and assist in diagnostic decision-making. This integration leads to faster and more accurate diagnoses, reducing human error and improving patient outcomes. Healthcare providers are increasingly adopting AI-powered imaging systems to enhance efficiency and meet the growing demand for diagnostic services.

Despite technological advancements, the multipurpose imaging system market faces challenges such as high initial investment costs and the need for specialized training. The complexity of integrating new systems with existing healthcare infrastructure can also pose difficulties. Additionally, concerns over data privacy and security, especially with the adoption of cloud-based solutions, may deter some healthcare providers from fully embracing these technologies.

The rising prevalence of chronic diseases such as cardiovascular disorders, diabetes, and cancer is driving the demand for advanced diagnostic imaging solutions. Multipurpose imaging systems offer comprehensive diagnostic capabilities, enabling early detection and monitoring of these conditions. Healthcare providers are investing in these systems to improve patient care and outcomes, presenting significant growth opportunities for the market.

The multipurpose imaging system market is subject to stringent regulatory requirements, including approvals from health authorities like the FDA and EMA. Navigating these regulatory processes can be time-consuming and costly for manufacturers. Additionally, varying regulations across different regions can complicate market entry and expansion strategies for companies operating internationally.

Rise in AI Integration: The integration of artificial intelligence in imaging systems is enhancing diagnostic accuracy and efficiency. AI algorithms are being developed to assist in image analysis, leading to faster and more accurate diagnoses. This trend is gaining traction in both developed and emerging markets.

Shift Towards Outpatient Diagnostics: There is a growing trend towards outpatient diagnostics, driven by the need for cost-effective healthcare solutions. Multipurpose imaging systems are being increasingly adopted in outpatient settings to provide comprehensive diagnostic services.

Development of Portable Imaging Solutions: The demand for portable imaging systems is rising, particularly in remote and underserved areas. Manufacturers are developing compact and lightweight imaging devices to cater to this need, improving accessibility to diagnostic services.

Focus on Sustainable Manufacturing: Environmental considerations are influencing the manufacturing processes of imaging systems. Companies are adopting sustainable practices, such as reducing energy consumption and minimizing waste, to align with global sustainability goals.

The Multipurpose Imaging System Market is segmented across product types, applications, and end-users, providing a comprehensive overview of market dynamics. By type, the market includes systems such as X-ray imaging, ultrasound, MRI, CT scans, and hybrid imaging solutions, each catering to specific diagnostic needs. Applications span hospitals, diagnostic centers, research institutions, and outpatient clinics, reflecting diverse usage patterns and technological adoption. End-users primarily comprise healthcare providers, research laboratories, and specialized diagnostic facilities, with adoption influenced by factors such as operational efficiency, diagnostic accuracy, and workflow integration. Regional preferences and investment trends also play a pivotal role in shaping market segmentation, offering insights for strategic planning.

X-ray imaging currently leads the Multipurpose Imaging System Market, accounting for approximately 35% of adoption due to its widespread use in hospitals, affordability, and ease of integration into clinical workflows. Ultrasound systems follow with 25%, favored for non-invasive diagnostics and prenatal care. MRI and CT scan systems contribute a combined 30%, mainly used in specialized diagnostics and high-resolution imaging requirements. Hybrid imaging systems account for the remaining 10%, providing advanced capabilities for research and complex medical applications.

Hospitals dominate the market application segment, representing approximately 50% of total utilization, driven by the need for comprehensive diagnostic solutions. Diagnostic centers hold 20%, leveraging multipurpose imaging systems for outpatient care. Research institutions account for 15%, primarily using high-resolution imaging for experimental studies. Outpatient clinics contribute 15%, with adoption accelerating due to portable imaging solutions and workflow optimization. In 2024, over 42% of hospitals in the U.S. reported integrating AI-assisted imaging for enhanced diagnostics, improving early detection rates by 18%.

Healthcare providers are the leading end-users of multipurpose imaging systems, accounting for roughly 60% of adoption. Their utilization is driven by operational efficiency, patient throughput optimization, and improved diagnostic accuracy. Research laboratories represent 20%, focusing on innovation and experimental imaging applications. Specialized diagnostic facilities make up 10%, catering to niche medical requirements, while outpatient clinics comprise the remaining 10%, benefitting from portable and cost-effective systems. Consumer adoption trends indicate that 38% of healthcare enterprises globally piloted advanced imaging solutions in 2024. Additionally, 55% of specialized diagnostic centers reported improved workflow efficiency through AI-assisted multipurpose imaging.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2025 and 2032.

North America reported over 12,500 installed multipurpose imaging systems across hospitals and diagnostic centers, with more than 4,200 new installations in 2024 alone. Europe accounted for 28% of global adoption, with Germany, France, and the UK collectively hosting 6,800 systems. Asia-Pacific reached 22% market penetration, with China, India, and Japan contributing to 5,400 units. South America accounted for 7%, primarily Brazil and Argentina, while Middle East & Africa held 5% with notable growth in UAE and South Africa. Rising investments, advanced infrastructure, and regional tech adoption are driving installation density and utilization rates across all regions.

North America holds approximately 38% of the global multipurpose imaging system market by installed volume. Hospitals and diagnostic centers are the primary demand drivers, especially in oncology and cardiology imaging. Regulatory support, such as FDA approvals for AI-enhanced imaging solutions, has accelerated adoption. Technological trends include integration of cloud-based image storage, AI-assisted diagnostics, and tele-radiology platforms. Local player GE Healthcare launched an AI-driven imaging workflow platform in 2024, improving diagnostic throughput by 15% across 120 facilities. Consumer behavior shows higher enterprise adoption in hospitals and specialty clinics, with 42% of facilities prioritizing digital transformation and operational efficiency.

Europe accounts for roughly 28% of the market, with Germany, the UK, and France leading installations. Regulatory bodies such as the European Medicines Agency and sustainability initiatives promote safe, energy-efficient imaging equipment. Emerging technologies include AI-enhanced imaging, robotic-assisted radiology, and hybrid PET/MRI solutions. Siemens Healthineers implemented a cloud-based imaging analytics platform in 2024, optimizing diagnostic workflows in over 80 hospitals. Regional adoption trends reflect regulatory compliance pressure, leading hospitals to prioritize explainable AI and high-precision diagnostics. Consumer behavior favors institutions investing in automation and telemedicine-enabled imaging solutions.

Asia-Pacific accounts for 22% of the installed base, with China, India, and Japan as top-consuming countries. The region benefits from rapid infrastructure development, increasing hospital capacities, and expanding private diagnostic networks. Technological trends include mobile imaging units, AI-assisted diagnostic platforms, and IoT-enabled device integration. Canon Medical Systems launched a compact AI-enabled CT scanner in Japan in 2024, improving throughput by 20%. Consumer behavior varies with higher adoption in urban centers and private hospitals, while tier-2 and tier-3 cities increasingly deploy portable imaging solutions for remote patient care.

South America represents 7% of the global market, with Brazil and Argentina as key contributors. Expansion of hospital infrastructure and modernization of diagnostic centers is fueling demand. Government incentives for healthcare digitization, along with trade policies favoring medical equipment import, support growth. Philips Healthcare launched portable ultrasound units in Brazil in 2024, enhancing diagnostic accessibility across 50 regional clinics. Consumer behavior shows higher adoption in urban hospitals, with a growing preference for integrated diagnostic platforms and mobile imaging services.

The Middle East & Africa hold 5% of the global market, with UAE and South Africa leading installations. Rising demand in oil & gas, construction, and specialized medical facilities is driving system deployment. Technological modernization includes AI-powered imaging and cloud-based PACS integration. Local player Mediclinic UAE implemented an AI-assisted MRI workflow in 2024, reducing scan times by 18%. Consumer behavior reflects selective adoption in urban centers and medical hubs, with emphasis on operational efficiency, advanced diagnostics, and remote consultation capabilities.

United States – 38% Market Share: High healthcare infrastructure investment and strong end-user adoption drive dominance.

Germany – 12% Market Share: Extensive hospital network and regulatory push for advanced imaging solutions ensure leading market position.

The Multipurpose Imaging System Market exhibits a moderately consolidated competitive environment, with over 85 active global players engaged in manufacturing, distribution, and technology innovation. The top five companies—GE Healthcare, Siemens Healthineers, Philips Healthcare, Canon Medical Systems, and Fujifilm Holdings—together control approximately 52% of the global market share, demonstrating strong market positioning and technological leadership. Strategic initiatives such as AI-enabled imaging platforms, cloud-based PACS integration, and advanced CT/MRI hybrid solutions are driving competitive differentiation. In 2024, GE Healthcare launched a next-generation multipurpose CT scanner across 120 hospitals in North America, while Siemens Healthineers introduced an AI-assisted imaging workflow for European diagnostic centers. Partnerships between technology providers and healthcare institutions are increasingly common, with over 30 joint development agreements recorded in 2024 alone. Innovation trends include portable imaging systems, AI-based diagnostic assistance, and automated workflow optimization. Despite the presence of large global players, numerous regional and niche manufacturers contribute approximately 48% of the market, highlighting ongoing opportunities in fragmented regional markets. Overall, competition is shaped by technology adoption, regulatory compliance, and service excellence, positioning leading companies to capture early advantages in emerging applications.

Canon Medical Systems

Fujifilm Holdings

Hitachi Medical Systems

Toshiba Medical Systems

Carestream Health

Hologic Inc.

Shimadzu Corporation

The Multipurpose Imaging System Market is undergoing significant technological transformation driven by advancements in AI, digital integration, and hybrid imaging modalities. Current technologies include AI-assisted radiology, which enables automated anomaly detection, improving diagnostic accuracy by over 20% in pilot studies across Europe and North America. Hybrid imaging systems, combining modalities like PET/CT and MRI/CT, enhance clinical versatility and patient throughput, reducing scan times by 15–18% in multi-center trials. Cloud-based PACS and secure tele-radiology platforms facilitate remote consultations and efficient data management, supporting over 5,000 hospitals globally. Emerging trends include portable imaging units designed for emergency and remote applications, with adoption in over 200 mobile clinics across Asia-Pacific. 3D reconstruction and volumetric imaging software improve surgical planning precision, with reported error reductions of 12–14% in preoperative workflows. Integration of IoT-enabled sensors provides real-time performance analytics, maintenance prediction, and automated quality control. Companies are investing in modular system designs, enabling flexible expansion and rapid deployment in both urban hospitals and rural facilities. Collectively, these technological advancements are enhancing operational efficiency, clinical outcomes, and scalability of multipurpose imaging systems worldwide.

In March 2024, Philips Healthcare launched the IntelliSpace AI imaging platform across 75 hospitals in the UK, enhancing workflow efficiency and reducing diagnostic turnaround times by 18%. Source: www.philips.com

In July 2023, Canon Medical Systems introduced a portable AI-enabled CT scanner in Japan and India, increasing diagnostic accessibility in over 50 regional medical centers. Source: www.canon-medical.com

In October 2024, Siemens Healthineers deployed AI-assisted hybrid PET/MRI systems in 60 European hospitals, improving early detection rates for oncology patients by 22%. Source: www.siemens-healthineers.com

In January 2024, GE Healthcare implemented cloud-based PACS integration for 120 hospitals in North America, reducing image retrieval times by 25% and improving remote diagnostic collaboration. Source: www.gehealthcare.com

The Multipurpose Imaging System Market Report offers a comprehensive assessment of the global landscape, covering diverse product types, applications, end-users, and geographic regions. Product segments analyzed include advanced CT, MRI, hybrid PET/CT, and portable imaging systems, detailing performance capabilities, adoption rates, and clinical utilization. Application insights focus on oncology, cardiology, neurology, and general diagnostic imaging, highlighting adoption patterns across hospitals, diagnostic centers, and research institutions. The report provides in-depth end-user analysis, covering healthcare facilities, private clinics, and academic research laboratories. Regional coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, presenting installation volumes, technological adoption, and local regulatory frameworks.

Additionally, the report examines emerging technologies such as AI-assisted diagnostics, cloud-based PACS, IoT-enabled imaging systems, and modular designs for flexible deployment. Market dynamics, competitive strategies, and innovation trends are discussed, offering actionable intelligence for decision-makers seeking opportunities in installation expansion, technology integration, and regional growth. Niche segments like mobile imaging units and 3D reconstruction platforms are also explored, providing a forward-looking perspective on evolving clinical requirements and market priorities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 150.0 Million |

| Market Revenue (2032) | USD 267.5 Million |

| CAGR (2025–2032) | 7.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | GE Healthcare, Siemens Healthineers, Philips Healthcare, Canon Medical Systems, Fujifilm Holdings, Hitachi Medical Systems, Toshiba Medical Systems, Carestream Health, Hologic Inc., Shimadzu Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |