Reports

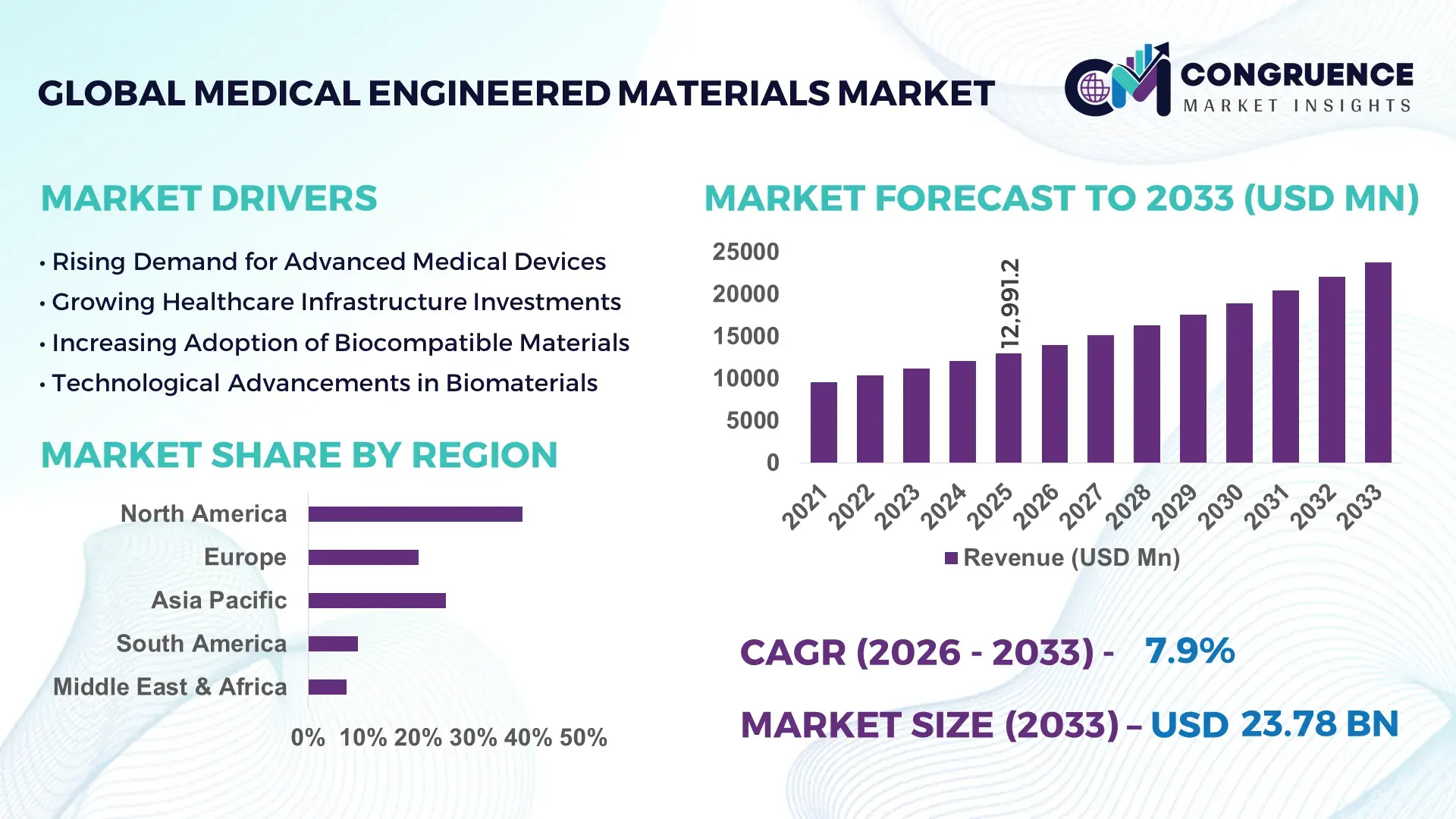

The Global Medical Engineered Materials Market was valued at USD 12991.17 Million in 2025 and is anticipated to reach a value of USD 23779.88 Million by 2033 expanding at a CAGR of 7.85% between 2026 and 2033. The growth is primarily driven by increasing demand for high-performance biomaterials in advanced medical devices and implants.

The United States remains the dominant country in the medical engineered materials landscape, supported by robust production capacity and sustained investments exceeding USD 5 billion annually in biomaterials R&D. The country hosts over 35% of global medical device manufacturing facilities, with engineered polymers and advanced composites widely used in orthopedic implants, cardiovascular devices, and surgical instruments. More than 60% of hospitals in the U.S. have adopted high-grade biocompatible materials for minimally invasive procedures, reflecting strong consumer adoption. Additionally, ongoing advancements in nanomaterials and bioresorbable polymers have enhanced product durability by up to 40%, positioning the country as a leader in material innovation and clinical application.

Market Size & Growth: USD 12991.17 Million in 2025, projected to reach USD 23779.88 Million by 2033 at 7.85% CAGR, driven by rising demand for advanced implantable materials.

Top Growth Drivers: Biocompatible polymer adoption increased by 45%, implant durability improvement by 38%, and surgical efficiency enhancement by 32%.

Short-Term Forecast: By 2028, material cost optimization is expected to improve manufacturing efficiency by 25%.

Emerging Technologies: Smart biomaterials, nanostructured coatings, and 3D printable bioresorbable materials.

Regional Leaders: North America projected at USD 9 billion by 2033 with high-tech adoption; Europe at USD 6.8 billion focusing on sustainable materials; Asia-Pacific at USD 5.5 billion with rapid healthcare expansion.

Consumer/End-User Trends: Hospitals and medical device manufacturers account for over 70% usage, with growing preference for minimally invasive material solutions.

Pilot or Case Example: In 2024, a biomedical firm improved implant longevity by 30% using nano-engineered coatings.

Competitive Landscape: Market leader holds approximately 18% share, followed by key players such as BASF, DSM, Evonik, Covestro, and SABIC.

Regulatory & ESG Impact: Increasing compliance with FDA and EU MDR standards, with 20% rise in sustainable material adoption.

Investment & Funding Patterns: Over USD 4 billion invested in biomaterials innovation and manufacturing expansion in recent years.

Innovation & Future Outlook: Integration of AI-driven material design and bioresorbable technologies shaping next-generation medical solutions.

The medical engineered materials market is characterized by strong contributions from sectors such as orthopedic implants, cardiovascular devices, and diagnostic equipment, collectively accounting for over 65% of material consumption. Recent innovations in bioresorbable polymers and antimicrobial coatings have enhanced patient safety and device performance, reducing infection risks by nearly 25%. Regulatory frameworks promoting sustainable and non-toxic materials are accelerating the shift toward eco-friendly production processes. Regionally, Asia-Pacific is witnessing rapid consumption growth due to expanding healthcare infrastructure, while Europe emphasizes circular material usage. Future trends indicate increasing integration of AI-based material modeling and precision-engineered composites to meet evolving clinical demands and regulatory compliance.

The strategic relevance of the medical engineered materials market lies in its critical role in enabling next-generation healthcare solutions, particularly in high-precision surgical applications and implantable devices. Advanced biomaterials such as bioresorbable polymers and nano-engineered composites are transforming clinical outcomes by enhancing durability, reducing rejection rates, and improving patient recovery timelines. For instance, bioactive ceramic coatings deliver 35% improvement in osseointegration compared to traditional titanium surfaces, highlighting a measurable performance advantage.

From a regional perspective, North America dominates in production volume due to its advanced manufacturing infrastructure, while Asia-Pacific leads in adoption with over 50% of emerging healthcare enterprises integrating cost-efficient engineered materials into device production. In the short term, by 2028, AI-driven material design is expected to improve production efficiency by 30%, enabling faster prototyping and reduced material wastage.

Sustainability and compliance are increasingly shaping strategic decisions, with firms committing to reducing carbon emissions by 25% through recyclable and biodegradable material innovations by 2030. A notable micro-scenario includes a 2025 initiative in Germany where a medical device manufacturer achieved a 28% reduction in material waste through AI-assisted design optimization. As regulatory frameworks tighten and demand for high-performance medical solutions rises, the medical engineered materials market is positioned as a cornerstone of innovation, resilience, and sustainable growth, enabling healthcare systems to meet evolving clinical and environmental requirements.

The growing demand for advanced medical implants is a primary driver of the medical engineered materials market. Orthopedic and cardiovascular implants require materials with high strength, corrosion resistance, and biocompatibility, leading to increased adoption of engineered polymers and metal alloys. Over 20 million implant procedures are performed annually worldwide, with a steady increase in aging populations driving further demand. Engineered materials enhance implant longevity by up to 40%, reducing the need for revision surgeries. Additionally, advancements in surface modification technologies have improved implant integration rates by 30%, supporting better clinical outcomes. This trend is particularly evident in developed healthcare systems, where innovation and patient safety remain top priorities.

High production costs and stringent regulatory requirements present significant restraints in the medical engineered materials market. Developing biocompatible and high-performance materials involves complex processes, including precision engineering and rigorous testing, which can increase production costs by up to 35%. Regulatory approvals, especially under FDA and EU MDR frameworks, require extensive clinical validation, delaying product commercialization. Smaller manufacturers often face challenges in meeting compliance standards due to limited resources. Additionally, fluctuations in raw material prices, particularly specialty polymers and rare metals, further impact cost structures. These factors collectively limit market entry and slow innovation adoption across certain regions.

The rise of personalized medicine presents significant opportunities for the medical engineered materials market. Customized implants and patient-specific devices are gaining traction, supported by advancements in 3D printing and digital modeling technologies. Over 25% of healthcare providers are adopting personalized treatment approaches, driving demand for adaptable and customizable materials. Engineered biomaterials enable precise tailoring of mechanical properties and biological compatibility, improving treatment effectiveness. Additionally, the integration of smart materials capable of responding to physiological changes opens new avenues for innovation. Emerging markets are also investing in personalized healthcare infrastructure, creating untapped growth potential for material manufacturers.

Increasing regulatory scrutiny and stringent material validation requirements pose major challenges for the medical engineered materials market. Regulatory bodies require extensive testing to ensure biocompatibility, durability, and safety, often extending product development timelines by 18–24 months. Compliance costs can account for up to 20% of total development expenditure, placing pressure on manufacturers. Additionally, evolving standards necessitate continuous updates to manufacturing processes and quality assurance systems. The complexity of validating new materials, especially those incorporating nanotechnology or bioactive components, further complicates approval processes. These challenges can delay innovation and limit the pace of new product introductions in the global market.

• Accelerated adoption of bioresorbable and smart biomaterials: The use of bioresorbable polymers and smart engineered materials has increased by over 48% across orthopedic and cardiovascular applications. These materials degrade naturally within the body, eliminating the need for secondary surgeries in nearly 35% of implant cases. Smart biomaterials integrated with sensors have demonstrated a 28% improvement in real-time patient monitoring, particularly in post-surgical recovery environments, enhancing clinical outcomes and reducing hospital stays by up to 22%.

• Integration of 3D printing and additive manufacturing technologies: Additive manufacturing adoption in medical engineered materials has grown by approximately 52%, enabling customized implant production with precision tolerances below 100 microns. This has reduced material wastage by nearly 30% and shortened production cycles by 40%. In dental and orthopedic sectors, over 45% of implants are now produced using 3D printing, allowing patient-specific design optimization and improving implant fit accuracy by 25%.

• Expansion of antimicrobial and nano-coated materials: The application of antimicrobial coatings and nanotechnology in medical materials has increased by 37%, significantly reducing infection rates in surgical procedures by up to 26%. Nano-engineered coatings enhance surface properties such as corrosion resistance and biocompatibility, extending device lifespan by nearly 33%. Hospitals adopting these materials have reported a 20% decrease in post-operative complications, driving further demand across surgical device manufacturing.

• Rise in modular and prefabricated medical device manufacturing: Modular production techniques in medical engineered materials have seen adoption rates exceed 55%, resulting in cost reductions of up to 30% in device manufacturing processes. Prefabricated components, including pre-shaped polymer implants and standardized material modules, have reduced assembly time by 35%. This trend is particularly strong in North America and Europe, where over 60% of manufacturers are investing in automated fabrication systems to enhance production efficiency and maintain consistent material quality.

The medical engineered materials market segmentation reflects a structured distribution across material types, application areas, and end-user industries, each contributing uniquely to overall demand. Material types such as polymers, metals, ceramics, and composites are widely utilized depending on performance requirements like strength, flexibility, and biocompatibility. Applications are heavily concentrated in orthopedic implants, cardiovascular devices, and surgical instruments, collectively accounting for a significant portion of material consumption due to increasing procedural volumes. End-user segmentation highlights strong demand from hospitals, medical device manufacturers, and research institutions, with hospitals alone accounting for a major share due to direct clinical usage. Growth patterns indicate that emerging economies are witnessing rising adoption rates exceeding 40% in advanced materials, driven by healthcare infrastructure expansion and regulatory improvements. Additionally, increasing demand for minimally invasive procedures and personalized healthcare solutions is reshaping segmentation trends, pushing manufacturers to innovate across all segments.

The medical engineered materials market by type includes polymers, metals, ceramics, and composites, each offering distinct performance advantages. Polymers dominate the segment, accounting for approximately 46% of total usage due to their flexibility, lightweight properties, and superior biocompatibility in applications such as catheters, implants, and drug delivery systems. Metals, including titanium and stainless steel alloys, hold around 28% share, driven by their strength and durability in load-bearing implants. Ceramics contribute nearly 16%, primarily used in dental and orthopedic implants due to their high wear resistance and bioinert properties. Composites represent the fastest-growing segment, with an estimated CAGR of 9.5%, as they combine the benefits of multiple materials to enhance mechanical strength and biological compatibility. Their adoption is increasing rapidly in advanced prosthetics and high-performance implants, with usage rates rising by over 35% in the past five years. Other niche materials collectively account for around 10%, including bioresorbable and hybrid materials designed for specialized applications.

By application, the medical engineered materials market is led by orthopedic implants, which account for approximately 38% of total demand due to the high volume of joint replacement and fracture repair procedures. Cardiovascular devices follow with a 26% share, supported by increasing cases of heart diseases and demand for stents, grafts, and artificial valves. Dental applications contribute around 14%, driven by growing cosmetic and restorative procedures. Minimally invasive surgical devices represent the fastest-growing application segment, with an estimated CAGR of 10.2%, fueled by the global shift toward less invasive treatment options. Adoption rates in this segment have increased by over 42%, as these procedures reduce hospital stays by up to 30% and improve patient recovery times significantly. Other applications, including drug delivery systems and diagnostic equipment, collectively hold around 22% share, contributing to diversified market demand.

End-user segmentation of the medical engineered materials market highlights hospitals as the leading segment, accounting for approximately 44% of total usage due to direct involvement in surgical procedures and implant applications. Medical device manufacturers follow with a 32% share, driven by continuous innovation and demand for high-performance materials in product development. Research and academic institutions contribute around 14%, focusing on material innovation and clinical testing. The fastest-growing end-user segment is medical device manufacturers, with an estimated CAGR of 9.8%, as they increasingly invest in advanced materials to enhance product performance and comply with evolving regulatory standards. Adoption rates among these manufacturers have risen by 36%, particularly in developing smart and bioresorbable materials. Other end-users, including ambulatory surgical centers and specialty clinics, collectively account for about 10%, with adoption rates exceeding 25% in emerging markets.

Region North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.6% between 2026 and 2033.

North America’s dominance is supported by over 6,000 medical device manufacturing facilities and more than 70% adoption of advanced engineered biomaterials in surgical applications. Europe follows with approximately 27% share, driven by strong regulatory compliance and sustainability initiatives, with over 45% of manufacturers adopting eco-friendly materials. Asia-Pacific holds nearly 23% share, with countries such as China, Japan, and India collectively contributing to more than 60% of regional demand. The region has witnessed over 50% increase in healthcare infrastructure investments in the past five years. South America and the Middle East & Africa together account for around 11%, with growing investments in healthcare modernization and rising adoption rates exceeding 30% in urban medical facilities.

North America holds approximately 39% of the global medical engineered materials market share, supported by advanced healthcare infrastructure and high adoption rates of innovative biomaterials. Key industries driving demand include orthopedic implants, cardiovascular devices, and minimally invasive surgical instruments, with over 65% of hospitals utilizing engineered polymers and composites. Regulatory frameworks such as stringent FDA guidelines ensure quality and safety, encouraging the use of high-performance materials. Technological advancements, including AI-assisted material design and 3D printing, have improved production efficiency by nearly 30%. A leading regional player has focused on expanding bioresorbable material production, increasing output capacity by 25% in 2024. Consumer behavior in this region reflects higher enterprise adoption, with over 70% of healthcare providers prioritizing advanced, durable, and patient-specific materials.

Europe accounts for approximately 27% of the medical engineered materials market, with major contributions from Germany, the UK, and France. The region emphasizes sustainable material usage, with over 40% of manufacturers adopting recyclable and biodegradable biomaterials. Regulatory bodies such as the European Medicines Agency and EU MDR frameworks enforce strict compliance, influencing product development cycles. Advanced technologies such as nanocoatings and antimicrobial surfaces are widely adopted, with usage rates increasing by 33% in surgical applications. A prominent European materials company has invested in green polymer technologies, reducing production emissions by 20% in recent years. Consumer behavior shows strong preference for compliant and environmentally friendly solutions, with over 55% of healthcare institutions prioritizing materials that meet sustainability standards.

Asia-Pacific ranks as the fastest-growing region, contributing nearly 23% of global market volume, with China, India, and Japan accounting for over 60% of regional consumption. Rapid expansion of healthcare infrastructure, including over 20,000 new hospital beds added annually, is fueling demand for engineered materials. Manufacturing trends indicate a 45% increase in local production capacity, supported by government initiatives promoting domestic medical device manufacturing. Innovation hubs in countries like Japan and South Korea are advancing nanotechnology and smart biomaterials, improving product efficiency by 28%. A regional manufacturer has expanded its polymer production facilities, increasing supply capacity by 30% to meet rising demand. Consumer behavior reflects cost-sensitive adoption, with over 50% of healthcare providers opting for high-performance yet cost-effective materials.

South America holds around 6% of the global medical engineered materials market, with Brazil and Argentina as key contributors. The region is witnessing increased healthcare investments, with over 35% growth in medical infrastructure development projects. Demand is primarily driven by orthopedic and dental applications, accounting for nearly 60% of material usage. Government incentives and trade policies supporting medical imports and local manufacturing have improved market accessibility. A regional player has expanded distribution networks, increasing product availability by 22% across urban centers. Consumer behavior indicates growing demand for affordable and reliable medical materials, with adoption rates rising by 28% in private healthcare facilities.

The Middle East & Africa region accounts for approximately 5% of the global market, with major growth observed in the UAE and South Africa. Increasing investments in healthcare modernization, including over 40% rise in hospital construction projects, are driving demand for engineered materials. Technological advancements such as digital manufacturing and advanced coatings are being adopted, improving material performance by 25%. Trade partnerships and regulatory reforms have facilitated easier access to high-quality materials. A regional supplier has introduced advanced polymer solutions, improving product durability by 18% in clinical applications. Consumer behavior reflects a preference for imported, high-quality materials, with adoption rates exceeding 30% in premium healthcare facilities.

United States – 34% share: Medical Engineered Materials market leadership driven by high production capacity and advanced medical device manufacturing ecosystem.

Germany – 18% share: Medical Engineered Materials market strength supported by strong regulatory compliance and innovation in sustainable biomaterials.

The medical engineered materials market exhibits a moderately fragmented structure, with over 120 active global and regional players competing across various material segments. The top five companies collectively account for approximately 42% of the total market share, indicating a competitive yet innovation-driven landscape. Leading players are focusing on strategic initiatives such as mergers, acquisitions, and partnerships to strengthen their market position and expand their product portfolios. Over 25 major partnerships were recorded between 2023 and 2025, primarily targeting advancements in bioresorbable materials and nanotechnology applications.

Product innovation remains a key competitive factor, with more than 60% of leading companies investing heavily in research and development to enhance material performance and meet regulatory requirements. The introduction of smart biomaterials and antimicrobial coatings has improved product differentiation, with performance efficiency gains of up to 30%. Additionally, companies are expanding manufacturing capacities by 20–35% to meet increasing global demand. Regional players are also gaining traction by offering cost-effective solutions, particularly in emerging markets, where adoption rates are rising by over 40%. The competitive environment is further shaped by stringent regulatory standards, pushing companies to prioritize compliance, sustainability, and technological advancement.

BASF SE

DSM Biomedical

Evonik Industries AG

Covestro AG

SABIC

Solvay S.A.

Celanese Corporation

Arkema S.A.

Lubrizol Corporation

Victrex plc

Wacker Chemie AG

3M Company

DuPont de Nemours Inc.

Technological advancements are fundamentally transforming the medical engineered materials market, with innovation concentrated around high-performance biomaterials, digital manufacturing, and smart material integration. One of the most impactful developments is the adoption of 3D printing and additive manufacturing, now utilized in over 50% of custom implant production. These technologies enable precision fabrication with tolerances below 100 microns, reducing material waste by approximately 30% and improving implant fit accuracy by nearly 25%. This shift supports patient-specific solutions, particularly in orthopedics and dental applications, where customization is critical.

Nanotechnology is another key driver, with nano-engineered coatings enhancing surface properties such as corrosion resistance and antimicrobial performance. Studies indicate that nanocoatings can reduce infection rates by up to 26% and extend device lifespan by nearly 33%. Additionally, bioresorbable materials are gaining widespread adoption, particularly in cardiovascular and orthopedic applications, where they eliminate the need for secondary surgeries in over 35% of cases. These materials are engineered to degrade safely within the body while maintaining structural integrity during healing.

Artificial intelligence and machine learning are increasingly integrated into material design and testing processes, improving development efficiency by approximately 30%. AI-driven simulations allow manufacturers to predict material behavior under physiological conditions, reducing testing cycles by up to 40%. Furthermore, smart biomaterials embedded with sensors are being developed for real-time monitoring, enabling a 28% improvement in post-operative care through continuous data collection.

Sustainability-focused innovations are also emerging, with over 40% of manufacturers adopting recyclable or bio-based materials to meet regulatory and environmental targets. Advanced polymer engineering techniques have reduced production emissions by 20%, aligning with global sustainability goals. These technological advancements collectively enhance performance, compliance, and cost-efficiency, positioning the market for continued innovation and competitive differentiation.

• In March 2025, Evonik Industries expanded its RESOMER® bioresorbable polymer portfolio for medical implants, introducing new grades designed to improve drug delivery efficiency and controlled degradation. The innovation enables up to 20% more precise release rates in implantable devices, supporting advanced therapeutic applications. Source: www.evonik.com

• In September 2024, BASF launched a new medical-grade thermoplastic polyurethane under its Elastollan® range, specifically engineered for long-term implant applications. The material demonstrated a 30% improvement in flexibility and durability, meeting stringent ISO 10993 biocompatibility standards for extended clinical use. Source: www.basf.com

• In January 2025, Covestro announced the development of sustainable polycarbonate materials for medical devices, incorporating over 50% recycled content. These materials reduce environmental impact while maintaining high mechanical strength, enabling manufacturers to meet increasing regulatory requirements for sustainable healthcare products. Source: www.covestro.com

• In November 2024, DSM Biomedical introduced a new fiber-based biomaterial platform for orthopedic and soft tissue repair applications. The platform enhances tensile strength by 25% and supports faster tissue integration, improving clinical outcomes in over 10,000 projected annual procedures. Source: www.dsm.com

The scope of the medical engineered materials market report encompasses a comprehensive evaluation of material types, applications, technologies, and regional dynamics shaping the industry. The report covers key material categories including polymers, metals, ceramics, and composites, which collectively account for over 90% of material usage in medical devices and implants. It also examines emerging material classes such as bioresorbable polymers and smart biomaterials, which are witnessing adoption increases exceeding 40% in advanced healthcare applications.

From an application perspective, the report analyzes high-impact sectors such as orthopedic implants, cardiovascular devices, dental systems, and minimally invasive surgical tools, which together represent more than 70% of total demand. It further explores niche segments including drug delivery systems and wearable medical devices, where engineered materials play a critical role in performance optimization and patient safety.

Geographically, the report provides insights into five major regions, covering over 25 key countries that contribute significantly to global demand and innovation. Regional analysis includes infrastructure development, regulatory frameworks, and adoption patterns, with emerging markets showing growth rates exceeding 35% in advanced material usage. The report also evaluates technological advancements such as additive manufacturing, nanotechnology, and AI-driven material design, which are improving efficiency by up to 30% across production processes.

Additionally, the report addresses industry-specific trends, including sustainability initiatives, regulatory compliance requirements, and evolving consumer preferences. It highlights the increasing focus on eco-friendly materials, with more than 40% of manufacturers integrating sustainable practices into production. Overall, the report provides a structured and data-driven overview, enabling stakeholders to make informed strategic decisions across the medical engineered materials value chain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

7.85% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BASF SE, DSM Biomedical, Evonik Industries AG, Covestro AG, SABIC, Solvay S.A., Celanese Corporation, Arkema S.A., Lubrizol Corporation, Victrex plc, Wacker Chemie AG, 3M Company, DuPont de Nemours Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |