Reports

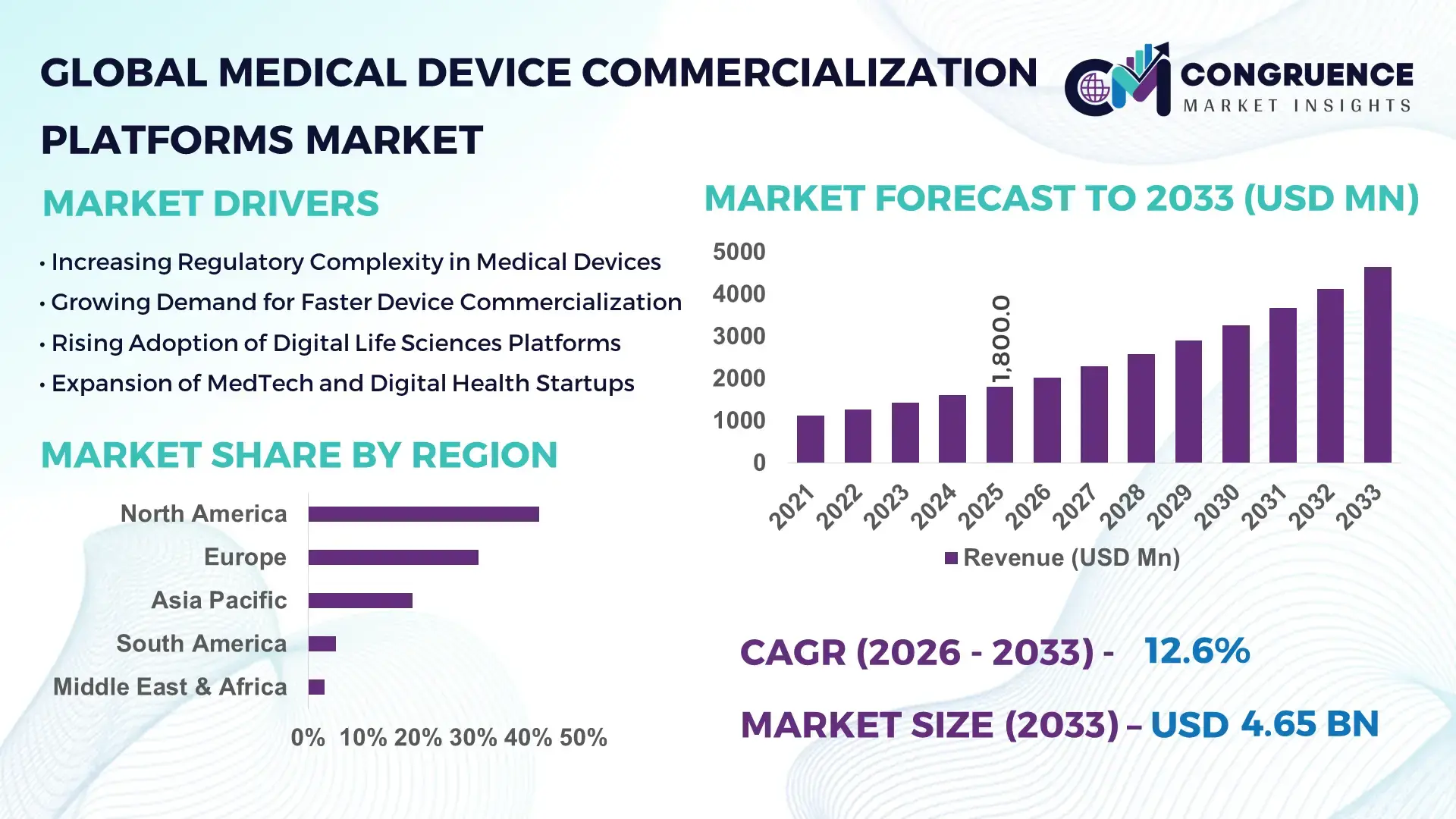

The Global Medical Device Commercialization Platforms Market was valued at USD 1,800 Million in 2025 and is anticipated to reach a value of USD 4,651.4 Million by 2033 expanding at a CAGR of 12.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by rising outsourcing of regulatory, clinical, and go-to-market activities as medical device manufacturers seek faster global launches and compliance efficiency.

The United States dominates the global Medical Device Commercialization Platforms Market through scale, technological depth, and investment intensity. The country hosts over 6,500 medical device manufacturers and accounts for more than 40% of global medical device R&D expenditure, with annual investments exceeding USD 35 billion. Commercialization platforms in the U.S. support high-volume launches across cardiovascular, orthopedic, and diagnostic devices, processing tens of thousands of regulatory submissions annually. Adoption of AI-enabled regulatory intelligence, cloud-based launch management tools, and real-world evidence platforms exceeds 65% among mid-to-large manufacturers, reinforcing platform-led commercialization workflows across the country.

Market Size & Growth: Valued at USD 1,800 Million in 2025, projected to reach USD 4,651.4 Million by 2033, driven by accelerated digital commercialization and regulatory complexity.

Top Growth Drivers: Regulatory outsourcing adoption at 58%, launch timeline reduction by 32%, post-market surveillance automation at 41%.

Short-Term Forecast: By 2028, average commercialization cycle times are expected to decline by 28% through platform-based automation.

Emerging Technologies: AI-driven regulatory intelligence, cloud-based launch orchestration, and real-world evidence analytics.

Regional Leaders: North America (USD 1,920 Million by 2033, enterprise-wide platform integration), Europe (USD 1,360 Million, MDR-focused adoption), Asia Pacific (USD 910 Million, rapid local-market rollout).

Consumer/End-User Trends: Medtech SMEs account for 46% of platform usage, driven by limited in-house regulatory capacity.

Pilot or Case Example: In 2024, a U.S.-based orthopedic launch platform reduced approval delays by 35%.

Competitive Landscape: IQVIA (~18% share), followed by Parexel, ICON, Syneos Health, Medpace.

Regulatory & ESG Impact: Platforms aligned with EU MDR, FDA QMSR, and digital traceability mandates.

Investment & Funding Patterns: Over USD 620 Million invested globally in commercialization-focused digital platforms since 2022.

Innovation & Future Outlook: Integration of AI, RWE, and predictive launch analytics shaping next-generation commercialization models.

The Medical Device Commercialization Platforms Market spans regulatory services (34%), clinical evidence generation (27%), market access and reimbursement support (21%), and post-launch surveillance tools (18%). Recent innovations include AI-assisted submission authoring and real-time compliance dashboards. Strong regulatory enforcement, cross-border launch demand, and rising Asia-Pacific consumption are reshaping platform capabilities, while integrated digital ecosystems define future growth trajectories.

The Medical Device Commercialization Platforms Market has become strategically critical as medical device manufacturers navigate increasingly complex regulatory, clinical, and market access environments. These platforms consolidate regulatory submissions, clinical evidence management, reimbursement planning, and post-market surveillance into unified digital ecosystems, reducing fragmentation and operational risk. AI-enabled regulatory intelligence delivers up to 42% faster dossier preparation compared to manual document management standards, significantly improving time-to-market predictability.

From a competitive standpoint, digital-first commercialization platforms now serve as a strategic differentiator. Cloud-native launch orchestration systems deliver 30% efficiency improvement compared to legacy, region-specific workflows, enabling parallel multi-country submissions. North America dominates in volume of platform deployments, while Europe leads in structured adoption with over 62% of MDR-regulated manufacturers relying on third-party commercialization platforms for compliance management.

Looking ahead, by 2028, AI-driven launch forecasting and real-world evidence analytics are expected to reduce post-launch compliance deviations by 25%. ESG considerations are also shaping platform design, with firms committing to 40% reduction in paper-based regulatory processes by 2030 through digital submissions and audit trails. In 2024, a Germany-based medtech firm achieved a 33% reduction in launch delays by deploying an AI-powered commercialization platform across five EU markets. Collectively, these dynamics position the Medical Device Commercialization Platforms Market as a pillar of operational resilience, regulatory assurance, and sustainable global expansion.

The Medical Device Commercialization Platforms Market is shaped by regulatory complexity, globalization of device launches, and the rapid digitalization of compliance and market access workflows. Manufacturers increasingly face simultaneous approvals across multiple jurisdictions, each with distinct regulatory frameworks and post-market obligations. Commercialization platforms address this challenge by centralizing regulatory intelligence, clinical data, and launch planning into standardized digital systems. The market is also influenced by growing adoption among small and mid-sized manufacturers, which now represent a substantial portion of platform demand due to constrained internal regulatory resources. Additionally, the convergence of real-world evidence requirements and digital health integration continues to redefine platform capabilities and long-term value creation.

Global regulatory frameworks such as EU MDR, FDA QMSR, and evolving Asia-Pacific approval pathways have significantly increased documentation, traceability, and post-market surveillance requirements. Medical device manufacturers now manage up to 3× more regulatory documentation per product launch compared to a decade ago. Commercialization platforms mitigate this burden by automating submission workflows, maintaining real-time regulatory intelligence, and enabling cross-functional collaboration. Studies indicate that platform adoption can reduce regulatory rework incidents by 29% and improve first-pass approval rates, making them essential tools for managing compliance-driven growth.

Despite their benefits, commercialization platforms require substantial upfront investment in system integration, data migration, and employee training. For mid-sized manufacturers, implementation costs can exceed USD 0.8–1.2 million per deployment, creating budgetary constraints. Legacy system incompatibility and fragmented internal data structures further slow adoption. Additionally, organizations operating in highly specialized device segments often require extensive customization, extending deployment timelines by 6–9 months, which can delay value realization and limit short-term uptake.

Emerging markets across Asia-Pacific, Latin America, and the Middle East are witnessing rapid growth in medical device approvals, with annual filing volumes increasing by over 20% in select regions. Commercialization platforms offer scalable solutions for managing localized regulatory requirements, language adaptation, and reimbursement pathways. Vendors that provide modular, region-specific compliance tools stand to benefit significantly as manufacturers pursue multi-country launches without proportional increases in internal regulatory teams.

Medical device commercialization platforms handle sensitive clinical, regulatory, and patient-related data, making cybersecurity and data sovereignty critical challenges. Regions such as the EU enforce strict data localization and privacy requirements, increasing compliance overhead. Approximately 37% of manufacturers cite data security concerns as a barrier to cloud-based platform adoption. Ensuring compliance with multiple data protection regimes while maintaining system interoperability remains a persistent operational challenge for platform providers.

Expansion of AI-Driven Regulatory Intelligence: Over 48% of new commercialization platforms launched since 2023 integrate AI for regulatory change detection and submission readiness scoring, reducing manual review workloads by 31% and improving compliance response times.

Growth of End-to-End Launch Orchestration Platforms: Approximately 52% of large manufacturers now deploy unified platforms covering regulatory, clinical, and reimbursement workflows, cutting cross-functional handoff delays by 27% and improving launch synchronization across regions.

Rising Adoption of Real-World Evidence Integration: More than 44% of platforms now incorporate post-market real-world data analytics, enabling early safety signal detection and supporting regulatory reporting efficiency improvements of 22%.

Shift Toward Modular, Scalable Platform Architectures: Around 57% of new deployments favor modular platform designs, allowing manufacturers to activate only required functions, reducing initial implementation costs by 25% while supporting phased global expansion.

The Medical Device Commercialization Platforms Market is segmented based on type, application, and end-user, reflecting the diversity of functions these platforms perform across the medical device lifecycle. By type, the market spans regulatory-focused platforms, integrated end-to-end commercialization platforms, clinical and evidence-generation platforms, and post-market surveillance solutions, each addressing distinct operational needs. Application-wise, segmentation aligns closely with pre-launch, launch, and post-launch activities, including regulatory submissions, market access planning, and lifecycle management. From an end-user perspective, demand varies significantly between large multinational manufacturers, mid-sized and small manufacturers, contract research organizations, and digital health innovators. This segmentation highlights how platform adoption is shaped by organizational scale, regulatory exposure, and geographic expansion strategies, with measurable differences in adoption intensity, functionality requirements, and deployment scope across segments.

The market by type is led by Integrated End-to-End Commercialization Platforms, which currently account for approximately 38% of overall adoption. These platforms consolidate regulatory submissions, clinical evidence management, reimbursement planning, and post-market surveillance into a single environment, reducing data silos and operational inefficiencies. Their leadership is supported by the fact that manufacturers using integrated platforms report 25–30% fewer cross-functional delays during global launches.

Regulatory Intelligence and Submission Management Platforms represent about 24% of adoption, driven by rising regulatory documentation requirements across the US, EU, and Asia-Pacific. Post-Market Surveillance and Real-World Evidence Platforms hold roughly 18%, reflecting increasing vigilance and reporting obligations. Clinical and Evidence Generation Platforms, including tools for managing trials and registries, collectively contribute around 20%.

The fastest-growing type is Post-Market Surveillance and Real-World Evidence Platforms, expanding at an estimated 14.8% CAGR, fueled by stricter post-approval monitoring rules and increasing use of real-world data for label extensions and compliance audits.

• In 2025, a national regulatory authority in Europe reported the deployment of an AI-enabled post-market surveillance platform across multiple device classes, enabling automated analysis of over 1 million adverse event records annually and improving reporting accuracy by more than 30%.

By application, Regulatory Submission and Approval Management is the leading segment, accounting for approximately 34% of platform utilization. This dominance is linked to the rising complexity of multi-country filings, where manufacturers now manage parallel submissions across an average of 6–8 jurisdictions per product. Launch Planning and Market Access Management follows with around 27% adoption, supporting pricing, reimbursement, and country sequencing decisions.

Post-Launch Lifecycle Management is the fastest-growing application, advancing at an estimated 15.2% CAGR, as regulators mandate continuous safety monitoring and real-world performance validation. Clinical Evidence Management and Label Expansion Support together account for roughly 39% of remaining application usage, serving both pre- and post-market needs.

Consumer and enterprise adoption trends reinforce this segmentation. In 2025, over 41% of global medical device manufacturers reported piloting digital platforms specifically for regulatory and launch coordination. In the US, nearly 45% of hospitals are involved in programs that feed real-world usage data into commercialization platforms for compliance and safety reporting.

• In 2024, a multinational public health organization confirmed that digital platforms supporting post-market surveillance were active in more than 160 hospitals worldwide, improving early detection of device-related safety signals for millions of patients.

Large and multinational medical device manufacturers form the leading end-user segment, representing approximately 46% of total platform adoption. Their dominance stems from broad product portfolios, frequent global launches, and high regulatory exposure across multiple markets. These organizations typically deploy platforms enterprise-wide, integrating regulatory, clinical, and market access teams.

Mid-sized and small manufacturers constitute the fastest-growing end-user group, expanding at an estimated 13.9% CAGR, as these firms increasingly outsource commercialization functions and rely on platforms to compensate for limited in-house regulatory expertise. Contract Research Organizations and Commercialization Service Providers contribute around 21%, leveraging platforms to manage multiple client portfolios efficiently. Digital health and emerging medtech startups collectively account for about 14%, focusing on modular, cloud-based deployments.

Adoption statistics highlight shifting behavior: in 2025, 38% of SMEs globally reported adopting commercialization platforms for first-time international launches, while over 52% of large manufacturers indicated that platform usage is now mandatory for new product introductions.

• In 2025, a global technology advisory firm reported that adoption of commercialization platforms among mid-sized medtech companies increased significantly, enabling hundreds of firms to reduce regulatory preparation time by more than 25%.

North America accounted for the largest market share at 42% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.2% between 2026 and 2033.

North America’s leadership is supported by high medical device launch volumes, advanced regulatory digitization, and strong adoption of integrated commercialization platforms across the United States and Canada. Europe follows with approximately 31% share, driven by stringent regulatory frameworks and harmonized compliance requirements across EU member states. Asia-Pacific holds nearly 19% share, reflecting rapid expansion in manufacturing capacity, digital health ecosystems, and cross-border device commercialization. South America and the Middle East & Africa together account for the remaining 8%, where adoption is rising steadily as governments modernize healthcare infrastructure and streamline device approval pathways. Across regions, increased platform penetration, multi-country launch requirements, and digital compliance tools continue to reshape regional demand dynamics.

North America represents approximately 42% of the global Medical Device Commercialization Platforms Market, making it the largest regional contributor. Demand is driven primarily by medical device manufacturing, digital health, and contract research organizations supporting large-scale product launches. Regulatory developments such as enhanced post-market surveillance requirements and quality system modernization have accelerated adoption of centralized commercialization platforms. Technological advancements include AI-enabled regulatory intelligence, cloud-based submission management, and real-world evidence integration, now used by over 60% of large manufacturers in the region. Local platform providers are increasingly offering modular, subscription-based solutions tailored to SMEs, enabling faster entry into regulated markets. Consumer behavior reflects high enterprise readiness, with healthcare organizations in the region showing significantly higher adoption of commercialization platforms compared to other regions, particularly for compliance tracking and launch coordination.

Europe accounts for roughly 31% of global market share, supported by key markets such as Germany, the United Kingdom, and France. The region’s regulatory environment, shaped by stringent medical device regulations and sustainability-focused compliance initiatives, has increased reliance on digital commercialization platforms. Manufacturers are adopting explainable, audit-ready systems to manage documentation, clinical evidence, and post-market obligations. Adoption of automation, AI-assisted submissions, and multilingual regulatory workflows is widespread, with more than 55% of European manufacturers integrating platform-based compliance tools. Regional players are focusing on interoperability and transparency to align with regulatory expectations. Consumer behavior in Europe reflects strong demand for traceable, explainable, and regulation-aligned commercialization solutions, particularly among mid-sized manufacturers navigating cross-border launches.

Asia-Pacific holds close to 19% of the global market and ranks as the fastest-expanding region by growth momentum. China, Japan, and India are the top consuming countries, supported by expanding medical device manufacturing clusters and rising export activity. Infrastructure development, local production incentives, and increasing regulatory digitization are strengthening demand for commercialization platforms. Regional innovation hubs are adopting cloud-native, mobile-enabled platforms to support rapid device approvals and market entry. Local platform providers are emphasizing scalability and multilingual capabilities to address diverse regulatory environments. Consumer behavior varies widely, with adoption driven by mobile-first workflows and digital health ecosystems, particularly among manufacturers targeting both domestic and international markets.

South America represents approximately 5% of global market share, with Brazil and Argentina as the key markets. Regional demand is influenced by healthcare infrastructure upgrades and evolving trade policies aimed at improving device accessibility. Governments are encouraging localized manufacturing and regional distribution, increasing the need for structured commercialization and compliance platforms. While digital adoption remains moderate, platform usage is rising among manufacturers managing multilingual submissions and region-specific regulatory pathways. Local players are focusing on compliance automation and documentation standardization. Consumer behavior in the region shows growing demand for platforms that support language localization and cost-efficient regulatory workflows.

The Middle East & Africa region accounts for roughly 3% of the global market, with growth concentrated in countries such as the UAE and South Africa. Demand is driven by healthcare modernization initiatives, expanding private healthcare investments, and regional trade partnerships. Governments are introducing digital health strategies and streamlined approval processes, increasing interest in commercialization platforms. Technological modernization includes cloud deployment and centralized regulatory tracking to support imported and locally manufactured devices. Regional players are aligning platforms with local regulatory requirements and international standards. Consumer behavior reflects selective adoption, with higher uptake among multinational manufacturers and healthcare groups operating across multiple countries.

United States – 36% Market Share: Strong dominance driven by high medical device production volumes, advanced regulatory digitization, and large-scale enterprise adoption.

Germany – 14% Market Share: Leadership supported by robust manufacturing capacity, strict regulatory compliance requirements, and widespread use of structured commercialization platforms.

The Medical Device Commercialization Platforms Market features a moderately fragmented competitive landscape with a growing number of active competitors innovating across regulatory compliance, launch orchestration, clinical evidence management, and post-market surveillance. There are 30+ significant global providers delivering a range of platform, analytics, and service solutions tailored to medtech manufacturers, CROs, and commercialization consultancies, with the combined share of the top 5 companies estimated at around 38–42%. Leading vendors include established life sciences software and services firms expanding their footprint into medtech commercialization workflows. Strategic initiatives such as expanded partnerships, integrated product launches, and long-term technology agreements are shaping competitive positioning — for example, a prominent global clinical and commercial partnership was announced between major platform players in 2025 to enhance interoperability between their systems, facilitating integrated regulatory, quality, and launch operations across customer instances.

Market leaders are also investing heavily in AI, cloud-native architectures, and data orchestration capabilities, enabling advanced regulatory intelligence, real-world evidence analytics, and integrated launch planning. Innovation trends include AI-driven workflow automation, master data management enhancements, and multi-platform integration frameworks that help reduce manual dependencies and accelerate time-to-compliance. Regional competition varies, with North America and Europe hosting a higher density of incumbents and Asia-Pacific seeing rapid entry of specialized digital solutions. M&A activity and strategic acquisitions of niche regulatory and analytics tools continue to influence the competitive structure, as incumbents seek to broaden their commercial lifecycle portfolios and strengthen market penetration.

Medtronic

Boston Scientific

Abbott Laboratories

Stryker Corporation

Johnson & Johnson

GE Healthcare

Siemens Healthineers

Philips Healthcare

Oracle Health Sciences

SAP Life Sciences

Dassault Systèmes (Medidata Solutions)

Clarivate

Thompson Reuters

Current and emerging technologies are fundamentally reshaping the Medical Device Commercialization Platforms Market, driving efficiency, compliance, and speed across the product lifecycle. AI and machine learning are being embedded into regulatory intelligence, documentation automation, and predictive analytics, enabling real-time tracking of global regulatory changes and advanced risk classification. For instance, advanced multimodal transformer frameworks achieve regulatory risk classification accuracy as high as over 90%, significantly outperforming traditional text-only methodologies.

Cloud-native architectures enable scalable deployment of commercialization workflows, supporting distributed teams and multi-jurisdictional compliance requirements. Cloud platforms facilitate centralized data repositories, secure document management, and modular API integrations that streamline cross-functional collaboration between regulatory, quality, and market access teams. The integration of master data management (MDM) tools, as supported by industry partnerships, enhances consistency in stakeholder engagement and analytics across platforms, improving decision-making for launch planning and post-market actions.

AI-driven analytics extend into real-world evidence (RWE) generation, enabling manufacturers to process large volumes of post-market safety data, clinical outcomes, and usage trends. These systems can identify safety signals proactively, reducing manual surveillance burdens. Emerging LLM-based assistants are being adopted to automate the drafting of regulatory submissions, clinical summaries, and compliance reports, enhancing accuracy and reducing preparation cycle times.

Integration-focused technologies—such as cross-vendor orchestration frameworks—allow data and workflows from disparate systems to converge into unified commercialization toolchains. This is evidenced by long-term strategic partnerships engineered to enable interoperability between CRM, regulatory, and analytics systems. The convergence of CRM, compliance, and analytics technologies is increasingly critical, as digital transformation demands platforms capable of handling complex, multi-dimensional commercialization tasks spanning regulatory, clinical, and launch operations.

• In April 2024, IQVIA and Salesforce expanded their global strategic partnership to accelerate development of the Salesforce Life Sciences Cloud — a next-generation engagement platform combining IQVIA’s Orchestrated Customer Engagement capabilities with Salesforce’s AI CRM to deliver a unified end-to-end solution for clinical, regulatory, and commercial functions. The new platform is expected to expand availability for medical technology customers by late 2025. Source: www.iqvia.com

• In August 2025, IQVIA and Veeva Systems announced long-term clinical and commercial partnerships resolving all prior legal disputes, enabling seamless use of each other’s data and technology across clinical, regulatory, quality, and commercial workflows. The agreement includes master data access and joint participation in technology partner programs to simplify integrations for shared customers. Source: www.iqvia.com

• In May 2025, Salesforce launched a certified Life Sciences Partner Network — a strategic ecosystem of systems integrators, consulting firms, and technology partners to support adoption and migration to the Life Sciences Cloud and Agentforce digital labor platform across pharma and medtech organizations. Source: www.salesforce.com

• In December 2025, Veeva Systems announced the availability of Veeva AI Agents for Vault CRM and PromoMats, delivering industry-specific AI functionality to boost productivity and customer centricity in commercial and regulatory workflows, with additional agents planned for clinical, safety, and quality applications through 2026. Source: www.veeva.com

The scope of the Medical Device Commercialization Platforms Market Report encompasses a comprehensive evaluation of digital and service-driven platform solutions that support regulatory compliance, clinical evidence management, launch planning, market access deployment, and post-market surveillance across global medical device lifecycles. It examines segmentation by technology type, including integrated commercialization suites, regulatory intelligence systems, real-world evidence platforms, launch orchestration tools, and quality and post-market surveillance solutions, providing decision-makers with insights into functionality, deployment models, and integration capabilities.

Geographically, the report covers major regions such as North America, Europe, Asia-Pacific, South America, and Middle East & Africa, detailing regional adoption trends, regulatory environments, and technology penetration. It analyzes key industry applications such as regulatory submission automation, medical affairs support, market access analytics, and quality management integration, identifying how platforms support device commercialization from pre-market planning to post-launch performance tracking.

The report also highlights emerging technologies impacting the market, including AI-driven analytics, natural language processing for document automation, cloud-native orchestration, master data interoperability, and integrated customer engagement solutions. It profiles industry focus areas such as digital transformation imperatives, cross-platform integration trends, and compliance-driven innovation strategies relevant to medtech manufacturers, CROs, and service providers.

Additionally, the scope covers competitive dynamics, strategic partnerships, and platform ecosystems that enable seamless connectivity across clinical, regulatory, quality, and commercial functions. It addresses niche segments such as real-world evidence analytics and regulatory intelligence accelerators, offering insights into growth drivers, technology adoption barriers, and strategic investment priorities for stakeholders navigating a complex global commercialization landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,800 Million |

| Market Revenue (2033) | USD 4,651.4 Million |

| CAGR (2026–2033) | 12.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Veeva Systems, IQVIA, Salesforce Life Sciences Cloud, Medtronic, Boston Scientific, Abbott Laboratories, Stryker Corporation, Johnson & Johnson, GE Healthcare, Siemens Healthineers, Philips Healthcare, Oracle Health Sciences, SAP Life Sciences, Dassault Systèmes (Medidata Solutions), Clarivate, Thompson Reuters |

| Customization & Pricing | Available on Request (10% Customization Free) |