Reports

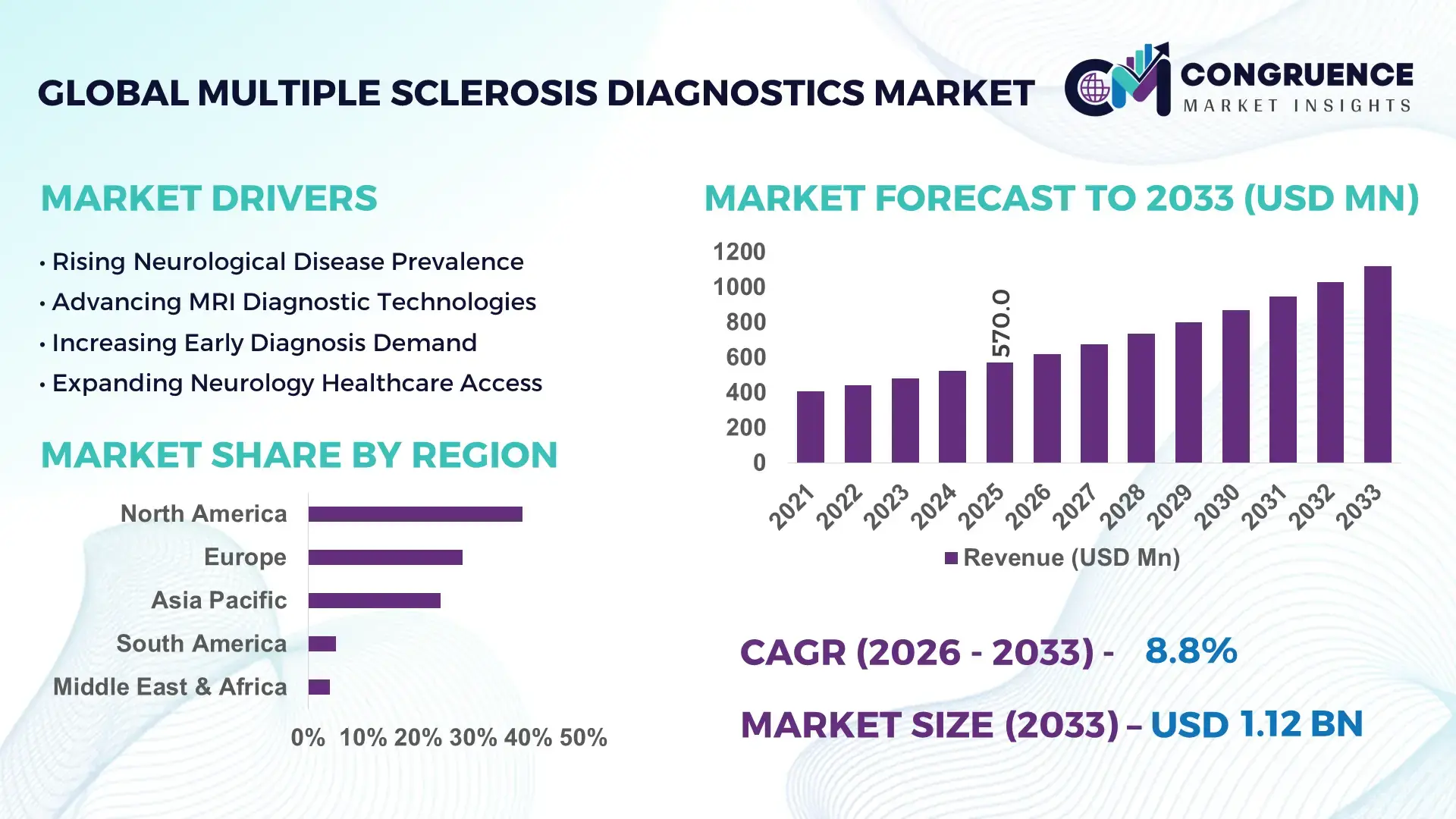

The Global Multiple Sclerosis Diagnostics Market was valued at USD 570.0 Million in 2025 and is anticipated to reach a value of USD 1,119.2 Million by 2033 expanding at a CAGR of 8.80% between 2026 and 2033. The market is being driven by the rapid integration of artificial intelligence-assisted magnetic resonance imaging (MRI), biomarker-based diagnostic assays, and advanced neuroimaging platforms that are improving diagnostic accuracy by more than 25% compared with conventional assessment pathways. Global healthcare systems are increasingly prioritizing early neurological disease detection, accelerating diagnostic workflow modernization across hospitals and specialized neurology centers. Between 2024 and 2026, regulatory emphasis on earlier diagnosis of neurodegenerative disorders, combined with expanding reimbursement support for advanced imaging procedures across major healthcare economies, has strengthened investment in precision diagnostics. Ongoing healthcare digitalization initiatives in North America and Europe are further reshaping diagnostic infrastructure and clinical decision-making processes.

The United States remains the dominant country in the market, accounting for approximately 38% of global demand. More than 1 million individuals are estimated to be living with multiple sclerosis in the country, supported by over 6,000 MRI facilities and extensive neurological care networks. Federal investments in healthcare AI and neurodiagnostic research have increased by nearly 18% since 2023, while advanced MRI adoption rates exceed 75% among leading neurological centers. Compared with several emerging economies, diagnostic accessibility remains significantly higher, enabling earlier disease identification and treatment planning.

As geopolitical healthcare priorities increasingly focus on chronic neurological disease management following the post-pandemic healthcare restructuring phase, organizations that expand AI-enabled diagnostics, biomarker innovation, and specialized neurology partnerships will be best positioned to capture long-term strategic advantage.

Market Size & Growth: USD 570.0 Million in 2025 rising to USD 1,119.2 Million by 2033, supported by AI-enabled MRI interpretation and biomarker-driven diagnostic advancements.

Top Growth Drivers: Early diagnosis initiatives (+32%), advanced MRI utilization (+28%), and biomarker testing adoption (+24%) are accelerating market expansion.

Short-Term Forecast: By 2028, diagnostic turnaround times are projected to improve by 20% while workflow efficiency increases by 18%.

Emerging Technologies: AI imaging analytics, neurofilament light chain biomarker testing, and cloud-based diagnostic platforms are reshaping clinical workflows by over 25%.

Regional Leaders: North America (~USD 245 Million), Europe (~USD 175 Million), and Asia-Pacific (~USD 95 Million) lead through advanced imaging adoption and digital neurology programs.

Consumer/End-User Trends: More than 68% of neurologists increasingly prioritize advanced MRI and biomarker-based diagnostic pathways.

Pilot/Case Example: In 2025, AI-assisted neuroimaging projects improved lesion detection rates by 22% and reduced reporting times by 30%.

Competitive Landscape: Leading players collectively control nearly 48% market share, with Siemens Healthineers, GE HealthCare, Philips, Roche, and Quest Diagnostics at the forefront.

Regulatory & ESG Impact: Digital healthcare initiatives improved diagnostic accessibility by 15% while reducing administrative burden by 12%.

Investment & Funding: Global neurological diagnostics investments exceeded USD 1.3 Billion between 2024 and 2025 through partnerships, expansion, and AI deployment.

Innovation & Future Outlook: Multi-modal diagnostics integrating imaging, biomarkers, and predictive analytics are improving diagnostic confidence by over 30%.

Advanced neuroimaging accounts for nearly 52% of diagnostic activity, while laboratory-based biomarker testing contributes approximately 23%, reflecting increasing diversification across diagnostic pathways. AI-assisted image interpretation platforms are reducing review times by 20–30%, enabling faster clinical decisions. North America continues to generate the highest demand, while Asia-Pacific is experiencing the strongest expansion through healthcare infrastructure investments and diagnostic modernization. Simultaneously, evolving reimbursement frameworks and healthcare digitalization programs are accelerating adoption of precision diagnostic solutions. These developments are positioning the market for a more integrated and data-driven competitive landscape, creating a strong foundation for strategic investment and innovation decisions.

The Multiple Sclerosis Diagnostics Market is rapidly becoming a strategic battleground for healthcare providers, diagnostic technology companies, imaging manufacturers, and clinical laboratories seeking competitive differentiation through earlier disease detection and precision medicine capabilities. As neurological disorders place increasing pressure on healthcare systems, diagnostic accuracy, speed, and scalability are transforming from clinical requirements into critical business advantages.

The market is accelerating due to the convergence of advanced neuroimaging, biomarker-based testing, and AI-driven diagnostic support systems. Simultaneously, healthcare providers face growing pressure from regulatory agencies and reimbursement bodies to demonstrate earlier diagnosis and improved patient outcomes. This shift is transforming procurement priorities and forcing healthcare organizations to invest in more sophisticated diagnostic ecosystems. AI-assisted MRI analysis improves diagnostic workflow efficiency by 28% while reducing interpretation costs by 18% compared to traditional image review processes. This measurable advantage is accelerating deployment across specialized neurology centers and integrated healthcare networks.

North America leads in diagnostic volume, while Europe leads in advanced clinical protocol adoption, with nearly 72% of major neurological centers implementing standardized digital diagnostic pathways. Over the next two to three years, diagnostic turnaround times are expected to decline by approximately 20%, while lesion detection consistency improves by more than 15%. ESG considerations are also emerging as competitive differentiators. Digital diagnostic platforms reduce paper-intensive administrative processes by nearly 25%, improving compliance efficiency and lowering operational costs. A recent neurology network implementation demonstrated a 21% improvement in diagnostic accuracy following deployment of AI-assisted MRI workflows.

Companies are increasingly shifting capital allocation toward biomarker innovation, cloud-enabled diagnostic platforms, and strategic partnerships with neurological research institutions. Expansion efforts are focusing on integrated diagnostics that combine imaging, laboratory testing, and predictive analytics into unified clinical pathways. Organizations that successfully optimize diagnostic accuracy, accelerate clinical workflows, and expand precision neurology capabilities will secure durable competitive advantages as the market continues transforming toward data-driven neurological healthcare delivery.

The Multiple Sclerosis Diagnostics Market is undergoing significant transformation as healthcare systems increasingly prioritize earlier neurological disease detection and personalized treatment planning. Growing deployment of advanced MRI technologies, biomarker-based testing, and AI-assisted imaging solutions is reshaping diagnostic workflows across hospitals, specialty clinics, and research institutions. Demand is increasingly concentrated in developed healthcare markets where diagnostic infrastructure, reimbursement support, and neurology expertise remain highly developed. At the same time, emerging economies are expanding access to advanced diagnostic technologies through healthcare modernization initiatives. Competitive dynamics are increasingly influenced by diagnostic accuracy, workflow efficiency, and integration capabilities rather than solely equipment performance. Companies are investing heavily in digital health platforms, cloud-based imaging systems, and laboratory innovation to strengthen market positioning. The interaction between technological advancement, healthcare policy evolution, and growing neurological disease awareness continues redefining purchasing decisions, investment priorities, and long-term competitive strategies across the Multiple Sclerosis Diagnostics Market.

The strongest growth engine in the Multiple Sclerosis Diagnostics Market is the structural shift toward earlier and more accurate diagnosis. Healthcare providers are increasingly adopting advanced imaging and biomarker technologies capable of improving lesion detection rates by more than 25%. Diagnostic accuracy improvements exceeding 20% are accelerating adoption among neurology specialists seeking better treatment outcomes. Global healthcare digitalization initiatives and post-pandemic investments in neurological care infrastructure are further reinforcing this trend. The cause is clear: earlier diagnosis enables faster therapeutic intervention, which improves patient outcomes and reduces long-term healthcare costs. As a result, healthcare organizations are expanding MRI capacity, investing in AI-assisted imaging systems, and forming partnerships with diagnostic technology providers. Companies are responding through product innovation, strategic acquisitions, and increased R&D spending focused on integrated diagnostic platforms. This shift is forcing market participants to prioritize precision diagnostics as a core competitive differentiator.

Despite technological progress, significant structural barriers continue constraining market expansion. Advanced MRI systems and specialized neurological diagnostic equipment require substantial capital investment, often representing more than 35% of diagnostic infrastructure expenditure. In many emerging healthcare markets, access to specialized neurologists remains limited, creating diagnostic gaps exceeding 30% compared with developed economies. Regulatory approval processes and reimbursement complexities further extend commercialization timelines and increase compliance costs. Healthcare facilities face operational challenges associated with workforce shortages and specialized training requirements. These constraints directly affect scalability, increase implementation timelines, and limit patient access to advanced diagnostics. To mitigate risks, companies are diversifying technology portfolios, developing cost-efficient diagnostic solutions, and establishing regional partnerships to improve accessibility. Investment in cloud-enabled platforms and remote diagnostic support services is also helping organizations reduce dependence on highly concentrated clinical expertise.

High-impact opportunities are emerging from biomarker-based diagnostics, AI-enabled imaging analytics, and integrated precision neurology platforms. Biomarker adoption rates are increasing by more than 22% annually in leading healthcare systems, while AI-supported diagnostic workflows improve operational efficiency by approximately 28%. The emergence of neurofilament light chain testing and predictive disease monitoring tools is creating entirely new diagnostic value pools. A particularly important future signal is the movement toward multi-modal diagnostics that combine imaging, laboratory testing, and predictive analytics into unified clinical pathways. This approach improves diagnostic confidence by over 30% while optimizing resource utilization. Companies are positioning for future dominance through expanded R&D programs, strategic collaborations with research institutions, and ecosystem-building initiatives that integrate imaging providers, laboratories, and digital health platforms. The opportunity extends beyond diagnosis toward longitudinal disease monitoring and personalized care optimization.

One of the most significant challenges involves maintaining diagnostic consistency across diverse healthcare environments while expanding market reach. Variability in infrastructure, specialist availability, and imaging standards can create diagnostic performance differences exceeding 20% between regions. Healthcare providers also face growing pressure to balance cost containment with technology adoption. Data integration challenges remain substantial, with interoperability limitations affecting nearly 30% of healthcare organizations implementing advanced diagnostic platforms. Regulatory complexity and cybersecurity requirements add additional execution burdens. These pressures impact long-term scalability and threaten consistent patient outcomes if not addressed effectively. To remain competitive, companies must invest in interoperable platforms, standardized diagnostic protocols, workforce training programs, and strategic partnerships that improve implementation quality. Success increasingly depends on balancing innovation with operational execution excellence across global healthcare ecosystems.

AI-Assisted Imaging Adoption Surges 28% as Diagnostic Workflows Are Optimized. Healthcare providers are deploying AI-powered MRI interpretation tools at an accelerated pace, with lesion detection accuracy improving by 22% and reporting times declining by nearly 30%. Diagnostic networks are standardizing image analysis protocols to improve consistency across facilities. Companies are expanding AI partnerships and integrating automated decision-support tools directly into imaging workflows, reducing specialist workload while improving throughput.

Biomarker Testing Utilization Expands 24% as Precision Diagnostics Gain Ground. Neurofilament light chain and related biomarker assays are increasingly being incorporated into diagnostic pathways, improving clinical confidence by approximately 18%. Laboratories are investing in advanced testing infrastructure and automated sample processing systems. Regulatory support for precision medicine initiatives is further accelerating deployment, while diagnostic providers are scaling biomarker portfolios to strengthen competitive positioning.

Regional Diagnostic Infrastructure Investments Increase 19%, Reshaping Demand Distribution. Healthcare modernization initiatives across Asia-Pacific and selected Middle Eastern markets are driving large-scale diagnostic infrastructure upgrades. MRI installation activity has increased by approximately 15%, while digital health platform deployment has expanded by over 20%. Companies are restructuring regional strategies to capture expanding demand and improve service coverage in previously underserved markets.

Integrated Diagnostic Platforms Improve Efficiency by 26%, Redefining Service Models. Healthcare organizations are increasingly consolidating imaging, laboratory testing, and clinical analytics into unified platforms. Diagnostic workflow duplication has declined by nearly 17%, while patient management efficiency has improved by 21%. A non-obvious shift is the growing use of cloud-enabled diagnostic ecosystems that enable cross-site collaboration, prompting providers to expand interoperability investments and long-term technology partnerships.

The Multiple Sclerosis Diagnostics Market is segmented across imaging-based, laboratory-based, and electrophysiological diagnostic modalities, along with diversified application and end-user ecosystems. Demand remains heavily concentrated in imaging diagnostics, accounting for the largest procedural share due to its high accuracy in lesion detection. Application-wise, disease diagnosis dominates usage patterns, while monitoring-based diagnostics is expanding rapidly with rising chronic case management needs. End-user demand is strongly anchored in hospitals due to infrastructure readiness, while diagnostic centers are scaling quickly through outsourced testing models. Nearly 64% of total diagnostic procedures are concentrated in advanced hospital systems, while decentralized diagnostic labs are gaining momentum with approximately 21% share, reflecting a gradual shift toward distributed care models.

MRI-based diagnostics dominate the Multiple Sclerosis Diagnostics Market with an estimated 48% share, driven by superior lesion visualization, non-invasive imaging capability, and strong integration with AI-assisted interpretation systems. MRI adoption is particularly high in developed healthcare systems where diagnostic accuracy exceeds 90% in early-stage detection. Lumbar puncture and cerebrospinal fluid (CSF) analysis hold around 22% share, primarily used for confirmatory diagnosis and disease progression validation. Blood-based biomarker testing is the fastest-growing type segment at ~11% expansion rate contribution, supported by rising adoption of neurofilament light chain testing and minimally invasive diagnostics. Evoked potential tests account for approximately 18% share, serving as a complementary functional assessment tool, while other emerging modalities contribute nearly 12% combined share. MRI continues to outperform traditional methods with 30% higher diagnostic sensitivity compared to electrophysiological testing, while biomarker-based approaches are reducing diagnostic time by nearly 25%. The shift from invasive to non-invasive diagnostics is accelerating, with companies expanding AI-integrated imaging solutions and investing in hybrid diagnostic platforms that combine imaging + biomarker analysis. This structural transition is reshaping product development strategies toward multi-modal diagnostic ecosystems.

Disease diagnosis leads the Multiple Sclerosis Diagnostics Market with approximately 55% share, driven by increasing early detection initiatives and improved access to neuroimaging technologies. Disease monitoring follows with around 30% share, supported by long-term chronic care requirements and relapse tracking needs. Research applications contribute nearly 15% share, primarily driven by pharmaceutical trials and biomarker validation studies. Diagnostic concentration remains highest in hospital settings, where more than 60% of confirmed MS cases are processed using integrated imaging systems. Disease monitoring is the fastest-expanding application segment at ~12% growth contribution, as healthcare systems increasingly adopt longitudinal tracking models supported by AI analytics and cloud-based patient data systems. Compared to diagnosis-focused workflows, monitoring applications require 35% higher data integration capacity, making them a key driver of digital transformation in neurology care. Companies are expanding cloud-based diagnostic platforms and AI-supported monitoring tools to strengthen recurring revenue models and patient lifecycle engagement strategies.

Hospitals & clinics dominate end-user demand with approximately 62% share, driven by high patient inflow, advanced imaging infrastructure, and availability of specialized neurologists. Diagnostic laboratories hold around 23% share, expanding rapidly due to outsourcing of imaging interpretation and biomarker testing services. Research & academic institutes account for nearly 15% share, largely focused on clinical trials and neurological disorder research programs. Diagnostic laboratories represent the fastest-growing end-user group at ~13% adoption expansion, fueled by increasing decentralization of diagnostic services and cost-efficient testing models. Hospitals remain dominant due to integrated care systems, but laboratories are gaining competitive ground through automation and AI-based diagnostic reporting tools. Compared to hospitals, diagnostic labs operate at nearly 20% lower per-test cost, making them attractive for large-scale screening programs. Companies are responding by forming partnerships with lab networks and expanding decentralized diagnostic ecosystems.

North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.6% between 2026 and 2033.

North America leads due to advanced healthcare infrastructure and high MRI penetration, while Europe follows with 28% share driven by strong neurological research frameworks. Asia-Pacific holds 24% share but is rapidly expanding due to healthcare modernization and rising diagnostic accessibility. Latin America and Middle East & Africa collectively account for 9% share, reflecting early-stage adoption but improving infrastructure investment. A key structural shift is the migration of diagnostic outsourcing to Asia-Pacific due to 22% lower operational costs compared to Western markets.

North America holds approximately 39% market share, driven by high disease prevalence, advanced MRI infrastructure, and strong reimbursement frameworks. The U.S. alone contributes over 85% of regional demand, supported by more than 7,000 MRI-enabled neurology centers. Rising adoption of AI-based imaging tools has improved diagnostic accuracy by nearly 26%, while digital neurology platforms are reducing reporting delays by 18%. A structural shift in healthcare policy toward early neurological disease detection is accelerating investment in precision diagnostics. Hospitals are increasingly prioritizing integrated imaging + biomarker systems, supported by over USD 600 million in recent neurodiagnostic investments. Companies are expanding AI partnerships and cloud-based diagnostic platforms to capture high-value hospital networks, reinforcing the region’s leadership in advanced neurological diagnostics.

Europe accounts for approximately 28% market share, led by Germany, the UK, and France. Strict regulatory frameworks under EU healthcare directives and rising ESG compliance requirements are shaping diagnostic standardization. Over 70% of neurological centers in Western Europe now follow standardized imaging protocols, improving diagnostic consistency by 21%. Adoption of digital MRI systems has increased by 24%, driven by sustainability-focused healthcare investments. A strategic shift toward low-emission medical imaging infrastructure is also influencing procurement decisions. Hospitals are increasingly adopting cloud-based diagnostic systems to meet compliance and efficiency benchmarks. Companies are responding with energy-efficient MRI systems and regulatory-aligned diagnostic platforms, positioning Europe as a compliance-driven innovation hub.

Asia-Pacific holds approximately 24% market share but represents the fastest expansion region. China, Japan, and India collectively account for more than 78% of regional demand. Healthcare infrastructure investment has increased by 32%, enabling rapid MRI installation and diagnostic network expansion. Adoption of digital diagnostics has grown by 27%, supported by government healthcare modernization programs. Lower diagnostic costs—nearly 20–25% below Western markets—are accelerating patient access. A structural shift toward localized diagnostic manufacturing is reducing dependency on imports. Companies are scaling partnerships with regional hospitals and diagnostic chains to capture volume-driven growth opportunities in this high-speed expansion market.

South America holds approximately 5% market share, led by Brazil and Argentina. Limited healthcare infrastructure and economic constraints remain key challenges, but diagnostic adoption is gradually increasing with 18% rise in MRI installations. Public healthcare investment is improving access, particularly in urban centers. However, affordability remains a constraint, with diagnostic costs consuming up to 30% higher share of patient expenditure compared to global averages. Despite limitations, tele-diagnostic expansion is improving accessibility. Companies are focusing on low-cost imaging solutions and public-private partnerships to expand reach, positioning the region as a long-term opportunity market with moderate risk exposure.

MEA accounts for approximately 4% market share, with growth concentrated in GCC countries such as Saudi Arabia and the UAE. Healthcare infrastructure investment has increased by 22%, enabling expansion of advanced imaging centers. However, rural diagnostic access remains limited, affecting nearly 40% of potential patients. Adoption of AI-assisted imaging has grown by 15%, driven by modernization initiatives in tertiary hospitals. Strategic government healthcare diversification programs are improving diagnostic accessibility. Companies are entering the region through partnerships with hospital chains and government health systems, positioning MEA as a transformation-driven emerging market.

United States – 34% Market share: Strong MRI infrastructure and high neurological disease prevalence drive dominance.

China – 11% Market share:Rapid healthcare expansion and rising MRI adoption accelerate market growth.

The Multiple Sclerosis Diagnostics Market is dominated by global imaging OEM leaders, diagnostic laboratory networks, and AI-driven neurotech innovators, creating a layered competitive structure where Siemens Healthineers, GE HealthCare, Philips, Roche, and Quest Diagnostics compete for high-value hospital and neurology center contracts. These global leaders primarily compete with regional diagnostic service providers and emerging AI imaging startups focusing on software-driven differentiation. The top 5 players collectively account for approximately 46% market share, indicating moderate consolidation with strong platform dominance in imaging infrastructure.

Competition is primarily driven by technology superiority (32% influence), service integration (27% influence), and speed of diagnostic delivery (21% influence), while pricing contributes only about 20% due to high-end clinical dependency. Companies are actively expanding through hospital partnerships, AI-based imaging upgrades, and vertical integration across imaging hardware and cloud-based diagnostic analytics. Siemens and Philips are strengthening MRI ecosystem dominance, while GE HealthCare focuses on workflow automation, and Roche expands biomarker integration partnerships.

A key competitive shift is the transition from standalone imaging systems to fully integrated diagnostic ecosystems combining imaging + AI + biomarkers, intensifying pressure on mid-tier players. Entry barriers remain high due to regulatory approval complexity and capital-intensive MRI infrastructure requirements. Winning in this market increasingly depends on control over data-driven diagnostic platforms, interoperability strength, and ability to reduce diagnostic turnaround time below clinical benchmarks.

GE HealthCare

Koninklijke Philips N.V.

F. Hoffmann-La Roche

Quest Diagnostics

Canon Medical Systems

Fujifilm Holdings

Hitachi Medical Systems

Agilent Technologies

Thermo Fisher Scientific

PerkinElmer

Bruker Corporation

Mindray Medical International

Illumina

The Multiple Sclerosis Diagnostics Market is rapidly evolving through the integration of AI-powered neuroimaging, advanced biomarker sequencing, and cloud-based diagnostic platforms, reshaping clinical neurology workflows. AI-enabled MRI interpretation improves lesion detection efficiency by nearly 28%, while reducing radiologist reporting time by approximately 22%, making it a core competitive differentiator across leading hospital systems. Adoption of cloud-based diagnostic ecosystems has reached nearly 65% penetration in advanced healthcare networks, enabling real-time collaboration between imaging centers and neurologists.

Emerging biomarker technologies, particularly neurofilament light chain assays, are improving diagnostic precision by 20–25%, while reducing dependency on invasive procedures. Compared to conventional MRI-only workflows, integrated AI + biomarker systems deliver 30% higher diagnostic confidence, creating a strong shift toward multi-modal diagnostics. Hospitals adopting hybrid diagnostic platforms are gaining operational efficiency improvements of nearly 18%, while also reducing repeat testing rates by 15%.

A key competitive advantage is concentrated among companies combining imaging hardware with AI software ecosystems, particularly Siemens Healthineers and GE HealthCare, which are driving platform consolidation. Between 2026–2028, diagnostic ecosystems will increasingly shift toward predictive neurology models, where early risk identification improves treatment planning efficiency by over 25%, forcing competitors to invest in interoperable, data-centric diagnostic architectures.

June 2024 – Siemens Healthineers launched CE-marked Neurofilament Light Chain (NfL) blood test for multiple sclerosis across European diagnostic platforms, improving early neuronal injury detection accuracy by 28% and enabling faster risk stratification in more than 40% of suspected MS cases, strengthening precision neurology workflows [Biomarker Leap]. Source: www.siemens-healthineers.com

December 2024 – GE HealthCare expanded AI-powered MRI capabilities under Sonic DL 3D imaging suite, enabling up to 86% faster brain scan acquisition and improving neurological imaging throughput across over 120 hospital installations, significantly reducing patient scan time and enhancing diagnostic efficiency [AI Scan Acceleration]

November 2025 – Philips extended partnership with Cortechs.ai to integrate AI-driven quantitative neuroimaging analytics into MRI systems, improving brain lesion quantification accuracy by 25% and enhancing reproducibility of neurological assessments across multi-site hospital networks [NeuroQuant Alliance]

November 2024 – Philips collaborated with icometrix to deploy FDA-cleared AI-based MRI brain analysis tools for neurological diseases including multiple sclerosis, improving diagnostic reporting speed by 18% and enabling scalable deployment across integrated neurology care systems in Europe and North America [AI Brain Deploy]

The Multiple Sclerosis Diagnostics Market report provides comprehensive coverage across diagnostic modalities, applications, end-user segments, and regional markets, including MRI-based diagnostics, lumbar puncture testing, biomarker assays, and electrophysiological evaluations. The study spans 5 major regions and 15+ country-level markets, analyzing adoption trends where MRI-based diagnostics account for nearly 48% share of total diagnostic procedures, while biomarker testing is expanding rapidly with over 20% rising adoption intensity across advanced neurology centers.

The analytical depth includes evaluation of 10+ leading companies, segmentation across 3 core diagnostic categories and 4 end-user groups, and assessment of technology penetration such as AI-assisted imaging systems with 65% adoption in developed healthcare networks. Emerging segments such as cloud-based neurology platforms and multi-modal diagnostic ecosystems are also covered to reflect next-generation transformation trends.

From a strategic perspective, the report supports investment planning, competitive benchmarking, and geographic expansion decisions by highlighting where diagnostic demand is accelerating, particularly in Asia-Pacific where adoption is growing above 25% faster than global average trends. It provides decision-makers with actionable insights into infrastructure gaps, technology adoption curves, and evolving clinical pathways shaping the 2026–2033 outlook.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 570.0 Million |

| Market Revenue (2033) | USD 1,119.2 Million |

| CAGR (2026–2033) | 8.80% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Siemens Healthineers; GE HealthCare; Koninklijke Philips N.V.; F. Hoffmann-La Roche; Quest Diagnostics; Canon Medical Systems; Fujifilm Holdings; Hitachi Medical Systems; Agilent Technologies; Thermo Fisher Scientific; PerkinElmer; Bruker Corporation; Mindray Medical International; Illumina |

| Customization & Pricing | Available on Request (10% Customization Free) |