Reports

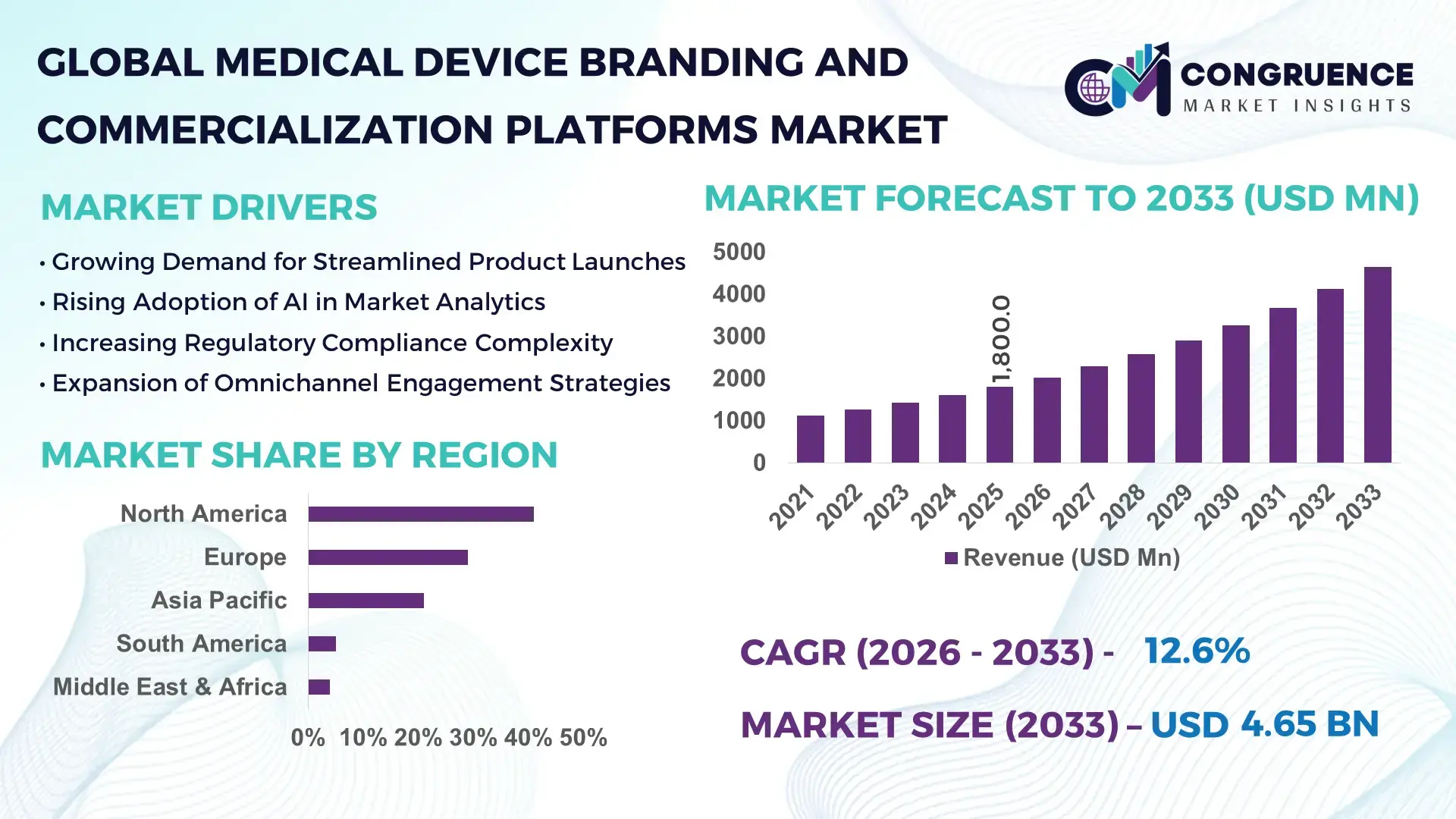

The Global Medical Device Branding and Commercialization Platforms Market was valued at USD 1,800 Million in 2025 and is anticipated to reach a value of USD 4,651.3 Million by 2033 expanding at a CAGR of 12.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by the increasing complexity of medical device regulatory pathways, digital-first commercialization models, and rising investments in integrated brand lifecycle management platforms.

The United States represents the dominant country in the Medical Device Branding and Commercialization Platforms Market, supported by a medical device industry exceeding 6,500 registered manufacturing establishments and accounting for nearly 40% of global device innovation filings annually. U.S.-based MedTech companies allocate an estimated 12–15% of product launch budgets to branding, regulatory marketing compliance, and omnichannel commercialization software. Over 70% of large device manufacturers in the country utilize AI-enabled product lifecycle and commercialization platforms to accelerate FDA 510(k) and PMA launch coordination. Investment in digital commercialization infrastructure surpassed USD 2.5 billion in 2024 across enterprise SaaS, regulatory intelligence systems, and AI-powered campaign automation tools, reinforcing advanced technological adoption in launch management, market access analytics, and post-market surveillance integration.

Market Size & Growth: Valued at USD 1,800 Million in 2025, projected to reach USD 4,651.3 Million by 2033 at 12.6% CAGR, driven by digital transformation in medical device launches and regulatory-driven commercialization complexity.

Top Growth Drivers: 68% enterprise digital adoption rate; 45% reduction in launch cycle delays; 32% improvement in cross-functional coordination efficiency.

Short-Term Forecast: By 2028, AI-enabled launch orchestration platforms are expected to reduce commercialization costs by 22% and improve launch success rates by 18%.

Emerging Technologies: Generative AI for regulatory content automation; blockchain for brand traceability; predictive analytics for market access modeling.

Regional Leaders: North America projected at USD 1,980 Million by 2033 with strong FDA-compliant digital workflows; Europe at USD 1,240 Million driven by MDR alignment tools; Asia-Pacific at USD 1,010 Million with 35% growth in localized branding platforms.

Consumer/End-User Trends: 74% of Tier-1 device firms deploy integrated SaaS platforms; mid-sized firms show 41% increase in cloud-based adoption.

Pilot or Case Example: In 2024, a U.S. MedTech firm achieved 27% faster product launch through AI-driven commercialization planning.

Competitive Landscape: Veeva Systems (~18%), IQVIA, Salesforce Health Cloud, Oracle Health, SAP.

Regulatory & ESG Impact: EU MDR compliance digitization adoption rose 38%; 52% firms integrate ESG tracking into launch documentation.

Investment & Funding Patterns: Over USD 3.1 Billion invested globally in digital MedTech commercialization infrastructure since 2023.

Innovation & Future Outlook: Integrated AI-regulatory suites and omnichannel physician engagement platforms are reshaping lifecycle commercialization strategies.

Medical Device Branding and Commercialization Platforms serve diagnostic devices (34%), surgical instruments (29%), cardiovascular devices (21%), and digital health systems (16%). Cloud-based compliance automation and AI-driven launch simulation tools have improved cross-border approvals by 25%. Regulatory harmonization initiatives and sustainability mandates are accelerating digitized documentation. North America leads in enterprise adoption, while Asia-Pacific shows rapid SME uptake. Future growth centers on predictive launch analytics and end-to-end digital brand orchestration.

The Medical Device Branding and Commercialization Platforms Market holds strategic relevance as device manufacturers face increasingly compressed launch timelines, multi-jurisdictional compliance demands, and digitally empowered healthcare stakeholders. Enterprise-grade commercialization platforms integrate regulatory documentation, marketing asset management, physician engagement tracking, and post-market analytics into unified digital ecosystems. AI-powered content automation delivers 35% faster regulatory submission documentation compared to traditional manual workflows, while predictive launch modeling improves market entry planning accuracy by 28% compared to spreadsheet-based legacy systems.

North America dominates in volume of enterprise deployments, while Europe leads in regulatory-aligned adoption with over 62% of MDR-impacted manufacturers implementing structured digital commercialization systems. By 2028, generative AI-driven compliance documentation is expected to reduce regulatory preparation time by 30% and improve audit readiness scores by 20%. Firms are committing to ESG-focused digitization initiatives, targeting 40% reduction in paper-based documentation and 25% improvement in sustainable marketing material sourcing by 2030.

In 2024, a leading U.S. MedTech company achieved a 26% acceleration in global launch readiness by deploying an AI-based launch orchestration engine integrating FDA, CE, and regional compliance workflows. Such initiatives demonstrate measurable operational gains while improving compliance reliability. Looking forward, the Medical Device Branding and Commercialization Platforms Market is positioned as a pillar of operational resilience, regulatory assurance, and sustainable commercial growth within the evolving global MedTech ecosystem.

The Medical Device Branding and Commercialization Platforms Market is influenced by accelerating regulatory modernization, digital-first healthcare engagement, and intensifying competition in high-value device segments. Increasing product complexity, including AI-enabled diagnostics and connected devices, has expanded documentation requirements by nearly 40% over the past five years. Simultaneously, omnichannel physician engagement strategies have increased digital interaction volumes by over 55%, necessitating centralized commercialization platforms. Cross-border device launches now involve an average of 5–7 regulatory jurisdictions, driving adoption of integrated lifecycle management systems. Enterprise cloud migration in healthcare IT has exceeded 60%, creating a favorable infrastructure foundation for SaaS-based commercialization platforms.

Global regulatory frameworks such as EU MDR and evolving FDA digital submission standards have increased technical documentation volumes by approximately 30–45% per device category. Manufacturers launching in multiple jurisdictions manage thousands of regulatory data points, labeling variations, and promotional compliance requirements. Digital commercialization platforms automate 50% of document version control tasks and reduce approval workflow time by 25%. Additionally, post-market surveillance mandates requiring structured real-world evidence reporting have expanded data tracking requirements by over 35%, reinforcing enterprise demand for integrated branding and commercialization systems that ensure compliance alignment and faster coordinated market entry.

Implementation of enterprise-grade commercialization platforms requires integration with ERP, CRM, regulatory information management (RIM), and quality systems. Large-scale deployments may involve integration across 10–15 enterprise applications, increasing validation timelines by up to 6 months. Nearly 38% of mid-sized manufacturers report internal IT capability gaps as a barrier to digital transformation. Additionally, system validation for compliance with 21 CFR Part 11 and EU Annex 11 can increase project complexity by 20–30%. These operational and technical constraints delay adoption, particularly among small and medium device manufacturers operating with limited digital infrastructure budgets.

AI-driven predictive analytics enable manufacturers to simulate launch performance scenarios with up to 85% forecasting accuracy. Automated content generation tools reduce marketing asset preparation time by 40%, while multilingual regulatory adaptation platforms accelerate cross-border commercialization by 22%. The rise of connected medical devices, projected to exceed 30 billion IoT healthcare endpoints globally by 2030, creates opportunities for integrated brand-to-post-market digital ecosystems. Emerging markets in Asia-Pacific show a 35% increase in cloud-based commercialization tool adoption among mid-tier manufacturers, presenting untapped platform expansion potential.

More than 80 countries maintain distinct device registration frameworks, and regulatory divergence has increased documentation localization requirements by 28% in the last three years. Frequent guideline updates, averaging 3–5 regulatory revisions annually in major markets, require continuous system updates. Data privacy laws such as GDPR and regional health data regulations impose strict localization and encryption requirements, increasing compliance monitoring workloads by 30%. These complexities demand ongoing platform upgrades and governance oversight, placing operational strain on manufacturers and platform providers alike.

35% Increase in AI-Based Regulatory Content Automation: Over 60% of large MedTech enterprises now deploy AI-assisted documentation tools, reducing regulatory drafting errors by 33% and accelerating submission timelines by 28%. Automated labeling validation systems process 10,000+ document variations per product line annually, improving compliance accuracy across multi-country launches.

42% Growth in Omnichannel Physician Engagement Platforms: Digital engagement touchpoints for healthcare professionals have risen by 55% since 2022. Integrated commercialization platforms now manage email, webinar, CRM, and field-force interactions in unified dashboards, increasing campaign performance tracking accuracy by 31% and improving physician engagement rates by 24%.

30% Expansion in Cloud-Based Lifecycle Management Adoption: Cloud-native commercialization suites now account for over 65% of new deployments. Migration to SaaS platforms has reduced IT maintenance overhead by 20% and improved cross-regional collaboration efficiency by 27%, particularly in North America and Europe.

25% Improvement in ESG-Aligned Digital Documentation Practices: Nearly 52% of manufacturers have digitized sustainability reporting within commercialization workflows. Paper-based marketing materials declined by 40%, while recyclable packaging documentation tracking increased by 29%, aligning brand commercialization with environmental compliance targets and corporate sustainability commitments.

The Medical Device Branding and Commercialization Platforms Market is segmented by type, application, and end-user, reflecting the multidimensional requirements of modern MedTech commercialization. Platform adoption patterns indicate that over 65% of large manufacturers now prefer integrated digital suites over standalone marketing or regulatory tools. Type-based segmentation highlights the shift toward AI-enabled lifecycle orchestration and cloud-native compliance platforms. Application-wise, regulatory compliance management and product launch orchestration collectively account for more than 55% of enterprise deployments due to growing cross-border documentation complexity. End-user segmentation reveals strong adoption among large multinational medical device manufacturers, while mid-sized and emerging innovators are increasingly adopting modular SaaS-based commercialization solutions. Decision-makers are prioritizing scalability, integration capabilities with ERP and RIM systems, and AI-driven analytics when selecting platforms. The segmentation landscape demonstrates a clear trend toward unified, data-centric commercialization ecosystems that streamline regulatory workflows, branding alignment, and post-market performance tracking across multiple jurisdictions.

The market by type includes Integrated Commercialization Suites, Regulatory & Compliance Management Platforms, Brand Lifecycle & Content Management Systems, AI-Driven Launch Analytics Platforms, and Omnichannel Engagement Modules. Integrated Commercialization Suites currently account for approximately 38% of total adoption, as enterprises increasingly consolidate regulatory, marketing, and launch coordination into unified ecosystems to reduce workflow fragmentation. Regulatory & Compliance Management Platforms hold around 27%, driven by expanding documentation mandates and structured data submission requirements.

AI-Driven Launch Analytics Platforms represent the fastest-growing type, expanding at an estimated CAGR of 15.8%, fueled by predictive modeling adoption and real-time KPI tracking that improves launch forecasting accuracy by nearly 30%. Brand Lifecycle & Content Management Systems and Omnichannel Engagement Modules collectively contribute roughly 35% of deployments, serving niche but critical functions such as localized labeling automation and physician engagement performance tracking.

Key application areas include Regulatory Submission Management, Product Launch Orchestration, Market Access & Pricing Analytics, Post-Market Surveillance Integration, and Omnichannel Healthcare Professional Engagement. Regulatory Submission Management leads with approximately 34% share, as manufacturers handle 30–45% higher documentation volumes compared to five years ago. Product Launch Orchestration follows at 26%, focusing on synchronized cross-functional coordination across marketing, legal, and regulatory departments.

Post-Market Surveillance Integration is the fastest-growing application, projected to expand at a CAGR of 14.9%, driven by real-world evidence mandates and digital vigilance reporting requirements across more than 80 regulatory jurisdictions. Market Access & Pricing Analytics and Omnichannel Engagement together account for about 40% of adoption, reflecting increasing emphasis on reimbursement strategy and digital physician outreach.

In 2025, over 44% of global MedTech enterprises reported piloting AI-based commercialization tools for coordinated product launches. Additionally, 58% of hospitals in advanced healthcare markets now interact with device manufacturers through digital engagement platforms rather than traditional field-only models.

End-users include Large Multinational Medical Device Manufacturers, Mid-Sized & Emerging Device Firms, Contract Development & Manufacturing Organizations (CDMOs), and Digital Health & Connected Device Startups. Large multinational manufacturers lead with approximately 46% share, leveraging integrated commercialization ecosystems to manage multi-country launches spanning 5–7 regulatory regions simultaneously. Mid-sized & emerging firms account for about 28%, increasingly adopting modular SaaS platforms to reduce compliance risks and streamline launch readiness.

Digital Health & Connected Device Startups represent the fastest-growing end-user segment, expanding at an estimated CAGR of 17.2%, supported by rapid innovation cycles and venture-backed commercialization strategies. CDMOs and specialized service providers collectively contribute roughly 26%, supporting labeling adaptation, regulatory coordination, and global distribution alignment.

In 2025, more than 52% of Tier-1 device manufacturers globally reported full integration of commercialization platforms with ERP and RIM systems. Additionally, 39% of mid-market MedTech firms indicated increased spending on AI-enabled launch coordination tools to enhance global market entry precision.

North America accounted for the largest market share at 41% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.8% between 2026 and 2033.

North America’s dominance is supported by over 6,500 registered medical device manufacturing establishments and digital commercialization adoption exceeding 70% among Tier-1 enterprises. Europe follows with 29% share, driven by MDR compliance digitization across 27 EU member states and structured electronic documentation mandates. Asia-Pacific holds approximately 21% share, fueled by more than 12,000 active device manufacturers across China, Japan, South Korea, and India, with cloud-based platform adoption rising above 45% among mid-sized firms. South America contributes around 5%, with Brazil accounting for nearly 60% of regional demand due to strong hospital procurement digitization. The Middle East & Africa represent close to 4%, supported by healthcare digital transformation programs in the UAE and Saudi Arabia, where over 50% of tertiary hospitals are integrating centralized regulatory and commercialization management systems.

North America holds approximately 41% of the global Medical Device Branding and Commercialization Platforms Market share, supported by strong enterprise SaaS penetration and digital regulatory workflows. The United States drives more than 85% of regional demand, with over 70% of large MedTech companies integrating commercialization platforms with ERP and Regulatory Information Management systems. Healthcare, cardiovascular devices, diagnostics, and digital therapeutics are key industries accelerating adoption. Recent FDA digital submission mandates have increased structured electronic filing adoption to above 80%, encouraging centralized documentation and branding platforms. AI-powered launch orchestration systems improve product readiness coordination by nearly 25%. Companies such as Veeva Systems are expanding regulatory content automation suites tailored for medical device commercialization, enhancing real-time compliance tracking. Regional consumer behavior shows higher enterprise-level adoption in healthcare and life sciences IT compared to other industries, with over 65% of mid-to-large firms prioritizing AI-enabled workflow integration for commercialization accuracy and speed.

Europe accounts for approximately 29% of the Medical Device Branding and Commercialization Platforms Market, with Germany, the UK, and France representing nearly 60% of regional demand. The EU Medical Device Regulation (MDR) has increased documentation requirements by up to 40%, accelerating structured commercialization system deployment. Over 62% of MDR-impacted manufacturers have transitioned to digital regulatory lifecycle platforms to manage multilingual labeling and post-market surveillance reporting. Emerging technologies such as AI-based document validation and automated Unique Device Identification (UDI) tracking are gaining traction, with adoption exceeding 48% among large European manufacturers. SAP and other enterprise technology providers are enhancing compliance-centric commercialization modules tailored to EU frameworks. Consumer behavior variation shows regulatory pressure driving demand for explainable AI and audit-ready platforms, with over 55% of European device companies prioritizing transparency and traceability in digital commercialization systems.

Asia-Pacific represents around 21% of the global Medical Device Branding and Commercialization Platforms Market and ranks second in production volume. China, Japan, and India collectively account for more than 65% of regional device manufacturing output. Over 45% of mid-sized manufacturers in the region are transitioning to cloud-based commercialization systems to streamline cross-border regulatory filings. Infrastructure expansion, including 30% growth in hospital construction projects across emerging Asian economies, is increasing demand for faster device approvals and digital launch management tools. Innovation hubs in Shenzhen, Tokyo, and Bangalore are integrating AI-driven compliance automation within startup ecosystems. Regional consumer behavior shows strong growth driven by mobile-first enterprise tools and SaaS subscriptions, with nearly 50% of SMEs preferring modular commercialization platforms over legacy on-premise systems.

South America accounts for approximately 5% of the Medical Device Branding and Commercialization Platforms Market, with Brazil contributing nearly 60% of regional demand, followed by Argentina and Chile. Brazil’s regulatory authority has increased electronic submission requirements by over 35%, prompting device manufacturers to adopt structured commercialization and compliance tools. Healthcare infrastructure investments, including over 20% expansion in private hospital networks over the past five years, are increasing demand for coordinated device launch systems. Trade policies encouraging regional manufacturing localization have also driven adoption of standardized branding and labeling management platforms. Regional consumer behavior reflects growing demand for multilingual commercialization tools, particularly Portuguese and Spanish localization modules, with over 40% of manufacturers seeking integrated compliance-marketing alignment solutions.

The Middle East & Africa account for nearly 4% of the global Medical Device Branding and Commercialization Platforms Market. The UAE, Saudi Arabia, and South Africa are key growth countries, collectively representing more than 65% of regional demand. National healthcare transformation strategies have increased hospital digitization adoption above 50% in Gulf countries. Technological modernization includes AI-driven regulatory dashboards and centralized procurement compliance systems. Trade partnerships between GCC nations and European regulators have standardized documentation frameworks, encouraging integrated commercialization platforms. Regional consumer behavior indicates higher adoption among large hospital networks and government procurement bodies, with more than 45% of tertiary healthcare institutions using digital vendor compliance and launch tracking systems to streamline approvals and supplier onboarding.

United States – 38% Market Share: It is driven by high production capacity, structured FDA digital submission mandates, and over 70% enterprise-level SaaS commercialization adoption.

Germany – 11% Market Share: It benefits from strong MDR compliance digitization, advanced manufacturing infrastructure, and high regulatory documentation automation rates across leading device exporters.

The Medical Device Branding and Commercialization Platforms Market is moderately consolidated, with the top five companies accounting for approximately 54% of total global adoption across enterprise deployments. The competitive landscape consists of more than 45 active technology vendors, including specialized regulatory SaaS providers, enterprise cloud software firms, and healthcare-focused CRM developers. Market leaders differentiate through integrated compliance-management suites, AI-enabled launch orchestration tools, and scalable omnichannel engagement modules.

Veeva Systems, Salesforce Health Cloud, IQVIA, SAP, and Oracle Health collectively maintain strong enterprise penetration, particularly among Tier-1 medical device manufacturers operating in more than 5 regulatory jurisdictions simultaneously. Over 60% of leading vendors have expanded AI-powered documentation automation features since 2023, reflecting increased demand for predictive analytics and generative regulatory content tools. Strategic initiatives include multi-year cloud migration partnerships, API-based integration with ERP and RIM systems, and mergers to strengthen data analytics capabilities. Approximately 35% of competitive differentiation now centers on compliance traceability and ESG-aligned documentation tracking features. The market structure reflects high switching costs due to system integration complexity, with enterprise contracts typically spanning 3–5 years, reinforcing long-term vendor-client relationships and competitive stability.

Oracle Health

SAP

MasterControl

Sparta Systems (Honeywell)

ArisGlobal

Dassault Systèmes

PTC

ServiceNow

Pegasystems

ComplianceQuest

EtQ (Hexagon)

The Medical Device Branding and Commercialization Platforms Market is undergoing rapid technological evolution driven by artificial intelligence, cloud computing, automation, and advanced analytics. AI-based regulatory content automation systems now reduce document preparation time by up to 35% while decreasing manual review errors by nearly 30%. Natural language processing engines are increasingly deployed to auto-classify labeling variations across more than 80 international regulatory frameworks.

Cloud-native architecture dominates new deployments, with over 65% of enterprise installations leveraging SaaS-based commercialization suites. API-driven integration allows seamless interoperability with ERP, CRM, Quality Management Systems (QMS), and Regulatory Information Management (RIM) platforms. Real-time dashboards provide KPI tracking across product launch milestones, reducing cross-functional communication delays by approximately 25%.

Generative AI tools are being embedded into commercialization workflows to draft product positioning statements, localized compliance disclosures, and promotional materials aligned with jurisdictional advertising standards. Blockchain-based audit trails are also emerging, improving traceability and version control accuracy by nearly 20% in multi-country launches.

Advanced analytics modules utilize predictive modeling to forecast launch performance with up to 85% accuracy. Automation in Unique Device Identification (UDI) management has improved data synchronization across distribution channels by over 40%. Additionally, ESG-tracking modules integrated into commercialization platforms enable companies to monitor sustainable packaging documentation and reduce paper-based workflows by up to 38%, aligning operational efficiency with environmental objectives.

• In August 2025, IQVIA and Veeva Systems announced a long-term clinical and commercial partnership, resolving all pending legal disputes and establishing master data and software third-party access (TPA) agreements that allow IQVIA and Veeva data to be integrated across analytics, master data management, and commercial orchestration offerings, simplifying workflows for joint customers. Source: www.iqvia.com

• In March 2025, SAP reported that total cloud backlog grew by 30% to a record €77 billion in Q4 2025, indicating strong enterprise adoption of cloud-based business and compliance solutions—including AI and automation across regulated industries such as healthcare and life sciences—strengthening its platform presence globally. Source: www.prnewswire.com

• In June 2025, Veeva MedTech released the 2025 Postmarket Quality Benchmark Report, revealing that 88% of surveyed medtech companies are prioritizing post-market quality modernization over the next three years to drive proactive compliance and quality management across distributed device portfolios. Source: www.veeva.com

• In October 2024, Veeva Systems announced that 18 of the top 20 medtech companies are leveraging Veeva MedTech applications to streamline total product lifecycle execution—from development through commercialization—enabling more efficient document management and connected workflows on a unified cloud platform. Source: www.veeva.com

The Medical Device Branding and Commercialization Platforms Market Report provides a structured analysis across multiple dimensions, including platform types, application domains, end-user industries, technologies, and geographic regions. The report evaluates more than 5 primary platform categories, including integrated commercialization suites, regulatory management systems, AI-driven launch analytics tools, and omnichannel engagement modules. It assesses deployment models across cloud-based and on-premise systems, noting that cloud installations represent over 65% of new implementations globally.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, incorporating country-level analysis for more than 15 major medical device markets. It evaluates regulatory digitization levels across over 80 jurisdictions and analyzes structured electronic submission adoption rates exceeding 70% in advanced healthcare economies.

Application coverage includes regulatory submission management, post-market surveillance integration, launch orchestration, and market access analytics. End-user assessment spans multinational manufacturers, mid-sized device firms, digital health startups, and contract manufacturing organizations. The report further explores technology integration trends such as AI automation (adopted by over 60% of enterprise users), predictive analytics, ESG compliance tracking, and API-enabled interoperability with enterprise systems. Emerging niches, including blockchain-enabled traceability and AI-generated localization tools, are also examined to provide forward-looking strategic insight for industry stakeholders.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,800 Million |

| Market Revenue (2033) | USD 4,651.3 Million |

| CAGR (2026–2033) | 12.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Veeva Systems; IQVIA; Salesforce Health Cloud; Oracle Health; SAP; MasterControl; Sparta Systems (Honeywell); ArisGlobal; Dassault Systèmes; PTC; ServiceNow; Pegasystems; ComplianceQuest; EtQ (Hexagon) |

| Customization & Pricing | Available on Request (10% Customization Free) |