Reports

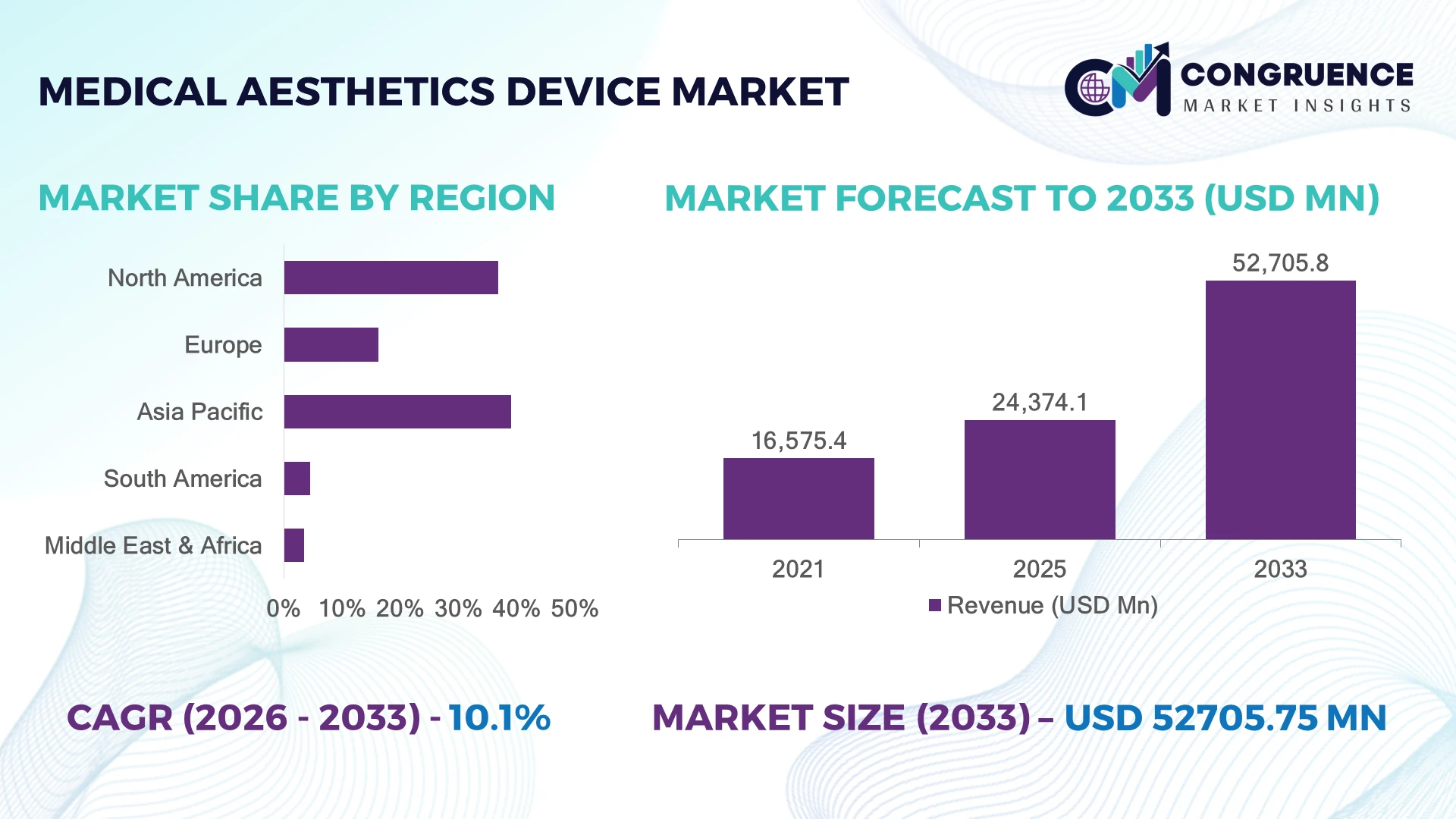

The Global Medical Aesthetics Device Market was valued at USD 24,374.09 Million in 2025 and is anticipated to reach a value of USD 52,705.76 Million by 2033 expanding at a CAGR of 10.12% between 2026 and 2033.Growth is accelerating through AI-enabled skin analysis systems, minimally invasive body contouring platforms, and energy-based treatment devices that reduce procedure time by nearly 30% while increasing clinic throughput across dermatology and cosmetic surgery networks.

The United States dominates the global medical aesthetics device market with nearly 38% share, supported by over USD 4.5 billion in annual aesthetic procedure spending, rapid adoption of robotic-assisted treatment platforms, and strong outpatient clinic expansion. South Korea follows as a high-density innovation hub, where advanced laser and RF device penetration exceeds 62% across premium dermatology centers. Rising U.S.-China medical technology trade restrictions in 2026 accelerated localized manufacturing investments across Asia-Pacific, while Germany strengthened Europe’s position through precision-engineered aesthetic systems exports and automated device integration in private clinics.

Manufacturers prioritizing AI-integrated treatment ecosystems, regionalized supply chains, and physician-training partnerships are securing faster commercial expansion and higher-margin clinical contracts in the high-growth global market.

Market Size & Growth: USD 24374.09 Million in 2025 reaching USD 52705.76 Million by 2033, driven by AI-enabled imaging, minimally invasive procedures, and clinic automation.

Top Growth Drivers: Non-invasive treatment demand rose 34%, AI-assisted diagnostics adoption increased 29%, and premium dermatology clinic expansion grew 21% globally.

Short-Term Forecast: By 2027, automated treatment planning platforms are expected to reduce procedure time by 26% and improve clinic utilization efficiency by 18%.

Emerging Technologies: AI skin mapping, robotic injectables, and advanced RF microneedling systems improved treatment precision by over 31% across high-volume clinics.

Regional Leaders: North America exceeds USD 18 billion with digital clinic integration, Asia-Pacific approaches USD 16 billion through manufacturing expansion, and Europe surpasses USD 11 billion with energy-based device adoption.

Consumer/End-User Trends: Over 57% of consumers now prefer non-surgical aesthetic procedures with shorter recovery periods and personalized treatment protocols.

Pilot/Case Example: In 2026, a multi-clinic laser optimization project reduced consumable waste by 19% and increased daily patient capacity by 24%.

Competitive Landscape: Leading manufacturers control nearly 46% market share, with strong competition among advanced laser, ultrasound, and RF platform providers.

Regulatory & ESG Impact: Sustainable device manufacturing programs lowered energy consumption by 17%, while stricter device compliance accelerated premium product replacement cycles.

Investment & Funding: Global investment exceeded USD 3.2 billion in 2026 through strategic partnerships, regional production facilities, and AI-driven aesthetics platforms.

Innovation & Future Outlook: Smart connected devices, cloud-based treatment analytics, and regenerative aesthetics technologies are reshaping long-term competitive positioning across global healthcare networks.

The Medical Aesthetics Device Market is advancing through strong demand for non-invasive facial rejuvenation, body contouring, and AI-assisted dermatology systems across outpatient clinics and specialty hospitals. Advanced RF, ultrasound, and laser platforms improved treatment precision by nearly 28% in 2026 while reducing recovery periods. Regional manufacturing diversification and tighter medical device compliance standards are accelerating localized supply-chain investments, creating a strong foundation for strategic expansion and technology-led competition.

The Medical Aesthetics Device Market is becoming strategically critical as healthcare providers, dermatology chains, and med-tech manufacturers compete through high-margin non-invasive treatment ecosystems and digitally integrated patient management platforms. In 2026, stricter medical device traceability standards in the United States and Europe accelerated localized component sourcing and cloud-connected treatment monitoring. Clinics adopting AI-assisted imaging and automated energy calibration systems reported nearly 27% faster patient turnaround and 18% lower consumable wastage, strengthening operational efficiency in high-volume aesthetic centers.

Advanced RF and ultrasound-based systems now outperform legacy standalone laser platforms by improving treatment precision by 31% while reducing recovery periods by nearly 22%. South Korea continues to lead in rapid deployment density and device innovation cycles, while Germany emphasizes precision-engineered systems with stricter compliance integration. In China, premium dermatology clinic expansion increased above 20% in Tier-1 cities, driven by rising demand for minimally invasive procedures and smart skin-analysis technologies. Over the next two years, AI-enabled treatment planning adoption is expected to exceed 45% across large multi-specialty aesthetic networks.

Aesthetic clinic operators are increasingly forming partnerships with software providers and device manufacturers to integrate diagnostics, treatment tracking, and subscription-based maintenance models into unified platforms. Companies investing in localized manufacturing, physician training infrastructure, and connected treatment ecosystems are securing stronger competitive positioning, faster deployment scalability, and higher long-term retention across the global medical aesthetics industry.

Non-invasive aesthetic procedures now account for more than 64% of total cosmetic interventions across developed healthcare markets, accelerating demand for advanced RF, ultrasound, and AI-guided laser platforms. In the United States, outpatient dermatology chains expanded treatment capacity by nearly 23% in 2026 through automated imaging and integrated patient workflow systems. South Korea strengthened export-focused manufacturing for energy-based devices as cross-border aesthetic tourism recovered above pre-2024 volumes. The shift toward shorter recovery cycles and personalized treatment protocols increased clinic utilization rates by 19%, directly improving operational profitability. In response, manufacturers are investing in AI-enabled diagnostics, physician certification programs, and localized assembly facilities to shorten delivery timelines and strengthen competitive positioning in premium treatment segments.

Advanced medical aesthetics systems continue to face deployment limitations due to elevated acquisition costs, component dependency, and tightening regulatory validation requirements. Multi-platform laser and RF devices experienced average component cost inflation of 14% in 2026 following semiconductor sourcing disruptions and stricter medical electronics certification rules in Germany and the United States. Smaller clinics in India and Southeast Asia reported installation delays exceeding 18% because of financing constraints and limited technical servicing infrastructure. These pressures directly affect scalability, replacement cycles, and operating margins for independent providers. To reduce exposure, manufacturers are expanding regional component sourcing networks, introducing modular device architectures, and securing long-term supplier agreements to stabilize procurement costs and maintain consistent product availability.

AI-driven treatment planning and connected skin diagnostics are creating high-value opportunities beyond conventional device sales. Smart imaging platforms improved treatment accuracy by 29% while reducing repeat corrective procedures by nearly 17% across advanced dermatology centers in Japan and the United States. Demand for subscription-based software ecosystems linked with aesthetic devices increased over 24% as clinics prioritized predictive maintenance and digital patient engagement tools. China is accelerating adoption of cloud-connected consultation platforms integrated with aesthetic treatment devices, particularly across urban private healthcare networks. Manufacturers are increasing R&D spending on regenerative aesthetics, robotic injectables, and adaptive energy calibration systems to secure recurring software-linked revenue streams. Companies developing integrated ecosystems instead of standalone hardware are positioning for stronger customer retention and higher long-term operational value.

The market faces increasing execution pressure from specialist workforce shortages, interoperability gaps, and complex multi-device integration requirements. More than 37% of mid-sized aesthetic clinics reported operational inefficiencies linked to inadequate technician training and inconsistent device calibration standards in 2026. In the United Kingdom and Canada, compliance audits for connected treatment systems increased substantially as cloud-linked diagnostic platforms expanded across outpatient networks. Integration failures between imaging software, patient databases, and treatment devices extended onboarding timelines by nearly 21%, reducing deployment consistency for multi-location operators. Companies must address these barriers through dedicated physician-training infrastructure, cybersecurity investment, and standardized interoperability frameworks. Firms capable of combining scalable digital integration with advanced clinical training will secure stronger operational resilience and long-term competitiveness in the evolving medical aesthetics ecosystem.

AI-Guided Treatment Expansion AI-assisted imaging and automated treatment calibration systems expanded across nearly 46% of premium dermatology clinics in 2026, reducing consultation time by 24% and improving procedural consistency by 19%. Clinics in the United States and Japan integrated cloud-linked diagnostic workflows to handle rising patient volumes with fewer manual adjustments. Device manufacturers are responding through software partnerships, subscription-based analytics platforms, and integrated ecosystem development to strengthen recurring service revenue and improve multi-location operational control.

Localized Manufacturing Realignment Medical device trade restrictions and semiconductor sourcing volatility accelerated regional manufacturing diversification, with over 31% of aesthetic device suppliers shifting partial production into South Korea, India, and Mexico during 2026. Lead times for advanced RF components declined by 17% after localized assembly adoption increased. Companies are restructuring procurement strategies, expanding supplier networks, and deploying modular device architectures to stabilize inventory availability and reduce operational exposure linked to cross-border logistics disruptions.

Rise of Energy-Based Platforms Multi-functional RF, ultrasound, and hybrid laser systems accounted for nearly 52% of newly installed aesthetic platforms in high-volume clinics, replacing single-function legacy devices with integrated treatment ecosystems. Clinics deploying combined energy-based systems improved room utilization efficiency by 21% while lowering maintenance complexity. Manufacturers are prioritizing platform consolidation, physician training partnerships, and software-enabled treatment customization to strengthen device retention and increase procedural flexibility across aesthetic networks.

Medical Spa Network Consolidation Large medical spa operators expanded aggressively across urban healthcare corridors, increasing multi-site deployment capacity by over 28% in 2026. Standardized treatment workflows and centralized procurement systems reduced operating costs by nearly 14% while improving patient throughput consistency. In Canada and Australia, labor shortages among certified aesthetic technicians accelerated automation adoption in consultation and imaging processes. Companies are responding through franchise partnerships, workforce certification programs, and integrated digital scheduling infrastructure to scale operations more efficiently.

Laser Devices remain the dominant segment in the Medical Aesthetics Device Market due to strong deployment scalability, multi-application capability, and established physician familiarity across dermatology clinics and cosmetic surgery centers. More than 48% of aesthetic treatment facilities in the United States continue to prioritize laser-based platforms for skin rejuvenation, pigmentation correction, and hair removal procedures because of faster treatment cycles and high procedural versatility. Manufacturers are enhancing laser precision through AI-assisted calibration and integrated cooling systems, improving treatment efficiency by nearly 22%. In contrast, Ultrasound Devices are emerging as the fastest-growing category as non-invasive lifting and contouring procedures gain wider acceptance among younger consumers seeking minimal recovery periods.

Radiofrequency Devices are strengthening adoption through lower maintenance complexity and improved compatibility with outpatient clinical workflows, while Body Contouring Devices are benefiting from rising demand for targeted fat reduction treatments in South Korea and Brazil. Skin Tightening Devices are also expanding steadily as aging demographics increase demand for minimally invasive anti-aging procedures. Companies are prioritizing hybrid platform development, strategic clinic partnerships, and software-integrated treatment systems to secure long-term procedural retention and expand premium service portfolios.

Skin Rejuvenation remains the leading application segment due to high repeat treatment frequency, broad demographic appeal, and expanding demand for minimally invasive anti-aging solutions. More than 54% of urban aesthetic clinics reported skin-focused procedures as their highest-utilization service category in 2026, supported by AI-assisted diagnostics and advanced laser resurfacing systems that improved treatment precision by nearly 26%. Facial Aesthetic Treatment is emerging as the fastest-growing application as younger patient groups increasingly adopt preventative aesthetic procedures integrated with digital skin analysis platforms. Providers are expanding treatment portfolios through automated imaging systems and personalized therapy planning to improve retention and increase procedural efficiency.

Hair Removal continues to maintain stable procedural demand because of standardized workflow integration and high-volume treatment scalability across medical spas and outpatient clinics. Body Contouring applications are strengthening through energy-based fat reduction technologies with shorter recovery cycles, while Tattoo Removal procedures are increasing steadily due to advancements in multi-wavelength laser systems reducing session requirements by nearly 18%. Companies are investing in multifunctional devices, subscription-based consultation platforms, and operator training programs to strengthen long-term patient engagement and optimize treatment throughput.

Dermatology Clinics represent the dominant end-user segment due to high procedural intensity, advanced diagnostic infrastructure, and consistent deployment of energy-based treatment systems. Nearly 44% of newly installed aesthetic devices in 2026 were deployed within specialized dermatology networks, particularly in the United States, South Korea, and Germany where outpatient cosmetic procedures continue expanding rapidly. Clinics improved patient throughput by approximately 21% through AI-assisted consultation systems and integrated scheduling platforms. Medical Spas are emerging as the fastest-growing end-user category as consumer preference shifts toward accessible, subscription-driven aesthetic services with shorter appointment cycles and personalized treatment plans.

Cosmetic Surgery Centers continue to maintain strong demand for advanced contouring and skin-tightening technologies requiring physician-led procedures, while Hospitals are focusing on integrated reconstructive and dermatological treatment capabilities. Beauty Clinics are increasingly adopting entry-level RF and laser systems to compete with premium service providers, and Ambulatory Surgical Centers are expanding minimally invasive procedural capacity through compact multifunctional platforms. Device manufacturers are targeting these segments with flexible financing models, operator certification programs, and customized software ecosystems to improve adoption scalability and long-term equipment utilization.

North America accounted for the largest market share at 36.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.4% between 2026 and 2033.

AI-Integrated Clinical Networks Accelerate Market Leadership

North America maintains the highest deployment concentration for advanced medical aesthetics systems due to strong outpatient infrastructure, premium cosmetic procedure demand, and rapid integration of AI-enabled diagnostic workflows. The region accounted for nearly 37% of global device installations in 2025, with the United States leading adoption of energy-based treatment systems across dermatology chains and medical spas. More than 42% of premium clinics integrated cloud-connected imaging and treatment calibration tools to improve procedural consistency and reduce consultation time. Device manufacturers are expanding regional training partnerships and localized servicing networks to support higher equipment utilization and recurring maintenance demand. Growing consolidation among multi-location aesthetic providers is also increasing procurement standardization and accelerating replacement cycles for legacy standalone systems.

United States Market Outlook: The United States remains the operational center of the North American market due to strong physician adoption, advanced reimbursement infrastructure for reconstructive procedures, and rapid expansion of private dermatology groups. In 2026, over 58% of large aesthetic clinic networks upgraded to multifunctional RF and laser platforms integrated with AI-assisted imaging systems. Domestic manufacturers are prioritizing software-linked treatment ecosystems, physician certification programs, and subscription-based maintenance contracts to strengthen long-term client retention and improve deployment scalability.

Precision Manufacturing and Compliance Modernization Reshape Deployment

Europe continues to strengthen its position through advanced medical device engineering, strict regulatory compliance, and rising adoption of minimally invasive treatment technologies. Germany, France, and Italy collectively represented over 61% of regional aesthetic device deployment activity in 2025, particularly across premium dermatology and cosmetic surgery centers. Stricter medical device traceability requirements increased demand for digitally connected treatment systems capable of automated documentation and workflow integration. European manufacturers improved energy efficiency in RF and laser systems by nearly 16% through sustainable hardware redesign and optimized cooling technologies. Companies are expanding partnerships with outpatient clinic networks and investing in localized service infrastructure to reduce maintenance downtime and strengthen long-term operational reliability.

Germany Market Outlook: Germany leads the European market through precision-engineered device manufacturing, advanced clinical integration capabilities, and strong export competitiveness in energy-based aesthetic technologies. More than 47% of premium cosmetic clinics in Germany adopted integrated laser-RF platforms with automated treatment tracking in 2026. Domestic manufacturers are strengthening interoperability standards and investing in AI-supported diagnostics to support compliance-heavy healthcare environments and improve procedural consistency across multi-site clinic operations.

High-Volume Manufacturing and Rapid Clinic Expansion Drive Scale

Asia-Pacific is emerging as the fastest-scaling medical aesthetics device market due to expanding private healthcare infrastructure, localized device manufacturing, and rising demand for non-invasive cosmetic procedures. China, South Korea, and Japan accounted for nearly 64% of regional deployment activity in 2025, supported by rapid expansion of dermatology clinics and medical spa chains. South Korea strengthened its role as a high-volume export hub for RF and laser systems, while China accelerated urban deployment of AI-integrated skin diagnostic platforms. Regional manufacturers reduced average device lead times by approximately 18% through localized component sourcing and modular assembly expansion. Companies are increasing investment in physician training ecosystems and strategic clinic partnerships to improve adoption scalability and strengthen premium service penetration.

China Market Outlook: China continues to expand aggressively through urban aesthetic clinic growth, domestic med-tech manufacturing, and strong digital healthcare integration. In 2026, AI-assisted skin analysis systems were deployed across more than 41% of newly established premium dermatology centers in Tier-1 cities. Domestic manufacturers are prioritizing cloud-connected treatment platforms, localized semiconductor sourcing, and strategic partnerships with private healthcare providers to improve operational resilience and reduce dependency on imported high-precision device components.

Urban Cosmetic Procedure Demand Supports Expansion

South America is experiencing steady operational expansion driven by growing urban cosmetic procedure demand, improving outpatient infrastructure, and wider adoption of minimally invasive treatment technologies. Brazil and Argentina represented nearly 68% of regional deployment concentration in 2025, supported by strong cosmetic surgery ecosystems and expanding medical spa networks. Clinics adopting multifunctional body contouring and skin-tightening systems improved treatment capacity by almost 19% while reducing procedural downtime. However, imported component dependency and uneven servicing infrastructure continue to limit deployment consistency outside major metropolitan centers. Manufacturers are responding through regional distributor partnerships, operator certification initiatives, and financing-focused sales models designed to improve equipment accessibility for mid-sized clinics.

Brazil Market Outlook: Brazil remains the strategic center of the South American market due to high cosmetic procedure volumes, strong physician specialization, and expanding private clinic networks. In 2026, nearly 52% of premium aesthetic centers in São Paulo and Rio de Janeiro upgraded to advanced ultrasound and RF-based contouring platforms. Device suppliers are strengthening local technical servicing infrastructure and physician education partnerships to improve long-term equipment utilization and reduce operational interruptions linked to imported replacement components.

Private Healthcare Investment Accelerates Technology Adoption

The Middle East & Africa market is advancing through premium healthcare infrastructure development, luxury medical tourism expansion, and increasing investment in private dermatology and cosmetic treatment facilities. The United Arab Emirates and Saudi Arabia collectively accounted for more than 57% of regional deployment activity in 2025, driven by rapid expansion of high-end outpatient aesthetic centers. Advanced laser and RF systems adoption increased by nearly 24% as clinics prioritized shorter treatment cycles and higher patient throughput. Governments and private healthcare operators are investing in specialized cosmetic treatment hubs, physician certification programs, and digitally integrated consultation systems to strengthen service quality and attract international medical tourism demand.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional modernization through premium clinic infrastructure, advanced imported device adoption, and strong healthcare diversification initiatives. In 2026, more than 46% of newly commissioned cosmetic treatment centers in Dubai integrated AI-supported imaging and cloud-based patient management systems. Operators are focusing on international physician partnerships, premium treatment standardization, and luxury outpatient service models to position the country as a high-value medical aesthetics destination with strong operational scalability.

Global leaders including Allergan Aesthetics, Cynosure, Cutera, Alma Lasers, and Lumenis compete directly against regional RF and laser manufacturers focused on lower-cost deployment models across Asia and Latin America. The top five players collectively control nearly 49% of the Medical Aesthetics Device Market through integrated treatment ecosystems, physician-training infrastructure, and premium clinic partnerships. Competition is centered on treatment precision, software integration, servicing speed, and consumable efficiency, with AI-assisted systems improving procedural consistency by over 25% and reducing calibration time by nearly 18%. Companies are expanding through localized manufacturing, cloud-connected diagnostics, and multi-clinic procurement agreements to secure long-term replacement cycles. Vertical integration in software, maintenance, and treatment analytics is reshaping competitive positioning, while stricter compliance standards are increasing barriers for low-cost standalone device suppliers. Winning in this market requires scalable clinical integration, fast servicing capability, physician loyalty, and continuous platform innovation.

Allergan Aesthetics

Cynosure

Cutera

Alma Lasers

Lumenis

Candela Medical

Fotona

Bausch Health Companies

Venus Concept

Solta Medical

InMode

Sciton

Merz Pharma

Lutronic Corporation

AI-assisted imaging, energy-based treatment platforms, and cloud-connected workflow systems are reshaping the Medical Aesthetics Device Market through higher procedural precision and faster clinical throughput. More than 44% of premium dermatology clinics deployed AI-supported skin analysis systems in 2026, reducing consultation time by nearly 24% and improving treatment planning consistency by 19%. Advanced RF and hybrid laser platforms are replacing standalone legacy systems by combining multiple procedures into one interface, lowering maintenance complexity and improving room utilization efficiency. Companies integrating diagnostics, treatment tracking, and software analytics into unified ecosystems are gaining stronger recurring-service advantages and higher equipment retention rates.

Emerging technologies including robotic injectables, adaptive ultrasound systems, and regenerative bio-material platforms are accelerating personalization across facial aesthetics and body contouring procedures. AI-guided calibration systems improved treatment accuracy by approximately 31% compared to conventional manual devices, while automated cooling technologies reduced post-procedure recovery periods by nearly 22%. Japan and South Korea are leading deployment density through high-volume outpatient clinics integrating digital treatment pathways and predictive maintenance software into everyday workflows.

Between 2026 and 2028, connected aesthetic ecosystems and software-linked devices will become major competitive differentiators as clinics prioritize operational scalability and multi-location standardization. Manufacturers investing early in AI integration, cloud interoperability, and modular device platforms will secure faster deployment cycles, stronger physician loyalty, and greater long-term procedural control.

March 2026 – Allergan Aesthetics presented 21 scientific e-posters at the AMWC Congress, highlighting rapid-onset TrenibotE neurotoxin performance with visible improvement reported as early as 8 hours after treatment. The development strengthened Allergan’s evidence-based positioning and expanded physician confidence in multimodal aesthetic treatment strategies.

January 2026 – Allergan Aesthetics unveiled nine new clinical data presentations at IMCAS 2026 covering injectables, biostimulatory fillers, and neurotoxin technologies. The company demonstrated strong patient satisfaction outcomes through Phase 3 and Phase 4 studies, reinforcing its premium innovation leadership and supporting broader physician adoption across facial aesthetic treatment portfolios.

August 2024 – InMode began large-scale delivery of newly launched aesthetic platforms after securing pre-orders that increased pro-forma quarterly performance to USD 102.6 million. The rollout improved consumables and service activity by 13%, strengthening the company’s recurring operational revenue model and expanding procedural platform utilization beyond traditional RF systems. Source: nasdaq.com

May 2024 – InMode expanded commercialization of next-generation minimally invasive treatment platforms, with proprietary surgical technologies contributing 84% of quarterly operational activity. Record consumables and service growth improved long-term platform retention and strengthened the company’s competitive positioning across integrated subdermal and non-invasive aesthetic procedure categories.

The Medical Aesthetics Device Market report provides comprehensive analysis across Laser Devices, Radiofrequency Devices, Ultrasound Devices, Body Contouring Devices, and Skin Tightening Devices, with detailed assessment of operational deployment trends, technology integration, and evolving clinical utilization patterns. The study evaluates major applications including Skin Rejuvenation, Hair Removal, Tattoo Removal, Body Contouring, and Facial Aesthetic Treatment while analyzing demand concentration across Hospitals, Dermatology Clinics, Cosmetic Surgery Centers, Medical Spas, Beauty Clinics, and Ambulatory Surgical Centers. More than 45% of current market deployment activity is concentrated within AI-assisted and energy-based treatment ecosystems integrated into outpatient cosmetic networks.

The report delivers region-wise insights across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, covering manufacturing concentration, infrastructure modernization, regulatory shifts, and competitive positioning between 2026 and 2033. It also evaluates emerging technologies such as robotic injectables, cloud-connected diagnostic platforms, regenerative aesthetics, and software-linked treatment systems. Strategic analysis supports expansion planning, procurement optimization, partnership evaluation, investment prioritization, and long-term competitive differentiation across high-growth medical aesthetics ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 24,374.09 Million |

|

Market Revenue in 2033 |

USD 52,705.76 Million |

|

CAGR (2026 - 2033) |

10.12% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Allergan Aesthetics, Cynosure, Cutera, Alma Lasers, Lumenis, Candela Medical, Fotona, Bausch Health Companies, Venus Concept, Solta Medical, InMode, Sciton, Merz Pharma, Lutronic Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |