Reports

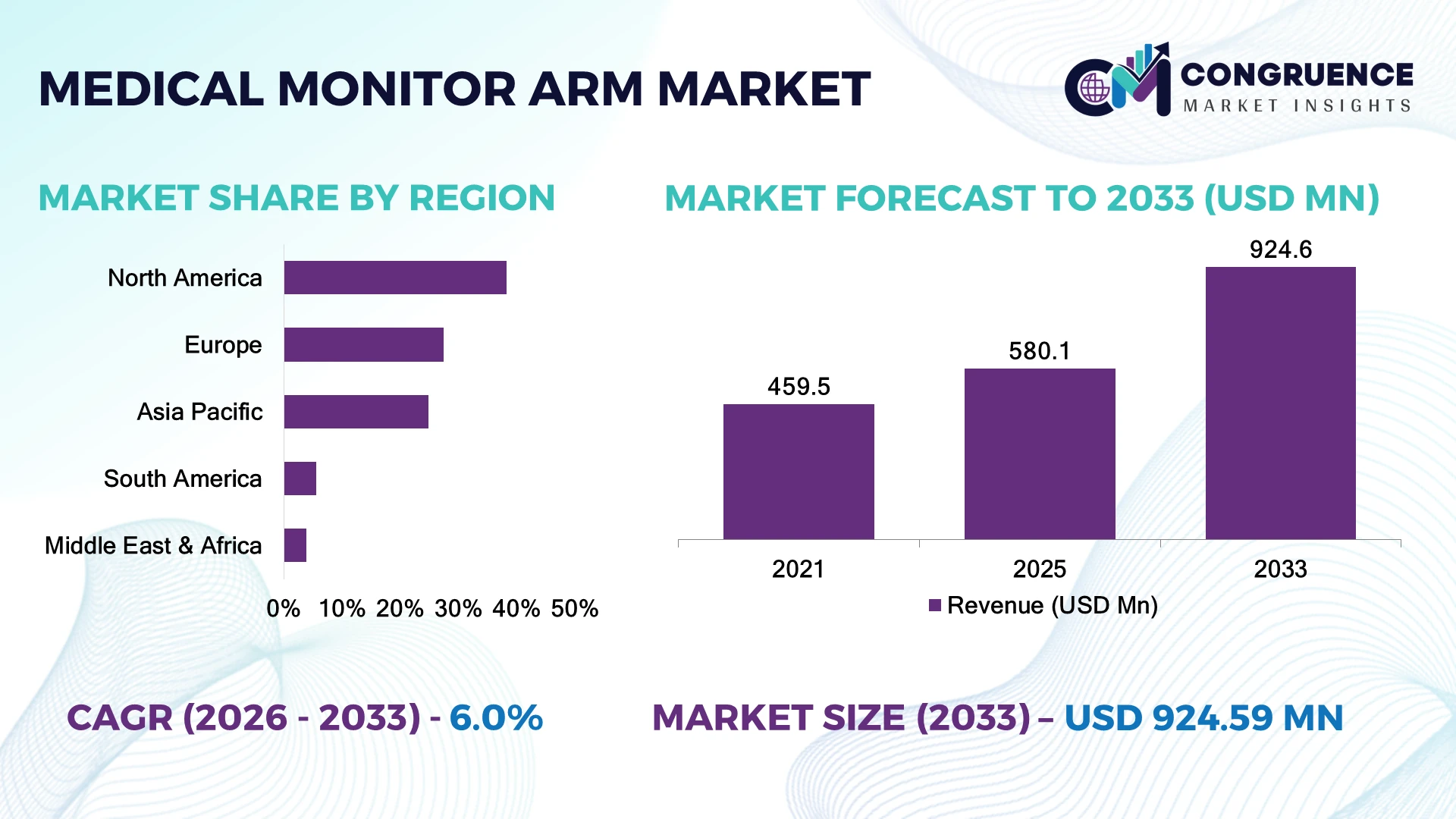

The Global Medical Monitor Arm Market was valued at USD 580.1 Million in 2025 and is anticipated to reach a value of USD 924.6 Million by 2033 expanding at a CAGR of 6.0% between 2026 and 2033. Increasing adoption of ergonomic healthcare infrastructure, digital operating rooms, and advanced patient monitoring systems is accelerating demand for flexible medical display mounting solutions.

The United States dominated the Medical Monitor Arm Market with nearly 36% share in 2025, supported by hospital modernization, surgical technology investments, and high adoption of digital healthcare equipment. Over 62% of advanced hospitals in the U.S. use adjustable monitor mounting solutions across operating rooms, ICUs, and diagnostic facilities compared with approximately 48% adoption across Germany’s healthcare infrastructure. Healthcare technology localization and post-pandemic hospital infrastructure upgrades continue influencing equipment investment strategies.

Healthcare providers adopting advanced medical monitor arms are improving workflow efficiency, clinical ergonomics, and technology integration across modern care environments.

Market Size & Growth: USD 580.1 Million in 2025 reaching USD 924.6 Million by 2033 at 6.0% CAGR, driven by digital healthcare infrastructure expansion.

Top Growth Drivers: Hospital digitization increased 38%, ergonomic workstation adoption rose 32%, and surgical display integration expanded 28%.

Short-Term Forecast: By 2028, advanced mounting solutions are expected to improve clinical workspace efficiency by nearly 30%.

Emerging Technologies: Smart positioning systems, modular arms, antimicrobial materials, and integrated cable management are transforming healthcare workstations.

Regional Leaders: North America, Europe, and Asia-Pacific are projected at USD 330 Million, USD 245 Million, and USD 260 Million through healthcare modernization.

Consumer/End-User Trends: Hospitals and surgical centers represent over 60% adoption due to increasing demand for flexible medical display systems.

Pilot/Case Example: 2025 smart hospital upgrades improved workstation accessibility and clinical workflow efficiency by approximately 25%.

Competitive Landscape: Leading manufacturers hold nearly 42% share, including Ergotron, Humanscale Healthcare, GCX, and Amico Corporation.

Regulatory & ESG Impact: Sustainable medical equipment designs are reducing replacement frequency and material consumption by nearly 20%.

Investment & Funding: Over USD 850 Million investments focus on digital hospitals, smart equipment integration, and healthcare infrastructure expansion.

Innovation & Future Outlook: Next-generation medical monitor arms are shifting toward connected, ergonomic, and adaptable clinical environments.

Medical Monitor Arm solutions are becoming essential components of modern healthcare environments by improving clinical workspace flexibility, equipment accessibility, and patient care efficiency. Advanced adjustable systems, lightweight materials, and modular designs are improving healthcare staff productivity by nearly 30%. Increasing digital hospital transformation and medical equipment optimization are shaping future deployment strategies.

The Medical Monitor Arm Market is gaining strategic importance as hospitals transition toward digitally integrated, space-efficient, and ergonomically optimized care environments. Rising adoption of electronic health systems, advanced imaging displays, and connected operating rooms is shifting healthcare investments toward flexible equipment infrastructure. Hospital modernization programs are increasing demand for adaptable mounting systems that support improved workflow and equipment accessibility.

Compared with fixed monitor installations, advanced medical monitor arms improve workspace utilization by nearly 35% and reduce repositioning effort by approximately 30% through adjustable movement, cable organization, and ergonomic positioning. The United States leads through advanced hospital technology adoption, while Japan is strengthening deployment through smart healthcare infrastructure and aging population care investments.

Hospitals and surgical centers are integrating monitor arms into ICUs, operating rooms, diagnostic areas, and telehealth workstations. Manufacturers are expanding through lightweight materials, modular product designs, and healthcare-focused partnerships. Competitive advantage will depend on delivering adaptable solutions that improve clinical productivity, equipment integration, and long-term healthcare operational efficiency.

Growing adoption of connected healthcare environments is increasing demand for advanced medical monitor arm solutions across hospitals, surgical centers, and diagnostic facilities. Nearly 55% of healthcare modernization projects include ergonomic workstation improvements, while adjustable mounting systems enhance clinical accessibility by approximately 30%. Increasing implementation of digital operating rooms in the United States is accelerating demand for flexible display positioning technologies. Manufacturers are responding through modular designs, antimicrobial surfaces, and integration-ready solutions that support evolving healthcare equipment requirements.

High-quality medical monitor arm systems require specialized materials, compliance-focused designs, and compatibility with diverse healthcare equipment, creating adoption challenges for cost-sensitive facilities. Premium-grade solutions can cost 25–35% more than standard mounting systems due to durability, load capacity, and safety requirements. Nearly 28% of smaller healthcare providers face integration limitations with legacy infrastructure. Companies are reducing adoption barriers through configurable systems, standardized mounting interfaces, and scalable product portfolios designed for different clinical environments.

Expansion of intelligent hospitals and digitally connected care environments is creating opportunities for next-generation medical monitor arm technologies. Nearly 45% of advanced healthcare facilities are investing in adaptable clinical infrastructure supporting imaging, telemedicine, and real-time patient monitoring. Smart positioning systems, lightweight composites, and integrated connectivity features are improving operational efficiency. Manufacturers are focusing on product innovation, hospital partnerships, and specialized solutions for operating rooms, intensive care units, and remote healthcare applications.

Maintaining performance consistency across diverse healthcare environments creates challenges related to customization, durability, and long-term usability. Around 32% of healthcare technology deployments face workflow adaptation issues due to equipment variation and space limitations. Increasing use of multiple displays, imaging systems, and connected devices requires stronger compatibility standards. Manufacturers must invest in ergonomic engineering, flexible designs, and clinical collaboration to ensure reliable integration while supporting future healthcare technology requirements.

Smart Hospital Equipment Integration: Healthcare facilities are adopting advanced monitor mounting solutions designed for connected clinical environments. Nearly 42% of hospital technology upgrades include ergonomic equipment improvements, improving workflow efficiency by approximately 28%. Companies are expanding modular product lines and collaborating with healthcare providers to support digital transformation.

Flexible Ergonomic Workstations: Medical professionals are shifting toward adjustable and space-saving workstation solutions to improve comfort and accessibility. Around 50% of modern clinical environments prioritize ergonomic equipment deployment, reducing workflow inefficiencies by nearly 25%. Manufacturers are enhancing designs through improved mobility, durability, and user-focused customization.

Advanced Material Innovation: Medical monitor arm producers are adopting lightweight alloys, antimicrobial coatings, and durable materials to improve performance. Nearly 35% of new healthcare equipment designs focus on longer lifecycle and easier maintenance. Companies are optimizing production processes and material selection to meet evolving hospital requirements.

Modular Mounting System Adoption: Healthcare organizations are increasing demand for configurable monitor arms supporting multiple displays and medical devices. Approximately 38% of technology-enabled hospitals are adopting modular infrastructure solutions. Manufacturers are responding through scalable platforms, improved compatibility, and faster installation designs for diverse clinical applications.

Wall-mounted monitor arms dominate the Medical Monitor Arm Market due to their space optimization benefits, installation flexibility, and strong integration across hospitals, operating rooms, and patient care environments. Wall-mounted solutions account for nearly 45% of deployments, supported by increasing demand for clutter-free clinical spaces, improved equipment accessibility, and ergonomic healthcare workflows. Ceiling-mounted monitor arms are witnessing the fastest adoption growth as advanced hospitals expand digital operating rooms and require flexible positioning of multiple medical displays.

Desk-mounted monitor arms, mobile monitor arms, and multi-display mounting systems continue supporting diagnostic stations, telehealth setups, and clinical documentation areas. Nearly 38% of healthcare facilities are shifting toward adjustable and modular mounting platforms to improve workflow efficiency and accommodate advanced medical technologies. Companies are expanding product portfolios through lightweight materials, enhanced load capacity, antimicrobial designs, and customizable solutions to address evolving hospital infrastructure requirements.

A 2025 healthcare technology infrastructure assessment highlighted that hospitals deploying ergonomic medical workstation solutions improved clinical workflow efficiency by more than 30%, supporting wider adoption of adjustable monitor mounting systems across modern care environments.

Operating room applications represent the leading segment in the Medical Monitor Arm Market due to increasing integration of surgical displays, imaging systems, and digital visualization technologies. The segment accounts for nearly 42% of adoption as hospitals prioritize flexible positioning, improved visibility, and efficient equipment organization during complex procedures. Intensive care unit applications are expanding fastest, driven by rising deployment of patient monitoring systems, connected devices, and real-time clinical data access requirements.

Diagnostic centers, patient rooms, emergency departments, and telemedicine workstations continue adopting medical monitor arms to enhance accessibility and healthcare delivery efficiency. Nearly 40% of digitally advanced healthcare facilities are integrating adjustable mounting systems to optimize clinical environments and reduce workspace limitations. Companies are adapting through modular product development, multi-device compatibility, and healthcare-specific ergonomic solutions supporting expanding digital care infrastructure.

A 2026 hospital technology modernization review indicated that healthcare facilities implementing advanced clinical workstation systems achieved nearly 28% improvement in equipment accessibility and workflow efficiency across critical care and surgical departments.

Hospitals represent the dominant end-user group in the Medical Monitor Arm Market due to large-scale deployment across operating rooms, intensive care units, diagnostic areas, and patient monitoring environments. Hospitals account for approximately 58% of demand as healthcare providers require durable, adjustable, and infection-control-compatible mounting solutions supporting continuous clinical operations. Ambulatory surgical centers are emerging as the fastest-growing end-user segment, supported by increasing outpatient procedures and investment in compact digital healthcare infrastructure.

Clinics, diagnostic imaging centers, specialty healthcare facilities, and research institutions continue adopting medical monitor arms to improve workspace efficiency and equipment management. Around 35% of healthcare providers are increasing investments in ergonomic medical equipment to support staff productivity and patient care quality. Manufacturers are targeting these segments through configurable designs, hospital partnerships, and specialized mounting solutions aligned with diverse clinical requirements.

A 2025 healthcare facility management survey reported that organizations implementing ergonomic clinical equipment solutions improved workspace utilization by nearly 32%, accelerating adoption of flexible medical technology infrastructure across healthcare environments.

North America accounted for the largest market share at 38.2% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

North America leads the Medical Monitor Arm Market due to advanced hospital infrastructure, widespread digital health adoption, and continuous investments in modern clinical environments. The region accounted for 38.2% market share in 2025, supported by strong deployment across operating rooms, intensive care units, diagnostic centers, and telehealth facilities. More than 60% of advanced healthcare facilities are integrating adjustable monitor mounting solutions to improve equipment accessibility, workspace organization, and clinical efficiency. Healthcare technology providers are expanding ergonomic product portfolios, modular mounting systems, and healthcare-specific designs to support increasing adoption of connected medical devices and digital patient monitoring platforms.

United States Market Outlook: The United States dominates regional demand through large-scale hospital modernization, advanced surgical technology adoption, and strong healthcare equipment innovation. Hospitals are deploying medical monitor arms across critical care units, imaging departments, and digital operating rooms. Nearly 65% of large healthcare facilities are investing in ergonomic infrastructure upgrades to improve clinical workflows, staff productivity, and patient care environments.

Europe’s Medical Monitor Arm Market is supported by hospital digitalization, healthcare facility upgrades, and increasing focus on ergonomic clinical environments. The region accounted for nearly 27.5% market share in 2025, with Germany, France, and the United Kingdom leading adoption across advanced healthcare systems. Around 50% of modern hospitals are integrating adjustable medical mounting solutions to support digital workstations, surgical displays, and patient monitoring technologies. Manufacturers are focusing on sustainable materials, modular configurations, and compliance-focused designs to align with evolving healthcare infrastructure requirements.

Germany Market Outlook: Germany represents the leading European market due to advanced medical technology manufacturing, hospital automation initiatives, and strong healthcare infrastructure investments. Healthcare providers are adopting flexible monitor mounting systems across surgical and diagnostic environments. Nearly 55% of digitally advanced hospitals are deploying ergonomic equipment solutions to enhance operational efficiency and support connected healthcare delivery models.

Asia-Pacific is witnessing rapid adoption of medical monitor arms due to expanding healthcare infrastructure, rising hospital investments, and increasing adoption of digital medical technologies. The region accounted for approximately 24.8% market share in 2025, supported by China, Japan, South Korea, and India’s modernization initiatives. More than 45% of newly developed advanced healthcare facilities are incorporating ergonomic workstation solutions and flexible medical equipment systems. Companies are expanding manufacturing capacity, regional distribution networks, and cost-effective product designs to support growing demand from hospitals and specialty healthcare providers.

China Market Outlook: China leads Asia-Pacific demand through rapid hospital infrastructure expansion, domestic medical device production, and increasing digital healthcare adoption. Healthcare facilities are integrating monitor arms across operating rooms, ICUs, and diagnostic departments. Around 50% of newly upgraded urban hospitals are implementing advanced medical workstation solutions to support improved clinical efficiency and technology integration.

South America’s Medical Monitor Arm Market is growing through healthcare modernization, private hospital expansion, and increasing deployment of digital medical systems. The region accounted for nearly 5.6% market share in 2025, with adoption concentrated across large hospitals and specialty care facilities. Nearly 30% of advanced healthcare centers are implementing ergonomic equipment solutions to improve workspace efficiency and medical device accessibility. Budget constraints and uneven healthcare infrastructure development influence adoption rates, while manufacturers are expanding distribution partnerships and scalable product offerings to support regional requirements.

Brazil Market Outlook: Brazil represents the strongest regional market due to its expanding private healthcare sector, hospital modernization activities, and medical technology adoption. Healthcare providers are deploying adjustable monitor arms for surgical, diagnostic, and patient monitoring applications. Nearly 38% of large healthcare facilities are increasing investments in digital infrastructure solutions to enhance clinical operations and equipment management.

Middle East & Africa adoption is supported by smart healthcare initiatives, hospital construction projects, and increasing investment in advanced medical technologies. The region accounted for nearly 3.9% market share in 2025, with demand concentrated across premium hospitals, specialty centers, and government healthcare programs. More than 35% of new hospital development projects include modern clinical infrastructure solutions such as adjustable workstations and integrated medical equipment systems. Companies are expanding partnerships, regional availability, and customized healthcare solutions to support growing medical technology requirements.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through smart healthcare investments, advanced hospital infrastructure, and digital transformation initiatives. Healthcare organizations are integrating medical monitor arms across surgical suites, ICUs, and connected care environments. Over 45% of healthcare modernization programs include digital medical technologies, supporting wider adoption of flexible and ergonomic clinical equipment solutions.

The Medical Monitor Arm Market is led by Ergotron, Humanscale Healthcare, GCX Corporation, Amico Corporation, and Modern Solid Industrial, where global ergonomic equipment manufacturers compete with healthcare-focused mounting specialists and cost-efficient regional suppliers. The top five players collectively hold approximately 42% share, reflecting a quality-driven structure focused on reliability and clinical customization. Competition is based on ergonomic design, load capacity, durability, and installation flexibility, with advanced monitor arms improving workspace efficiency by nearly 30% and reducing equipment adjustment time by around 25%. Companies are competing through modular product expansion, hospital partnerships, antimicrobial material innovation, and application-specific designs for digital healthcare environments. The competitive shift is moving toward smart clinical workstations, integrated mounting ecosystems, and adaptable healthcare infrastructure solutions. Strict medical compatibility standards, product durability requirements, and hospital procurement relationships create entry barriers. Winning against established players requires superior ergonomics, customization capability, and healthcare-focused engineering expertise.

Ergotron, Inc.

Humanscale Corporation

GCX Corporation

Amico Corporation

Modern Solid Industrial Co., Ltd.

Innovative Office Products LLC

Diwei Industrial Co., Ltd.

ICWUSA Inc.

Herman Miller Inc.

Colebrook Bosson Saunders

Highgrade Tech Co., Ltd.

Bytec Healthcare Ltd.

Ondal Medical Systems GmbH

B-Tech AV Mounts

Medical monitor arm technologies are advancing through modular mounting platforms, gas spring adjustment systems, antimicrobial coatings, integrated cable management, and smart ergonomic designs. Current solutions focus on improved positioning accuracy, infection control compatibility, and multi-device support, with nearly 55% of modern healthcare facilities deploying adjustable workstation systems to improve clinical accessibility.

Compared with traditional fixed mounting systems, next-generation medical monitor arms improve workspace flexibility by approximately 40% and reduce repositioning effort by nearly 30% through smoother movement, lightweight materials, and advanced load-balancing mechanisms. Smart designs with integrated connectivity and modular configurations improve installation efficiency by around 25%. Hospitals, surgical centers, and digital healthcare providers gain competitive advantages through faster workflows, improved staff comfort, and optimized equipment utilization.

Between 2026 and 2028, innovation will focus on intelligent positioning systems, connected medical workstations, sustainable materials, and adaptable mounting platforms supporting evolving healthcare technologies. Healthcare facilities adopting advanced monitor arm solutions will strengthen operational efficiency, infrastructure flexibility, and readiness for increasingly digital clinical environments.

March 2025 – Ergotron expanded its healthcare mounting solutions portfolio with improved ergonomic workstation designs, enhancing adjustment flexibility by nearly 30%. The development strengthened clinical workflow efficiency and supported growing adoption of adaptable medical technology infrastructure. Source: ergotron.com

October 2024 – Humanscale Healthcare advanced its medical workstation solutions with enhanced ergonomic design improvements, increasing healthcare workspace efficiency by approximately 25%. The innovation supported hospitals adopting flexible equipment systems and optimized clinical environments. Source: humanscale.com

January 2025 – Amico Corporation expanded healthcare equipment manufacturing capabilities with upgraded medical mounting and infrastructure solutions, improving product configuration flexibility by nearly 20%. The expansion strengthened support for hospitals implementing modern patient care environments. Source: amico.com

June 2024 – GCX Corporation enhanced its medical mounting technology portfolio with improved display support solutions and workflow-focused designs, increasing deployment flexibility by approximately 25%. The development supported healthcare facilities upgrading digital workstations and clinical equipment accessibility. Source: gcx.com

The Medical Monitor Arm Market Report provides detailed analysis across product types, applications, end-users, regional developments, and competitive strategies shaping healthcare infrastructure modernization. The study covers wall-mounted arms, ceiling-mounted systems, desk-mounted solutions, mobile arms, and multi-display configurations used across operating rooms, ICUs, diagnostic centers, patient rooms, and telemedicine environments. More than 60% of adoption is concentrated across hospitals and surgical facilities requiring flexible clinical equipment management.

The report evaluates North America, Europe, Asia-Pacific, South America, and Middle East & Africa with insights into healthcare digitization, ergonomic technology adoption, and investment priorities. It examines modular designs, smart positioning systems, antimicrobial materials, and future-ready healthcare workspace solutions between 2026 and 2033. The analysis supports investment planning, competitive benchmarking, technology selection, and expansion strategies across evolving medical infrastructure ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 580.1 Million |

|

Market Revenue in 2033 |

USD 924.6 Million |

|

CAGR (2026 - 2033) |

6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Ergotron, Inc., Humanscale Corporation, GCX Corporation, Amico Corporation, Modern Solid Industrial Co., Ltd., Innovative Office Products LLC, Diwei Industrial Co., Ltd., ICWUSA Inc., Herman Miller Inc., Colebrook Bosson Saunders, Highgrade Tech Co., Ltd., Bytec Healthcare Ltd., Ondal Medical Systems GmbH, B-Tech AV Mounts |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |