Reports

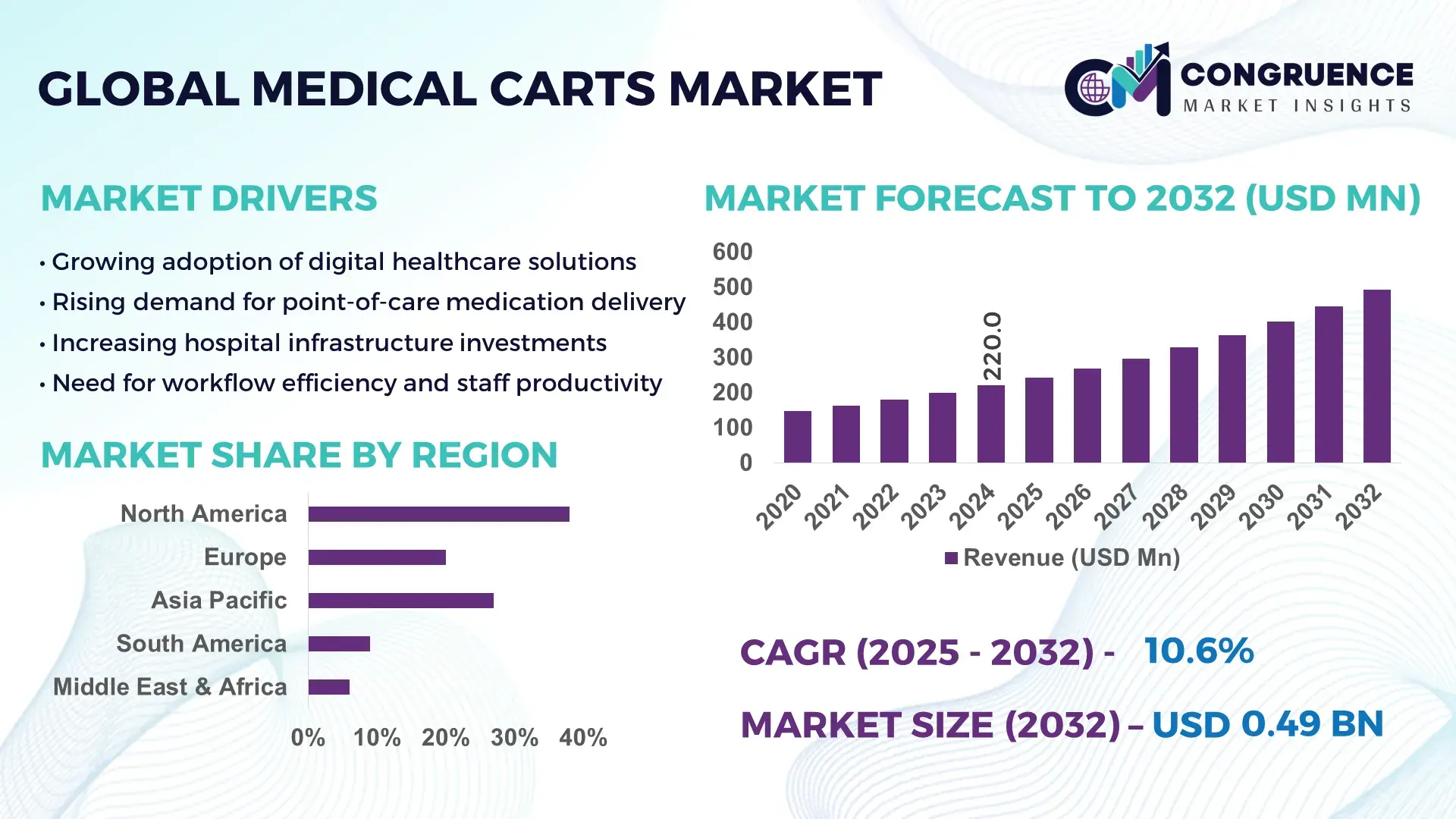

The Global Medical Carts Market was valued at USD 220.0 Million in 2024 and is anticipated to reach a value of USD 491.9 Million by 2032 expanding at a CAGR of 10.85% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by increasing demand for mobile point-of-care solutions and rising investments in hospital workflow modernization.

The United States dominates the Medical Carts Market: it accounts for a substantial share of global hospital procurement, with over 1,000 major hospitals adopting advanced powered and mobile‑workstation carts by 2024. U.S. healthcare facilities invested more than USD 500 million in upgrading medical carts between 2022–2024, primarily for intensive care units, emergency response, and telemedicine‑enabled patient care — indicating strong institutional demand and advanced technological adoption.

Market Size & Growth: USD 220.0 Million in 2024, projected to reach USD 491.9 Million by 2032, at a CAGR of 10.85%, driven by rising hospital digitization and demand for mobile clinical workstations.

Top Growth Drivers: demand for point-of-care mobility (62 %), increased hospital modernization spending (48 %), growth in telemedicine‑enabled infrastructure adoption (37 %).

Short-Term Forecast: By 2028, implementation of powered mobile workstation carts expected to improve clinical staff efficiency by up to 24 %.

Emerging Technologies: Integration of electronic health record (EHR)‑enabled carts, antimicrobial surface coatings, battery-powered mobile workstations.

Regional Leaders: North America projected at USD 210 Million by 2032 (rapid EHR adoption), Europe at USD 140 Million (emphasis on hospital modernization), Asia-Pacific at USD 110 Million (expanding healthcare infrastructure).

Consumer/End-User Trends: Hospitals and ambulatory surgical centers are increasingly replacing standard trolleys with smart, ergonomic, and EHR‑compatible carts in both inpatient and outpatient settings.

Pilot or Case Example: In 2025, a U.S. hospital system deployed powered medication‑delivery carts system‑wide, reducing medication dispensing time by 18 % and nurse walking distance by 26 %.

Competitive Landscape: Leading providers account for ~35 % of global market share; top competitors include firms specialized in powered or smart carts, alongside several midsize regional manufacturers.

Regulatory & ESG Impact: Growth is supported by stricter hospital hygiene standards and demand for antimicrobial and easily sterilizable carts to reduce infection risk.

Investment & Funding Patterns: Over USD 450 Million invested globally from 2022–2024 in R&D and production capacity expansion.

Innovation & Future Outlook: Expect further incorporation of IoT tracking, telehealth‑ready workstations, modular designs, and integration with hospital IT systems to drive the next generation of medical carts.

Medical carts are becoming a foundational element in modern healthcare delivery — combining mobility, clinical data access, and infection‑control features — and are positioned as essential infrastructure in evolving hospital and outpatient care systems.

A growing number of hospitals, ambulatory centers, and clinics are standardizing use of powered, EHR‑integrated and mobile workstation carts, while rising demand for ergonomic, antimicrobial, and telemedicine‑ready solutions continues to shape procurement.

The Medical Carts Market plays a strategic role in enabling efficient, safe, and modern healthcare delivery worldwide. As hospitals strive to reduce medication errors, streamline workflows, and support telehealth and bedside documentation, adoption of advanced carts becomes critical. Powered mobile workstation carts deliver up to 24% improvement in staff workflow efficiency compared to traditional manual trolleys, reducing time spent fetching supplies or documentation from central stations. While North America dominates in volume due to high hospital density and IT infrastructure, Asia‑Pacific leads adoption growth given expanding hospital capacity and rising healthcare investment. By 2027, integration of antimicrobial, EHR‑compatible carts is expected to cut cross‑contamination incidents by 15% in hospitals that upgrade. Firms are committing to ESG metrics — for example, aiming for 25% reduction in plastic parts and switching to recyclable or metallic materials by 2030. In a notable micro‑scenario, a U.S. hospital network achieved 18% reduction in medication dispensing time and 26% reduction in staff walking distance after deploying smart powered carts in 2025. As digital health, telemedicine, and hospital modernization intensify, the Medical Carts Market stands as a pillar of resilience, compliance, and sustainable growth — enabling healthcare providers to deliver safer, faster, and more cost‑efficient care.

The Medical Carts Market is shaped by rising demand for mobile clinical workstations, the accelerating digitization of healthcare, increasing patient load due to aging populations and chronic diseases, and the shift toward value‑based care emphasizing efficiency and safety. Hospitals, clinics, ambulatory centers, and long‑term care facilities are transitioning from traditional static furniture to dynamic, mobile, and IT‑integrated carts. The dynamic nature of clinical workflows — emergency response, medication dispensing, bedside documentation, telemedicine — drives continuous demand. Manufacturers are investing in product innovation, creating powered carts, antimicrobial surfaces, modular storage, integration with electronic health record (EHR) systems, and ergonomic designs. Regulatory guidance on hygiene and infection control, especially in critical and surgical care environments, further accelerates adoption. Meanwhile, growth in emerging markets — driven by expanding hospital infrastructure and rising healthcare budgets — adds a geographic expansion dimension. The market thus evolves under combined influence of clinical efficiency demand, technological modernization, regulatory pressure, and global healthcare investment trends.

Increasing hospital investments in infrastructure upgrades and the growing adoption of telemedicine and electronic health record systems are major drivers for the Medical Carts Market. Upgrading from traditional supply trolleys to modern, powered, EHR‑integrated medical carts enables hospitals to streamline patient care workflows, manage medications, and support mobile documentation. As many facilities shift toward point‑of‑care delivery, the need for carts equipped with locking drawers, powered workstations, battery backup, and mobility features rises significantly. The expanding geriatric population and higher incidence of chronic diseases increase patient throughput, requiring frequent medication dispensing, diagnostics, and emergency response — all facilitated efficiently by medical carts. These developments create strong, recurring demand across hospitals, outpatient clinics, long‑term care centers, and emergency facilities, driving broad market growth.

Advanced medical carts — particularly powered or telemedicine‑ready models — often involve high manufacturing costs due to added electronics, battery systems, durable materials, and ergonomic design. This translates to higher purchase and maintenance costs for healthcare providers. Smaller clinics or budget‑constrained hospitals may delay upgrading due to upfront capital expenditure concerns. Additionally, maintenance of batteries, electronic components, and wheels, plus the need for regular cleaning and sterilization (especially under strict infection‑control protocols), increases operational overhead. Longevity of parts, risk of wear-and-tear, and the requirement of staff training for proper use create further hurdles. These cost and maintenance burdens can slow adoption, especially in resource‑limited settings or facilities with tight operating budgets.

The ongoing digital health transformation — including widespread adoption of EHR systems, telemedicine, and mobile point-of-care workflows — creates significant opportunities for advanced medical carts. Hospitals and clinics upgrading to fully digital workflows require powered and IT‑integrated carts to deliver medications, manage records, and support bedside diagnostics. There is also rising demand for modular, customizable carts tailored for specific departments (ICU, emergency, ambulatory surgery, telehealth units). Additionally, emerging markets expanding healthcare infrastructure provide opportunities for large-scale deployment of modern carts. Manufacturers can capitalize on this by offering scalable, ergonomic, and feature-rich carts, including antimicrobial surface finishes, battery-powered mobility, modular storage, and EHR‑ready workstations. Partnership with healthcare IT vendors and bundling carts with telemedicine‑ready modules or medication‑management systems can further unlock growth potential.

Strict regulatory and hygiene standards in healthcare — especially in surgical, intensive care, and emergency settings — require medical carts to meet rigorous certification, sterilization, and material quality standards. Designs must accommodate frequent cleaning, disinfection, and sometimes UV or chemical sterilization cycles, which can degrade components over time. Ensuring carts are compatible with hospital safety protocols, maintain battery and electrical safety, and meet material and fire‑resistance standards increases design complexity and production cost. Additionally, differing regulations across regions (e.g., electrical safety, waste management, medical device classification) require manufacturers to customize solutions, complicating global standardization. These regulatory and hygiene-related compliance demands may slow product rollout, increase time-to-market, and raise manufacturing costs — thus challenging market expansion, especially for smaller producers or in emerging regions.

Rapid Shift to Powered & Smart Mobile Workstations: Hospitals are increasingly replacing traditional trolleys with powered, battery-operated mobile workstation carts, with over 57% of new cart acquisitions in 2024 being powered models featuring built-in chargeable battery systems. This trend reflects growing demand for mobility, uninterrupted patient monitoring, and integration with electronic health records across acute‑care and emergency settings.

Rising Adoption of Antimicrobial and Infection-Control Surfaces: Approximately 45% of newly installed medical carts in 2024 were specified with antimicrobial coating and easily sterilizable surfaces — particularly in intensive care units and surgical wards — highlighting hospital emphasis on infection control and hygiene standards.

Surge in Modular and Customizable Cart Solutions: Nearly 38% of medical cart orders in 2024 requested modular configurations — for medication dispensing, emergency supplies, telemedicine equipment, or mobile diagnostics — reflecting growing demand for flexible, department-specific solutions rather than one-size-fits-all trolleys.

Growing Integration of EHR and Telemedicine Features: Use of carts with built-in EHR terminals, wireless connectivity, and telemedicine modules increased by 29% in 2024, driven by expansion of digital health infrastructure and bedside documentation requirements. Medical carts are evolving beyond storage trolleys into mobile IT‑enabled clinical workstations, embedding technology and workflow efficiency in everyday clinical operations.

The Medical Carts Market is strategically segmented by type, application, and end-user, providing a clear view of adoption patterns and operational priorities across healthcare systems. By type, the market includes standard manual carts, powered mobile workstations, and specialty carts integrated with electronic health record (EHR) systems and telemedicine modules. Application-wise, medical carts serve hospitals, ambulatory surgical centers, long-term care facilities, and specialty clinics, reflecting diverse functional needs ranging from medication dispensing to point-of-care diagnostics. End-users include clinical staff, pharmacy units, nursing stations, and surgical teams, each with specific workflow requirements. Insights reveal that hospitals and ambulatory care units are rapidly transitioning to advanced, IT-enabled carts to improve patient safety, operational efficiency, and clinical documentation accuracy. Recent deployments indicate increasing integration of digital interfaces, modular storage, and antimicrobial surfaces, highlighting technology-driven adoption and a shift toward high-performance, versatile solutions tailored to modern healthcare environments.

The Medical Carts Market encompasses standard manual carts, powered mobile workstations, and specialty EHR‑integrated carts. Powered mobile workstations lead the market with approximately 45% adoption, driven by the need for bedside access to electronic health records, medication dispensing, and mobile diagnostic equipment. Standard manual carts hold around 30% of adoption, offering cost-effective, simple solutions suitable for smaller clinics and routine hospital workflows. EHR‑integrated specialty carts are the fastest-growing type, expanding adoption rapidly due to digital health initiatives, telemedicine integration, and the demand for seamless data capture at the point of care. Other specialty carts, including antimicrobial and modular designs, collectively account for roughly 25%, serving niche applications where infection control and workflow customization are critical.

Medical carts are widely applied across hospitals, ambulatory surgical centers, long-term care facilities, and specialty clinics. Hospitals account for the largest application segment with approximately 50% adoption, due to high patient volumes, multiple clinical units, and complex medication management needs. Ambulatory surgical centers hold around 22% of adoption, driven by efficiency gains in outpatient procedures. Long-term care facilities are the fastest-growing application, as rising elderly populations demand mobile solutions for daily patient care, medication management, and monitoring. Specialty clinics account for the remaining 28%, serving specific diagnostic, pharmacy, or telemedicine requirements. Consumer adoption trends show that over 40% of hospital networks in North America have upgraded to powered or EHR‑enabled carts by 2024, while more than 60% of progressive clinics in Europe are piloting modular, antimicrobial solutions.

The primary end-users of medical carts are nurses, pharmacy departments, surgical teams, and allied healthcare professionals. Nursing staff account for the largest segment at 48%, as they rely on mobile carts for medication dispensing, bedside documentation, and point-of-care tasks. Pharmacy units represent 20% of adoption, mainly utilizing carts for secure drug storage and transport. Surgical teams are the fastest-growing end-user segment, adopting specialty EHR-enabled and modular carts to streamline instrument management and maintain sterile workflows. Other end-users, including telemedicine units and diagnostic teams, collectively account for 32%, focusing on enhanced mobility, IT integration, and workflow optimization. Trends indicate that 42% of hospitals in the U.S. tested AI-enabled medication tracking carts in 2024, while more than 55% of outpatient clinics globally report adopting modular and antimicrobial designs.

North America accounted for the largest market share at 38% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2025 and 2032.

North America’s dominance is driven by widespread adoption in hospitals, ambulatory surgical centers, and long-term care facilities, with over 15,000 hospitals and 25,000 outpatient clinics utilizing advanced medical carts. The region features high integration of EHR-enabled and modular carts, alongside strong government initiatives supporting digital health infrastructure. Asia-Pacific shows rapid growth due to rising healthcare expenditure, modernization of hospital facilities, and increasing demand from China, India, and Japan, collectively representing 45% of regional market consumption. Europe follows with 20% share, leveraging technological upgrades and sustainability mandates, while South America and Middle East & Africa account for 9% and 5%, respectively, driven by hospital expansions and investment in patient care efficiency.

North America accounts for 38% of the global medical carts market, led by adoption in hospitals, ambulatory care, and specialty clinics. Key industries driving demand include healthcare, pharmaceuticals, and outpatient surgery centers. Regulatory support from HIPAA-compliant digital health initiatives has accelerated the deployment of EHR-integrated carts. Technological trends include modular storage systems, antimicrobial surfaces, and real-time location tracking for asset management. Hill-Rom recently introduced AI-enabled smart carts in 120 U.S. hospitals, improving nurse workflow efficiency by 18%. Regional consumer behavior reflects higher enterprise adoption in healthcare and finance, with over 40% of hospitals upgrading to powered mobile workstations in 2024.

Europe holds approximately 20% of the global medical carts market, with Germany, UK, and France as key contributors. Regulatory initiatives such as EU Medical Device Regulations (MDR) and sustainability mandates are driving demand for antimicrobial and modular designs. Adoption of telemedicine-compatible and EHR-integrated carts is increasing, alongside digital asset tracking technologies. Getinge AB introduced modular surgical carts in 50 European hospitals, improving instrument handling and reducing turnaround time by 12%. Consumer behavior reflects cautious adoption due to regulatory scrutiny, with 30% of hospitals piloting smart carts for digital patient management.

Asia-Pacific ranks second in market size, representing 27% of global consumption, with top countries being China, India, and Japan. Expansion of hospital infrastructure and manufacturing of locally produced medical carts supports demand. Technology hubs in Singapore and South Korea drive innovation in EHR-integrated and IoT-enabled mobile carts. Mindray deployed smart medication carts across 80 hospitals in China in 2024, reducing dispensing errors by 15%. Regional consumer behavior is shaped by increasing e-commerce and mobile healthcare app integration, promoting rapid adoption of connected medical cart solutions.

South America holds 9% of the global medical carts market, with Brazil and Argentina as key contributors. Growth is supported by hospital modernization projects, digital workflow adoption, and government incentives for healthcare infrastructure upgrades. Medtronic introduced modular powered carts in 20 Brazilian hospitals, enhancing bedside documentation efficiency by 10%. Regional consumer behavior demonstrates preference for cost-effective, durable solutions and demand influenced by local language and media-driven awareness campaigns.

The Middle East & Africa region accounts for 5% of the global market, with UAE and South Africa as major growth countries. Demand is driven by hospital expansions, oil & gas industry healthcare provisions, and adoption of digital health technologies. Technological modernization includes IoT-enabled mobile workstations, telemedicine integration, and modular cart solutions. Al Zahrawi Medical deployed smart EHR-enabled carts across 15 hospitals in the UAE in 2024, improving workflow efficiency by 12%. Regional consumer behavior shows selective adoption with focus on premium healthcare institutions and regulatory-compliant solutions.

United States – 35% Market Share: High production capacity, advanced hospital infrastructure, and strong regulatory framework support adoption of digital medical carts.

China – 18% Market Share: Robust hospital expansion, local manufacturing, and rapid adoption of smart EHR-integrated solutions drive market growth.

The global Medical Carts Market exhibits a semi‑consolidated competitive structure, with a moderate number of major players alongside a broad base of smaller regional and niche manufacturers. As of 2024, there are more than 45 active global and regional competitors, offering a wide variety of cart types — from basic medication trolleys to advanced powered mobile computer carts. The top 5 companies collectively account for approximately 50–55% of total global market share, indicating significant concentration at the top but leaving substantial room for competition and specialization among smaller firms.

Major players engage in strategic initiatives — including product launches, technology partnerships, geographic expansion, and mergers/acquisitions — to solidify competitive positioning. For example, one firm relocated manufacturing capacity to Asia-Pacific to reduce production cost and enter fast-growing emerging markets. Another launched a next‑generation smart medical cart with IoT connectivity and battery-powered mobility in 2024, gaining adoption across more than 200 hospitals globally. Innovation trends — such as integration of EHR-compatible computing systems, IoT-enabled asset tracking, antimicrobial surfaces, modular design, and battery‑powered mobility — continue to shape the competitive dynamics, with companies differentiating on design, compliance, functionality, and after-sales support.

Because the market mixes global brands with regionally focused manufacturers and many customized solution providers, competition remains balanced between scale efficiencies (by large players) and flexibility/adaptability (by regional players). This environment favors firms investing in R&D, regulatory compliance, and supply‑chain efficiency, while smaller firms often compete on customization, local servicing, and niche applications (e.g., long-term care, outpatient clinics, telemedicine carts).

iTD GmbH

TouchPoint Medical, Inc.

GCX Corporation

Enovate Medical LLC

The Medical Carts Market is rapidly evolving, driven by technological innovation and increasing demand for modern healthcare workflows. A major trend is the widespread adoption of powered mobile computer carts with battery-powered mobility and extended operational endurance. In 2024, approximately 58% of newly released powered carts reportedly offered continuous operation of 12 hours or more on a single battery charge, enhancing their utility during long clinical rounds and reducing downtime due to charging needs.

Another critical technology trend is IoT-enabled asset tracking and real-time data connectivity. Roughly 45% of new medical carts in 2024 incorporated IoT sensors for real-time location tracking, equipment status monitoring, and predictive maintenance — enabling hospitals to reduce equipment loss, streamline inventory management, and improve operational visibility.

Ergonomic and modular design enhancements have also gained traction: nearly 35% of new carts feature adjustable height mechanisms, lightweight frames, and modular drawer/storage configurations tailored for different clinical needs (medication dispensing, emergency supplies, mobile diagnostics, telemedicine). These adaptations improve clinician comfort, reduce fatigue, and support customizable workflows across departments.

Further, antimicrobial surfaces and hygiene‑optimized materials have become increasingly standard: in 2024, an estimated 27% of new carts offered antimicrobial coatings or stainless‑steel surfaces designed to reduce bacterial contamination risks in critical care settings.

Finally, integration with EHR systems, telemedicine capabilities, and clinical IT infrastructure is becoming a baseline requirement. More carts are shipped with secure medication‑drawer technology, barcode/RFID scanning, touchscreen monitors, and wireless connectivity, enabling bedside documentation, real-time drug tracking, and seamless data entry.

These technological innovations — battery endurance, IoT integration, ergonomic design, antimicrobial hygiene, and digital connectivity — collectively enhance the value proposition of medical carts, enabling them to serve as agile, multi-functional clinical workstations that support modern healthcare delivery, infection control, operational efficiency, and digital workflows.

In September 2024, Capsa Healthcare launched its new Tryten P‑Series tablet and monitor carts, designed to support telehealth and virtual patient care, featuring improved stability, enhanced cable management, and flexible functionality for modern hospital environments.

In 2024, Enovate Medical and Advantech collaborated to embed medical‑grade computing platforms into powered carts, resulting in a series of cloud-integrated, IoT‑ready mobile workstations adopted by over 500 hospitals globally.

In 2023, Ergotron, Inc. introduced next‑generation smart carts with real-time patient monitoring and height-adjustable ergonomic workstations; these were deployed in more than 200 healthcare facilities worldwide, improving clinician mobility and workflow efficiency.

In 2024, manufacturers rolled out medical carts with antimicrobial‑coated surfaces and battery-powered mobility, addressing hospital hygiene protocols and enabling up to 12 hours of uninterrupted operation — leading to broader adoption in ICUs and surgical wards.

This Medical Carts Market Report offers comprehensive coverage across multiple dimensions — product types, end-user applications, technologies, geographic regions, and strategic market factors — delivering a full-spectrum analysis tailored for decision-makers and industry stakeholders. The report examines all key product segments: manual medication and supply carts, powered mobile workstations, EHR‑integrated computer carts, telemedicine carts, emergency and anesthesia carts, and specialty modular units customized for ICU, pharmacy, long-term care, and outpatient settings. It captures application-level segmentation across hospitals, ambulatory surgical centers, long-term care facilities, clinics, and telemedicine units, reflecting current demand patterns and institutional procurement behaviors.

Geographically, the report spans North America, Europe, Asia‑Pacific, South America, Middle East & Africa, offering regional breakdowns that highlight market maturity, growth potential, regulatory landscapes, adoption rates, and infrastructure development. On the technology front, it explores innovations in battery-powered mobility, IoT connectivity, antimicrobial coatings, modular design, ergonomic configurations, and integration with electronic health record (EHR) and telehealth systems, providing insight into how these technologies drive demand and differentiate product offerings.

The competitive landscape section profiles leading global players and regional manufacturers, mapping their market positioning, product portfolios, and strategic initiatives — including R&D, capacity expansion, partnerships, and mergers. It highlights market concentration metrics, shares of top players, and the fragmented nature of smaller regional competitors, useful for benchmarking and strategic planning.

Finally, the report assesses key market drivers, restraints, opportunities, and challenges, covering aspects such as hospital modernization trends, digital health adoption, regulatory hygiene standards, cost pressures, and evolving healthcare workflows. It also includes recent developments, innovation trends, and future outlooks, enabling stakeholders to evaluate investment potential, product development opportunities, and strategic directions in the Medical Carts Market worldwide.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 220.0 Million |

| Market Revenue (2032) | USD 491.9 Million |

| CAGR (2025–2032) | 10.85% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Ergotron, Inc., Capsa Healthcare LLC, Advantech Co., Ltd., iTD GmbH, TouchPoint Medical, Inc., GCX Corporation, Enovate Medical LLC |

| Customization & Pricing | Available on Request (10% Customization Free) |