Reports

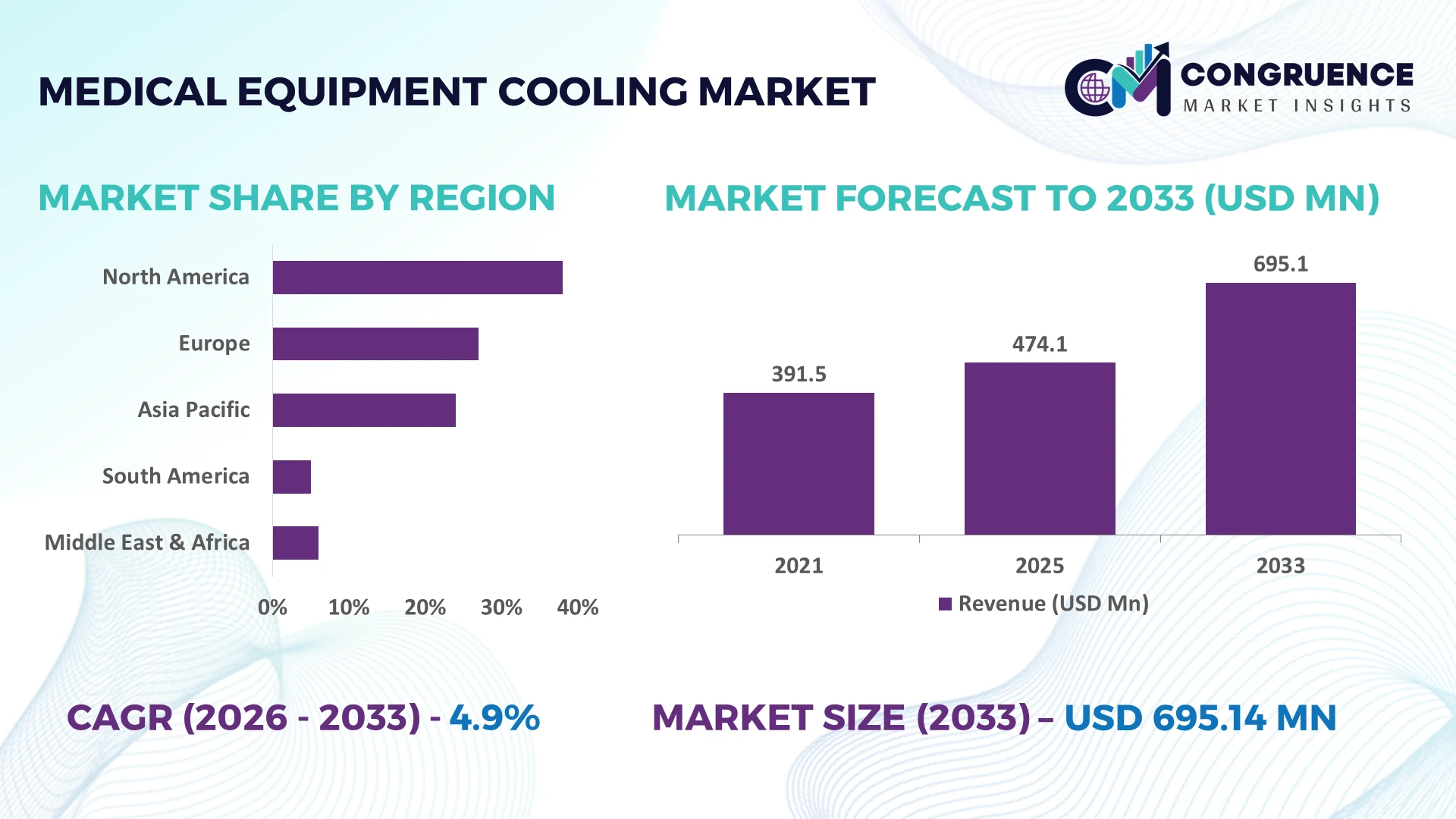

The Global Medical Equipment Cooling Market was valued at USD 474.1 Million in 2025 and is anticipated to reach a value of USD 695.14 Million by 2033 expanding at a CAGR of 4.9% between 2026 and 2033. Growth is driven by rising deployment of high-power MRI, CT, radiotherapy, and diagnostic imaging systems requiring precision thermal management, alongside increasing adoption of liquid-based and energy-efficient cooling technologies in modern healthcare infrastructure.

The United States accounts for approximately 34% of global market activity, supported by large-scale hospital modernization, over USD 15 billion in annual medical technology investments, and widespread deployment of advanced diagnostic equipment. Compared with Germany, the U.S. maintains higher installation density of premium imaging systems, while Germany leads European manufacturing excellence and thermal engineering integration. Ongoing healthcare localization initiatives and global semiconductor supply-chain realignment in 2026 continue to reinforce equipment production and adoption.

Manufacturers should prioritize advanced cooling solutions, localized production partnerships, and energy-efficient product portfolios to strengthen competitive positioning in high-investment healthcare markets.

Market Size & Growth: USD 474.1 Million in 2025, reaching USD 695.14 Million by 2033 at 4.9% CAGR, driven by advanced diagnostic imaging expansion and precision thermal management demand.

Top Growth Drivers: High-performance imaging installations increased by 11%, liquid cooling adoption exceeded 18%, and energy-efficient hospital upgrades expanded by 14%.

Short-Term Forecast: By 2028, advanced cooling systems improve equipment uptime by 15% while reducing maintenance costs by approximately 12%.

Emerging Technologies: AI-enabled thermal monitoring, liquid cooling, and advanced heat exchanger materials improve cooling efficiency by over 20% in next-generation medical equipment.

Regional Leaders: North America approaches USD 245 Million, Europe exceeds USD 180 Million, and Asia-Pacific surpasses USD 170 Million, supported by hospital digitization and regional manufacturing expansion.

Consumer/End-User Trends: More than 62% of new tertiary hospitals prioritize energy-efficient cooling for MRI, CT, and radiotherapy equipment installations.

Pilot/Case Example: In 2026, a hospital modernization program reduced imaging equipment overheating incidents by 22% through intelligent cooling optimization.

Competitive Landscape: Leading manufacturers collectively control approximately 38% of the global market, with Boyd, Lytron, Schneider Electric, Vertiv, and Koolance maintaining strong positions.

Regulatory & ESG Impact: Energy-efficiency initiatives lower cooling-related power consumption by nearly 16%, aligning with stricter healthcare sustainability targets and equipment performance standards.

Investment & Funding: More than USD 1.2 Billion supports manufacturing expansion, strategic partnerships, and regional supply-chain diversification across advanced medical technologies.

Innovation & Future Outlook: Compact liquid-cooled architectures and smart predictive maintenance accelerate next-generation healthcare equipment reliability while supporting global production expansion.

Medical Equipment Cooling Market demand is accelerating across diagnostic imaging, radiotherapy, laboratory instruments, and surgical systems as manufacturers introduce compact liquid-cooling platforms, intelligent thermal sensors, and predictive maintenance capabilities. More than 28% of newly developed premium imaging systems integrate advanced thermal management features, while ongoing supply-chain localization and evolving energy-efficiency requirements are reshaping procurement strategies, setting the foundation for the following strategic market assessment.

Medical equipment cooling has become a strategic differentiator as healthcare providers deploy higher-power imaging, radiotherapy, and laboratory systems that require precise thermal stability and uninterrupted operation. Infrastructure modernization and supply-chain restructuring since 2026 are encouraging manufacturers to localize component sourcing and redesign cooling architectures for greater resilience. This shift is strengthening competitive positioning by reducing equipment downtime while improving lifecycle performance across hospitals and diagnostic centers.

Advanced liquid cooling systems deliver approximately 20% higher heat dissipation efficiency than conventional air-cooled designs while lowering maintenance requirements by nearly 15% in high-load operating environments. The United States leads large-scale deployment through hospital technology upgrades, whereas Japan emphasizes compact, precision-engineered cooling modules for space-constrained healthcare facilities. Over the next two to three years, intelligent thermal monitoring is expected to be integrated into more than 35% of newly installed premium diagnostic platforms, improving predictive maintenance and operational continuity.

A leading imaging equipment manufacturer recently deployed AI-assisted thermal management across flagship MRI installations, reducing unplanned service interventions by approximately 18%. Companies are responding through strategic supplier partnerships, localized manufacturing investments, and co-development agreements with thermal engineering specialists. Organizations that combine advanced cooling innovation with resilient supply networks and digital monitoring capabilities will secure stronger operational efficiency and long-term competitive advantage.

Growing installation of MRI, CT, PET, and radiotherapy systems is accelerating demand for advanced thermal management technologies capable of maintaining consistent operating temperatures. More than 30% of newly commissioned premium imaging systems incorporate intelligent cooling controls, while liquid-based solutions improve thermal efficiency by around 20% and reduce service interruptions by nearly 15%. China continues expanding domestic medical equipment manufacturing through industrial modernization initiatives, encouraging suppliers to establish localized production and engineering partnerships. In response, leading companies are investing in compact cooling platforms, smart monitoring software, and integrated thermal modules that enhance equipment reliability. The strategic advantage increasingly lies in delivering complete thermal management ecosystems rather than standalone cooling components.

Medical equipment cooling systems rely on specialized pumps, heat exchangers, electronic controllers, and certified materials, creating procurement challenges during component shortages. Lead times for certain precision thermal components remain approximately 25% longer than pre-disruption levels, while compliance testing can extend product qualification cycles by nearly 18%. Germany-based manufacturers continue facing pressure from specialized material availability and strict medical equipment certification requirements, slowing commercialization timelines. Companies are mitigating these constraints through supplier diversification, regional manufacturing expansion, and long-term procurement agreements. Organizations with broader sourcing strategies and standardized component platforms are reducing operational disruptions while protecting production continuity and delivery commitments.

AI-enabled predictive cooling, digital diagnostics, and connected hospital infrastructure are creating new opportunities beyond conventional hardware supply. Intelligent thermal management platforms reduce unexpected maintenance events by approximately 22%, while automated cooling optimization lowers energy consumption by nearly 14%. South Korea is expanding smart hospital initiatives that encourage integration of connected medical equipment with real-time thermal monitoring systems. Manufacturers are increasing investment in embedded sensors, cloud-based diagnostics, and collaborative technology partnerships to deliver value-added lifecycle services. The emerging competitive opportunity lies in combining cooling hardware with software-driven performance optimization that supports preventive maintenance and long-term equipment utilization.

Deploying advanced cooling technologies consistently across hospitals with different infrastructure standards remains a significant execution challenge. Around 32% of healthcare facilities continue operating legacy equipment that requires customized thermal integration, while engineering installation time increases by approximately 17% for mixed-platform environments. The United States faces increasing pressure to modernize aging hospital infrastructure without disrupting critical clinical operations. Companies must strengthen engineering expertise, interoperability capabilities, and digital commissioning processes while expanding technical service partnerships. Success depends on delivering standardized yet adaptable cooling solutions that maintain performance, simplify integration, and support sustainable long-term deployment across diverse healthcare ecosystems.

Smart Predictive Thermal Control AI-enabled thermal monitoring is becoming standard across premium imaging platforms, with intelligent diagnostics reducing unexpected cooling failures by approximately 20% and lowering service visits by 16%. Rising labor shortages and stricter uptime targets are accelerating software integration, while manufacturers are expanding analytics partnerships to deliver remote performance monitoring and predictive maintenance capabilities.

Localized Manufacturing Expansion Medical equipment producers are restructuring thermal component supply chains, with over 35% of strategic sourcing programs emphasizing regional suppliers to improve delivery reliability. Component localization shortens procurement cycles by nearly 18% while reducing logistics exposure. Companies in the United States and China are increasing manufacturing partnerships and qualifying multiple suppliers to strengthen production continuity.

Compact Liquid Cooling Adoption Advanced liquid cooling architectures are replacing conventional bulky assemblies in next-generation imaging systems, improving heat transfer efficiency by around 22% while reducing equipment footprint by 15%. Increasing installation of space-constrained diagnostic facilities is driving modular product development, prompting suppliers to standardize compact cooling platforms for faster deployment and simplified maintenance.

Energy-Optimized Cooling Platforms Hospitals are prioritizing energy-efficient thermal management as sustainability targets become integrated into procurement decisions. Advanced heat exchangers and variable-speed cooling technologies reduce cooling-related electricity consumption by approximately 14% and extend component operating life by nearly 12%. Manufacturers are accelerating product redesign, automation, and lifecycle service agreements to differentiate through lower operating costs and improved equipment reliability.

Liquid Cooling Systems represent the leading segment because they deliver superior thermal stability, higher heat transfer efficiency, and reliable performance for advanced MRI, CT, and radiotherapy equipment operating under continuous workloads. Nearly 48% of newly installed high-performance diagnostic systems utilize liquid-based thermal management, while equipment downtime declines by approximately 18% compared with conventional air-cooled configurations. Air Cooling Systems remain widely deployed in cost-sensitive installations due to lower maintenance complexity, whereas Compressor-Based Cooling Systems continue supporting high-capacity medical applications requiring precise temperature regulation.

Hybrid Cooling Systems are emerging as the fastest-growing segment by combining liquid and air technologies to improve efficiency while reducing operational energy consumption by around 15%. Thermoelectric Cooling Systems are expanding within compact laboratory instruments where vibration-free operation is essential. Manufacturers are investing in modular cooling architectures, integrated monitoring electronics, and application-specific product development to address evolving healthcare requirements. Investment priorities increasingly favor scalable, intelligent cooling platforms capable of supporting future medical equipment upgrades without significant infrastructure modifications.

MRI Systems account for the largest application share because superconducting magnets and continuous high-power operation require highly stable thermal management for uninterrupted clinical performance. Approximately 42% of advanced medical cooling installations support MRI equipment, while intelligent thermal control reduces operational interruptions by nearly 17%. CT Scanners remain another major application as higher scan throughput increases cooling intensity, and Diagnostic Imaging platforms continue expanding through hospital modernization initiatives emphasizing equipment reliability and patient workflow optimization.

Linear Accelerators represent the fastest-growing application as oncology treatment capacity expands and thermal precision becomes increasingly important for treatment consistency. Laboratory Equipment is also adopting compact cooling technologies to improve analytical accuracy and instrument stability. Equipment manufacturers are integrating predictive diagnostics, modular cooling units, and remote monitoring capabilities to simplify servicing and maximize utilization. Demand is shifting toward integrated thermal ecosystems that improve equipment availability while lowering total maintenance requirements across high-value diagnostic environments.

Hospitals continue to dominate purchasing activity because they operate the broadest range of imaging, diagnostic, and treatment equipment requiring continuous thermal management. Nearly 58% of advanced cooling system deployments are installed within hospital environments, where optimized cooling improves equipment availability by approximately 16% and supports higher patient throughput. Medical Device Manufacturers remain important buyers for factory-level equipment integration, while Research Laboratories prioritize precision cooling for specialized analytical and experimental platforms.

Diagnostic Centers represent the fastest-growing end-user segment as outpatient imaging capacity expands and facilities seek compact, energy-efficient thermal solutions. Specialty Clinics are increasing investment in advanced diagnostic equipment with integrated cooling technologies to improve operational reliability within limited infrastructure footprints. Suppliers are responding through customized product portfolios, long-term service contracts, strategic OEM collaborations, and flexible lifecycle support programs. Competitive differentiation increasingly depends on delivering application-specific cooling systems aligned with the operational requirements of each healthcare environment.

North America accounted for the largest market share at 38.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 6.2% CAGR between 2026 and 2033.

Advanced Healthcare Infrastructure Driving Thermal Innovation

North America maintains the highest deployment concentration for medical equipment cooling due to its extensive installed base of MRI, CT, radiotherapy, and laboratory systems. The region represents approximately 38.4% of global demand, supported by continuous replacement of legacy imaging platforms and rapid adoption of intelligent thermal management technologies. More than 45% of newly commissioned premium diagnostic systems integrate predictive cooling capabilities to improve equipment uptime and reduce maintenance interventions. Medical device manufacturers are strengthening partnerships with thermal engineering specialists while expanding localized component production to improve supply resilience. Hospital modernization programs and increasing adoption of digital service platforms continue to accelerate deployment of energy-efficient cooling solutions across major healthcare networks.

United States Market Outlook: The United States leads regional demand through its extensive healthcare infrastructure, advanced medical device manufacturing ecosystem, and continuous investment in diagnostic technology upgrades. Over 60% of large tertiary hospitals are prioritizing thermal monitoring integration for newly installed imaging equipment, while domestic manufacturers continue expanding production capacity for precision cooling modules. Strategic collaboration between healthcare providers and equipment suppliers is accelerating deployment of intelligent cooling platforms that improve operational reliability and lifecycle efficiency.

Sustainable Engineering and Precision Manufacturing Expansion

Europe remains a major production and technology hub for precision medical cooling systems, supported by advanced engineering capabilities and stringent equipment performance standards. The region contributes nearly 27% of global market activity, with manufacturers emphasizing energy-efficient thermal management and compact system integration. Approximately 36% of new product development programs now prioritize low-energy cooling architectures to align with sustainability objectives. Healthcare modernization initiatives and industrial automation continue driving demand for intelligent cooling technologies, while manufacturers strengthen partnerships with component suppliers to improve product standardization and production efficiency across specialized medical equipment applications.

Germany Market Outlook: Germany serves as the region's industrial backbone through its strong medical technology manufacturing base, engineering expertise, and highly specialized thermal component suppliers. More than 40% of domestic premium imaging equipment production incorporates advanced liquid cooling technologies. Companies continue investing in precision manufacturing, automated assembly, and collaborative product development to strengthen export competitiveness and maintain leadership in high-performance medical equipment cooling solutions.

Manufacturing Scale Accelerates Market Expansion

Asia-Pacific is emerging as the fastest-expanding market due to rapid healthcare infrastructure development, large-scale medical equipment manufacturing, and increasing domestic production capabilities. The region accounts for approximately 29% of global deployment activity, while more than 50% of newly established medical equipment production facilities are located across major industrial hubs in China, Japan, and South Korea. Government-supported healthcare modernization and localized manufacturing initiatives are encouraging suppliers to expand production of compact and intelligent cooling systems. Companies are also increasing investment in regional engineering centers to shorten product development cycles and improve customization for domestic healthcare providers.

China Market Outlook: China continues strengthening its position through expanding medical device manufacturing capacity, integrated supply chains, and large-scale healthcare infrastructure investment. More than 45% of regional production capacity for medical imaging equipment is concentrated within the country, supporting strong demand for advanced thermal management technologies. Domestic manufacturers are increasing automation, expanding supplier partnerships, and accelerating development of locally engineered cooling systems to improve competitiveness across both domestic and export markets.

Healthcare Modernization Supporting Equipment Upgrades

South America is experiencing steady adoption of medical equipment cooling technologies as hospitals expand diagnostic capabilities and replace aging imaging infrastructure. The region represents approximately 5.8% of global demand, with investment increasingly directed toward advanced diagnostic centers and oncology facilities. Nearly 18% of recent healthcare equipment procurement programs have included upgraded thermal management specifications to improve equipment reliability and operating efficiency. International manufacturers are expanding distributor partnerships and localized technical support networks to strengthen after-sales service while addressing infrastructure variability across healthcare facilities.

Brazil Market Outlook: Brazil remains the largest market in the region due to its extensive hospital network, expanding diagnostic imaging capacity, and growing private healthcare investment. Major healthcare providers continue upgrading MRI and CT installations with advanced cooling technologies to improve equipment utilization and reduce operational interruptions. Manufacturers are reinforcing regional service capabilities, technical training programs, and strategic partnerships to improve deployment quality and long-term customer support.

Hospital Infrastructure Investment Reshaping Demand

Middle East & Africa is advancing through sustained investment in healthcare infrastructure, specialty hospitals, and advanced diagnostic facilities. The region contributes approximately 4.8% of global market demand, supported by government-backed healthcare expansion and modernization programs. More than 22% of newly commissioned tertiary healthcare projects include high-performance imaging systems requiring precision cooling technologies. Equipment manufacturers are strengthening regional partnerships, expanding technical service capabilities, and establishing localized support centers to improve installation quality and equipment lifecycle management while addressing diverse operating environments.

Saudi Arabia Market Outlook: Saudi Arabia leads regional deployment through large-scale healthcare transformation initiatives, hospital construction programs, and increasing investment in advanced diagnostic technologies. More than 30% of recently commissioned tertiary healthcare facilities incorporate next-generation imaging systems requiring intelligent thermal management. Global manufacturers are expanding local partnerships, technical training, and service infrastructure to support long-term equipment performance while aligning with national healthcare localization objectives.

The market is led by Vertiv, Schneider Electric, Boyd, Lytron, and Koolance, competing directly against specialized thermal engineering firms and regional cooling system integrators. The top five players collectively account for approximately 41% of the global market, creating a moderately consolidated competitive structure. Global leaders differentiate through integrated thermal technologies, while regional suppliers compete on customization, delivery speed, and project-specific engineering. Liquid cooling platforms improve thermal efficiency by nearly 20%, and predictive monitoring reduces service interventions by around 18%, making technology leadership a decisive advantage. Companies are strengthening competitive positions through localized manufacturing, OEM partnerships, modular product development, and vertical integration of heat exchangers, pumps, and intelligent control systems. Supply-chain localization has shortened component lead times by nearly 15% for diversified manufacturers, intensifying pressure on import-dependent suppliers. Consolidation is increasingly centered on proprietary cooling technologies and lifecycle service capabilities. High certification requirements and precision engineering expertise remain significant entry barriers. Winning requires scalable innovation, resilient supply networks, application-specific customization, and long-term OEM relationships.

Vertiv

Schneider Electric

Boyd

Lytron

Koolance

Laird Thermal Systems

Advanced Cooling Technologies

Rittal

Pfannenberg

Huber Kältemaschinenbau

ThermoTek

Delta Electronics

Advanced liquid cooling, intelligent thermal monitoring, and compact heat exchanger technologies are redefining medical equipment cooling performance. Liquid cooling systems deliver approximately 20% greater heat dissipation than conventional air-based platforms while reducing thermal fluctuations by nearly 18%. Around 45% of newly developed premium imaging systems incorporate intelligent cooling controls, enabling continuous temperature optimization and higher equipment availability. Healthcare equipment manufacturers benefit through improved reliability, longer component life, and lower maintenance requirements.

Emerging technologies include AI-driven predictive diagnostics, digital twin-based thermal simulation, advanced thermoelectric modules, and high-efficiency microchannel heat exchangers. AI-enabled monitoring reduces unexpected maintenance events by approximately 22%, while digital thermal optimization lowers cooling energy consumption by nearly 14%. Compared with legacy rule-based cooling systems, predictive thermal management improves operational efficiency by roughly 17%. OEMs and specialized cooling technology providers gain the strongest competitive advantage by integrating software analytics with precision cooling hardware and remote lifecycle management services.

Between 2026 and 2028, modular liquid cooling architectures, edge-connected monitoring platforms, and low-power thermal materials will accelerate commercial deployment across diagnostic imaging, radiotherapy, and laboratory equipment. More than 38% of next-generation medical platforms are expected to incorporate integrated intelligent cooling modules, enabling faster servicing, standardized deployment, and enhanced equipment resilience. Companies investing early in AI-enabled thermal ecosystems, compact cooling platforms, and interoperable digital diagnostics will strengthen operational performance, reduce lifecycle costs, and secure long-term differentiation in increasingly technology-driven healthcare infrastructure.

March 2025 Vertiv introduced the CoolLoop Trim Cooler, a hybrid heat rejection system supporting both liquid and air cooling for high-density thermal applications. The platform improves deployment flexibility across diverse operating conditions while supporting higher cooling efficiency for advanced infrastructure.

September 2025 Schneider Electric unveiled its integrated Motivair liquid cooling portfolio following the Motivair acquisition, combining coolant distribution units, heat exchangers, and cooling loops into one platform. The portfolio leverages over 15 years of liquid-cooling expertise, strengthening end-to-end thermal management capabilities. Source: se.com

September 2025 Boyd announced delivery of 5 million liquid cold plates manufactured through its global production network, demonstrating high-volume thermal manufacturing capability. The milestone reinforces supply reliability and supports faster deployment of precision cooling technologies across advanced equipment applications. Source: boydcorp.com

April 2026 Vertiv acquired Strategic Thermal Labs to strengthen chip-level liquid cooling engineering and high-density thermal validation capabilities. The acquisition expands cold-plate design expertise and enhances system-level performance, accelerating advanced thermal solution development for next-generation cooling applications. Source: vertiv.com

This report delivers a comprehensive assessment of the Medical Equipment Cooling Market across Air Cooling Systems, Liquid Cooling Systems, Thermoelectric Cooling Systems, Compressor-Based Cooling Systems, and Hybrid Cooling Systems. It evaluates demand across MRI Systems, CT Scanners, Linear Accelerators, Diagnostic Imaging, and Laboratory Equipment, together with Hospitals, Diagnostic Centers, Research Laboratories, Medical Device Manufacturers, and Specialty Clinics. The analysis covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, while examining deployment trends, technology adoption, and competitive positioning across more than 10 leading industry participants.

The report provides strategic insights into intelligent thermal management, liquid cooling innovation, predictive monitoring, compact cooling architectures, and energy-efficient system integration. It highlights segment adoption patterns, operational deployment priorities, evolving procurement strategies, and enterprise investment direction between 2026 and 2033. The assessment supports market entry planning, product portfolio optimization, partnership evaluation, regional expansion decisions, competitive benchmarking, and long-term business strategy through detailed analysis of technology shifts, end-user demand, and emerging application opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 474.1 Million |

Market Revenue in 2033 | USD 695.14 Million |

CAGR (2026 - 2033) | 4.9% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Vertiv, Schneider Electric, Boyd, Lytron, Koolance, Laird Thermal Systems, Advanced Cooling Technologies, Rittal, Pfannenberg, Huber Kältemaschinenbau, ThermoTek, Delta Electronics |

Customization & Pricing | Available on Request (10% Customization is Free) |