Reports

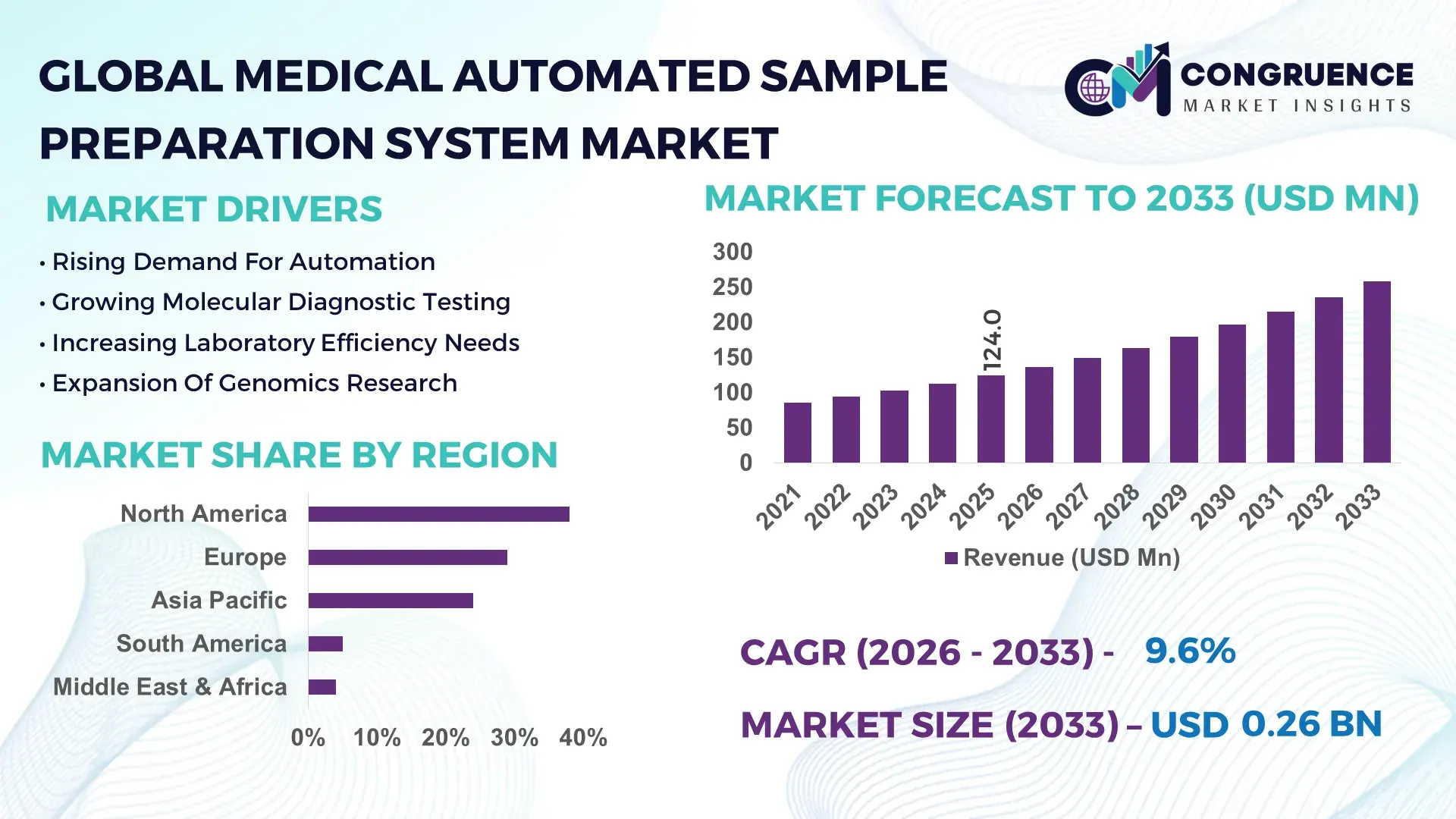

The Global Medical Automated Sample Preparation System Market was valued at USD 124.0 Million in 2025 and is anticipated to reach a value of USD 258.5 Million by 2033 expanding at a CAGR of 9.62% between 2026 and 2033. Rising deployment of AI-enabled liquid handling platforms, automated nucleic acid extraction systems, and robotics-integrated laboratory workflows is accelerating operational throughput by over 35% across diagnostic and pharmaceutical laboratories globally. Between 2024 and 2026, healthcare laboratories faced intensified pressure from post-pandemic testing optimization, stricter sample traceability regulations, and skilled labor shortages, forcing large-scale automation upgrades across North America, Europe, and Asia-Pacific.

The United States continues to dominate the Medical Automated Sample Preparation System market with approximately 34% global share, supported by more than 6,800 high-throughput clinical laboratories and over USD 4.5 billion annual investment in laboratory automation and precision diagnostics infrastructure. Pharmaceutical R&D facilities in the country increased automated sample processing deployment by nearly 41% between 2023 and 2025, significantly higher than several European counterparts where implementation expansion remained below 28%. Strong integration between biotech companies, hospital networks, and molecular diagnostics providers has accelerated demand for fully automated workflows capable of reducing manual preparation errors by nearly 45% while improving processing speed by over 50%.

As laboratory efficiency, reproducibility, and compliance standards become decisive competitive factors, companies are strategically prioritizing scalable automation ecosystems, AI-assisted workflow optimization, and regional manufacturing expansion to secure long-term operational advantage.

Market Size & Growth: The market reached USD 124.0 Million in 2025 and is projected at USD 258.5 Million by 2033, driven by 40% faster automated molecular diagnostics workflows.

Top Growth Drivers: Clinical lab automation adoption rose 38%, genomic testing demand increased 33%, and robotic liquid handling integration expanded 29% globally.

Short-Term Forecast: By 2028, automated sample processing is expected to reduce laboratory turnaround time by 31% and manual preparation errors by 27%.

Emerging Technologies: AI-guided sample tracking, robotic pipetting systems, and cloud-connected laboratory automation improved workflow accuracy by over 36%.

Regional Leaders: North America leads at USD 47 Million, Europe exceeds USD 33 Million, while Asia-Pacific approaches USD 29 Million through rapid hospital automation expansion.

Consumer/End-User Trends: More than 58% of advanced diagnostic laboratories shifted toward fully integrated automated preparation platforms during 2024–2025.

Pilot/Case Example: In 2025, a multi-site diagnostics deployment reduced sample contamination rates by 42% and increased throughput efficiency by 37%.

Competitive Landscape: Top manufacturers collectively control nearly 48% market share, led by Thermo Fisher Scientific, Agilent Technologies, Danaher, Qiagen, and PerkinElmer.

Regulatory & ESG Impact: Automated systems reduced reagent waste by 24% while supporting stricter laboratory traceability compliance across regulated healthcare markets.

Investment & Funding: Global laboratory automation investments exceeded USD 2.1 billion in 2025, fueled by strategic biotech partnerships and regional manufacturing expansion.

Innovation & Future Outlook: Next-generation modular automation and AI-driven workflow orchestration are reshaping high-throughput diagnostics and precision medicine laboratories globally.

Clinical diagnostics accounted for nearly 44% of overall Medical Automated Sample Preparation System demand, followed by pharmaceutical and biotechnology applications contributing approximately 32%, driven by rising genomic sequencing and high-throughput molecular testing requirements. Automated liquid handling and robotic extraction technologies improved laboratory productivity by more than 35% while reducing contamination incidents across regulated healthcare facilities. North America maintained strong infrastructure-led demand, whereas Asia-Pacific witnessed accelerated deployment due to localized manufacturing expansion and healthcare digitalization initiatives. Increasing supply chain regionalization and stricter laboratory compliance standards are further pushing companies toward scalable automation ecosystems, setting the stage for deeper strategic transformation across global laboratory operations.

The Medical Automated Sample Preparation System market is rapidly transforming into a critical competitive battleground for diagnostics providers, biotechnology firms, pharmaceutical manufacturers, and hospital laboratory networks seeking faster, error-free, and scalable processing capabilities. Rising pressure to manage expanding molecular diagnostics volumes, precision medicine workflows, and genomic sequencing complexity is accelerating the transition from manual preparation methods toward intelligent automation ecosystems capable of delivering higher reproducibility and operational consistency. As laboratories prioritize efficiency and compliance simultaneously, automation is shifting from an operational upgrade to a core strategic infrastructure investment.

Between 2024 and 2026, increasing regulatory scrutiny around laboratory traceability, contamination control, and reproducibility standards forced healthcare systems and contract research organizations to accelerate automation deployment across centralized testing facilities. AI-integrated sample preparation platforms now improve workflow efficiency by nearly 43% while reducing operational costs by approximately 29% compared to legacy semi-automated laboratory systems. This performance gap is fundamentally reshaping procurement strategies and vendor competition across the diagnostics value chain.

North America leads in overall processing volume and installed laboratory automation infrastructure, while Asia-Pacific leads in deployment acceleration with nearly 37% increase in new automated laboratory installations supported by healthcare infrastructure expansion and localized production initiatives. Europe remains strategically important for compliance-driven adoption, particularly within advanced molecular diagnostics and pharmaceutical quality-control applications. Over the next two to three years, laboratories deploying fully automated preparation workflows are expected to improve sample throughput capacity by over 46% while reducing technician-dependent manual intervention by nearly 40%. Sustainability is also emerging as a competitive differentiator, with automated reagent optimization systems lowering consumable waste by approximately 22%, improving both operational efficiency and ESG compliance positioning.

A major diagnostic laboratory network in 2025 reported a 34% reduction in sample processing turnaround time after integrating robotic liquid handling and AI-based workflow scheduling across multi-site testing operations. Simultaneously, major manufacturers are shifting capital allocation toward modular automation platforms, regional manufacturing hubs, and cloud-connected laboratory ecosystems to strengthen recurring revenue models and customer retention. The competitive landscape is increasingly defined by companies capable of optimizing automation scalability, compliance intelligence, and workflow integration simultaneously, making technological execution and infrastructure positioning decisive long-term competitive advantages.

The Medical Automated Sample Preparation System market is being reshaped by accelerating laboratory automation demand, expanding molecular diagnostics adoption, and rising pressure to improve operational precision across healthcare and pharmaceutical environments. Healthcare systems globally are prioritizing automated workflows to reduce manual handling variability, improve sample traceability, and support increasing diagnostic testing volumes. Advanced robotic liquid handling systems, automated nucleic acid extraction platforms, and AI-enabled workflow management tools are rapidly transforming laboratory infrastructure and operational models. The market is also influenced by workforce shortages within clinical laboratories, where automation deployment has improved sample processing efficiency by more than 35% across high-throughput testing facilities. Simultaneously, regulatory pressure surrounding contamination control, reproducibility, and digital traceability is forcing laboratories to modernize legacy preparation systems. Pharmaceutical and biotechnology companies are increasingly integrating fully automated sample preparation solutions into drug discovery and genomic research pipelines to reduce turnaround times and improve experimental consistency. As supply chains regionalize and healthcare systems invest in resilient diagnostic infrastructure, companies are accelerating strategic partnerships, manufacturing expansion, and cloud-enabled automation capabilities to strengthen long-term competitiveness.

The rapid expansion of molecular diagnostics, genomic testing, and precision medicine workflows is becoming the primary structural force accelerating Medical Automated Sample Preparation System adoption globally. Diagnostic laboratories processing infectious disease, oncology, and genetic testing samples have experienced testing volume increases exceeding 38% over the past two years, forcing laboratories to prioritize automated preparation platforms capable of handling higher throughput with lower error rates. Automated sample preparation systems reduce manual handling steps by nearly 45%, significantly improving reproducibility and contamination control across regulated laboratory environments. The global shortage of skilled laboratory technicians has further intensified automation investment, particularly in North America and Europe where workforce gaps exceeded 21% in several centralized diagnostic networks during 2025. Simultaneously, healthcare providers are under pressure to shorten test turnaround times while maintaining compliance with stricter traceability and quality-control regulations. In response, companies are accelerating robotic liquid handling deployment, expanding AI-assisted workflow integration, and forming strategic partnerships with molecular diagnostics providers. Several biotechnology firms increased automation-related capital allocation by more than 30% between 2024 and 2025, signaling a long-term operational shift toward scalable, digitally connected laboratory ecosystems.

Despite strong automation momentum, high implementation costs and complex laboratory integration requirements remain major structural restraints limiting broader Medical Automated Sample Preparation System adoption. Advanced robotic preparation platforms often require significant upfront investment in software integration, laboratory redesign, staff training, and workflow calibration, increasing deployment costs by nearly 28% compared to semi-automated systems. Smaller diagnostic laboratories and regional healthcare facilities continue facing budget constraints that delay large-scale modernization initiatives. Integration challenges are also intensifying as laboratories attempt to connect automated preparation systems with legacy laboratory information management systems (LIMS), cloud databases, and diagnostic analyzers. More than 32% of mid-sized laboratories reported operational disruption during automation transition phases in 2025, particularly where interoperability standards remained inconsistent across vendors. Global semiconductor supply concentration and precision component sourcing disruptions further extended equipment lead times across several regions between 2024 and 2025. To mitigate these risks, manufacturers are diversifying component sourcing strategies, offering modular automation platforms, and expanding service-based subscription models that reduce upfront infrastructure burden. Companies are also investing heavily in interoperability-focused software architectures to simplify multi-platform integration and accelerate deployment scalability.

AI-powered laboratory orchestration and decentralized diagnostic expansion are creating substantial strategic opportunities across the Medical Automated Sample Preparation System market. Intelligent workflow optimization systems are improving sample routing efficiency by over 41% while reducing reagent consumption by approximately 19%, making AI integration a major competitive differentiator for laboratories seeking operational optimization. Simultaneously, decentralized testing expansion across outpatient clinics, regional hospitals, and mobile diagnostic networks is increasing demand for compact, modular automated preparation systems capable of supporting distributed healthcare models. Asia-Pacific and Middle East healthcare modernization programs accelerated localized diagnostics deployment by nearly 34% between 2024 and 2025, opening new opportunities for scalable automation providers. Companies are increasingly developing portable, cloud-connected preparation platforms that support remote monitoring, predictive maintenance, and multi-site workflow synchronization. A non-obvious opportunity is emerging within pharmaceutical clinical trials, where automated preparation systems are reducing sample variability across geographically dispersed testing sites, significantly improving research consistency and regulatory readiness. In response, leading manufacturers are expanding AI-driven software capabilities, strengthening ecosystem partnerships with diagnostics companies, and building regional manufacturing hubs to capture rapidly expanding healthcare automation demand.

The Medical Automated Sample Preparation System market faces growing execution challenges related to interoperability complexity, evolving compliance standards, and operational scalability across diverse laboratory environments. Large healthcare systems increasingly require seamless integration between automated preparation systems, sequencing platforms, digital pathology tools, and centralized data infrastructure, yet interoperability inconsistencies continue delaying deployment timelines and reducing operational efficiency. Nearly 29% of healthcare laboratories reported workflow synchronization issues after integrating multi-vendor automation platforms during 2025. Escalating cybersecurity concerns are also emerging as laboratories transition toward cloud-connected automation ecosystems handling sensitive diagnostic data. Compliance requirements surrounding patient data protection, audit trails, and digital traceability increased software validation costs by nearly 18% across regulated healthcare markets. Additionally, infrastructure limitations in emerging economies continue constraining large-scale automation deployment despite rising diagnostics demand. Companies unable to optimize integration reliability, cybersecurity resilience, and service responsiveness risk losing long-term enterprise contracts. To remain competitive, manufacturers are accelerating investments in interoperable software architecture, localized technical support networks, predictive maintenance capabilities, and strategic collaborations with healthcare IT providers to strengthen execution scalability and customer retention.

42% Increase in AI-Integrated Laboratory Automation Deployment Reshaping Workflow Execution — Clinical laboratories are rapidly integrating AI-enabled scheduling, robotic pipetting, and digital sample tracking systems to improve processing consistency and reduce technician dependency. Automated workflow orchestration reduced preparation bottlenecks by nearly 31% during 2025, while cloud-connected monitoring improved operational visibility across multi-site laboratory networks. Companies are expanding software partnerships and embedding predictive maintenance tools to optimize uptime amid ongoing laboratory staffing shortages.

36% Expansion in Modular Automation Platforms Redefining Mid-Sized Laboratory Adoption — Demand is shifting toward scalable modular systems that allow laboratories to expand automation capacity without full infrastructure replacement. Mid-sized healthcare facilities increased modular platform deployment by approximately 36% as procurement teams prioritized flexible integration and lower implementation complexity. Vendors are restructuring product portfolios around compact automation units and subscription-based deployment models to address rising cost sensitivity and evolving regional procurement behavior.

28% Reduction in Reagent Waste Driving Sustainability-Focused Automation Upgrades — Laboratories are aggressively optimizing consumable usage and traceability performance in response to stricter compliance requirements and rising operating costs. Automated reagent dispensing systems lowered material waste by nearly 28% while improving batch consistency across molecular diagnostics workflows. Companies are increasingly redesigning platforms around energy-efficient operation and closed-loop reagent management systems to strengthen ESG positioning and regulatory readiness simultaneously.

33% Growth in Asia-Pacific Localized Manufacturing Accelerating Supply Chain Restructuring — Healthcare automation manufacturers are expanding regional production hubs across China, India, and Southeast Asia to reduce equipment lead times and improve pricing competitiveness. Localized component sourcing improved delivery efficiency by nearly 24% while reducing dependency on cross-border precision equipment shipments. Companies are forming regional partnerships and expanding localized service capabilities as faster deployment speed becomes a decisive competitive factor across high-growth healthcare infrastructure markets.

The Medical Automated Sample Preparation System market is segmented across type, application, and end-user categories, reflecting the increasing diversification of laboratory automation requirements across healthcare and life sciences industries. Demand remains heavily concentrated in high-throughput automated liquid handling and nucleic acid extraction systems due to their critical role in molecular diagnostics, genomic sequencing, and pharmaceutical research workflows. Clinical diagnostics applications account for the largest share of system deployment, while biotechnology and precision medicine laboratories are rapidly accelerating automation integration to improve scalability and reproducibility. Approximately 44% of total market demand is generated by hospital and centralized diagnostic laboratory networks, driven by rising testing volumes and compliance-focused workflow modernization. Simultaneously, pharmaceutical and biotechnology research applications are gaining momentum as automation adoption improves sample consistency and reduces operational variability by more than 30%. Companies are increasingly shifting product development toward modular automation architectures, AI-assisted workflows, and cloud-enabled laboratory integration platforms to capture expanding demand across both large-scale and decentralized testing environments.

Automated liquid handling systems dominate the Medical Automated Sample Preparation System market with approximately 39% share due to their scalability, workflow flexibility, and broad integration across molecular diagnostics, genomics, and pharmaceutical testing environments. Their ability to reduce manual pipetting errors by nearly 45% while improving throughput efficiency has positioned them as the foundational automation layer for high-volume laboratories. In contrast, automated nucleic acid extraction systems represent the fastest-growing segment with deployment expansion exceeding 34%, fueled by rising infectious disease testing, precision oncology, and genomic sequencing demand. The competitive dynamic between liquid handling platforms and extraction systems reflects a broader market transition from generalized automation toward specialized molecular workflow optimization. While liquid handling systems continue dominating large centralized laboratories due to integration flexibility and operational scalability, extraction-focused platforms are rapidly gaining adoption within decentralized diagnostics and point-of-care molecular testing environments. Remaining technologies, including automated centrifugation, sample purification, and integrated robotic preparation platforms, collectively account for nearly 27% share, maintaining strategic relevance in advanced pharmaceutical and clinical research applications. Manufacturers are increasingly prioritizing AI-enabled workflow coordination, modular platform expansion, and cloud-connected laboratory integration to strengthen competitive differentiation. Investment momentum is shifting toward platforms capable of supporting multi-assay automation, interoperability, and flexible deployment scalability, making intelligent workflow integration the key strategic battleground across the type landscape.

• According to a 2025 report by the International Federation of Clinical Chemistry, automated liquid handling systems were adopted by over 62% of high-throughput diagnostic laboratories, resulting in nearly 41% improvement in processing accuracy and workflow efficiency, reinforcing their growing strategic importance.

Clinical diagnostics remains the leading application segment within the Medical Automated Sample Preparation System market, accounting for approximately 46% of total deployment due to rising molecular testing volumes, infectious disease surveillance, and precision diagnostics expansion. Large diagnostic networks increasingly depend on automated preparation workflows to improve reproducibility, accelerate turnaround times, and strengthen contamination control compliance. Automated preparation systems reduced sample handling time by nearly 38% across high-volume clinical testing facilities during 2025. Genomics and molecular diagnostics applications represent the fastest-growing segment, expanding adoption by more than 35% as personalized medicine, oncology profiling, and next-generation sequencing workloads intensify globally. The contrast between mature clinical diagnostics applications and emerging genomics-focused workflows highlights a major operational transition from routine automation toward highly specialized precision testing ecosystems. Pharmaceutical research, biotechnology screening, and forensic testing applications collectively contribute approximately 32% market share while maintaining strong strategic relevance in high-complexity laboratory environments. Usage patterns are shifting toward integrated automation platforms capable of handling multi-assay workflows, decentralized sample processing, and AI-assisted laboratory coordination simultaneously. In response, companies are expanding cloud-based workflow management capabilities, investing in modular assay compatibility, and strengthening strategic partnerships with sequencing and molecular diagnostics providers. Demand is increasingly concentrating around platforms that optimize both operational throughput and regulatory traceability performance.

• According to a 2025 report by the Global Molecular Diagnostics Council, automated clinical diagnostic preparation systems were deployed across over 4,500 advanced laboratory networks, improving sample processing speed by 39%, highlighting their rapid operational adoption.

Hospitals and centralized diagnostic laboratories dominate the Medical Automated Sample Preparation System market with nearly 44% share, supported by rising diagnostic workloads, large-scale testing infrastructure, and increasing dependence on automated molecular workflows. These facilities prioritize high-throughput systems capable of reducing manual intervention, improving reproducibility, and supporting strict laboratory compliance standards. Automated preparation deployment within major hospital laboratory networks improved operational throughput by approximately 36% during 2025. Biotechnology and pharmaceutical companies represent the fastest-growing end-user segment, with automation adoption increasing by over 33% as drug discovery, genomic screening, and precision medicine research activities accelerate globally. The distinction between established hospital laboratory demand and rapidly scaling biotechnology adoption reflects a broader shift from routine automation toward innovation-driven research optimization. Academic research institutes, contract research organizations, and forensic laboratories collectively account for approximately 23% of market demand while maintaining specialized adoption patterns focused on assay flexibility and experimental precision. Buying behavior is increasingly centered around modular scalability, interoperability, and AI-assisted workflow management rather than standalone automation hardware. Companies are responding through customized deployment models, subscription-based software integration, and strategic laboratory ecosystem partnerships. Future demand is shifting toward end-users seeking scalable automation infrastructure capable of supporting decentralized testing, digital traceability, and precision diagnostics expansion simultaneously.

• According to a 2025 report by the International Laboratory Automation Association, adoption among biotechnology and pharmaceutical companies increased by 34%, with over 2,800 organizations implementing automated preparation workflows, leading to nearly 37% improvement in research efficiency and operational consistency, indicating a strong shift in demand dynamics.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.4% between 2026 and 2033.

North America maintains strong dominance due to its advanced diagnostic laboratory infrastructure, high molecular testing volumes, and early adoption of AI-enabled laboratory automation technologies. Europe captured approximately 29% market share, supported by strict laboratory compliance standards, sustainability-focused healthcare modernization, and widespread pharmaceutical research integration. Asia-Pacific accounted for nearly 24% share but is rapidly accelerating through healthcare infrastructure expansion, localized manufacturing investment, and large-scale diagnostics automation deployment across China, India, Japan, and Southeast Asia. South America and Middle East & Africa collectively represented approximately 9% share, driven by expanding hospital modernization initiatives and improving laboratory digitization. Ongoing supply chain regionalization and localized production strategies are pushing global manufacturers to prioritize Asia-Pacific expansion while maintaining innovation leadership and regulatory positioning in North America and Europe.

North America accounted for approximately 38% of the global Medical Automated Sample Preparation System market due to its highly developed clinical diagnostics infrastructure, strong pharmaceutical research ecosystem, and rapid deployment of AI-integrated laboratory automation platforms. The United States leads regional demand as centralized laboratory networks increasingly prioritize high-throughput molecular diagnostics and genomic sequencing workflows. More than 61% of advanced diagnostic laboratories upgraded automated preparation systems during 2024–2025 to improve sample traceability and reduce technician dependency. Regulatory pressure surrounding contamination control and digital audit compliance is accelerating investment in cloud-connected laboratory ecosystems and intelligent workflow orchestration tools. Major healthcare providers expanded robotic liquid handling deployment capacity by nearly 33% during 2025, while biotechnology companies intensified automation spending to accelerate precision medicine programs. Enterprise buyers increasingly prioritize interoperability, predictive maintenance capabilities, and scalable automation architectures, making North America the primary strategic region for premium innovation-focused expansion.

Europe represented nearly 29% of the global Medical Automated Sample Preparation System market, driven by stringent laboratory quality regulations, sustainability-focused healthcare modernization, and strong pharmaceutical manufacturing activity across Germany, France, the United Kingdom, and Switzerland. Laboratories across the region accelerated automation integration to comply with stricter traceability, contamination control, and digital documentation requirements introduced under evolving healthcare and in-vitro diagnostics frameworks. Approximately 54% of large European diagnostic facilities upgraded automated sample tracking and reagent optimization systems between 2024 and 2025 to improve compliance efficiency and reduce operational waste. Sustainability has become a major competitive factor, with automated reagent management platforms lowering consumable waste by nearly 24% across regulated laboratory environments. Pharmaceutical and biotechnology companies are increasingly prioritizing energy-efficient automation systems and modular workflow architectures to optimize compliance performance while controlling operational costs. Europe continues forcing technological adaptation and workflow innovation through regulation-driven operational transformation.

Asia-Pacific accounted for approximately 24% of the global Medical Automated Sample Preparation System market and remains the fastest-expanding regional hub due to accelerating healthcare infrastructure investment, localized manufacturing growth, and rising molecular diagnostics demand across China, India, Japan, and South Korea. Large hospital networks and biotechnology laboratories are rapidly deploying automated preparation systems to address rising testing volumes and laboratory workforce shortages. Localized production expansion improved regional equipment delivery efficiency by nearly 27% during 2025 while reducing procurement dependency on imported precision laboratory systems. China and India collectively represented over 58% of regional demand as healthcare systems accelerated laboratory digitization and centralized diagnostics expansion. More than 43% of newly established molecular testing laboratories across Asia-Pacific adopted modular automated preparation platforms due to their scalability and lower deployment complexity. Companies are aggressively expanding regional manufacturing, distribution, and technical support infrastructure, making Asia-Pacific the critical global market for scale-driven automation expansion and long-term deployment growth.

South America contributed approximately 5% of the global Medical Automated Sample Preparation System market, with Brazil and Argentina representing the largest regional demand centers due to expanding diagnostic laboratory modernization and rising infectious disease testing requirements. Public and private healthcare providers are increasingly investing in automated molecular testing workflows to improve sample consistency and reduce operational bottlenecks across centralized laboratory networks. However, infrastructure limitations, import dependency, and budget constraints continue restricting large-scale deployment across several healthcare systems. Nearly 37% of regional laboratories still rely on partially automated workflows due to high implementation costs and interoperability challenges. Despite these constraints, deployment of compact modular automation systems increased by approximately 22% during 2025, particularly among urban hospital laboratories prioritizing operational efficiency improvements. Enterprise buyers remain highly price-sensitive and prioritize scalable systems with lower maintenance requirements, positioning South America as a strategically attractive but execution-sensitive market balancing long-term opportunity against infrastructure risk.

Middle East & Africa accounted for nearly 4% of the global Medical Automated Sample Preparation System market, driven by expanding healthcare modernization programs, hospital infrastructure investment, and growing molecular diagnostics deployment across the United Arab Emirates, Saudi Arabia, and South Africa. Governments and private healthcare groups are accelerating laboratory automation adoption to strengthen diagnostic capacity, improve operational efficiency, and reduce dependence on overseas testing networks. Healthcare infrastructure investment across major Gulf countries increased automated laboratory deployment activity by approximately 26% during 2025, particularly within centralized diagnostics and infectious disease testing facilities. Strategic partnerships between healthcare providers and international laboratory technology companies are supporting rapid digital transformation and localized technical training initiatives. Enterprise buyers increasingly prioritize integrated automation platforms capable of reducing turnaround times and improving traceability compliance. As healthcare diversification strategies intensify across the region, Middle East & Africa is emerging as a strategically important market for infrastructure-led diagnostics automation expansion.

United States – 34% Market share: Dominates due to advanced molecular diagnostics infrastructure, high pharmaceutical R&D investment, and widespread deployment of AI-driven laboratory automation systems.

China – 16% Market share: Leadership is driven by rapid healthcare infrastructure expansion, localized automation manufacturing, and large-scale deployment of high-throughput diagnostic laboratory networks.

The Medical Automated Sample Preparation System market is characterized by intense competition between global laboratory automation leaders, precision diagnostics technology innovators, and regional cost-focused automation suppliers. Major companies including Thermo Fisher Scientific, Agilent Technologies, Danaher Corporation, Qiagen, and PerkinElmer collectively control approximately 48% of global market activity, competing aggressively across molecular diagnostics, genomics, and pharmaceutical laboratory automation ecosystems.

Competition is increasingly centered on workflow integration capability, AI-enabled automation intelligence, throughput optimization, and regulatory traceability performance rather than hardware pricing alone. Advanced robotic preparation platforms improved laboratory processing efficiency by over 40%, while modular automation systems reduced deployment complexity by nearly 28%, reshaping procurement priorities across healthcare networks. Global leaders are accelerating partnerships with diagnostics providers, expanding regional manufacturing capacity, and vertically integrating software orchestration tools to strengthen recurring revenue models and long-term enterprise retention.

The competitive landscape is shifting toward cloud-connected laboratory ecosystems and interoperable automation architectures, creating high entry barriers related to compliance validation, software integration, and technical service scalability. Companies capable of combining automation precision, AI-driven workflow intelligence, and rapid deployment support are positioned to outperform traditional hardware-centric competitors.

Agilent Technologies

Danaher Corporation

Qiagen

PerkinElmer

Tecan Group

Hamilton Company

Bio-Rad Laboratories

Roche Diagnostics

Eppendorf SE

Hudson Robotics

Aurora Biomed

Shimadzu Corporation

Analytik Jena

The Medical Automated Sample Preparation System market is rapidly evolving through the integration of AI-enabled workflow orchestration, robotic liquid handling, automated nucleic acid extraction, and cloud-connected laboratory management technologies. Automated robotic pipetting platforms improved sample handling precision by approximately 44% while reducing manual intervention across high-throughput molecular testing laboratories. Nearly 58% of advanced diagnostic facilities globally deployed partially or fully automated preparation workflows during 2025, accelerating the transition toward intelligent laboratory ecosystems.

Current technology adoption is heavily concentrated around modular automation systems capable of supporting multi-assay diagnostics, genomic sequencing, and pharmaceutical research simultaneously. AI-assisted scheduling and predictive maintenance tools reduced workflow downtime by nearly 27%, enabling laboratories to optimize throughput consistency and improve operational scalability. Companies benefiting most from these advancements include centralized diagnostics providers, biotechnology research organizations, and pharmaceutical quality-control laboratories requiring high reproducibility and traceability performance.

Compared to legacy semi-automated systems, next-generation AI-integrated sample preparation platforms improve workflow efficiency by over 43% while lowering operational costs by approximately 29%. Cloud-enabled automation integration is becoming a major competitive advantage as laboratories increasingly prioritize remote monitoring, interoperability, and multi-site coordination capabilities. Manufacturers are responding through ecosystem-focused software development, modular architecture expansion, and intelligent automation partnerships.

Between 2026 and 2028, decentralized diagnostics, portable molecular testing, and real-time laboratory analytics are expected to accelerate adoption of compact automated preparation systems optimized for distributed healthcare environments. Companies acting early on AI-driven interoperability, digital traceability, and scalable automation infrastructure are expected to secure stronger enterprise positioning as laboratory digitization rapidly intensifies globally.

June 2024 – Agilent Technologies partnered with ePrep for distribution of the ePrep ONE automated chromatography sample preparation workstation across selected regions, strengthening mass spectrometry-focused workflow automation capabilities. The platform improved preparation reliability through syringe-based precision handling while supporting scalable batch customization for laboratories. [Workflow Expansion] Source: www.eprep-analytical.com

January 2024 – Agilent Technologies announced a collaboration with Incyte to develop advanced companion diagnostics programs supporting hematology and oncology applications. The partnership targeted faster biomarker identification and precision diagnostics deployment as companion diagnostics adoption accelerated toward the projected USD 14 billion market opportunity. [Precision Alliance]

March 2025 – Thermo Fisher Scientific launched the Transcend VTLX-1 UHPLC system designed to automate online sample cleanup and preparation for LC-MS workflows. The system significantly reduced manual preparation steps while improving throughput consistency and assay reproducibility across clinical research and forensic laboratories. [Automation Acceleration]

March 2025 – Thermo Fisher Scientific introduced the Vulcan Automated Lab platform to improve semiconductor laboratory automation efficiency and process scalability. The integrated system enhanced productivity and yield optimization while reducing operational costs, reflecting the broader cross-industry acceleration of intelligent automated laboratory infrastructure deployment. [Integrated Intelligence]

The Medical Automated Sample Preparation System Market Report provides comprehensive coverage across automation technologies, laboratory applications, end-user industries, and major geographic regions shaping global demand transformation. The report evaluates key technology segments including automated liquid handling systems, nucleic acid extraction platforms, robotic preparation systems, AI-assisted workflow orchestration, and cloud-connected laboratory automation solutions. It further analyzes demand distribution across clinical diagnostics, genomics, pharmaceutical research, biotechnology, and forensic laboratory environments while assessing adoption behavior among hospitals, centralized diagnostic laboratories, biotechnology companies, and research institutions.

The report delivers detailed analytical coverage across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, incorporating more than 25 country-level operational and demand indicators. Over 58% of advanced diagnostic laboratories globally have shifted toward integrated automation workflows, while modular automation deployment increased by approximately 36% across mid-sized healthcare facilities during 2025. The study also profiles leading technology providers, regional expansion strategies, interoperability trends, and workflow optimization developments influencing competitive positioning.

Additionally, the report examines emerging opportunities within decentralized diagnostics, AI-enabled laboratory coordination, and scalable cloud-based automation ecosystems expected to reshape laboratory infrastructure between 2026 and 2033. It supports strategic decision-making related to investment prioritization, product expansion, manufacturing localization, partnership development, and competitive differentiation within rapidly transforming healthcare automation markets.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 124.0 Million |

| Market Revenue (2033) | USD 258.5 Million |

| CAGR (2026–2033) | 9.62% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Thermo Fisher Scientific; Agilent Technologies; Danaher Corporation; Qiagen; PerkinElmer; Tecan Group; Hamilton Company; Bio-Rad Laboratories; Roche Diagnostics; Eppendorf SE; Hudson Robotics; Aurora Biomed; Shimadzu Corporation; Analytik Jena |

| Customization & Pricing | Available on Request (10% Customization Free) |