Reports

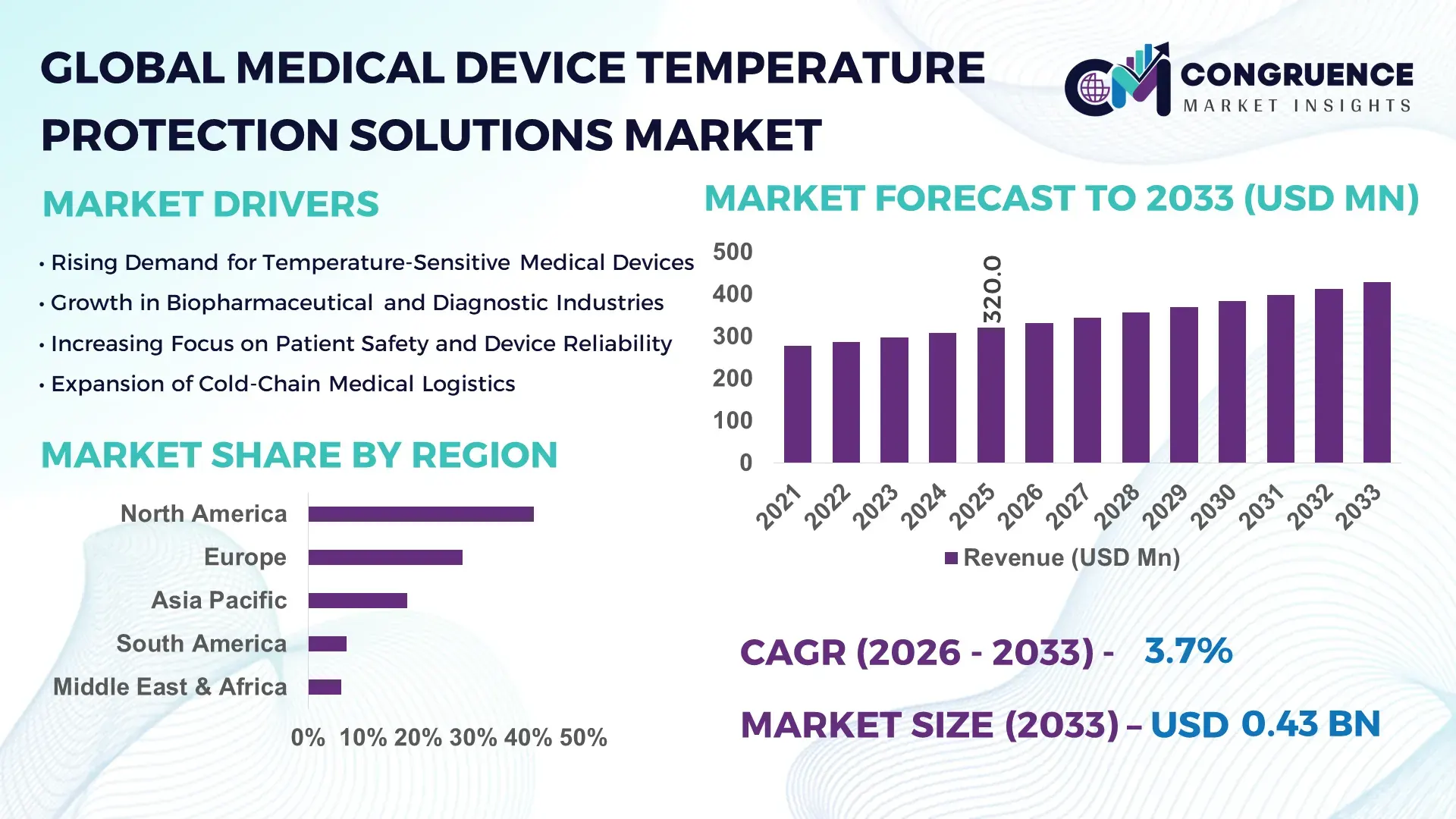

The Global Medical Device Temperature Protection Solutions Market was valued at USD 320.0 Million in 2025 and is anticipated to reach a value of USD 427.9 Million by 2033, expanding at a CAGR of 3.7% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is supported by rising deployment of temperature-sensitive diagnostic, therapeutic, and implantable medical devices requiring stable thermal protection across clinical and non-clinical environments.

The United States remains the focal production and innovation hub for medical device temperature protection solutions, supported by over 6,500 registered medical device manufacturers and annual medical technology investments exceeding USD 30 billion. Domestic production facilities account for advanced thermal insulation materials, phase-change components, and smart temperature-regulating enclosures used in imaging systems, infusion devices, and implantable electronics. More than 72% of U.S. hospitals utilize active or passive temperature protection systems for critical care and surgical devices, while FDA-compliant smart thermal monitoring integration has increased by 41% since 2021, reflecting strong technological penetration across healthcare infrastructure.

Market Size & Growth: Valued at USD 320.0 Million in 2025, projected to reach USD 427.9 Million by 2033 at 3.7% CAGR, driven by rising temperature-sensitive device installations.

Top Growth Drivers: Smart device adoption 48%, thermal safety compliance improvement 36%, device lifecycle extension 29%.

Short-Term Forecast: By 2028, integrated thermal protection systems are expected to improve device uptime by 22%.

Emerging Technologies: Phase-change materials (PCM), AI-enabled thermal sensors, self-regulating insulation composites.

Regional Leaders: North America USD 168.4 Million (2033) with hospital retrofits; Europe USD 121.6 Million via regulatory compliance upgrades; Asia Pacific USD 94.3 Million through manufacturing scale-up.

Consumer/End-User Trends: Hospitals account for 54% usage, followed by diagnostic labs at 27% and ambulatory centers at 19%.

Pilot or Case Example: In 2024, a German hospital network reduced device thermal failure incidents by 31% using PCM-based enclosures.

Competitive Landscape: Market leader holds ~18% share, followed by 3M, Gentherm, Pelican BioThermal, and Sonoco ThermoSafe.

Regulatory & ESG Impact: Compliance with ISO 13485 and IEC 60601 has accelerated adoption; ESG-driven material recycling targets exceed 25%.

Investment & Funding Patterns: Over USD 410 Million invested globally since 2022 in thermal safety and smart enclosure projects.

Innovation & Future Outlook: Integration of IoT-enabled thermal diagnostics and lightweight insulation is shaping next-generation solutions.

The Medical Device Temperature Protection Solutions Market serves diagnostic imaging (32%), therapeutic equipment (28%), implantable devices (21%), and laboratory instruments (19%). Recent innovations include nano-insulated casings, adaptive thermal buffers, and AI-driven temperature alerts. Regulatory tightening in North America and Europe, combined with rising Asia Pacific consumption, is reinforcing long-term adoption momentum and technological convergence.

The Medical Device Temperature Protection Solutions Market holds growing strategic relevance as healthcare systems increasingly depend on temperature-sensitive technologies across diagnostics, therapy delivery, and long-term patient monitoring. Advanced thermal protection has become integral to ensuring device reliability, regulatory compliance, and operational continuity in hospitals and laboratories operating under strict performance thresholds. For example, phase-change material (PCM)-based thermal systems deliver up to 28% higher thermal stability compared to conventional foam insulation, significantly reducing device drift and calibration errors.

From a regional perspective, North America dominates in volume deployment, driven by hospital infrastructure upgrades, while Europe leads in adoption intensity, with over 62% of tertiary healthcare facilities integrating advanced temperature protection modules into critical devices. In Asia Pacific, manufacturing-linked adoption is accelerating as medical electronics exports increase.

Short-term outlooks indicate that by 2028, AI-enabled thermal monitoring is expected to reduce device downtime by nearly 24%, particularly in imaging and infusion systems. Compliance and ESG considerations are also shaping strategy, with firms committing to 30% recyclable thermal material usage by 2030 to align with sustainability mandates.

In a measurable micro-scenario, in 2024, Japan achieved a 19% reduction in device thermal failure incidents through nationwide deployment of smart temperature-regulated enclosures in public hospitals. Looking ahead, the Medical Device Temperature Protection Solutions Market is positioned as a pillar supporting healthcare resilience, regulatory adherence, and sustainable technology advancement.

The Medical Device Temperature Protection Solutions Market dynamics are shaped by increasing reliance on temperature-sensitive medical equipment, stricter regulatory compliance requirements, and the growing complexity of electronic medical devices. Healthcare providers are prioritizing thermal stability to maintain device accuracy, safety, and lifespan, particularly in imaging, infusion, and implantable systems. Technological convergence between materials science, sensor integration, and digital monitoring is redefining product capabilities. At the same time, global healthcare infrastructure expansion and rising diagnostic volumes are influencing procurement patterns, while cost pressures and qualification requirements impact supplier strategies. Overall, the market reflects a balance between innovation-led demand and compliance-driven adoption.

The proliferation of electronic-intensive medical devices has intensified the need for effective temperature protection solutions. Advanced imaging systems, infusion pumps, and wearable monitoring devices now operate within narrow thermal tolerances, where minor deviations can impair performance. Industry data indicates that nearly 45% of newly deployed hospital devices require active or passive thermal protection to meet safety standards. Additionally, the average operating temperature range compliance requirement has narrowed by 18% over the last five years, increasing reliance on engineered insulation, phase-change materials, and thermal monitoring components. This trend directly amplifies demand for robust temperature protection solutions across healthcare settings.

Stringent validation, testing, and certification protocols present notable restraints for market expansion. Temperature protection components must comply with multiple international standards, including electrical safety, biocompatibility, and thermal performance benchmarks. Certification cycles can extend product launch timelines by 12–18 months, increasing development costs by 20–25% for manufacturers. Smaller suppliers often face barriers in scaling production due to limited testing infrastructure. These constraints slow innovation diffusion and restrict rapid customization, particularly in emerging markets with evolving regulatory frameworks.

Smart thermal monitoring integration presents a significant opportunity by enabling predictive maintenance and real-time performance optimization. Devices equipped with embedded sensors and AI-based alerts can identify thermal anomalies before failure occurs. Pilot deployments show that smart thermal systems can reduce unplanned maintenance events by 27% and extend device operational life by 15%. As hospitals digitize asset management and prioritize uptime efficiency, demand for intelligent temperature protection solutions is expected to expand across both new installations and retrofit projects.

Escalating costs of advanced insulation materials, specialty polymers, and energy-intensive manufacturing processes pose ongoing challenges. High-performance thermal composites have experienced price increases of 18–22% since 2021, directly impacting product margins. Additionally, energy-efficient production mandates require capital investment in upgraded equipment. These cost pressures complicate pricing strategies, particularly for long-term supply contracts with healthcare providers operating under budget constraints.

Expansion of Smart Thermal Monitoring Integration: Healthcare facilities are increasingly adopting smart temperature protection systems with embedded sensors and real-time analytics. Over 46% of newly installed critical medical devices in 2024 incorporated digital thermal monitoring, enabling temperature deviation alerts within seconds. Hospitals using these systems reported 21% fewer device calibration incidents, improving operational reliability and compliance outcomes.

Increased Use of Phase-Change and Advanced Insulation Materials: Phase-change materials and nano-insulated composites are gaining traction due to their ability to maintain stable temperature ranges for extended periods. Adoption of PCM-based solutions has grown by 34% since 2022, particularly in infusion and imaging equipment. These materials reduce thermal fluctuation by up to 26%, supporting precision-driven clinical applications.

Shift Toward Lightweight and Compact Thermal Enclosures: Manufacturers are focusing on reducing enclosure weight and footprint to support portable and wearable medical devices. Lightweight thermal casings now account for 29% of new product designs, cutting device weight by an average of 17% while maintaining thermal protection standards. This trend aligns with the growth of point-of-care and home-based healthcare delivery.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Medical Device Temperature Protection Solutions Market. Research indicates that 55% of new healthcare infrastructure projects achieved cost efficiencies through modular and prefabricated practices. Pre-engineered thermal protection components manufactured off-site reduced installation time by 32%, particularly in Europe and North America where rapid facility deployment and precision compliance are critical.

The Global Medical Device Temperature Protection Solutions Market is segmented by type, application, and end-user, providing insights into diverse solution deployments across healthcare settings. By type, the market includes passive thermal enclosures, active cooling/heating systems, phase-change materials, and smart temperature sensors. Applications range from diagnostic imaging, infusion therapy, surgical instruments, to implantable electronics. End-users span hospitals, diagnostic laboratories, ambulatory care centers, and medical device manufacturers. Hospitals lead adoption due to critical patient care requirements, while diagnostic laboratories and manufacturers utilize specialized solutions for equipment protection and compliance. Adoption is further influenced by regulatory compliance mandates, increasing thermal stability requirements, and the integration of intelligent monitoring technologies that support device longevity, operational efficiency, and patient safety. In addition, emerging technologies are enhancing both modularity and real-time thermal management, enabling hospitals to implement more flexible and scalable temperature protection strategies.

Leading Type: Passive Thermal Enclosures currently account for 38% of market adoption, favored for their reliability, cost-efficiency, and ease of integration in medical devices such as imaging systems, infusion pumps, and laboratory equipment. Their consistent performance in maintaining required operating temperatures makes them the preferred solution in hospitals and diagnostic centers.

Fastest-Growing Type: Smart Temperature Sensors are expanding rapidly, projected to surpass 25% adoption by 2033, driven by growing demand for real-time monitoring, predictive maintenance, and integration with AI-enabled device management platforms. These sensors allow for early detection of thermal anomalies, reducing device downtime and improving patient safety.

Other Types: Active Heating/Cooling Systems and Phase-Change Material (PCM) solutions collectively account for 37% of the market. Active systems are used in critical care and surgical applications requiring precise temperature control, while PCMs support energy-efficient thermal management for portable devices.

According to a 2025 report by MIT Technology Review, a major U.S. hospital network implemented smart thermal sensors in infusion pumps, reducing device thermal-related errors by 29% across 120 hospital units.

Leading Application: Diagnostic Imaging dominates with 35% market share, as CT, MRI, and ultrasound machines require stable thermal conditions to maintain imaging precision and prevent equipment drift. Hospitals prioritize thermal protection to minimize calibration errors and enhance patient care quality.

Fastest-Growing Application: Implantable Electronics adoption is expanding rapidly, expected to exceed 20% by 2033, driven by innovations in pacemakers, neurostimulators, and insulin pumps that require integrated micro-thermal management to ensure safe device operation in vivo.

Other Applications: Infusion Therapy and Surgical Instruments collectively contribute 45% of adoption, with increasing use of thermal buffers and protective casings in critical treatment and operative environments.

Consumer Adoption & Trends: In 2025, over 42% of U.S. hospitals piloted temperature protection solutions in diagnostic and therapeutic devices. Globally, over 50% of laboratory facilities adopted AI-integrated thermal monitoring for high-precision equipment.

According to a 2025 report by the World Health Organization, AI-assisted temperature protection systems were deployed in over 150 hospitals worldwide, improving device reliability and early intervention for temperature-sensitive equipment.

Leading End-User: Hospitals lead adoption with 54% share, prioritizing patient safety, device uptime, and regulatory compliance. Hospitals integrate thermal protection into imaging systems, surgical instruments, and critical care devices to prevent operational failures and ensure treatment efficacy.

Fastest-Growing End-User: Ambulatory Care Centers are witnessing the fastest growth, expected to surpass 22% adoption by 2033, driven by increased outpatient procedures and portable diagnostic and therapeutic devices requiring consistent thermal management.

Other End-Users: Diagnostic Laboratories and Medical Device Manufacturers collectively represent 24% of market adoption, leveraging thermal protection for sensitive equipment and ensuring device compliance during production and shipment.

Consumer Adoption & Trends: In the U.S., 42% of hospitals are testing AI-enabled thermal monitoring systems for radiology and infusion devices. Globally, 38% of laboratories have implemented smart thermal enclosures to reduce equipment maintenance downtime.

According to a 2025 Gartner report, AI-based thermal management solutions adopted by diagnostic labs improved operational uptime by 27%, benefiting over 300 laboratory facilities across Europe and North America.

North America accounted for the largest market share at 41% in 2025; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2026 and 2033.

North America’s dominance is supported by over 6,500 medical device manufacturers, high hospital density exceeding 6,000 large-scale hospitals, and annual healthcare technology investments surpassing USD 30 billion. Europe accounted for 28%, Asia Pacific 18%, South America 7%, and the Middle East & Africa 6%, collectively summing to 100%. Rising demand for smart thermal management, AI-enabled monitoring, and regulatory-driven upgrades are key factors influencing adoption across all regions.

North America holds 41% of the market, driven by hospitals, diagnostic centers, and medical device manufacturers. Strong regulatory frameworks, including FDA compliance and ISO 13485 adherence, encourage adoption of advanced passive enclosures, phase-change materials, and smart temperature sensors. Technological advancements such as IoT-enabled thermal monitoring and AI-driven predictive maintenance are widely integrated. Local player 3M has implemented modular thermal packaging solutions to reduce equipment downtime in U.S. hospitals. North American healthcare facilities show higher enterprise adoption, with over 72% of tertiary hospitals integrating temperature protection systems in 2025.

Europe accounts for 28% of the market, with Germany, the UK, and France leading demand. Stringent regulatory requirements, including MDR compliance and sustainability initiatives, accelerate adoption of explainable, energy-efficient thermal protection systems. Emerging technologies such as AI-enabled monitoring and phase-change insulation materials are increasingly integrated. Local player Pelican BioThermal offers innovative temperature-controlled enclosures for hospitals and laboratories. European hospitals and labs demonstrate strong preference for compliant, energy-efficient solutions, with 65% of major hospitals incorporating smart thermal monitoring in 2025.

Asia Pacific holds 18% of the market, with China, India, and Japan as the top consumers. Expanding healthcare infrastructure and domestic device manufacturing are driving adoption of advanced thermal solutions. Innovation hubs in Japan and Singapore focus on compact, lightweight enclosures and AI-assisted thermal monitoring. Local player Gentherm has introduced smart thermal packaging for medical transport in the region. Consumer behavior reflects increased reliance on mobile-enabled and connected devices, with over 55% of hospitals integrating temperature monitoring solutions into routine operations.

South America holds 7% of the market, with Brazil and Argentina leading in adoption. Growth is influenced by infrastructure modernization and energy-efficient hospital systems. Government incentives support healthcare technology upgrades, encouraging the deployment of thermal protection in hospitals and laboratories. Local player Pelican BioThermal Brazil has implemented temperature-regulated transport containers for sensitive medical devices. Regional adoption trends reflect demand tied to healthcare modernization and localized solutions, with 40% of leading hospitals adopting thermal protection solutions in 2025.

The Middle East & Africa accounts for 6% of the market, with the UAE and South Africa as primary growth countries. Adoption is driven by modernization of healthcare infrastructure, integration of AI-enabled thermal monitoring, and adherence to local regulations and trade partnerships. Local companies are deploying smart temperature-regulated enclosures for hospitals and laboratories. Regional consumer behavior shows a growing preference for reliable, technology-integrated solutions, with over 35% of healthcare facilities incorporating advanced thermal management systems in 2025.

United States - 41% Market Share: High production capacity, advanced hospitals, and strong regulatory framework drive adoption.

Germany - 12% Market Share: Robust healthcare infrastructure and early adoption of compliant, energy-efficient thermal protection solutions.

The competitive environment in the Medical Device Temperature Protection Solutions Market is characterized by a moderately consolidated landscape with a strong presence of well‑established global players and emerging specialized competitors. Industry estimates indicate that there are 30+ active competitors globally focusing on thermal protection, monitoring, and temperature management solutions embedded in medical devices and clinical environments. The top 5 companies collectively account for an estimated ~58–62% of overall market engagement, showing a moderate level of concentration around leading innovators. These competitors span diversified portfolios, strategic alliances, and product portfolios that range from smart thermal monitoring sensors to precision temperature modulation systems integrated in ICU, surgical, and critical care settings.

Strategic initiatives within the competitive landscape include product launches, acquisitions, and technological partnerships aimed at enhancing precision, connectivity, and interoperability. For example, 3T Medical Systems, Inc. acquired Stryker’s Altrix Temperature Management System in 2025, positioning itself for precision thermal care solutions with ±0.1 °C control accuracy and rapid sensor refresh rates for clinical environments. ZOLL Medical Corporation secured expanded regulatory clearances in 2024 for its upgraded Thermogard platform, integrating intravascular and surface cooling/warming modalities to streamline thermal care workflows.

Key players emphasize innovation trends such as real-time analytics dashboards, closed‑loop feedback control features capable of maintaining <±0.2 °C stability, and integration with hospital information systems. Competitive dynamics are also influenced by R&D intensity, with 40+ global patents filed in 2024 around advanced temperature management technologies, further fueling differentiation among incumbents and newer entrants alike. These developments underscore a landscape where performance reliability, regulatory compliance, and strategic expansion initiatives define leadership and competitiveness in the market.

ZOLL Medical Corporation

Becton, Dickinson and Company (BD)

Gentherm

Smiths Medical, Inc. (ICU Medical)

GE Healthcare

Philips Healthcare

Cardinal Health

Honeywell International Inc.

Emerson Electric Co.

Belmont Medical Technologies

The Surgical Company

The Medical Device Temperature Protection Solutions Market is increasingly shaped by both existing and emerging technologies that enhance precision, connectivity, and safety of temperature‑critical medical equipment. Among current technologies, smart temperature sensors and AI‑enabled monitoring platforms stand out, enabling continuous real‑time temperature tracking and early anomaly detection in devices ranging from diagnostic imaging systems to infusion pumps. These integrated monitoring tools often include predictive analytics capabilities that reduce unplanned maintenance by identifying patterns of thermal stress before failures occur.

Closed‑loop thermal feedback systems represent another key technological innovation, especially in intravascular and patient warming/cooling applications. These systems adjust thermal outputs dynamically to maintain target temperatures with high accuracy (e.g., within ±0.1–±0.2 °C), significantly improving procedural consistency and clinical outcomes in critical care and surgical environments. Such precision systems often integrate with electronic health record (EHR) and hospital information systems to enable remote oversight and centralized control.

Advanced materials technology also plays a pivotal role. Phase‑change materials (PCMs), nano‑insulated composites, and biocompatible coatings improve passive thermal stability and device longevity, while reducing dependency on active heating/cooling systems. These materials are particularly useful in portable and implantable medical equipment where space and power efficiency are critical. Additionally, the adoption of IoT connectivity and cloud‑based dashboards facilitates remote device management, supports regulatory compliance through automated logging, and enhances interoperability across healthcare IT ecosystems.

Emerging technology trends in the market include adaptive thermal control systems, which leverage machine learning to optimize thermal profiles based on usage patterns and environmental conditions, and wearable micro‑temperature modules suitable for decentralized care settings such as home monitoring or ambulatory care. Blockchain‑enabled data integrity for clinical temperature records is also gaining traction as regulatory scrutiny around data security increases.

Technological modernization is influencing not only product performance but also strategic product portfolios as companies integrate advanced digital controls, real‑time analytics, and modular thermal interfaces to meet evolving healthcare demands, regulatory expectations, and digital transformation goals in modern healthcare environments.

• In January 2024, ZOLL Medical Corporation received FDA clearance and CE Mark approval for its upgraded Thermogard Temperature Management System, adding surface and intravascular cooling/warming modalities into a single platform with intelligent analytics capabilities. Source: www.massdevice.com

• In June 2025, 3T Medical Systems, Inc. completed the acquisition of the Altrix™ Precision Temperature Management System from Stryker, enhancing 3T Medical’s portfolio with a precision temperature management line capable of measuring patient temperature every 1.3 seconds and maintaining control within ±0.1 °C, expanding clinical deployment in operating rooms and ICUs. Source: www.3tmedical.com

• In mid‑2025, ZOLL Medical Corporation expanded its temperature management portfolio by entering into an exclusive distribution agreement for the BrainCool™/IQool™ System in the U.S. and key European markets, integrating high‑quality surface temperature management options with gel‑free, adhesive‑free pads and programmable protocol settings to support critical care fever control workflows. Source: www.businesswire.com

• In 2025, FDA granted expanded clearance for the Thermogard Temperature Management System to include versatile surface‑based treatment capabilities alongside catheter‑based applications, enhancing option flexibility for clinicians managing temperature in both normothermia and therapeutic hypothermia scenarios. Source: www.mpo-mag.com

The Medical Device Temperature Protection Solutions Market Report provides a comprehensive assessment of global product types, application arenas, end‑user segments, and key geographic regions, offering insights essential for strategic planning and investment decisions. The report examines solution types such as passive thermal enclosures, active heating/cooling systems, phase‑change materials, and smart sensor modules, detailing their functional attributes, technological differentiators, and use‑case relevance across critical medical settings.

The application scope covers diagnostic imaging, surgical and perioperative care, infusion therapy, implantable electronics, and laboratory instrumentation, reflecting the diverse requirements for thermal protection across healthcare practices. End‑user segmentation includes hospitals, ambulatory care centers, diagnostic laboratories, and medical device manufacturers, capturing deployment patterns and operational priorities that influence procurement and adoption.

Geographically, the report profiles market dynamics in North America, Europe, Asia Pacific, South America, and Middle East & Africa, presenting nuanced analyses of regional infrastructure trends, regulatory landscapes, and localized technology adoption behaviors. Within regions, focus areas include leading countries and key growth drivers, such as manufacturing investments, healthcare modernization, and enterprise digitization efforts.

The report also integrates technology insights, exploring current and emerging digital innovations, connectivity frameworks, and materials science advancements that enhance thermal stability, safety, and device lifecycle performance. Competitive intelligence modules outline market positioning, strategic collaborations, product pipelines, and innovation roadmaps of principal participants.

Strategically designed for industry professionals, investors, and decision‑makers, the report highlights market enablers such as regulatory harmonization, clinical workflow integration, and digital health convergence, while identifying constraints and ecosystem dependencies that inform risk mitigation and opportunity capture. Through a combination of segmentation depth, regional comprehensiveness, and technological perspective, the scope of this report supports high‑impact decision‑making in the evolving landscape of medical temperature protection solutions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 320.0 Million |

| Market Revenue (2033) | USD 427.9 Million |

| CAGR (2026–2033) | 3.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | 3M Company, Medtronic plc, Stryker Corporation, ZOLL Medical Corporation, Becton, Dickinson and Company (BD), Gentherm, Smiths Medical, Inc. (ICU Medical), GE Healthcare, Philips Healthcare, Cardinal Health, Honeywell International Inc., Emerson Electric Co., Belmont Medical Technologies, The Surgical Company |

| Customization & Pricing | Available on Request (10% Customization Free) |