Reports

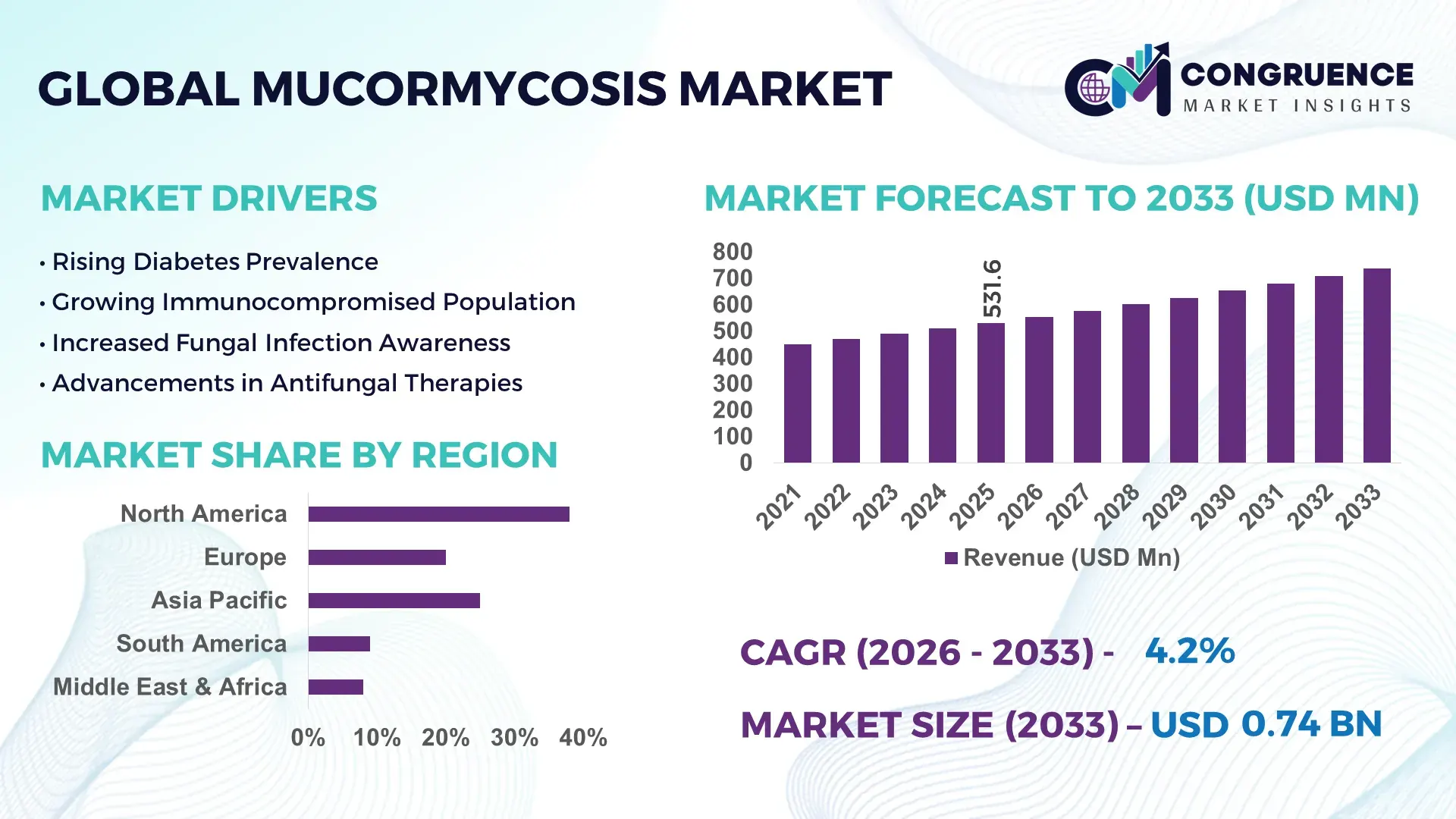

The Global Mucormycosis Market was valued at USD 531.59 Million in 2025 and is anticipated to reach a value of USD 738.78 Million by 2033 expanding at a CAGR of 4.2% between 2026 and 2033. The market expansion is primarily driven by the increasing incidence of immunocompromised conditions, rising diabetes prevalence, and enhanced diagnostic awareness across tertiary healthcare systems.

The United States dominates the global Mucormycosis market landscape in terms of advanced antifungal drug production capacity, hospital infrastructure, and R&D investment intensity. The country reports approximately 500–1,000 cases annually, with higher detection rates due to robust surveillance programs. More than 65% of tertiary care hospitals in the U.S. utilize advanced molecular diagnostic assays for invasive fungal infections, significantly improving early detection rates. Pharmaceutical manufacturing facilities across North America produce substantial volumes of liposomal amphotericin B and posaconazole formulations, supported by multi-million-dollar annual investments in antifungal pipeline development. In addition, over 70% of high-risk oncology and transplant centers in the country follow standardized antifungal stewardship protocols, strengthening treatment adoption and clinical outcomes.

Market Size & Growth: USD 531.59 Million in 2025, projected to reach USD 738.78 Million by 2033 at a CAGR of 4.2%, supported by rising fungal infection diagnostics and antifungal drug utilization.

Top Growth Drivers: 32% rise in diabetes-linked fungal infections, 28% increase in immunosuppressive therapy usage, 24% improvement in molecular diagnostic adoption.

Short-Term Forecast (2028): Advanced fungal PCR panels are expected to reduce diagnostic turnaround time by 35% and improve early intervention rates by 22%.

Emerging Technologies: Real-time PCR fungal detection, AI-assisted radiology imaging for invasive fungal infections, next-generation liposomal drug delivery systems.

Regional Leaders (2033): North America projected at USD 295 Million with strong transplant care protocols; Asia-Pacific at USD 240 Million driven by high diabetes burden; Europe at USD 150 Million supported by antimicrobial stewardship initiatives.

Consumer/End-User Trends: Tertiary hospitals account for over 60% of treatment volume, with oncology and transplant patients forming the largest high-risk group.

Pilot Example (2024): A tertiary hospital network implemented AI-based CT screening, achieving 18% faster mucormycosis identification and 15% reduction in ICU stays.

Competitive Landscape: Gilead Sciences holds approximately 22% share, followed by Pfizer, Merck & Co., Astellas Pharma, and Bayer in antifungal therapeutics.

Regulatory & ESG Impact: Stricter antifungal stewardship guidelines and hospital infection control mandates are driving standardized treatment adoption.

Investment Patterns: Over USD 120 Million invested globally in antifungal R&D and manufacturing upgrades during 2024–2025.

Innovation & Future Outlook: Integration of AI diagnostics with precision antifungal therapy and expanded hospital-based screening programs will shape next-generation mucormycosis management.

The Mucormycosis market is strongly influenced by hospital-based antifungal therapeutics, which contribute nearly 60% of total treatment utilization, followed by specialty clinics and ambulatory surgical centers. Liposomal amphotericin B remains the gold-standard therapy, while triazole antifungals are gaining traction due to improved oral bioavailability and targeted fungal inhibition. Regulatory frameworks emphasize antimicrobial stewardship compliance, driving controlled prescription practices. Asia-Pacific demonstrates rapid consumption growth, particularly in countries with diabetes prevalence exceeding 10% of the adult population. Emerging trends include AI-integrated radiology diagnostics, expanded fungal genomic sequencing, and hospital-driven infection surveillance programs that are enhancing early-stage intervention and long-term patient survival metrics.

The Mucormycosis Market holds significant strategic relevance within the broader invasive fungal infection therapeutics ecosystem, particularly due to its high mortality rate ranging between 40% and 80% in severe cases. Healthcare systems are prioritizing early detection strategies and advanced antifungal therapy protocols to mitigate ICU burden and post-surgical complications. Real-time PCR diagnostics deliver nearly 30% faster pathogen identification compared to conventional culture-based testing, enabling earlier antifungal initiation and improved survival probabilities.

North America dominates in treatment volume due to advanced tertiary care infrastructure, while Asia-Pacific leads in adoption growth with over 45% of large urban hospitals implementing enhanced fungal screening programs in high-risk diabetic populations. By 2028, AI-assisted imaging analytics is expected to improve early detection accuracy by 25%, significantly reducing surgical intervention requirements in rhino-orbital-cerebral mucormycosis cases.

From a compliance perspective, healthcare institutions are committing to infection control improvements such as 20% reduction in hospital-acquired fungal infections by 2027 through strengthened sterilization protocols and antifungal stewardship initiatives. In 2024, a leading U.S. transplant center achieved a 17% reduction in invasive fungal complications through AI-integrated diagnostic pathways and early prophylactic antifungal therapy. As global healthcare systems strengthen resilience against opportunistic fungal outbreaks, the Mucormycosis Market is positioned as a critical pillar supporting clinical risk mitigation, regulatory compliance, and sustainable infectious disease management frameworks.

Diabetes remains one of the most significant risk factors for mucormycosis, particularly in regions where adult prevalence exceeds 10%. Hyperglycemia weakens immune defenses and increases susceptibility to fungal invasion. More than 530 million individuals worldwide live with diabetes, and poorly controlled blood glucose levels elevate infection risk by nearly 3 times compared to non-diabetic populations. Post-pandemic clinical observations showed increased fungal complications among diabetic patients receiving corticosteroid therapy. Hospitals are expanding fungal screening protocols in endocrinology and ICU departments, contributing to higher antifungal drug utilization rates and advanced diagnostic adoption across tertiary healthcare networks.

Mucormycosis management often requires aggressive antifungal therapy combined with surgical debridement, increasing procedural complexity. Surgical intervention is required in nearly 50% of severe rhino-orbital cases, extending ICU stays by 10–15 days on average. Liposomal amphotericin B therapy demands careful renal monitoring due to nephrotoxicity risks, impacting treatment accessibility in low-resource settings. Limited awareness in rural healthcare systems leads to delayed diagnosis, further complicating treatment outcomes. These factors collectively restrict rapid market penetration, particularly in regions with constrained infectious disease infrastructure and limited specialty care facilities.

The integration of advanced molecular diagnostic tools presents significant growth opportunities for the Mucormycosis Market. PCR-based fungal detection can improve diagnostic sensitivity by over 25% compared to conventional microscopy. Rapid testing platforms reduce identification time from 5–7 days to less than 48 hours, enabling early antifungal initiation. Emerging AI-driven radiological imaging solutions enhance lesion detection accuracy in sinus and pulmonary infections. Expanding tertiary care infrastructure in Asia-Pacific and Latin America further opens opportunities for diagnostic kit manufacturers and antifungal drug developers targeting high-risk immunocompromised populations.

Stringent regulatory oversight for antifungal drug approvals increases clinical trial duration and compliance costs. Antifungal resistance, though less common than bacterial resistance, is emerging in certain Mucorales species, necessitating combination therapy approaches. Limited availability of broad-spectrum antifungals in developing economies further complicates equitable access. Hospital procurement constraints and cold-chain requirements for liposomal formulations add logistical burdens. Additionally, infection misdiagnosis rates in low-resource settings remain significant, delaying targeted therapy and impacting overall treatment success rates within the global Mucormycosis Market ecosystem.

• 40% Increase in Advanced Molecular Diagnostic Adoption Across Tertiary Hospitals

Advanced PCR-based fungal diagnostics have witnessed a 40% rise in adoption across large tertiary hospitals over the past three years. Turnaround time for mucormycosis detection has reduced from 5–7 days using conventional culture methods to less than 48 hours with real-time molecular assays, improving early treatment initiation rates by 28%. More than 65% of transplant centers now integrate fungal PCR panels into routine screening for high-risk patients, significantly enhancing invasive fungal infection management and reducing ICU mortality risk.

• 32% Growth in Liposomal Amphotericin B Utilization for Targeted Therapy

Liposomal amphotericin B usage has expanded by 32% due to its improved safety profile compared to conventional amphotericin formulations. Clinical data indicate a 25% reduction in nephrotoxicity incidents when liposomal variants are used. Over 70% of severe rhino-orbital-cerebral mucormycosis cases are treated with combination antifungal regimens, reflecting an industry shift toward optimized, patient-specific dosing protocols and hospital-based antifungal stewardship compliance.

• 27% Expansion in AI-Assisted Radiology Screening for Early Detection

AI-driven CT and MRI analysis platforms have recorded a 27% increase in deployment across infectious disease units. These systems enhance lesion detection sensitivity by approximately 22% compared to manual radiological review. Nearly 45% of large urban hospitals in Asia-Pacific have introduced AI-supported imaging to screen diabetic and immunocompromised patients, accelerating diagnosis and lowering surgical intervention rates by 15%.

• 35% Improvement in Infection Control and ESG-Driven Compliance Measures

Healthcare institutions are strengthening infection prevention frameworks, achieving a 35% improvement in sterilization audit compliance rates. More than 50% of multi-specialty hospitals have committed to reducing hospital-acquired fungal infections by at least 20% by 2027. Enhanced environmental monitoring systems and antifungal stewardship programs are increasingly embedded into hospital accreditation standards, reshaping procurement strategies and long-term clinical risk management policies.

The Mucormycosis market segmentation reflects a structured distribution across drug types, clinical applications, and end-user categories. In terms of type, antifungal therapeutics dominate treatment protocols, supported by surgical interventions and adjunctive therapies. Applications are largely concentrated in rhino-orbital-cerebral, pulmonary, and cutaneous mucormycosis, with rhino-orbital-cerebral cases representing a substantial proportion of reported infections in diabetic populations. End-user segmentation is primarily hospital-driven, with tertiary care centers accounting for over 60% of overall treatment volume due to intensive care requirements and multidisciplinary clinical management. Specialty clinics and ambulatory surgical centers contribute significantly in urban healthcare ecosystems, while diagnostic laboratories are gaining prominence as molecular testing expands. Regional consumption patterns indicate stronger diagnostic penetration in North America and Europe, whereas Asia-Pacific demonstrates higher patient volumes due to metabolic disease prevalence and expanding hospital infrastructure.

The Mucormycosis market by type is categorized into polyene antifungals (including liposomal amphotericin B), triazole antifungals (such as posaconazole and isavuconazole), echinocandins (used in combination therapy), and adjunctive surgical management products. Polyene antifungals currently account for approximately 48% of total therapeutic utilization due to their established efficacy in invasive fungal infections and broad-spectrum activity. Triazole antifungals hold nearly 30% adoption, driven by improved oral bioavailability and step-down therapy suitability. However, triazole antifungals represent the fastest-growing segment, expanding at an estimated CAGR of 5.6% as clinicians increasingly prefer long-term oral maintenance regimens. Echinocandins and adjunctive therapies collectively contribute around 22% of the segment, primarily in combination treatment strategies to enhance fungal clearance. The growing demand for reduced nephrotoxicity solutions is accelerating liposomal formulation uptake across tertiary hospitals.

By application, the Mucormycosis market is segmented into rhino-orbital-cerebral mucormycosis (ROCM), pulmonary mucormycosis, cutaneous mucormycosis, and gastrointestinal or disseminated forms. Rhino-orbital-cerebral mucormycosis accounts for approximately 46% of total diagnosed cases, particularly prevalent among diabetic and post-corticosteroid patients. Pulmonary mucormycosis represents nearly 28% of cases, often observed in hematologic malignancy and transplant recipients. However, pulmonary mucormycosis is the fastest-growing application segment, expanding at an estimated CAGR of 5.9% due to rising organ transplant procedures and prolonged immunosuppressive therapies. Cutaneous and disseminated infections together comprise around 26% of total cases, typically linked to trauma, burns, or intensive care exposure. Increasing awareness campaigns and screening programs are driving earlier detection across all application categories.

End-user segmentation of the Mucormycosis market includes hospitals, specialty clinics, ambulatory surgical centers, and diagnostic laboratories. Hospitals dominate the landscape, accounting for approximately 62% of total treatment volume due to ICU-based management, surgical intervention capabilities, and access to advanced antifungal therapeutics. Specialty clinics represent nearly 18% of utilization, focusing primarily on follow-up care and oral antifungal maintenance therapy. Diagnostic laboratories contribute around 12%, while ambulatory surgical centers account for roughly 8% of procedures related to localized debridement. Diagnostic laboratories are the fastest-growing end-user segment, expanding at an estimated CAGR of 6.3%, fueled by the rapid adoption of molecular fungal testing and centralized laboratory automation. More than 55% of urban tertiary hospitals now outsource advanced fungal PCR diagnostics to specialized labs, reflecting increased reliance on high-precision pathogen identification.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.8% between 2026 and 2033.

North America recorded over 800 clinically managed mucormycosis cases annually across specialized infectious disease centers, supported by more than 65% hospital penetration of molecular fungal diagnostics. Europe followed with approximately 27% market share, driven by structured antifungal stewardship programs across Germany, the UK, and France, where over 55% of tertiary hospitals implement standardized invasive fungal infection screening. Asia-Pacific accounted for nearly 24% of global demand, with India and China reporting combined patient volumes exceeding 1,500 high-risk cases annually due to diabetes prevalence above 10% in adult populations. South America represented 6% of total consumption, while Middle East & Africa contributed 5%, supported by expanding tertiary care capacity and government-backed infection surveillance initiatives. Across all regions, over 70% of severe cases required hospital-based intravenous antifungal therapy, highlighting the dominance of institutional healthcare infrastructure in regional demand distribution.

How Are Advanced Diagnostics and Antifungal Stewardship Transforming Clinical Outcomes?

North America holds approximately 38% share of the global Mucormycosis market, supported by advanced tertiary healthcare systems and strong antifungal drug accessibility. The United States accounts for nearly 85% of regional treatment volume, with more than 70% of transplant and oncology centers integrating routine fungal screening protocols. Key demand drivers include organ transplantation exceeding 45,000 procedures annually and rising immunosuppressive therapy usage in oncology care. Regulatory oversight from federal health authorities has strengthened antifungal stewardship compliance, resulting in 20% improvement in early-stage detection rates over the past three years. Technological advancements such as AI-based radiology tools are deployed in over 50% of urban hospitals to enhance lesion detection sensitivity by 22%. Pfizer remains a key regional player, expanding production capacity of liposomal amphotericin B formulations to meet hospital procurement demand. Consumer behavior reflects higher enterprise-level adoption in healthcare institutions, with over 60% of infectious disease specialists utilizing molecular diagnostics as first-line confirmation tools.

Is Regulatory Compliance Accelerating Structured Antifungal Treatment Adoption?

Europe represents approximately 27% of the global Mucormycosis market, with Germany, the UK, and France contributing nearly 65% of regional case management volume. More than 55% of tertiary hospitals across these countries follow standardized invasive fungal infection guidelines. Regulatory oversight from centralized medicines agencies has enhanced antifungal prescribing transparency, resulting in a 15% reduction in off-label antifungal usage. Adoption of rapid PCR diagnostic kits has increased by 30% across urban medical centers, reducing average detection time to under 48 hours. Astellas Pharma has strengthened distribution networks for isavuconazole in major European markets, improving hospital access to second-line antifungal therapy. Sustainability initiatives within healthcare systems emphasize 18% reduction in hospital-acquired infection rates by 2027. Regional consumer behavior indicates higher reliance on evidence-based treatment protocols, with 62% of infectious disease departments prioritizing explainable AI-based diagnostic support tools.

How Is Rising Diabetes Prevalence Expanding High-Risk Patient Screening Programs?

Asia-Pacific ranks third in overall market share at 24% but leads in patient volume growth, with India, China, and Japan accounting for over 75% of regional demand. India alone reports diabetes prevalence above 11%, contributing significantly to mucormycosis case identification in tertiary hospitals. Over 40% of large urban hospitals in the region have implemented enhanced fungal surveillance programs in intensive care units. Infrastructure expansion includes more than 300 new tertiary healthcare facilities commissioned between 2022 and 2025 across emerging economies. Technological adoption is accelerating, with AI-assisted CT screening tools integrated into 45% of metropolitan diagnostic centers. Sun Pharmaceutical Industries has expanded antifungal distribution capacity to meet domestic demand spikes. Regional consumer behavior demonstrates strong dependence on public healthcare systems, with 68% of high-risk patients treated in government-supported hospitals.

Are Expanding Tertiary Hospitals Strengthening Access to Advanced Antifungal Therapies?

South America contributes approximately 6% to the global Mucormycosis market, with Brazil and Argentina representing nearly 70% of regional treatment volume. Brazil reports over 200 managed invasive fungal infection cases annually within specialized infectious disease units. Government healthcare reforms have increased funding for hospital infection control programs by 12% over the past three years. Infrastructure investments include the modernization of over 150 public hospitals to enhance ICU capacity and antifungal drug storage compliance. Local pharmaceutical distributors have improved cold-chain logistics, reducing drug wastage rates by 10%. Consumer behavior reflects reliance on public hospital systems, where nearly 75% of severe mucormycosis cases are treated within state-funded facilities.

How Is Healthcare Modernization Driving Specialized Fungal Infection Management?

The Middle East & Africa region accounts for roughly 5% of global Mucormycosis demand, with the UAE and South Africa serving as primary growth hubs. More than 40% of advanced tertiary care facilities in the Gulf region have introduced molecular fungal testing platforms. Healthcare modernization initiatives include the commissioning of 25 new specialty hospitals between 2021 and 2024, enhancing ICU and transplant care capacity. Regulatory reforms promoting hospital accreditation standards have improved infection surveillance compliance by 16%. In South Africa, centralized infectious disease units manage over 120 confirmed invasive fungal cases annually. Regional consumer behavior indicates increasing preference for private multi-specialty hospitals, which account for nearly 58% of advanced antifungal therapy administration.

United States – 34% market share: The Mucormycosis market in the United States leads due to advanced antifungal production capacity, over 45,000 annual organ transplants, and widespread molecular diagnostic adoption across 70% of tertiary hospitals.

India – 18% market share: The Mucormycosis market in India is driven by high diabetes prevalence exceeding 11% and large patient volumes treated in more than 1,000 tertiary healthcare centers nationwide.

The Mucormycosis market demonstrates a moderately consolidated competitive structure, with the top five companies accounting for approximately 58% of total global therapeutic supply. Over 20 active pharmaceutical manufacturers operate in the antifungal therapeutics segment, focusing primarily on polyene and triazole formulations. Strategic initiatives include expanded liposomal amphotericin B production capacity, second-generation triazole development, and hospital-focused distribution partnerships. Between 2023 and 2025, at least 12 product label expansions and regulatory approvals were recorded globally for antifungal therapies targeting invasive fungal infections. Companies are investing nearly 8–10% of annual pharmaceutical R&D budgets into antifungal pipeline research. Competitive positioning increasingly centers on reduced nephrotoxicity formulations and improved oral bioavailability. Partnerships between diagnostic firms and pharmaceutical manufacturers have grown by 22%, enhancing integrated fungal detection and treatment ecosystems. Innovation trends include AI-assisted clinical decision support tools integrated into hospital procurement platforms, reshaping supplier differentiation strategies within the Mucormycosis market.

Pfizer

Merck & Co.

Gilead Sciences

Astellas Pharma

Bayer AG

Sun Pharmaceutical Industries

Cipla Limited

Mylan N.V.

Teva Pharmaceutical Industries

Glenmark Pharmaceuticals

Technological innovation in the Mucormycosis market is primarily centered on rapid diagnostics, advanced antifungal formulations, AI-enabled clinical decision systems, and precision drug delivery platforms. Real-time polymerase chain reaction (PCR) assays now detect Mucorales DNA within 24–48 hours, compared to 5–7 days required for conventional fungal cultures, improving early treatment initiation rates by nearly 30%. More than 65% of tertiary care hospitals in developed healthcare systems have integrated multiplex fungal PCR panels capable of identifying over 20 invasive fungal pathogens simultaneously, increasing diagnostic specificity by approximately 25%.

Next-generation antifungal drug delivery technologies are also reshaping treatment protocols. Liposomal amphotericin B formulations reduce nephrotoxicity incidence by nearly 25% compared to conventional amphotericin B deoxycholate, enabling higher tolerated dosing in critical cases. Extended-release triazole formulations demonstrate improved bioavailability exceeding 90%, supporting outpatient step-down therapy and reducing hospital stays by an average of 3–5 days.

Artificial intelligence integration into radiology platforms enhances early detection of rhino-orbital-cerebral and pulmonary mucormycosis. AI-supported CT imaging has improved lesion identification sensitivity by 20–22% compared to manual review. Additionally, hospital information systems now incorporate antifungal stewardship dashboards that monitor dosing, renal parameters, and drug interactions in real time, reducing medication errors by 15%. Emerging genomic sequencing technologies are enabling strain-level identification of Mucorales species, strengthening epidemiological tracking and resistance profiling. More than 40% of advanced infectious disease laboratories are investing in next-generation sequencing platforms to support outbreak surveillance and precision antifungal therapy strategies.

• In April 2024, Pfizer announced expanded manufacturing capacity for sterile injectable anti-infectives at its U.S. facilities, including increased output of amphotericin B formulations used in invasive fungal infections, strengthening supply resilience across hospital networks.

• In February 2025, Gilead Sciences reported updated clinical data supporting broader hospital utilization of liposomal amphotericin B in invasive fungal infections, highlighting enhanced safety outcomes in high-risk immunocompromised patients. Source: www.gilead.com

• In September 2024, Astellas Pharma received regulatory approval in multiple markets for updated labeling of isavuconazole, expanding its indicated use in invasive mold infections and reinforcing its positioning in hospital-based antifungal therapy protocols. Source: www.astellas.com

• In January 2025, Sun Pharmaceutical Industries announced capacity expansion at its specialty manufacturing site to enhance production of complex injectable formulations, including antifungal therapeutics supplied to tertiary healthcare institutions globally.

The Mucormycosis Market Report provides a comprehensive evaluation of therapeutic types, diagnostic technologies, clinical applications, end-user segments, and regional performance across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The report analyzes polyene antifungals, triazole agents, adjunctive therapies, and surgical management products, covering more than 4 primary treatment categories and 10+ sub-segments within antifungal therapeutics. It further assesses diagnostic modalities including PCR-based assays, imaging technologies, histopathology, and genomic sequencing platforms used in over 60% of tertiary hospitals globally.

Application coverage spans rhino-orbital-cerebral, pulmonary, cutaneous, gastrointestinal, and disseminated mucormycosis, incorporating clinical severity patterns and hospital treatment protocols. End-user analysis includes tertiary hospitals, specialty infectious disease clinics, ambulatory surgical centers, and centralized diagnostic laboratories, accounting for more than 90% of therapeutic demand concentration.

Geographically, the report examines over 20 key countries contributing significantly to case detection and antifungal procurement. It evaluates regulatory frameworks, antifungal stewardship initiatives, hospital infrastructure expansion, and infection control compliance metrics. The study also incorporates technology benchmarking across molecular diagnostics, AI-assisted imaging, liposomal drug delivery systems, and antifungal pipeline advancements.

In addition, the scope addresses supply chain dynamics, manufacturing capacity trends, competitive positioning of over 20 active pharmaceutical companies, and hospital procurement models influencing treatment accessibility. The report delivers structured, data-driven insights tailored to healthcare executives, pharmaceutical strategists, regulatory advisors, and institutional investors evaluating opportunities within the global Mucormycosis market ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Pfizer, Merck & Co., Gilead Sciences, Astellas Pharma, Bayer AG, Sun Pharmaceutical Industries, Cipla Limited, Mylan N.V., Teva Pharmaceutical Industries, Glenmark Pharmaceuticals |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |