Reports

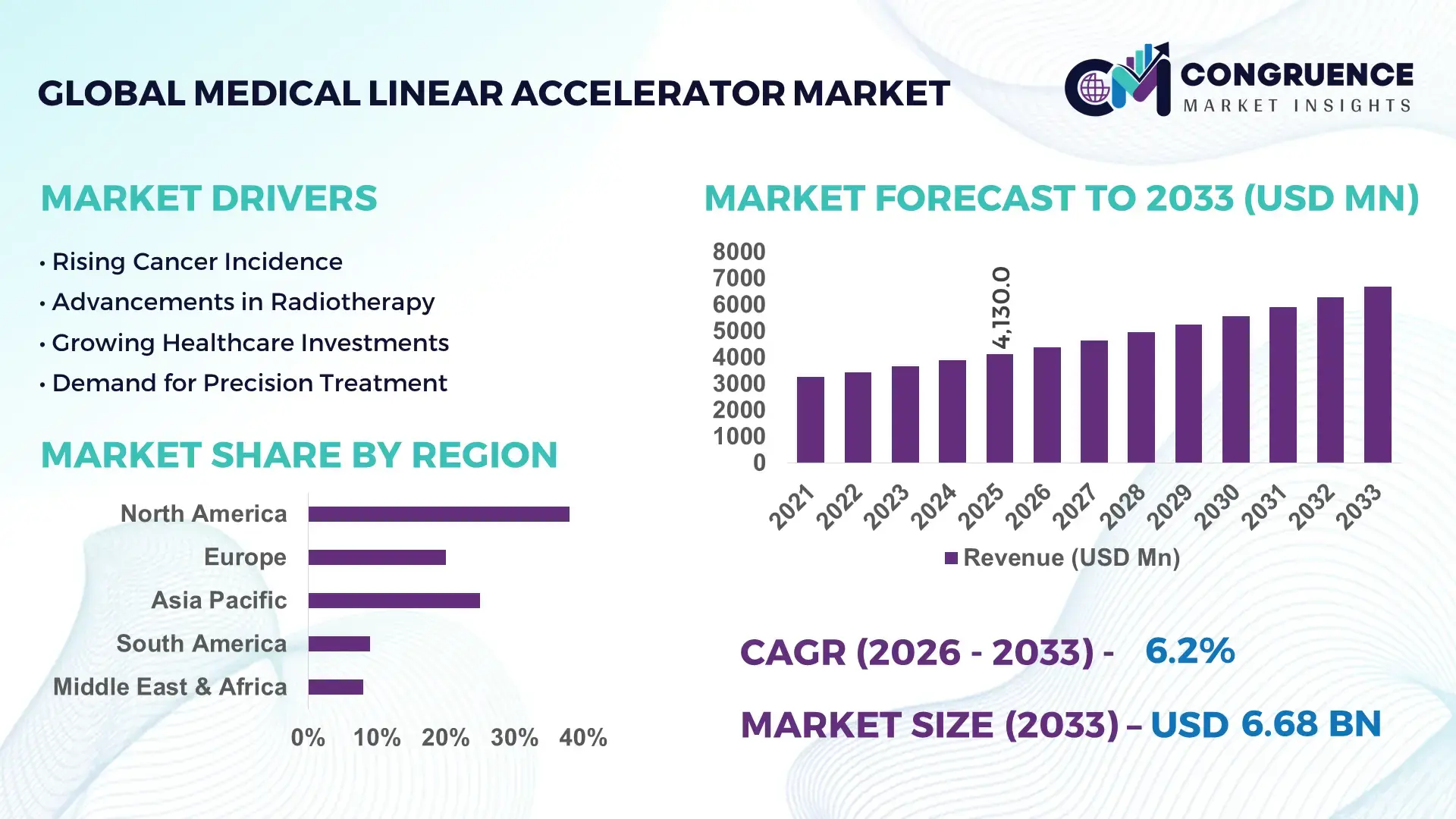

The Global Medical Linear Accelerator Market was valued at USD 4130 Million in 2025 and is anticipated to reach a value of USD 6677.57 Million by 2033 expanding at a CAGR of 6.19% between 2026 and 2033. Rapid integration of AI-assisted adaptive radiotherapy, image-guided treatment systems, and high-precision oncology workflows is accelerating replacement cycles, with treatment accuracy improving by over 30% compared to conventional radiotherapy platforms while reducing session planning time by nearly 25%.

The United States dominates the global medical linear accelerator market with nearly 38% share, supported by large-scale oncology infrastructure investments exceeding USD 2.5 billion annually across hospital networks and cancer centers. More than 72% of advanced radiation oncology facilities in the country operate image-guided or adaptive radiotherapy-enabled LINAC systems, compared with below 45% adoption in several emerging markets. The country also benefits from strong integration between oncology software developers, precision imaging providers, and accelerator manufacturers, enabling faster deployment of next-generation systems. China follows with aggressive localization initiatives and double-digit installation growth, while Germany maintains leadership in high-efficiency treatment planning integration across public healthcare institutions.

Market Size & Growth: Global market reached USD 4130 million in 2025 and advances toward USD 6677.57 million by 2033, driven by AI-enabled adaptive radiotherapy and precision oncology expansion at 6.19% CAGR.

Top Growth Drivers: Cancer incidence growth contributes 34%, AI-based treatment planning 28%, and hospital radiation infrastructure modernization 22% to new procurement demand.

Short-Term Forecast: By 2027, automated treatment workflow integration reduces planning time by 25% and improves patient throughput efficiency by 18%.

Emerging Technologies: AI-guided contouring, adaptive radiotherapy, and cloud-connected oncology imaging platforms achieve adoption rates above 60% in advanced cancer centers.

Regional Leaders: North America exceeds USD 2.4 billion with strong adaptive therapy deployment, Asia-Pacific crosses USD 1.8 billion through hospital expansion, while Europe advances precision oncology installations across public healthcare systems.

Consumer/End-User Trends: More than 68% of tertiary hospitals prioritize compact high-energy LINAC systems supporting faster treatment cycles and lower operational downtime.

Pilot/Case Example: In 2025, multi-site oncology deployment programs improved radiation targeting precision by 31% while reducing repeat imaging procedures by 19%.

Competitive Landscape: Leading manufacturers control nearly 57% combined market share, with competition centered on AI integration, software ecosystems, and service network expansion.

Regulatory & ESG Impact: Updated radiation safety standards improved treatment monitoring compliance by 24%, while energy-efficient systems lowered operational power consumption by 15%.

Investment & Funding: Global oncology infrastructure investments surpassed USD 4 billion in 2025, fueled by hospital partnerships, regional manufacturing expansion, and supply-chain localization initiatives.

Innovation & Future Outlook: MRI-guided radiotherapy, autonomous treatment calibration, and digital twin-based oncology planning are reshaping next-generation high-growth radiation treatment strategies.

Hospital-based oncology treatment centers account for nearly 52% of total medical linear accelerator deployments, followed by specialized cancer institutes at 31%, reflecting the rising concentration of advanced radiation therapy services in integrated healthcare networks. AI-assisted adaptive radiotherapy systems improved treatment workflow efficiency by 27% during 2025–2026, while compact high-energy LINAC platforms reduced maintenance downtime by 18%. North America leads premium system adoption, whereas Asia-Pacific records the fastest installation expansion due to large-scale oncology infrastructure upgrades and domestic manufacturing support programs. Increasing regulatory emphasis on precision treatment validation and localized component sourcing is accelerating investment in software-integrated radiotherapy ecosystems, setting the stage for deeper strategic competition across high-growth oncology markets.

The medical linear accelerator market is rapidly transforming into a strategic battleground for oncology technology leadership as healthcare systems prioritize precision cancer treatment capacity, workflow optimization, and long-term operational efficiency. Rising cancer treatment volumes, aging populations, and hospital digitization programs are accelerating procurement cycles across advanced and emerging healthcare economies. Regulatory tightening around radiation accuracy and treatment traceability is also shifting competition toward software-integrated, AI-enabled radiotherapy ecosystems. Adaptive radiotherapy platforms now command over 41% of new installations in high-capacity cancer centers, reflecting the market’s transition from hardware-focused procurement toward intelligent treatment infrastructure.

AI-assisted adaptive radiotherapy improves treatment planning efficiency by 32% while reducing operational costs by 21% compared to legacy fixed-protocol systems. North America leads in installation volume, while Western Europe leads in advanced treatment adoption with nearly 64% integration of image-guided and adaptive therapy workflows across major oncology institutions. Over the next three years, automated contouring and cloud-connected oncology planning systems are projected to reduce patient wait times by 18% and improve treatment throughput by 24%. ESG positioning is also becoming a competitive advantage, with energy-efficient LINAC platforms lowering hospital power consumption by 14% while supporting stricter radiation compliance frameworks.

In 2025, a multi-hospital oncology network deployment in Asia reduced treatment recalibration frequency by 27% through AI-driven dose optimization and predictive maintenance integration. Manufacturers are increasingly shifting capital allocation toward compact high-throughput systems, regional manufacturing hubs, and oncology software partnerships to strengthen recurring service revenues and reduce supply-chain exposure. Companies optimizing integrated treatment ecosystems, localized support infrastructure, and AI-driven clinical workflows are securing stronger competitive positioning as global oncology modernization accelerates.

Precision oncology expansion is accelerating demand for advanced medical linear accelerators as healthcare systems prioritize high-accuracy radiotherapy and faster patient throughput. More than 58% of tertiary cancer centers upgraded radiation platforms between 2024 and 2026 to support image-guided and adaptive treatment workflows. AI-assisted planning systems improved treatment precision by 31% while reducing setup time by 22%, forcing hospitals to replace aging radiotherapy infrastructure. Simultaneously, geopolitical semiconductor sourcing shifts and regional healthcare localization policies accelerated domestic oncology equipment investments across Asia and North America. In response, manufacturers are expanding production capacity, increasing software integration partnerships, and accelerating modular system launches. Companies prioritizing scalable oncology ecosystems are strengthening procurement advantages and long-term institutional contract positioning globally.

High infrastructure costs and component supply concentration are constraining medical linear accelerator deployment across cost-sensitive healthcare systems. Advanced radiotherapy installation projects require nearly 35% higher infrastructure expenditure compared to conventional oncology equipment due to shielding requirements, imaging integration, and specialized facility upgrades. More than 62% of critical semiconductor and precision imaging components remain concentrated within limited supplier networks, increasing procurement delays and maintenance risks. Regulatory approval timelines also expanded by 18% in several developed markets following stricter radiation safety validation standards. These pressures are forcing hospitals to delay replacement cycles and limit capacity expansion. To mitigate risk, manufacturers are diversifying component sourcing, securing long-term supplier agreements, and developing compact lower-energy systems with reduced infrastructure dependency and faster deployment timelines.

AI-integrated oncology platforms are redefining competitive advantage by transforming medical linear accelerators into intelligent treatment ecosystems. Adaptive radiotherapy software increased treatment workflow efficiency by 29% while reducing repeat imaging procedures by 17%, creating measurable operational savings for high-volume cancer centers. Emerging markets across Southeast Asia, the Middle East, and Latin America are expanding oncology infrastructure programs, with advanced radiotherapy installations increasing by over 21% annually through public-private healthcare investment models. A major future signal is the rise of MRI-guided and cloud-connected treatment systems enabling real-time therapy optimization. Companies are responding through aggressive R&D investment, regional manufacturing expansion, and software ecosystem partnerships. Businesses securing integrated AI-enabled oncology capabilities are positioning for stronger service revenues and long-term institutional adoption leadership globally.

Complex implementation requirements and operational skill shortages are threatening sustainable expansion across advanced radiotherapy networks. More than 43% of healthcare providers in emerging regions face shortages of trained radiation oncology specialists, limiting effective utilization of next-generation linear accelerator systems. Treatment calibration complexity and software integration demands increased commissioning timelines by nearly 26%, slowing large-scale deployment across multi-site hospital networks. Energy-intensive oncology infrastructure is also creating pressure in regions with unstable power grids and rising electricity costs, directly affecting treatment continuity and operational scalability. Companies must solve interoperability gaps, workforce training limitations, and predictive maintenance challenges to maintain competitive relevance. Manufacturers investing in automation, remote diagnostics, and strategic hospital partnerships are improving deployment efficiency and strengthening long-term operational resilience across expanding oncology ecosystems.

AI-driven treatment planning adoption increased 34% across oncology networks during 2025–2026, reshaping radiotherapy execution workflows. Hospitals are integrating automated contouring and adaptive planning software to reduce treatment preparation time by 26% and improve targeting precision by 29%. Companies are accelerating cloud-based oncology software partnerships and embedding predictive maintenance capabilities to optimize equipment uptime. Regulatory pressure for treatment traceability is also forcing providers to standardize digital oncology workflows globally.

Compact linear accelerator installations expanded 27% as healthcare providers optimized space utilization and decentralized cancer treatment access. Mid-sized hospitals and ambulatory oncology centers reduced facility modification costs by nearly 21% through compact system deployment. Asia-Pacific facilities accelerated procurement following regional healthcare infrastructure expansion and localized component manufacturing initiatives. Manufacturers are restructuring product portfolios toward modular systems with faster installation cycles and lower energy consumption to capture emerging decentralized treatment demand.

Image-guided radiotherapy integration surpassed 61% in advanced cancer centers, redefining operational precision standards. Real-time imaging workflows reduced treatment recalibration frequency by 24% while improving patient throughput efficiency by 18%. A non-obvious shift is emerging as hospitals prioritize workflow interoperability over raw treatment power, forcing vendors to optimize software ecosystems rather than hardware alone. Companies are increasing integration partnerships with oncology imaging providers to secure long-term platform dependency.

Subscription-based oncology servicing contracts increased 31%, shifting business models beyond equipment sales. Healthcare providers are prioritizing uptime guarantees, remote diagnostics, and lifecycle management to reduce unplanned maintenance costs by 19%. Semiconductor sourcing instability and specialist labor shortages accelerated demand for predictive servicing capabilities. Manufacturers are expanding regional technical support hubs and recurring-service models, redefining competitive positioning around operational continuity instead of standalone hardware procurement.

The medical linear accelerator market is segmented by type, application, and end-user, with demand increasingly concentrated around high-precision oncology workflows and integrated treatment ecosystems. Image-guided and high-energy systems together account for over 56% of installations due to superior treatment accuracy and multi-tumor capability. Radiation therapy remains the dominant application with nearly 38% utilization share, while stereotactic and image-guided procedures are rapidly shifting procurement priorities toward software-enabled platforms. Hospitals and cancer treatment centers collectively contribute more than 67% of total demand as centralized oncology infrastructure expands globally. Companies are strategically repositioning toward compact, AI-integrated systems and service-based delivery models to capture decentralized treatment growth and operational efficiency demand.

High-Energy Systems dominate the medical linear accelerator market with nearly 34% share due to their ability to support deep-tissue tumor treatment, high patient throughput, and multi-application oncology workflows across large hospital networks. Their structural advantage lies in scalability and compatibility with advanced imaging and adaptive radiotherapy platforms, making them the preferred choice for high-volume cancer centers. However, Image-Guided Systems are emerging as the fastest-growing category, recording adoption growth above 23% as healthcare providers prioritize treatment precision, workflow automation, and real-time targeting optimization. Compared to conventional High-Energy Systems, Image-Guided Systems reduce recalibration requirements by 24% and improve treatment consistency across complex oncology cases.

Compact Systems, Stereotactic Systems, and Low-Energy Systems collectively account for nearly 41% of market demand, driven by decentralized cancer treatment expansion and cost-sensitive healthcare infrastructure upgrades. Compact Systems are gaining traction in ambulatory and regional treatment centers due to 19% lower installation costs and reduced facility modification requirements. Meanwhile, Stereotactic Systems remain strategically relevant for high-precision neurological and small-target tumor therapies. Companies are accelerating investment in AI-integrated imaging, modular designs, and lower-energy efficiency platforms to capture shifting procurement priorities. Demand is clearly moving toward intelligent, workflow-optimized systems rather than standalone treatment hardware.

Radiation Therapy remains the leading application in the medical linear accelerator market with approximately 38% share, supported by widespread clinical use across high-volume oncology centers and standardized cancer treatment protocols. Demand concentration exists because radiation therapy supports broad tumor categories, scalable patient throughput, and integrated multi-session treatment planning. However, Image-Guided Radiotherapy is emerging as the fastest-growing application, expanding by more than 24% as hospitals prioritize adaptive oncology workflows, treatment accuracy, and reduced exposure to surrounding healthy tissue. Compared with traditional Radiation Therapy workflows, Image-Guided Radiotherapy improves targeting consistency by 27% while reducing repeat imaging frequency by 18%.

Stereotactic Radiosurgery and Intensity-Modulated Radiotherapy are reshaping advanced oncology treatment pathways, particularly in neurological and precision tumor management applications. Together with Tumor Treatment and Cancer Research applications, these segments account for nearly 49% of operational demand. Hospitals are increasingly integrating AI-assisted treatment planning and cloud-based oncology imaging to optimize multi-application platform utilization. Companies are responding by scaling software-driven treatment ecosystems, accelerating compatibility upgrades, and expanding integrated radiotherapy deployment capabilities. Demand is steadily shifting from generalized radiation delivery toward precision-guided and data-integrated oncology execution models that improve operational efficiency and clinical consistency.

Hospitals dominate the medical linear accelerator market with nearly 42% demand share due to high patient intake volumes, centralized oncology infrastructure, and stronger capital investment capabilities for integrated radiotherapy systems. Their purchasing behavior is heavily focused on scalable treatment platforms, AI-assisted workflows, and long-term service agreements that maximize operational continuity. Cancer Treatment Centers represent the fastest-growing end-user segment, expanding by over 26% as specialized oncology networks accelerate high-precision treatment deployment and outpatient cancer care expansion. Compared with Hospitals, Cancer Treatment Centers prioritize workflow optimization, adaptive radiotherapy integration, and faster patient turnaround efficiency.

Specialty Clinics, Research Institutes, Ambulatory Care Centers, and Academic Medical Centers collectively contribute approximately 44% of market demand, supported by increasing decentralized oncology treatment access and clinical research activity. Ambulatory Care Centers are gaining traction through compact system adoption and lower infrastructure dependency, while Research Institutes continue investing in stereotactic and image-guided treatment technologies for advanced oncology trials. Manufacturers are responding with flexible financing models, modular product customization, and strategic hospital partnerships to capture diversified procurement demand. Future demand is shifting toward specialized, high-efficiency treatment environments that prioritize software integration, remote diagnostics, and scalable oncology workflow management.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.41% between 2026 and 2033.

North America leads in advanced oncology infrastructure and high adoption of AI-enabled radiotherapy systems, with over 72% of tertiary cancer centers operating image-guided treatment platforms. Europe contributes nearly 29% of global demand and leads in precision treatment compliance, sustainability-focused procurement, and energy-efficient radiotherapy deployment. Meanwhile, Asia-Pacific captures more than 24% of global installations and is accelerating through localized manufacturing expansion, hospital infrastructure investments, and rising oncology treatment capacity across China, India, and Southeast Asia. Latin America and the Middle East are witnessing targeted deployment growth as governments prioritize cancer treatment accessibility. Semiconductor localization policies and regional healthcare modernization programs are reshaping supply chains, forcing manufacturers to expand regional production, service hubs, and AI-integrated treatment ecosystems globally.

North America controls nearly 38% of the global medical linear accelerator market, supported by high oncology treatment volumes, strong reimbursement frameworks, and rapid deployment of AI-assisted radiotherapy systems. More than 72% of major cancer centers across the United States and Canada operate image-guided or adaptive treatment platforms, reflecting aggressive modernization of radiation oncology infrastructure. Tightened radiation safety validation requirements and semiconductor supply diversification efforts are reshaping procurement priorities toward software-integrated and locally supported systems. Hospitals reduced treatment planning time by 26% through automated contouring adoption during 2025–2026. Healthcare providers increasingly prefer scalable service-based procurement models with predictive maintenance integration and long-term workflow optimization. Companies are prioritizing this region to secure high-value institutional contracts and strengthen recurring oncology platform revenues.

Europe represents approximately 29% of the global medical linear accelerator market, led by Germany, France, and the United Kingdom through strong public healthcare oncology investments and strict radiation compliance frameworks. More than 64% of advanced treatment facilities across Western Europe implemented image-guided radiotherapy integration to meet precision treatment and patient safety standards. Sustainability regulations are also forcing hospitals to prioritize energy-efficient accelerator systems that reduce operational power usage by nearly 15%. Healthcare institutions increasingly favor interoperable oncology ecosystems capable of centralized treatment monitoring and workflow optimization. Manufacturers are responding with localized servicing networks, software-focused treatment upgrades, and strategic hospital partnerships. The region is forcing companies to compete on compliance performance, operational efficiency, and integrated digital oncology execution rather than hardware capability alone.

Asia-Pacific ranks as the fastest-expanding medical linear accelerator market, accounting for nearly 24% of global demand and recording aggressive oncology infrastructure deployment across China, India, Japan, and South Korea. China alone contributes over 41% of regional installation activity through localized manufacturing expansion and public hospital modernization programs. Healthcare providers are prioritizing compact and image-guided systems that reduce infrastructure modification costs by 19% while increasing treatment throughput efficiency by 22%. Regional manufacturers are scaling domestic component production and AI-enabled treatment integration to reduce import dependency and accelerate deployment timelines. Hospitals across the region increasingly favor cost-efficient, high-capacity radiotherapy ecosystems capable of serving large patient volumes. Companies are prioritizing Asia-Pacific to capture installation scale, manufacturing efficiency, and long-term oncology infrastructure expansion opportunities.

South America contributes nearly 6% of the global medical linear accelerator market, with Brazil and Argentina leading regional oncology infrastructure deployment through public healthcare modernization and expanding cancer treatment access. Demand is rising as urban cancer centers increase advanced radiotherapy installation capacity by over 18%, particularly for image-guided treatment systems. However, high import dependency, currency volatility, and uneven healthcare infrastructure remain major deployment constraints across secondary markets. Hospitals are increasingly adopting compact systems that lower installation costs by approximately 17% and reduce operational complexity. Regional healthcare providers show strong preference for flexible financing, localized servicing, and modular treatment platforms. Companies view the region as a high-potential but execution-sensitive market requiring localized partnerships, pricing adaptation, and long-term infrastructure support strategies.

The Middle East & Africa region accounts for approximately 3% of global medical linear accelerator demand, driven by rising oncology infrastructure investment across Saudi Arabia, the United Arab Emirates, and South Africa. Government-backed healthcare modernization programs and international hospital partnerships are accelerating deployment of advanced radiotherapy systems across high-capacity treatment centers. More than 28% of newly commissioned oncology facilities in the Gulf region integrated image-guided treatment technologies during 2025–2026. Healthcare providers are prioritizing scalable systems with remote diagnostics and predictive servicing to overcome specialist workforce shortages and operational constraints. Regional procurement increasingly favors long-term technology partnerships and turnkey oncology infrastructure deployment models. Companies are targeting the region to establish early positioning in underpenetrated but rapidly modernizing cancer treatment ecosystems.

United States – Holds approximately 38% share of the Medical Linear Accelerator market due to advanced oncology infrastructure, strong AI-enabled radiotherapy adoption, and high institutional treatment capacity.

China – Accounts for nearly 16% share of the Medical Linear Accelerator market, supported by aggressive healthcare infrastructure expansion, localized manufacturing growth, and rising public oncology investment.

The medical linear accelerator market is dominated by competition between global technology leaders such as Varian, Elekta, Siemens Healthineers, Accuray, and Canon Medical against regional cost-focused manufacturers and software-integrated oncology innovators. The top five players collectively control nearly 68% of global market share through strong hospital relationships, integrated oncology ecosystems, and advanced radiotherapy software capabilities. Competition is increasingly centered on AI-assisted treatment planning, image-guided precision, and service-network responsiveness, with automated workflow integration improving treatment efficiency by 32% and reducing recalibration needs by 24%. Companies are accelerating regional manufacturing expansion, oncology software partnerships, and predictive maintenance deployment to strengthen recurring service revenues. Vertical integration and localized component sourcing are reshaping competitive positioning amid semiconductor supply pressure and regulatory tightening. High capital intensity, clinical validation requirements, and long procurement cycles remain major entry barriers. Winning now depends on integrated treatment ecosystems, localized support infrastructure, and AI-driven workflow optimization capabilities.

Varian Medical Systems

Elekta AB

Siemens Healthineers

Accuray Incorporated

Canon Medical Systems Corporation

ViewRay Technologies

Hitachi Ltd.

Panacea Medical Technologies

Shinva Medical Instrument Co., Ltd.

IntraOp Medical Corporation

Best Medical International

Mitsubishi Electric Corporation

Mevion Medical Systems

P-Cure Ltd.

AI-assisted adaptive radiotherapy and image-guided treatment systems are reshaping current medical linear accelerator operations by improving targeting precision and reducing workflow inefficiencies. More than 61% of advanced oncology centers integrated image-guided radiotherapy platforms during 2025–2026, while automated contouring reduced treatment planning time by 26%. Compared with legacy fixed-protocol systems, AI-enabled adaptive radiotherapy improves treatment accuracy by 32% and lowers recalibration frequency by 24%. Hospitals are increasingly prioritizing integrated oncology ecosystems combining imaging, planning, and predictive maintenance to maximize patient throughput and reduce operational delays.

Emerging technologies between 2026 and 2028 are centered on MRI-guided radiotherapy, cloud-connected oncology workflows, and AI-enhanced CT-LINAC platforms. New-generation systems improve imaging clarity by nearly 30% while reducing unnecessary radiation exposure during treatment planning. Compact high-efficiency accelerators are also gaining rapid adoption, particularly in ambulatory oncology networks, due to 19% lower installation costs and faster deployment cycles. Manufacturers are accelerating software interoperability partnerships and modular system development to strengthen recurring service models and long-term institutional platform dependency.

Disruptive innovation is increasingly focused on autonomous treatment optimization, digital twin-based therapy simulation, and predictive servicing integration. Real-time motion management systems improved treatment continuity by 21% across multi-site oncology networks in 2025. Companies with strong AI imaging capabilities, cloud integration, and localized service infrastructure are capturing higher-value institutional contracts as healthcare providers shift from standalone hardware procurement toward intelligent, scalable radiotherapy ecosystems.

January 2026 – Elekta received FDA 510(k) clearance for the Elekta Evo CT-LINAC platform featuring AI-enhanced Iris imaging technology, improving image clarity and treatment precision during radiotherapy workflows. The development strengthened Elekta’s competitive position in advanced adaptive oncology systems and accelerated U.S. clinical deployment momentum. [AI Imaging Shift] Source: Elekta

September 2025 – Varian Medical Systems unveiled major Halcyon platform upgrades integrating PerfectKinetix Dynamic Couch, IDENTIFY motion management, and HyperSight imaging, enabling image-guided radiotherapy sessions in under 10 minutes. The upgrade improved workflow efficiency and expanded precision treatment capabilities across high-volume oncology centers. [Workflow Precision Upgrade] Source: Varian Medical Systems

February 2025 – Elekta secured a public healthcare contract with Mexico’s IMSS for deployment of eight linear accelerators across multiple oncology facilities, strengthening regional treatment infrastructure capacity. The project accelerated high-precision radiotherapy accessibility and reinforced Elekta’s strategic expansion across Latin American healthcare modernization programs. [Regional Capacity Expansion] Source: Elekta Mexico Announcement

2025 – Accuray Incorporated expanded deployment focus around the Radixact platform featuring integrated adaptive planning, real-time motion synchronization, and accelerated imaging workflows. The system improved clinical workflow efficiency while supporting highly personalized radiation therapy delivery across complex oncology indications through continuous 360-degree precision treatment capabilities. [Adaptive Therapy Scaling] Source: Accuray Radixact Platform

This report provides comprehensive coverage of the global medical linear accelerator market across system types, clinical applications, end-user groups, and regional demand dynamics. The analysis includes High-Energy Systems, Low-Energy Systems, Compact Systems, Image-Guided Systems, and Stereotactic Systems, alongside application areas such as Radiation Therapy, Image-Guided Radiotherapy, Stereotactic Radiosurgery, and Cancer Research. End-user evaluation spans Hospitals, Cancer Treatment Centers, Specialty Clinics, Research Institutes, Ambulatory Care Centers, and Academic Medical Centers across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 61% of analyzed oncology facilities have integrated image-guided workflows, while compact systems account for nearly 19% lower infrastructure modification costs in decentralized treatment environments.

The report delivers strategic insight into technology adoption trends, operational transformation, supply-chain restructuring, and AI-driven oncology workflow integration between 2026 and 2033. It profiles key global manufacturers, compares treatment platform capabilities, and evaluates deployment patterns across mature and emerging healthcare systems. Analytical depth includes adoption concentration by region, treatment workflow optimization metrics, and evolving procurement behavior, with over 64% of advanced cancer centers prioritizing software-integrated radiotherapy ecosystems. The study supports investment planning, expansion prioritization, product positioning, and competitive benchmarking for manufacturers, healthcare providers, institutional buyers, and oncology infrastructure stakeholders navigating rapidly transforming precision radiotherapy markets.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 4130 Million |

|

Market Revenue in 2033 |

USD 6677.57 Million |

|

CAGR (2026 - 2033) |

6.19% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Varian Medical Systems, Elekta AB, Siemens Healthineers, Accuray Incorporated, Canon Medical Systems Corporation, ViewRay Technologies, Hitachi Ltd., Panacea Medical Technologies, Shinva Medical Instrument Co., Ltd., IntraOp Medical Corporation, Best Medical International, Mitsubishi Electric Corporation, Mevion Medical Systems, P-Cure Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |