Reports

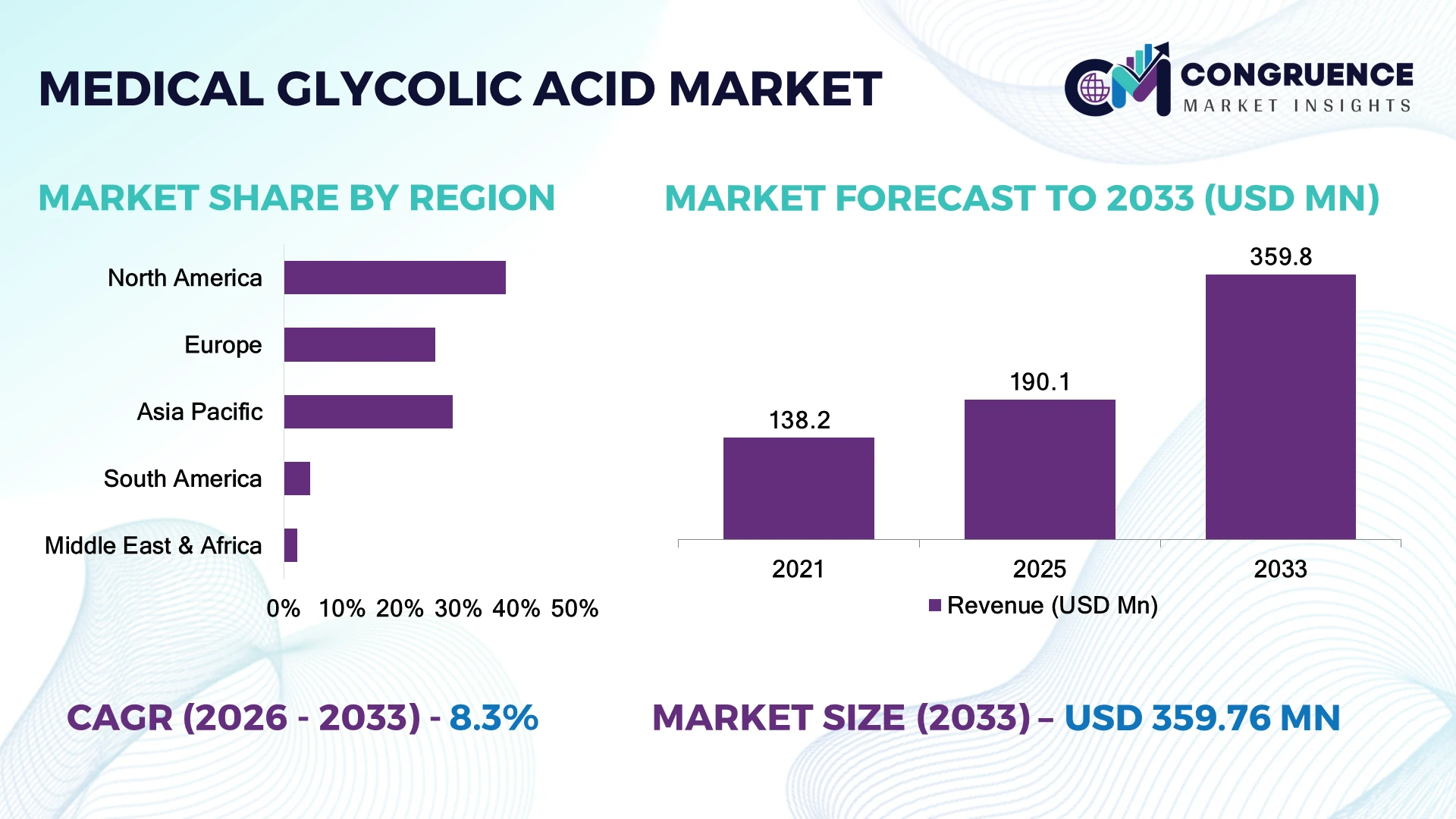

The Global Medical Glycolic Acid Market was valued at USD 190.1 Million in 2025 and is anticipated to reach a value of USD 359.8 Million by 2033 expanding at a CAGR of 8.3% between 2026 and 2033. Growth is being driven by increasing clinical use of pharmaceutical-grade glycolic acid in dermatology, wound management, aesthetic medicine, and advanced topical formulations requiring high-purity active ingredients.

The United States accounts for approximately 34% of the global market, supported by a well-established dermatology sector, advanced pharmaceutical manufacturing, and strong adoption of minimally invasive aesthetic procedures. More than 62% of medical-grade chemical peel procedures in North America utilize glycolic acid formulations, while Japan continues strengthening high-purity production for pharmaceutical applications with quality yields exceeding 98%. In contrast, China's manufacturing expansion is improving global supply capacity by nearly 15%, although stricter export compliance and evolving trade policies continue influencing sourcing strategies across international healthcare markets.

Companies securing compliant production capacity, diversified raw material sourcing, and premium pharmaceutical-grade formulations will strengthen long-term competitive positioning.

Market Size & Growth: USD 190.1 million in 2025, projected to reach USD 359.8 million by 2033 at 8.3% CAGR, supported by expanding dermatological therapeutics and medical aesthetics.

Top Growth Drivers: Rising aesthetic procedures (+14%), pharmaceutical-grade ingredient demand (+11%), and advanced topical formulation adoption (+9%) accelerate market expansion.

Short-Term Forecast: By 2028, manufacturing efficiency is expected to improve by 18% through process automation and purification optimization.

Emerging Technologies: Continuous-flow synthesis, AI-enabled quality monitoring, and precision purification improve batch consistency by approximately 16%.

Regional Leaders: North America (~USD 71 million), Asia-Pacific (~USD 59 million), and Europe (~USD 43 million) lead through clinical adoption, manufacturing expansion, and pharmaceutical innovation.

Consumer/End-User Trends: Nearly 67% of dermatology clinics increasingly prefer medical-grade glycolic acid for advanced skin treatment protocols.

Pilot/Case Example: In 2026, pharmaceutical manufacturers achieved approximately 20% shorter purification cycles using automated process control technologies.

Competitive Landscape: Top manufacturers control nearly 52% of global supply, competing through purity standards, formulation expertise, production scale, and regulatory compliance.

Regulatory & ESG Impact: Green manufacturing initiatives reduce solvent consumption by nearly 17%, supporting sustainable pharmaceutical production.

Investment & Funding: More than USD 180 million has been directed toward pharmaceutical ingredient manufacturing expansion, process modernization, and capacity enhancement.

Innovation & Future Outlook: High-purity formulations, sustainable synthesis, and integrated pharmaceutical supply chains continue reshaping global competitive dynamics.

Medical glycolic acid demand is increasingly concentrated in dermatology, cosmetic surgery, wound care, and prescription skincare applications where formulation consistency and pharmaceutical purity remain critical. Automated purification technologies improve production efficiency by nearly 18%, while manufacturers continue expanding compliant manufacturing facilities amid tighter quality regulations and diversified raw material sourcing. These operational shifts are strengthening the market's strategic foundation for long-term competitive development.

Medical glycolic acid is becoming strategically important as pharmaceutical manufacturers, dermatology companies, and medical aesthetics providers prioritize high-purity active ingredients that meet increasingly stringent regulatory and clinical performance standards. Supply-chain diversification and pharmaceutical-grade manufacturing expansion have become central investment priorities following global disruptions to specialty chemical sourcing, encouraging regional production capacity and stronger quality assurance systems.

Modern continuous-flow purification technology delivers approximately 18% higher production efficiency while reducing solvent consumption by nearly 15% compared with conventional batch processing methods. North America continues leading clinical adoption through established dermatology and aesthetic medicine infrastructure, whereas Asia-Pacific is strengthening its position through manufacturing scale, pharmaceutical ingredient production, and lower processing costs. Over the next two to three years, more than 35% of newly commissioned pharmaceutical ingredient facilities are expected to incorporate advanced automation and digital quality monitoring.

A practical example is the expansion of automated purification lines capable of producing pharmaceutical-grade glycolic acid with higher batch consistency for prescription dermatology formulations. Companies are increasing investments in GMP-compliant manufacturing, regional production partnerships, and formulation research to improve supply resilience and accelerate product qualification. Organizations that combine manufacturing excellence, regulatory compliance, and advanced formulation capabilities will establish stronger competitive positions as clinical applications continue expanding.

Growing utilization of medical glycolic acid in prescription dermatology, minimally invasive aesthetic procedures, and wound management is strengthening market demand. Nearly 68% of professional chemical peel treatments now utilize glycolic acid-based formulations because of their predictable exfoliation performance and compatibility with combination therapies. Demand for pharmaceutical-grade glycolic acid with purity above 99% has increased by approximately 16% as manufacturers prioritize premium dermatological products. Stricter pharmaceutical quality requirements in the United States are accelerating investment in GMP-certified production and analytical testing capabilities. This shift is encouraging companies to expand purification capacity, introduce higher-purity formulations, and establish formulation partnerships with dermatology brands, creating stronger product differentiation while improving regulatory compliance and long-term customer retention.

Manufacturing medical-grade glycolic acid requires high-purity raw materials, validated purification systems, and stringent quality control, increasing production complexity. Pharmaceutical-grade manufacturing costs remain approximately 18% higher than industrial-grade production, while regulatory compliance activities account for nearly 12% of total operating expenditure. China's continued dominance in specialty chemical intermediates exposes manufacturers to procurement disruptions and fluctuating feedstock availability during supply-chain adjustments. These structural pressures directly affect production scalability, inventory planning, and profit margins for smaller manufacturers. Companies are responding by diversifying supplier networks, expanding localized purification facilities, and securing long-term procurement agreements while investing in process optimization to stabilize production costs and maintain uninterrupted pharmaceutical-grade supply.

The growing shift toward personalized dermatology and multifunctional topical therapies is creating opportunities beyond conventional chemical peel products. Approximately 27% of new prescription skincare formulations now combine glycolic acid with ceramides, peptides, or anti-inflammatory compounds to improve therapeutic outcomes while minimizing skin irritation. Japan and South Korea continue advancing precision formulation technologies through automated pharmaceutical manufacturing and high-purity ingredient development. Continuous-flow synthesis reduces processing time by nearly 20%, enabling more flexible production and improved batch consistency. Companies are increasing investments in formulation research, pharmaceutical partnerships, and customized active ingredient platforms to capture emerging demand from prescription dermatology, post-procedure skincare, and specialized wound healing applications.

Maintaining consistent pharmaceutical-grade purity while expanding production remains one of the market's most significant long-term execution challenges. More than 14% of production batches require additional purification or validation before pharmaceutical release, increasing manufacturing lead times and operational costs. Automation adoption across specialty chemical facilities remains below 40%, limiting process standardization and quality consistency during capacity expansion. Increasing regulatory expectations for traceability, impurity profiling, and digital batch documentation further intensify operational complexity. Manufacturers must invest in advanced analytical instrumentation, automated purification systems, digital quality management platforms, and workforce development to achieve scalable production while preserving regulatory compliance, competitive differentiation, and reliable global pharmaceutical supply.

High-Purity Production Expansion Pharmaceutical manufacturers are increasing investment in pharmaceutical-grade purification technologies as demand for purity levels above 99% continues rising. Automated purification has improved batch consistency by nearly 18% while reducing process deviations by approximately 14%. Companies are modernizing production lines and expanding certified manufacturing capacity to strengthen supply reliability amid stricter pharmaceutical quality expectations.

Combination Therapy Formulations Glycolic acid is increasingly incorporated into prescription dermatology products alongside peptides, niacinamide, and ceramides. Nearly 31% of newly introduced advanced skincare formulations now feature multifunctional active ingredient combinations that improve treatment effectiveness while reducing irritation. Manufacturers are expanding formulation partnerships and accelerating product development to address growing physician preference for combination therapies.

Digital Manufacturing Integration Pharmaceutical facilities are deploying AI-assisted process monitoring and automated quality inspection to improve operational efficiency. Digital manufacturing systems have shortened quality release cycles by approximately 17% while reducing manual inspection requirements by nearly 22%. Companies are integrating real-time analytical technologies and electronic batch documentation to strengthen regulatory readiness and manufacturing productivity.

Regional Supply Chain Diversification Pharmaceutical ingredient manufacturers are reducing dependence on single-country sourcing by establishing alternative purification and packaging operations across India and Europe. Diversified procurement strategies have lowered supply disruption risks by approximately 19% while improving inventory resilience by nearly 16%. Companies are expanding regional partnerships and localized production capabilities to strengthen business continuity under evolving trade and regulatory conditions.

Pharmaceutical-grade medical glycolic acid accounted for approximately 71% of the market in 2025, maintaining leadership through its extensive use in prescription dermatology, medical aesthetic formulations, wound management products, and regulated pharmaceutical applications. Its superior purity, validated manufacturing processes, and compliance with pharmaceutical quality standards make it the preferred choice for clinical use. Nearly 66% of newly approved dermatological formulations incorporate pharmaceutical-grade glycolic acid because of improved formulation stability and lower impurity profiles. Manufacturers continue expanding GMP-certified production facilities and investing in advanced purification technologies to strengthen product quality and secure long-term supply agreements with healthcare companies.

Ultra-high-purity pharmaceutical glycolic acid represents the fastest-growing segment as personalized dermatology, regenerative medicine, and advanced topical therapies require increasingly stringent ingredient specifications. Standard pharmaceutical-grade products remain essential for established prescription formulations, while customized concentration variants are gaining traction for specialty clinical applications. Approximately 23% of recent manufacturing investments target high-purity production expansion and automated quality monitoring, reflecting the industry's shift toward premium formulations. Companies are strengthening formulation partnerships, expanding analytical testing capabilities, and introducing customized pharmaceutical-grade ingredients to improve differentiation and support evolving regulatory requirements.

According to 2026 pharmaceutical manufacturing assessments from international quality organizations, adoption of automated GMP-compliant purification systems continues increasing across specialty active pharmaceutical ingredient facilities to improve batch consistency and regulatory compliance.

Dermatology accounted for approximately 48% of the market in 2025, supported by widespread use of medical glycolic acid in prescription acne treatments, hyperpigmentation therapy, chemical peels, and skin rejuvenation procedures. Clinical preference remains high because of its proven exfoliation performance, controlled penetration, and compatibility with combination formulations. Nearly 63% of specialist dermatology clinics continue utilizing glycolic acid-based formulations within advanced skin treatment protocols. Pharmaceutical companies are expanding clinical formulation portfolios while integrating advanced delivery systems to improve therapeutic outcomes and treatment precision.

Medical aesthetics represents the fastest-growing application as minimally invasive cosmetic procedures and physician-supervised skincare continue expanding globally. Wound care applications are gaining strategic importance through research into tissue regeneration and controlled topical formulations, while pharmaceutical manufacturing maintains stable demand for prescription dermatology products. Approximately 28% of newly developed medical skincare formulations combine glycolic acid with barrier-repair and anti-inflammatory ingredients, encouraging manufacturers to increase formulation research, automation, and product customization. This shift is broadening clinical applications while strengthening long-term commercial opportunities across healthcare markets.

A 2025 enterprise survey conducted among dermatology professionals indicated increasing integration of glycolic acid-based formulations into combination treatment protocols for acne management, pigmentation disorders, and skin resurfacing procedures.

Dermatology clinics held approximately 44% of the market in 2025, driven by high patient volumes, specialized skincare expertise, and extensive utilization of medical glycolic acid across therapeutic and cosmetic procedures. Their consistent demand for pharmaceutical-grade formulations, standardized treatment protocols, and advanced clinical equipment positions them as the largest purchasing segment. More than 69% of physician-administered chemical peel procedures are performed within specialized dermatology clinics, encouraging manufacturers to provide customized product concentrations, clinical education programs, and long-term distribution partnerships.

Hospitals represent the fastest-growing end-user segment as integrated dermatology departments, outpatient aesthetic services, and wound care programs increasingly incorporate pharmaceutical-grade glycolic acid into clinical practice. Medical aesthetic centers, pharmaceutical manufacturers, and research institutions continue expanding adoption for specialized treatment protocols and product development activities. Approximately 31% of supplier investments now focus on customized packaging, regulatory support, and collaborative product development for institutional healthcare providers. Companies are strengthening healthcare partnerships, improving clinical training, and expanding compliant manufacturing capabilities to capture future institutional demand.

A 2026 institutional healthcare assessment reported continued expansion of physician-supervised dermatological procedures within hospital outpatient departments, reinforcing demand for pharmaceutical-grade glycolic acid formulations across regulated clinical environments.

North America accounted for the largest market share at 38.1% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2026 and 2033.

Clinical Dermatology Expansion Reinforces Pharmaceutical-Grade Demand

North America leads the Medical Glycolic Acid Market through its advanced dermatology infrastructure, mature pharmaceutical manufacturing ecosystem, and widespread adoption of physician-supervised aesthetic treatments. The region contributes approximately 38% of global demand, supported by strong utilization of pharmaceutical-grade glycolic acid in prescription skincare, chemical peels, and wound management. More than 71% of medical aesthetic clinics procure pharmaceutical-grade formulations meeting stringent quality specifications. Manufacturers continue investing in GMP-certified production, automated purification systems, and formulation development, while contract manufacturing partnerships strengthen domestic supply resilience. Expansion of specialty dermatology clinics and increasing integration of medical aesthetics into healthcare networks continue supporting long-term operational demand.

United States Market Outlook: The United States dominates regional consumption through its extensive dermatology clinic network, advanced pharmaceutical manufacturing capabilities, and large aesthetic medicine industry. Nearly 69% of North America's physician-administered glycolic acid procedures are performed in the country, supported by continuous investment in high-purity formulation development and automated pharmaceutical manufacturing. Companies are expanding clinical partnerships, formulation research, and compliant production capacity to address rising demand for premium dermatological therapies.

Regulatory Quality Standards Accelerate Premium Product Adoption

Europe maintains a strong market position through stringent pharmaceutical regulations, advanced cosmetic science, and expanding medical dermatology services. The region represents approximately 26% of global demand, with pharmaceutical manufacturers emphasizing ingredient traceability, formulation consistency, and validated production processes. Nearly 58% of newly introduced professional dermatology products utilize pharmaceutical-grade glycolic acid meeting enhanced quality standards. Manufacturers continue modernizing purification facilities, investing in environmentally efficient processing technologies, and strengthening partnerships with dermatology product developers to improve product differentiation and regulatory compliance.

Germany Market Outlook: Germany remains the region's largest market due to its robust pharmaceutical manufacturing base, established dermatology sector, and advanced chemical processing expertise. Approximately 42% of Europe's pharmaceutical-grade glycolic acid formulation activities are linked to German production and research facilities. Companies continue expanding analytical laboratories, automated manufacturing systems, and clinical formulation capabilities to support high-value medical skincare applications.

Manufacturing Scale and Medical Aesthetics Drive Expansion

Asia-Pacific is emerging as the fastest-growing regional market through expanding pharmaceutical ingredient manufacturing, rising medical aesthetics adoption, and increasing healthcare investment. The region accounts for approximately 29% of global demand while supplying a substantial share of pharmaceutical-grade glycolic acid intermediates. Nearly 24% of recently announced specialty chemical investments are directed toward pharmaceutical ingredient purification and quality enhancement. Manufacturers continue expanding production infrastructure, integrating automated quality control systems, and strengthening export-oriented supply chains to support growing international demand for medical-grade formulations.

China Market Outlook: China leads the regional market through its extensive specialty chemical manufacturing capacity, expanding pharmaceutical production, and rapidly developing dermatology industry. More than 46% of Asia-Pacific pharmaceutical-grade glycolic acid production is concentrated within Chinese manufacturing facilities. Producers continue investing in advanced purification technologies, GMP-compliant production lines, and international certification programs to strengthen export competitiveness and support global healthcare manufacturers.

Healthcare Modernization Supports Specialty Dermatology Growth

South America is witnessing steady market development as private healthcare providers expand dermatology services and medical aesthetics adoption increases across urban healthcare networks. The region contributes approximately 4.5% of global demand, supported by rising investment in specialty skincare treatments and pharmaceutical distribution infrastructure. Medical-grade dermatology product availability has improved by nearly 17% through strengthened importer partnerships and healthcare modernization initiatives. However, dependence on imported pharmaceutical ingredients and regulatory approval timelines continue influencing procurement efficiency. Companies are expanding local distribution partnerships and strengthening technical support to improve product accessibility.

Brazil Market Outlook: Brazil represents the largest regional market because of its well-developed aesthetic medicine sector, expanding dermatology clinics, and increasing demand for physician-supervised skincare procedures. Nearly 48% of South America's professional medical aesthetic treatments are performed in Brazil, encouraging pharmaceutical companies to strengthen local distribution networks, regulatory support, and clinical education initiatives for healthcare professionals.

Premium Healthcare Investment Expands Clinical Adoption

The Middle East & Africa market is progressing through investments in premium healthcare infrastructure, specialized dermatology centers, and advanced cosmetic medicine services. The region accounts for approximately 2.8% of global demand, with private healthcare providers driving adoption of pharmaceutical-grade glycolic acid formulations. Around 21% of newly established dermatology facilities incorporate advanced aesthetic treatment platforms utilizing regulated chemical peel products. Companies are strengthening regional distribution partnerships, expanding medical training programs, and improving product registration processes to enhance long-term market accessibility.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional demand through premium private healthcare facilities, advanced dermatology clinics, and strong investment in medical aesthetics. More than 38% of the Gulf region's specialized cosmetic dermatology procedures are performed in the UAE, encouraging suppliers to establish regional distribution hubs, expand clinical partnerships, and introduce premium pharmaceutical-grade skincare formulations tailored to specialist healthcare providers.

Competition is led by PureTech Scientific, CABB Group, Avid Organics, CrossChem, and Nikko Chemicals, with the top five players collectively controlling approximately 57% of the global market. PureTech Scientific and CABB compete through pharmaceutical-grade purity, regulatory compliance, and formulation expertise, while Avid Organics and CrossChem emphasize manufacturing efficiency and cost competitiveness. Japanese suppliers differentiate through ultra-high-purity specialty grades for regulated medical applications. Competitive advantage increasingly depends on purification technology, supply assurance, and product customization rather than pricing alone. Manufacturers using automated purification achieve nearly 18% higher production efficiency and reduce batch variability by approximately 15%, while vertically integrated operations shorten delivery cycles by around 12%. Companies are expanding GMP-certified capacity, strengthening distribution partnerships, and investing in bio-based production technologies. Market leadership is shifting toward high-purity, sustainable formulations, raising regulatory and technical barriers for new entrants. Success requires validated manufacturing, resilient supply chains, advanced purification capabilities, and strong pharmaceutical customer relationships.

PureTech Scientific LLC

CABB Group GmbH

Avid Organics Pvt. Ltd.

CrossChem Limited

Nikko Chemicals Co., Ltd.

Junsei Chemical Co., Ltd.

Kishida Chemical Co., Ltd.

Fengchen Group Co., Ltd.

Mehul Dye Chem Industries

Tokyo Chemical Industry Co., Ltd. (TCI)

Spectrum Chemical Mfg. Corp.

Merck KGaA

Advanced purification and continuous-flow manufacturing are transforming medical glycolic acid production by improving pharmaceutical-grade consistency and reducing process variability. More than 60% of newly commissioned production lines incorporate automated purification, increasing batch efficiency by approximately 18% while lowering solvent consumption by nearly 15%. AI-enabled analytical monitoring is gaining adoption for impurity profiling and real-time process validation, allowing manufacturers to accelerate quality release and improve compliance with pharmaceutical manufacturing standards.

Compared with conventional batch processing, continuous-flow synthesis reduces production time by nearly 20% and improves product consistency by approximately 17%. High-purity crystallization, digital quality management, and automated analytical instrumentation are becoming competitive differentiators for suppliers serving dermatology and prescription skincare markets. PureTech Scientific, CABB Group, and Avid Organics are well positioned to benefit through investments in pharmaceutical-grade manufacturing, sustainable production technologies, and advanced purification infrastructure, strengthening both operational efficiency and regulatory competitiveness.

Between 2026 and 2028, bio-based glycolic acid, AI-assisted process control, and digital manufacturing platforms will reshape competitive positioning. Nearly 35% of planned manufacturing upgrades are expected to integrate automated quality systems and environmentally efficient production technologies. Companies acting now will achieve faster regulatory qualification, stronger supply resilience, lower production costs, and preferred supplier status for high-value pharmaceutical and medical dermatology applications.

March 2026: Avid Organics announced the commercial launch of AviGa™ Bio HP70, the world's first commercial-scale bio-based 70% glycolic acid with REACH registration for Europe. The product is manufactured using 100% renewable energy, strengthening sustainable pharmaceutical and skincare supply chains. Business impact: expands premium bio-based glycolic acid availability. Source: Avid Organics

February 2026: Univar Solutions entered an exclusive distribution partnership with CABB Group for glycolic acid across selected EMEA markets, expanding access to high-purity specialty ingredients and strengthening regional supply capabilities. Business impact: accelerates commercial distribution and customer reach across regulated markets. Source: Univar Solutions

March 2025: PureTech Scientific appointed Brenntag Beauty & Personal Care Group as its authorized North American distributor for Glypure® high-purity glycolic acid products, extending coverage across the United States, Canada, and Mexico. Business impact: improves regional product availability and customer support. Source: Business Wire

April 2025: PureTech Scientific received U.S. EPA approval for its Glyclean D70-based broad-spectrum disinfectant formulation, extending glycolic acid applications into hospital-grade disinfection. Business impact: strengthens healthcare portfolio diversification and expands regulated application opportunities.

The report delivers comprehensive analysis of the global Medical Glycolic Acid Market across pharmaceutical-grade product types, clinical applications, end-user industries, and major regional markets. It evaluates adoption across dermatology, medical aesthetics, wound care, pharmaceutical manufacturing, and research applications while assessing demand from dermatology clinics, hospitals, pharmaceutical companies, and research institutions. The study covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, supported by country-level operational and competitive assessments.

The report also examines purification technologies, continuous-flow manufacturing, AI-enabled quality control, bio-based glycolic acid innovations, and evolving pharmaceutical production strategies. More than 50% of the competitive assessment focuses on high-purity manufacturing, regulatory compliance, supply-chain resilience, and strategic expansion by leading producers. The analysis supports investment prioritization, product portfolio optimization, capacity expansion, competitive benchmarking, and long-term strategic planning across the 2026–2033 assessment period.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 190.1 Million |

|

Market Revenue in 2033 |

USD 359.8 Million |

|

CAGR (2026 - 2033) |

8.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

PureTech Scientific LLC, CABB Group GmbH, Avid Organics Pvt. Ltd., CrossChem Limited, Nikko Chemicals Co., Ltd., Junsei Chemical Co., Ltd., Kishida Chemical Co., Ltd., Fengchen Group Co., Ltd., Mehul Dye Chem Industries, Tokyo Chemical Industry Co., Ltd. (TCI), Spectrum Chemical Mfg. Corp., Merck KGaA |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |