Reports

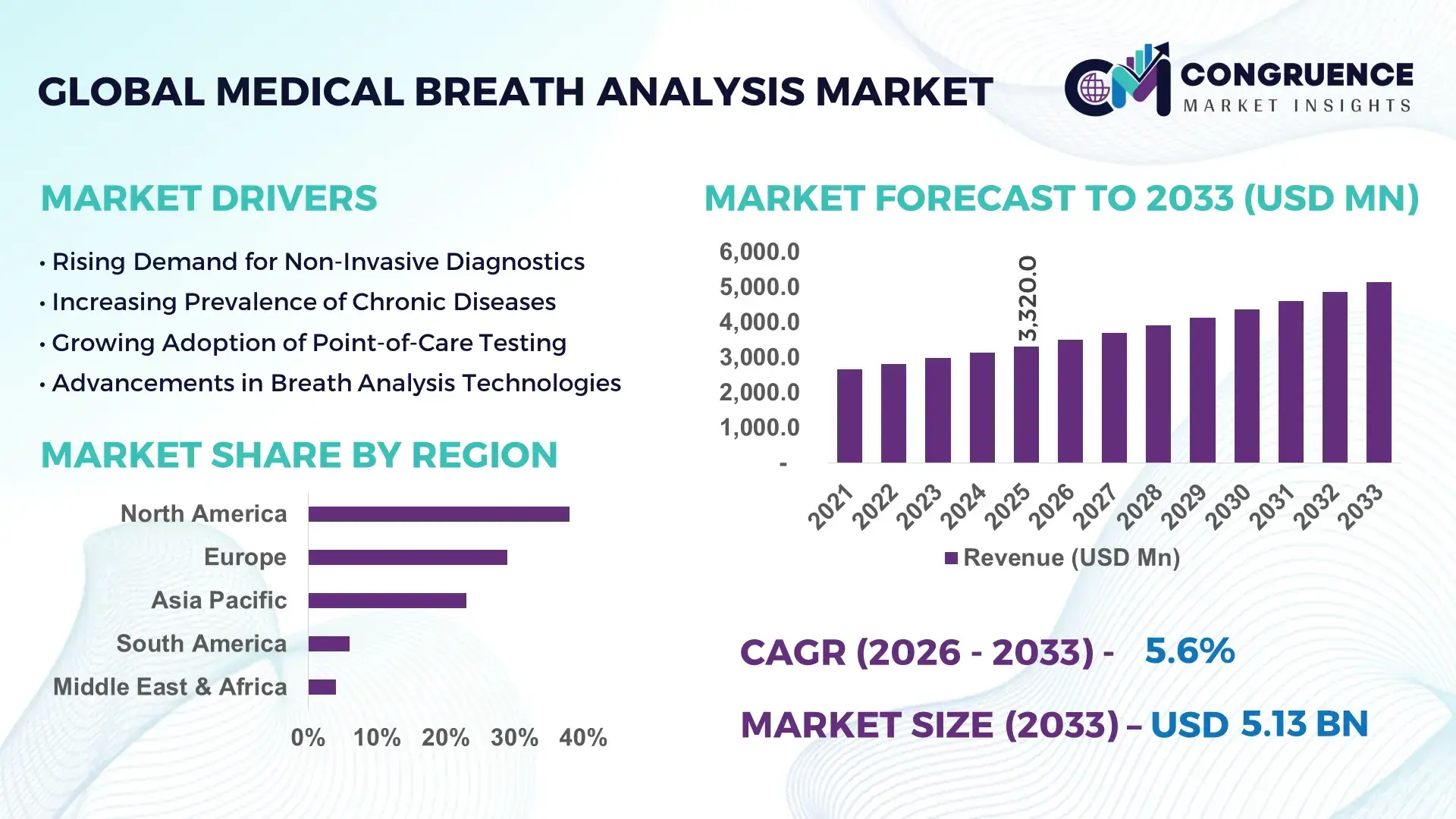

The Global Medical Breath Analysis Market was valued at USD 3,320.0 Million in 2025 and is anticipated to reach a value of USD 5,133.9 Million by 2033 expanding at a CAGR of 5.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by increasing demand for non-invasive diagnostic technologies and rising prevalence of respiratory and metabolic disorders.

The United States dominates the Medical Breath Analysis Market with advanced healthcare infrastructure and high diagnostic adoption rates. Over 68% of hospitals in the U.S. have integrated non-invasive diagnostic tools, including breath analyzers, into routine screening programs. The country accounts for approximately 40% of global clinical trials focused on breath biomarker detection. Investments exceeding USD 1.2 billion have been directed toward portable breath diagnostic technologies between 2022 and 2025. Key applications include asthma monitoring, gastrointestinal disorder detection, and cancer screening, with over 35% of pulmonology clinics utilizing breath analysis systems. Technological advancements such as AI-based gas chromatography systems have improved diagnostic accuracy by up to 27%, supporting large-scale adoption across healthcare facilities.

Market Size & Growth: USD 3,320.0 Million in 2025, projected to reach USD 5,133.9 Million by 2033, growing at 5.6% CAGR, driven by demand for non-invasive diagnostics.

Top Growth Drivers: Non-invasive diagnostics adoption (48%), respiratory disease prevalence increase (42%), early disease detection demand (36%).

Short-Term Forecast: By 2028, diagnostic efficiency is expected to improve by 22% due to AI integration.

Emerging Technologies: AI-enabled gas sensors, nanotechnology-based biosensors, portable real-time breath analyzers.

Regional Leaders: North America (USD 1,950 Million by 2033, high hospital integration), Europe (USD 1,420 Million, regulatory-driven adoption), Asia-Pacific (USD 1,200 Million, rapid healthcare expansion).

Consumer/End-User Trends: Increasing preference for home-based diagnostics with 31% adoption among chronic disease patients.

Pilot or Case Example: In 2024, a clinical pilot improved early lung disease detection rates by 26% using AI breath analyzers.

Competitive Landscape: Market leader holds ~18% share; key players include Thermo Fisher Scientific, Siemens Healthineers, Bedfont Scientific, Owlstone Medical, and Philips Healthcare.

Regulatory & ESG Impact: Stricter FDA and EU MDR regulations boosting device standardization and sustainability compliance.

Investment & Funding Patterns: Over USD 900 Million invested in breath diagnostics startups and R&D since 2022.

Innovation & Future Outlook: Integration with wearable devices and cloud diagnostics platforms shaping future growth.

Medical Breath Analysis Market is supported by healthcare (52%), research (28%), and homecare sectors (20%). Innovations in nanomaterial sensors and AI algorithms are improving detection sensitivity by 25%. Regulatory frameworks like FDA approvals and EU MDR compliance ensure product reliability. Asia-Pacific shows 34% consumption growth due to rising healthcare access, while future trends include integration with telehealth platforms.

The Medical Breath Analysis Market holds strong strategic relevance due to its ability to transform diagnostics through non-invasive, rapid, and cost-efficient methods. Healthcare systems globally are prioritizing early disease detection, with breath analysis technologies reducing diagnostic turnaround time by up to 35% compared to conventional blood-based testing. AI-powered breath analysis delivers 28% improvement in diagnostic accuracy compared to traditional gas chromatography methods, enhancing clinical decision-making efficiency.

North America dominates in volume due to established healthcare infrastructure, while Asia-Pacific leads in adoption with over 39% of healthcare institutions integrating portable diagnostic tools. This regional divergence reflects varying priorities, with developed markets focusing on precision diagnostics and emerging markets emphasizing accessibility and cost efficiency.

By 2028, AI-driven breath analytics is expected to improve disease detection rates by 30%, particularly in oncology and respiratory disorders. Companies are increasingly integrating IoT-enabled devices, enabling remote patient monitoring and reducing hospital visits by approximately 25%.

Firms are committing to ESG targets, including reducing diagnostic waste by 20% and adopting eco-friendly sensor materials by 2030. In 2024, a U.S.-based healthcare provider achieved a 22% reduction in diagnostic costs through AI-enabled breath analysis systems deployed across 150 clinics.

Looking ahead, the Medical Breath Analysis Market is positioned as a critical pillar supporting healthcare resilience, regulatory compliance, and sustainable diagnostic innovation, driving long-term industry transformation.

The Medical Breath Analysis Market is influenced by evolving healthcare needs, technological advancements, and increasing demand for non-invasive diagnostic solutions. Rising prevalence of chronic diseases such as asthma, COPD, and gastrointestinal disorders is significantly shaping market demand. Over 262 million people globally suffer from asthma, increasing the need for real-time diagnostic tools. The integration of advanced sensor technologies, including nanotechnology and AI-based analytics, is improving detection sensitivity by over 20%, enabling early disease diagnosis. Additionally, healthcare providers are focusing on reducing diagnostic costs and improving patient comfort, which supports the adoption of breath analysis systems. Regulatory frameworks and clinical validation requirements also play a crucial role in shaping market entry and expansion strategies. Increasing investments in R&D and partnerships between technology providers and healthcare institutions are further driving innovation and market growth.

The growing preference for non-invasive diagnostic procedures is a key driver of the Medical Breath Analysis Market. Traditional diagnostic methods such as blood tests and biopsies often involve discomfort, higher costs, and longer processing times. In contrast, breath analysis offers rapid, painless, and real-time diagnostic capabilities. Studies indicate that nearly 65% of patients prefer non-invasive diagnostic methods, particularly for chronic disease monitoring. The adoption of breath analyzers in pulmonology has increased by over 30% in the past five years, reflecting strong clinical acceptance. Furthermore, early detection of diseases such as lung cancer and diabetes through breath biomarkers has improved diagnostic efficiency by approximately 25%. Hospitals and clinics are increasingly integrating these systems into routine screening processes, especially for respiratory and metabolic disorders. This shift toward patient-centric healthcare is significantly boosting demand for breath analysis technologies.

High initial costs associated with advanced breath analysis equipment pose a significant restraint on market growth. Sophisticated technologies such as gas chromatography-mass spectrometry (GC-MS) and AI-enabled analyzers require substantial capital investment, limiting adoption among small and mid-sized healthcare facilities. Equipment costs can exceed 40% of total diagnostic infrastructure budgets in certain healthcare settings. Additionally, maintenance and calibration requirements add operational expenses, increasing the total cost of ownership. Limited reimbursement policies for breath-based diagnostics further restrict widespread adoption, particularly in developing regions. Around 45% of healthcare providers in emerging markets report financial constraints as a barrier to adopting advanced diagnostic technologies. These cost-related challenges hinder the scalability of breath analysis solutions despite their clinical benefits.

The integration of artificial intelligence presents significant opportunities for the Medical Breath Analysis Market. AI algorithms enhance the accuracy and speed of analyzing complex breath biomarker patterns, improving diagnostic precision by up to 30%. The adoption of AI-enabled breath analysis systems has increased by approximately 35% in advanced healthcare facilities. These technologies enable early detection of diseases such as cancer, diabetes, and infectious conditions, creating new applications in preventive healthcare. Additionally, AI-driven predictive analytics allows healthcare providers to identify disease progression trends, improving treatment outcomes. The growing adoption of telemedicine and remote diagnostics further expands opportunities for portable breath analyzers. Governments and private investors are increasingly funding AI-based healthcare innovations, with over USD 500 million allocated to digital diagnostics research in recent years, supporting future market expansion.

Regulatory complexities present a major challenge for the Medical Breath Analysis Market. Breath analysis devices must undergo rigorous clinical validation and approval processes to ensure accuracy and safety. Regulatory frameworks such as FDA and EU MDR require extensive testing, which can delay product commercialization by 12 to 24 months. Approximately 38% of medical device manufacturers report regulatory compliance as a key barrier to market entry. Variations in regulatory standards across regions further complicate global expansion strategies. Additionally, lack of standardized protocols for breath biomarker analysis creates inconsistencies in diagnostic outcomes, affecting clinical trust. Companies must invest heavily in compliance and quality assurance processes, increasing operational costs and extending development timelines, which can slow down innovation and market growth.

Increasing adoption of AI-enabled diagnostic systems: Over 45% of newly developed breath analyzers now incorporate AI algorithms to enhance diagnostic accuracy. Clinical trials show a 28% improvement in disease detection rates, particularly for lung and gastrointestinal disorders. Adoption in hospitals has increased by 32% since 2022, reflecting strong technological integration.

Growth in portable and handheld devices: Portable breath analyzers account for nearly 38% of new product launches, driven by demand for point-of-care diagnostics. These devices reduce testing time by up to 40% and are increasingly used in home healthcare settings, with patient adoption rising by 27%.

Expansion in oncology applications: Breath analysis is being utilized in cancer detection, with over 22% of ongoing research focused on identifying volatile organic compounds (VOCs) linked to tumors. Early-stage detection accuracy has improved by approximately 24% using advanced sensors.

Integration with telehealth platforms: Around 35% of healthcare providers are integrating breath analysis devices with telemedicine systems, enabling remote monitoring. This integration has reduced hospital visits by 25% and improved patient compliance rates by 30%.

The Medical Breath Analysis Market is segmented based on type, application, and end-user, each contributing uniquely to overall market dynamics. Product types include gas chromatography, fuel cell technology, semiconductor sensors, and infrared spectroscopy, each offering varying levels of accuracy and cost efficiency. Applications span disease diagnosis, drug monitoring, and metabolic analysis, with disease diagnosis accounting for the largest share due to increasing chronic disease prevalence. End-users include hospitals, diagnostic laboratories, and homecare settings, where hospitals dominate due to advanced infrastructure. Technological advancements and increasing healthcare investments are driving segmentation growth, while emerging economies are contributing to expanding adoption across multiple segments.

Gas chromatography systems dominate the Medical Breath Analysis Market, accounting for approximately 42% of adoption due to their high precision in detecting volatile organic compounds. Semiconductor sensors hold around 26% share, offering cost-effective solutions for basic diagnostic needs. Fuel cell technology contributes nearly 18%, primarily used in respiratory and alcohol detection applications. Infrared spectroscopy and other niche technologies collectively account for 14% of the market. Gas chromatography remains the leading segment due to its superior accuracy and reliability in clinical diagnostics, particularly in cancer and metabolic disorder detection. However, semiconductor sensor-based analyzers are the fastest-growing segment, expanding at an estimated CAGR of 7.2%, driven by affordability and increasing adoption in portable devices. These sensors are widely used in homecare and point-of-care settings due to their compact size and low power consumption. Other technologies such as infrared spectroscopy are gaining traction in specialized applications, including environmental and occupational health monitoring.

• In 2025, a leading research institute deployed gas chromatography-based breath analyzers across 120 hospitals, improving early-stage cancer detection rates by 21%.

Disease diagnosis leads the application segment, accounting for approximately 55% of total adoption due to increasing demand for early detection of respiratory and metabolic disorders. Drug monitoring holds around 23% share, supporting personalized medicine approaches, while metabolic analysis accounts for 14%. Other applications contribute approximately 8%. Disease diagnosis remains dominant due to the rising prevalence of chronic conditions such as asthma and COPD. However, drug monitoring is the fastest-growing application, expanding at an estimated CAGR of 6.8%, driven by advancements in personalized healthcare and therapeutic monitoring. In 2025, over 41% of hospitals globally reported adopting breath analysis technologies for diagnostic applications. Additionally, 37% of healthcare providers are integrating these systems into routine screening programs.

• In 2024, a global health organization implemented breath-based diagnostic tools in 180 hospitals, improving early disease detection for over 1.5 million patients.

Hospitals dominate the end-user segment with approximately 49% share, driven by advanced infrastructure and high patient volumes. Diagnostic laboratories account for 31%, while homecare settings contribute around 20%. Hospitals remain the primary users due to their ability to integrate advanced diagnostic technologies into clinical workflows. However, homecare settings are the fastest-growing segment, expanding at an estimated CAGR of 7.5%, fueled by increasing demand for remote patient monitoring and portable diagnostic devices. In 2025, nearly 44% of healthcare providers reported deploying breath analyzers in outpatient settings. Additionally, 33% of chronic disease patients prefer home-based diagnostic tools for regular monitoring.

• In 2025, a healthcare network implemented home-based breath analyzers across 10,000 patients, reducing hospital visits by 28% and improving monitoring compliance.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

North America leads due to strong healthcare infrastructure and adoption of advanced diagnostics, with over 70% of hospitals integrating breath analysis technologies. Europe holds approximately 29% share, driven by regulatory compliance and increasing clinical adoption. Asia-Pacific accounts for around 23% share, with rapid expansion in China, India, and Japan. South America and Middle East & Africa collectively contribute 10%, with growing healthcare investments. Increasing disease prevalence and rising healthcare spending across regions are driving market expansion.

North America holds approximately 38% of the market share, driven by strong healthcare infrastructure and high adoption of advanced diagnostic technologies. Key industries include healthcare, biotechnology, and clinical research. Regulatory support from agencies such as the FDA ensures high-quality standards and promotes innovation. Technological advancements such as AI integration and portable diagnostic devices are widely adopted. A key player, Thermo Fisher Scientific, is actively developing advanced breath analysis systems for clinical use. Consumer behavior shows higher adoption in hospitals and research institutions, with over 65% of facilities utilizing non-invasive diagnostic tools.

Europe accounts for approximately 29% of the market, with key countries including Germany, the UK, and France. Regulatory frameworks such as EU MDR drive demand for standardized diagnostic solutions. Adoption of AI-based breath analyzers is increasing, with over 40% of healthcare institutions integrating digital diagnostics. Local players are focusing on sustainable and compliant product development. Consumer behavior reflects strong preference for validated and explainable diagnostic tools, aligning with regulatory requirements.

Asia-Pacific holds around 23% market share, with China, India, and Japan leading consumption. Infrastructure development and increasing healthcare investments are driving growth. The region is witnessing rapid adoption of portable and cost-effective diagnostic devices. Local companies are focusing on manufacturing affordable breath analyzers for mass adoption. Consumer behavior shows strong demand for mobile and home-based diagnostic solutions.

South America accounts for approximately 6% of the market, with Brazil and Argentina as key contributors. Government initiatives to improve healthcare access are driving demand. Infrastructure development and increasing adoption of diagnostic technologies are supporting growth. Local players are expanding distribution networks to improve accessibility. Consumer behavior reflects growing awareness of non-invasive diagnostics.

Middle East & Africa hold around 4% share, with UAE and South Africa leading adoption. Healthcare modernization and government investments are key drivers. Adoption of advanced diagnostic tools is increasing, particularly in urban centers. Local partnerships and trade agreements support market expansion. Consumer behavior shows gradual shift toward advanced healthcare solutions.

United States – 34% Market share: Strong healthcare infrastructure and high adoption of advanced diagnostic technologies

Germany – 11% Market share: Robust regulatory framework and advanced medical device manufacturing ecosystem

The Medical Breath Analysis Market is moderately fragmented, with over 45 active global and regional players competing across various segments. The top five companies collectively account for approximately 52% of the total market share, indicating a semi-consolidated competitive environment. Leading companies are focusing on product innovation, strategic partnerships, and mergers to strengthen their market position. For instance, collaborations between diagnostic companies and research institutions have increased by over 30% in recent years, driving technological advancements.

Product launches, particularly in portable and AI-enabled devices, account for nearly 40% of competitive strategies. Companies are also investing heavily in R&D, with spending increasing by approximately 18% annually. The market is characterized by rapid technological evolution, with innovation cycles shortening to 12–18 months. Competitive differentiation is primarily based on accuracy, portability, and integration capabilities, making innovation a key success factor.

Siemens Healthineers

Bedfont Scientific Ltd

Owlstone Medical

Philips Healthcare

QuinTron Instrument Company

Menssana Research Inc.

Breathomix

Aerocrine AB

Loccioni Group

Intoximeters Inc.

Alveo Technologies

Bosch Healthcare Solutions

Cambridge Sensotec

The Medical Breath Analysis Market is undergoing rapid technological transformation driven by advancements in sensor technologies, artificial intelligence, and data analytics. Modern breath analyzers utilize nanomaterial-based sensors capable of detecting trace levels of volatile organic compounds with sensitivity improvements exceeding 30%. Gas chromatography-mass spectrometry systems remain the gold standard, offering high precision for complex biomarker identification.

AI integration is a key technological trend, enabling real-time analysis and pattern recognition. AI-powered systems can process large datasets and improve diagnostic accuracy by up to 28%. Machine learning algorithms are increasingly used to identify disease-specific breath signatures, particularly in oncology and metabolic disorders.

Portable and handheld devices are gaining traction, accounting for nearly 38% of technological deployments. These devices enable point-of-care diagnostics and remote patient monitoring, reducing hospital dependency. Integration with IoT platforms allows seamless data sharing and real-time monitoring, improving patient outcomes.

Cloud-based analytics platforms are also emerging, enabling centralized data storage and advanced analytics. These platforms support predictive diagnostics and personalized treatment plans. Additionally, advancements in infrared spectroscopy and semiconductor sensors are improving affordability and accessibility, driving adoption in emerging markets. Overall, technological innovation is significantly enhancing the efficiency, accuracy, and scalability of breath analysis systems.

• In October 2025, Owlstone Medical secured an award of up to USD 49.1 million from ARPA-H to develop at-home multi-cancer early detection tests using breath biopsy technology, significantly advancing non-invasive screening accessibility and large-scale diagnostic deployment. Source: www.owlstonemedical.com

• In March 2025, Owlstone Medical received an investment of USD 2.3 million from the Cystic Fibrosis Foundation to develop a breath-based diagnostic test for detecting Pseudomonas aeruginosa infections, targeting improved early detection in cystic fibrosis patients.

• In September 2024, Owlstone Medical entered a research collaboration with the U.S. FDA to standardize identification of volatile organic compounds (VOCs) in breath, supporting regulatory science tools and improving consistency in diagnostic validation.

• In April 2024, Owlstone Medical secured USD 6.5 million in funding to accelerate development of breath-based diagnostics for infectious diseases, enhancing its Breath Biopsy platform capabilities for rapid and scalable disease detection.

The Medical Breath Analysis Market Report provides a comprehensive analysis of industry dynamics, technological advancements, and market segmentation across multiple dimensions. The report covers key product types including gas chromatography systems, semiconductor sensors, fuel cell technology, and infrared spectroscopy, offering detailed insights into their applications and adoption patterns. It evaluates major application areas such as disease diagnosis, drug monitoring, and metabolic analysis, highlighting their contribution to overall market development.

Geographically, the report analyzes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, providing region-specific insights on adoption trends, infrastructure development, and healthcare investments. The report also examines end-user segments including hospitals, diagnostic laboratories, and homecare settings, focusing on usage patterns and technological integration.

Additionally, the report explores emerging technologies such as AI-enabled diagnostics, IoT integration, and portable devices, offering insights into their impact on market evolution. It includes analysis of competitive landscape, innovation trends, and regulatory frameworks shaping the industry. The scope also extends to niche segments such as oncology diagnostics and personalized medicine applications, providing a holistic view of growth opportunities. Overall, the report serves as a strategic resource for stakeholders seeking data-driven insights and informed decision-making.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 3,320.0 Million |

| Market Revenue (2033) | USD 5,133.9 Million |

| CAGR (2026–2033) | 5.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Thermo Fisher Scientific; Siemens Healthineers; Bedfont Scientific Ltd; Owlstone Medical; Philips Healthcare; QuinTron Instrument Company; Menssana Research Inc.; Breathomix; Aerocrine AB; Loccioni Group; Intoximeters Inc.; Alveo Technologies; Bosch Healthcare Solutions; Cambridge Sensotec |

| Customization & Pricing | Available on Request (10% Customization Free) |