Reports

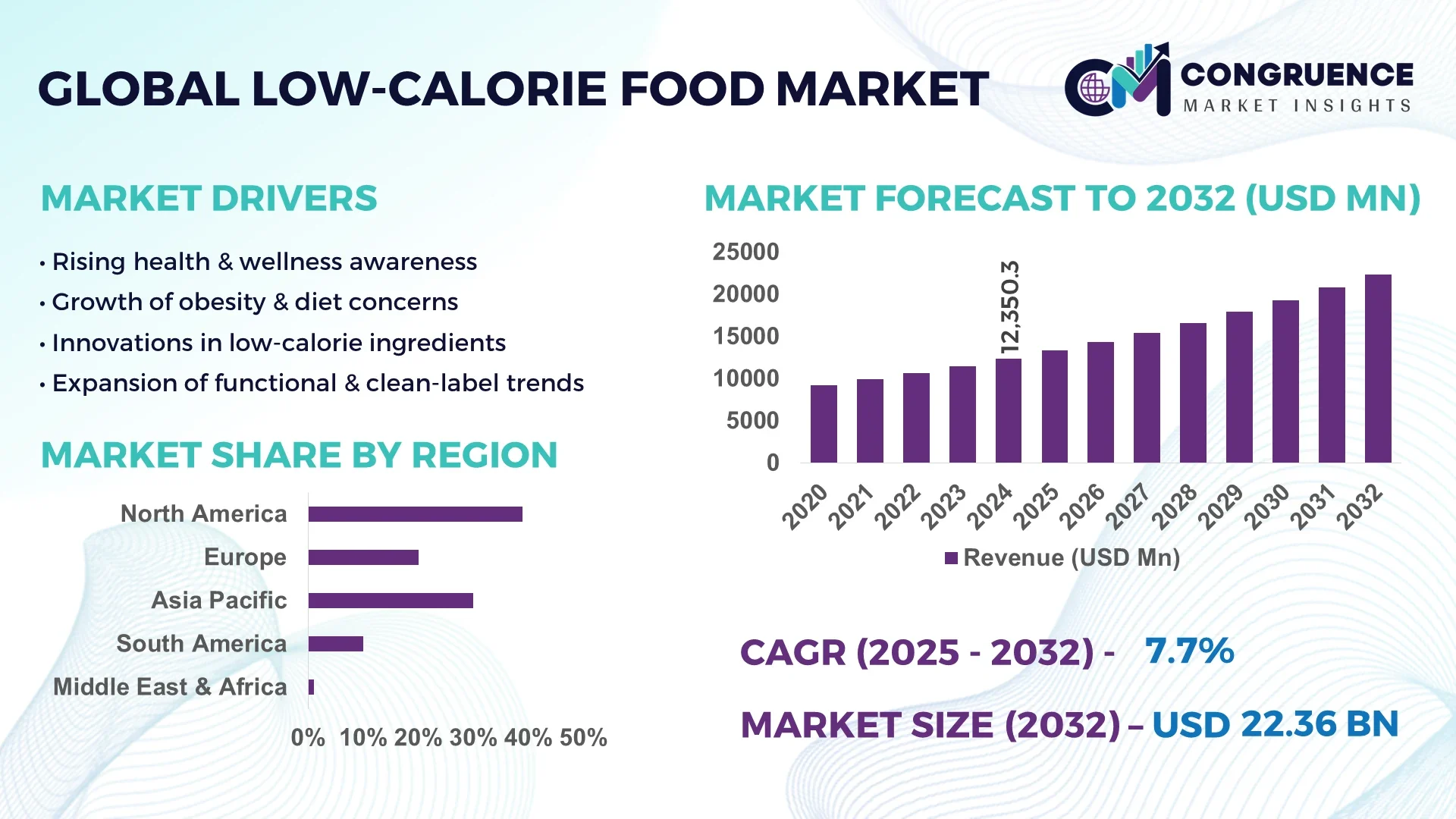

The Global Low-calorie Food Market was valued at USD 12,350.28 Million in 2024 and is anticipated to reach a value of USD 24,077.87 Million by 2032 expanding at a CAGR of 7.7% between 2025 and 2032. This growth is primarily driven by increasing consumer demand for health-oriented food products and shifting dietary preferences toward low-sugar and reduced-fat alternatives.

The United States dominates the global low-calorie food market, backed by strong production capabilities, high R&D investment in food formulation, and advanced distribution infrastructure. The country hosts more than 400 active low-calorie product manufacturing facilities, with annual investments exceeding USD 1.2 billion in alternative sweeteners and protein-based food innovations. Adoption of low-calorie products among urban consumers in the U.S. surpassed 68% in 2024, driven by technological advancements in natural sugar substitutes and the integration of AI-driven nutritional analytics in product development.

Market Size & Growth: Valued at USD 12.35 Billion in 2024, projected to reach USD 24.07 Billion by 2032, expanding at a CAGR of 7.7%. Growth driven by increased demand for functional and low-calorie food products.

Top Growth Drivers: 1) Rising health awareness (42%), 2) Expanding availability of sugar-free formulations (36%), 3) Increasing use of natural sweeteners such as stevia and monk fruit (28%).

Short-Term Forecast: By 2028, production efficiency of low-calorie food lines is expected to improve by 18% through process automation and ingredient optimization.

Emerging Technologies: AI-driven nutritional profiling, precision fermentation for calorie reduction, and advanced microencapsulation of flavor and nutrients.

Regional Leaders: North America projected to reach USD 9.8 Billion by 2032 with strong retail penetration; Europe forecasted at USD 7.1 Billion driven by clean-label demand; Asia-Pacific expected to hit USD 5.6 Billion led by urban dietary shifts.

Consumer/End-User Trends: Growing adoption among millennials and fitness-focused consumers; 54% of users actively prefer low-calorie snacks and beverages over traditional products.

Pilot or Case Example: In 2024, a collaborative project between PepsiCo and Cargill achieved a 22% reduction in sugar content using AI-optimized sweetener formulations.

Competitive Landscape: Market leader Nestlé holds approximately 14% share, followed by Danone, Unilever, PepsiCo, and General Mills.

Regulatory & ESG Impact: Stricter sugar tax frameworks and sustainability labeling mandates across major economies are promoting reformulated low-calorie food launches.

Investment & Funding Patterns: Over USD 2.8 Billion invested in 2023–2024 in low-calorie ingredient innovation and digital nutrition platforms.

Innovation & Future Outlook: Integration of nutrigenomics, sustainable ingredient sourcing, and real-time calorie tracking technologies are shaping the next phase of market evolution.

The Low-calorie Food Market is expanding across diverse industry sectors including bakery, confectionery, beverages, and ready-to-eat meals, each contributing significantly to overall demand. Recent technological advancements in sweetener formulation, precision fermentation, and texture modification are redefining product innovation and consumer satisfaction. Regulatory emphasis on sugar reduction and sustainable labeling continues to influence product development and marketing strategies globally. The market’s growth is further supported by shifting dietary patterns in Asia-Pacific and Europe, where urban populations are increasingly adopting functional and calorie-controlled foods. Future outlook remains strong with emerging innovations in bio-based ingredients and AI-driven personalization of dietary products.

The strategic relevance of the Low-calorie Food Market lies in its alignment with global health, sustainability, and innovation goals. As consumers increasingly seek functional and nutritionally optimized products, companies are leveraging new technologies to enhance formulation efficiency, shelf stability, and nutritional accuracy. Smart food processing technology delivers 28% improvement in nutrient retention compared to conventional heat-based processing, offering significant differentiation for manufacturers focusing on clean-label, low-calorie products. North America dominates in production volume, while Europe leads in adoption with 61% of enterprises incorporating low-calorie formulations into their product portfolios.

By 2027, AI-powered nutritional modeling is expected to improve formulation accuracy by 25%, reducing production waste and ingredient variability. Firms are committing to ESG-aligned improvements such as achieving 35% packaging recyclability and 20% carbon emission reduction by 2030. In 2024, Japan achieved a 30% sodium reduction in processed foods through a precision fermentation initiative led by Ajinomoto, setting a measurable benchmark for regional innovation in low-calorie formulation.

Looking ahead, the Low-calorie Food Market is poised to become a cornerstone of sustainable nutrition, underpinned by digital transformation, bio-ingredient innovation, and strong regulatory compliance. It represents a resilient growth pathway for food manufacturers adapting to global shifts toward health-conscious, eco-efficient, and technology-integrated food systems.

Rising consumer health awareness has become a major catalyst for the Low-calorie Food Market. With more than 70% of global consumers actively seeking products with reduced sugar and fat content, manufacturers are innovating through nutritional optimization and ingredient substitution. Studies indicate that 62% of millennials and Gen Z consumers prefer foods with calorie transparency and functional benefits such as protein enrichment or fiber infusion. The growth of digital health platforms and fitness applications has reinforced this trend, linking dietary behavior with measurable outcomes. As a result, major food companies are investing heavily in low-calorie alternatives across bakery, beverages, and dairy segments, reflecting a clear shift toward preventive health consumption.

The Low-calorie Food Market faces production constraints stemming from ingredient cost fluctuations and formulation challenges. Natural sweeteners such as stevia, erythritol, and monk fruit extracts often exhibit variable global pricing, with cost volatility reaching up to 18% annually due to limited agricultural yield and extraction inefficiencies. Furthermore, replicating the taste and texture of traditional high-calorie foods requires advanced R&D and precision blending, leading to increased operational expenditure. Small and mid-sized manufacturers encounter barriers in adopting specialized processing technologies, impacting scalability. These cost pressures, combined with stringent labeling standards and regional regulatory inconsistencies, continue to challenge sustained profitability across market participants.

The integration of AI-driven precision nutrition presents significant opportunities for the Low-calorie Food Market. AI and data analytics can optimize ingredient ratios, reducing formulation time by 30% while maintaining taste and nutritional balance. By 2026, AI-enabled manufacturing systems are projected to lower product development cycles by 22%, supporting agile responses to consumer demand. Additionally, wearable health technology adoption is expanding the personalized nutrition market, where low-calorie foods play a pivotal role in daily dietary management. Food producers leveraging smart production lines and digital quality monitoring can achieve higher efficiency, better traceability, and enhanced regulatory compliance, creating long-term competitive advantages in the evolving food ecosystem.

Regulatory disparities and consumer perception issues remain critical challenges for the Low-calorie Food Market. Variations in ingredient approval standards across regions—such as differing limits on artificial sweeteners between the EU and the U.S.—create compliance burdens for multinational producers. Additionally, despite growing demand, 27% of consumers still perceive low-calorie foods as less flavorful or highly processed, impacting adoption rates. Maintaining sensory satisfaction while ensuring calorie reduction requires extensive R&D and marketing investment. Furthermore, the industry faces tightening regulations around health claims and labeling accuracy, necessitating transparency and scientific validation. Overcoming these challenges is vital for ensuring consumer trust and facilitating consistent global market expansion.

• Expansion of Functional Ingredient Integration: The adoption of functional ingredients such as plant-based proteins, probiotics, and omega-3 fatty acids is accelerating across low-calorie food categories. In 2024, approximately 58% of newly launched low-calorie products included added nutritional fortification, up from 43% in 2022. Manufacturers are increasingly focusing on multifunctional ingredient blends that enhance both taste and health value, with over 35% of R&D investments in 2024 directed toward fortification technologies. This trend supports the shift toward holistic nutrition, catering to the growing consumer base prioritizing wellness-driven consumption.

• Growth in Ready-to-Eat (RTE) and On-the-Go Products: Convenience remains a dominant purchasing factor, with 62% of consumers preferring RTE low-calorie options over traditional packaged meals. Urban working populations and fitness-conscious demographics are driving innovation in portion-controlled, shelf-stable snacks and beverages. Between 2023 and 2024, the launch rate for RTE low-calorie meals increased by 27%, emphasizing demand for time-efficient nutrition solutions. This shift is influencing supply chain agility and encouraging automation across packaging and distribution operations.

• Rising Adoption of Natural Sweeteners and Clean-Label Formulations: The transition toward natural, plant-derived sweeteners is reshaping product formulations. Stevia-based and monk fruit–based sweeteners accounted for 46% of total sweetener usage in 2024, compared to 31% in 2021. Consumer demand for clean-label transparency led 72% of manufacturers to reformulate products without artificial additives. Regulatory pressure for reducing synthetic ingredients further amplifies this movement, fostering brand differentiation and improved consumer trust.

• Digital and AI-driven Personalization in Food Development: The integration of digital analytics and AI in low-calorie food innovation increased by 33% year-over-year in 2024. Companies now employ predictive algorithms to align calorie profiles with consumer dietary data, enhancing product targeting efficiency by 25%. Personalized diet platforms are driving cross-collaboration between food producers and health-tech firms, with 48% of new low-calorie brands incorporating AI-based nutritional customization tools. This technological alignment underscores the market’s evolution toward data-driven food solutions.

The Low-calorie Food Market segmentation reveals distinct patterns across type, application, and end-user categories, reflecting the diversification of consumer demand and production capabilities. By type, low-calorie sweeteners, beverages, and dairy alternatives hold substantial portions due to increasing demand for sugar-free and protein-enriched options. Applications span across bakery, confectionery, beverages, and ready meals, each influenced by regional dietary behaviors and lifestyle trends. End-user segmentation highlights strong adoption by retail, foodservice, and health-focused outlets catering to the wellness-driven population. The growing alignment of product innovation with consumer data analytics and sustainability objectives continues to refine segmentation balance, strengthening market adaptability and investment attractiveness.

Low-calorie sweeteners currently account for approximately 38% of the global market, making them the leading type due to their widespread integration across food and beverage manufacturing. Beverages follow with around 27% share, driven by the proliferation of low-sugar drinks in urban centers. Dairy alternatives, including low-fat yogurts and protein-enriched milk products, represent 21%, while snacks and bakery substitutes collectively hold the remaining 14%. The fastest-growing segment is low-calorie dairy alternatives, projected to grow at a CAGR of 8.2% due to heightened lactose-free and plant-based demand. Comparatively, stevia-based formulations deliver 22% better taste retention than older artificial sweeteners, leading to greater consumer preference. Increasing technological advancements in extraction and blending processes are enhancing ingredient stability and sweetness perception.

The beverage segment dominates the Low-calorie Food Market, accounting for 41% of total applications, attributed to the surge in functional drinks, zero-sugar sodas, and fortified water. Bakery and confectionery applications follow at 29%, where calorie reduction is achieved through ingredient substitution and precision fermentation. Ready-to-eat meals hold 19%, and dairy-based foods represent the remaining 11%. The fastest-growing application segment is functional beverages, projected to grow at a CAGR of 9.1%, supported by increasing consumer focus on hydration and nutrition synergy. In comparison, low-calorie beverage reformulations deliver 26% higher ingredient efficiency than traditional syrup-based production. Manufacturers are implementing cold-blending technologies that enhance nutrient retention and taste stability.

Retail and supermarkets represent the leading end-user segment, accounting for 46% of Low-calorie Food Market distribution, as consumers increasingly purchase health-centric food products through organized retail networks. Foodservice outlets, including cafés and quick-service restaurants, contribute 31%, while e-commerce channels account for 17% and institutional buyers (such as hospitals and fitness centers) hold 6%. The fastest-growing end-user category is e-commerce, projected to expand at a CAGR of 10.4%, fueled by digital ordering platforms and AI-driven nutrition tracking. Retail adoption rates in developed economies reached 63% in 2024, while online health-food platforms recorded a 29% year-over-year increase in low-calorie product listings. Foodservice chains are rapidly adapting to this trend, integrating reduced-calorie menus with real-time calorie disclosure systems.

North America accounted for the largest market share at 39% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.4% between 2025 and 2032.

Europe followed with a 28% share, while South America and the Middle East & Africa represented 18% and 15%, respectively. In 2024, over 63% of global low-calorie product innovations originated from North America, particularly within beverages and snacks. Meanwhile, Asia-Pacific witnessed a 32% year-over-year increase in low-calorie product launches, driven by growing middle-class consumers and urbanization. Europe continues to lead regulatory standardization, with 74% of its food manufacturers committed to reformulation targets. South America and the Middle East are showing accelerating adoption, fueled by digital retail platforms and government-backed nutrition campaigns. The combination of regional diversification, technology integration, and health-focused consumer preferences continues to shape the competitive global landscape of the Low-calorie Food Market.

North America held a 39% share of the global Low-calorie Food Market in 2024, supported by strong industrial infrastructure and significant R&D investments in low-calorie formulation. Key industries driving demand include beverages, bakery, and ready-to-eat food manufacturing. Regulatory frameworks such as sugar reduction targets and front-of-pack calorie labeling have accelerated innovation, with over 68% of companies adopting AI-assisted recipe optimization. Local players like PepsiCo and General Mills are investing in natural sweetener R&D and digital food formulation technologies. The region also demonstrates high consumer preference for functional low-calorie foods, with 61% of adults purchasing reduced-sugar products regularly. North American consumers favor personalized nutrition solutions, supported by digital tracking and health apps that influence their dietary choices.

Europe captured approximately 28% of the global Low-calorie Food Market in 2024, led by countries such as Germany, the United Kingdom, and France. The region’s focus on sustainability and regulatory compliance has accelerated low-calorie product innovation, with 72% of food manufacturers reformulating to reduce sugar, salt, and artificial additives. Regulatory bodies like the European Food Safety Authority (EFSA) have implemented strict labeling standards, promoting transparency and consumer trust. Digital transformation in food production is also advancing, with 45% of European producers integrating AI-based quality control systems. Companies such as Danone and Unilever are pioneering eco-efficient packaging and zero-sugar formulations. European consumers are increasingly guided by ethical and environmental considerations, favoring locally sourced, plant-based low-calorie alternatives.

Asia-Pacific ranked second in total market volume in 2024 and is projected to grow the fastest through 2032. China, India, and Japan collectively accounted for over 57% of the region’s low-calorie food consumption. The expansion of digital retail networks and smart manufacturing infrastructure has enhanced access to health-oriented foods. Technological advancements, including precision fermentation and AI-assisted product design, are driving localized innovation. Regional players in Japan and South Korea are pioneering hybrid plant-based low-calorie foods integrating traditional flavors with modern health attributes. Consumer adoption is expanding rapidly through e-commerce platforms, where mobile health apps influence over 48% of purchase decisions. Asia-Pacific consumers are increasingly prioritizing nutrition transparency and low-calorie convenience products for urban lifestyles.

South America accounted for 18% of the global Low-calorie Food Market in 2024, with Brazil and Argentina emerging as the key contributors. Government-led nutrition campaigns and sugar taxation initiatives are spurring the adoption of healthier food alternatives. The market benefits from expanding production facilities and ingredient innovation in Brazil, where over 40% of beverage manufacturers introduced low-calorie options in 2024. Local producers are leveraging regionally sourced natural sweeteners such as stevia and fruit concentrates to align with sustainability goals. Consumer awareness has increased significantly, with 52% of surveyed consumers reporting a shift toward reduced-calorie products. Regional foodservice outlets are also incorporating calorie disclosure menus, influencing purchase decisions in urban centers.

The Middle East & Africa region represented 15% of the global Low-calorie Food Market in 2024, driven by increasing urbanization, diversification of food production, and strong health awareness campaigns. The UAE and South Africa are leading markets, accounting for 63% of regional consumption. The region is witnessing modernization in food technology, with smart processing facilities and clean-label reformulations gaining momentum. Local producers are focusing on calorie-conscious foods aligned with cultural dietary preferences. In 2025, a UAE-based company introduced a fully AI-monitored production line that improved formulation consistency by 27%. Regional consumers are highly responsive to health marketing, with 46% preferring low-calorie foods linked to wellness or fitness benefits.

United States – 27% Market Share: Dominance attributed to advanced production infrastructure, strong R&D investment in sweetener technologies, and high consumer adoption of low-sugar food alternatives.

China – 18% Market Share: Leadership driven by large-scale manufacturing capabilities, rapid expansion of digital retail channels, and growing middle-class demand for low-calorie packaged foods.

The Low-calorie Food Market is highly competitive and moderately fragmented, with over 350 active global competitors spanning product manufacturing, ingredient innovation, and digital nutrition services. The combined market share of the top five companies — Nestlé, Danone, Unilever, PepsiCo, and General Mills — accounts for approximately 54% of the global market. These leaders maintain dominance through robust R&D, strategic partnerships, and targeted product launches, with more than 420 new low-calorie products introduced globally in 2024 alone. Innovation trends include AI-assisted formulation, plant-based ingredient development, and smart nutrition analytics, with 48% of market leaders integrating advanced technology to improve product efficiency and taste profiles. Strategic initiatives such as mergers and acquisitions are shaping competition, with 27 major collaborations recorded in 2024, targeting both emerging markets and product portfolio expansion. The competitive landscape is further intensified by mid-sized players focusing on niche segments such as clean-label, organic low-calorie foods, which account for 21% of the market, creating a dynamic environment where innovation and adaptability are critical for sustained leadership.

PepsiCo, Inc.

General Mills, Inc.

The Kraft Heinz Company

Ajinomoto Co., Inc.

Cargill, Incorporated

Tate & Lyle PLC

Ingredion Incorporated

Kerry Group plc

SunOpta Inc.

The Low-calorie Food Market is undergoing significant transformation through the adoption of advanced technologies that enhance product development, manufacturing efficiency, and consumer engagement. Artificial intelligence is increasingly deployed to create low-calorie products that maintain taste and texture while optimizing nutritional profiles. By 2024, approximately 42% of leading manufacturers had adopted AI-assisted recipe formulation tools, reducing development time by 18% and improving product consistency. Blockchain technology is also being leveraged to enhance transparency and traceability in ingredient sourcing and production processes, with 37% of manufacturers employing blockchain-based verification systems to ensure authenticity and compliance with evolving regulatory requirements. Smart packaging solutions such as QR codes and embedded nutritional labels are growing in adoption, providing consumers with real-time product information and contributing to informed purchase decisions. In developed markets, adoption of smart packaging rose by 29% in 2024. Sustainable manufacturing technologies are another key driver, with automated energy-efficient processing lines reducing waste generation by up to 21% in recent initiatives. These technological advancements are enabling companies to meet evolving consumer expectations while strengthening operational efficiency and aligning with sustainability objectives.

In May 2023, Nestlé introduced its Vital Pursuit line, targeting users of GLP-1 weight-loss drugs like Ozempic and Wegovy. The line includes 12 high-protein, nutrient-rich products such as frozen protein pasta and sandwich melts, portioned to match the reduced appetite of weight-loss drug users. These products are priced under $5 and became available by late 2024.

In August 2023, Conagra Brands launched a "GLP-1 friendly" label on 26 Healthy Choice frozen meals, highlighting their suitability for consumers using appetite-suppressing medications. The meals are high in protein, low in calories, and fiber-rich, catering to the dietary needs of this growing consumer base.

In November 2024, South Korean companies like Daesang Corp and Samyang Corp expanded production of allulose, a natural sugar substitute with near-zero calorie content. Despite its higher cost compared to table sugar, allulose is gaining popularity due to its taste similarity to sugar and is widely available in South Korean supermarkets.

In June 2024, California became the first U.S. state to ban ultra-processed foods in school meals under the new law AB1264. The legislation mandates that "particularly harmful" ultra-processed foods be defined by 2028, with schools beginning to phase them out by 2029 and implementing a complete ban by 2035. This initiative targets foods high in sugar, salt, and additives, aiming to provide students with healthier meal options.

The Low-calorie Food Market Report offers a comprehensive analysis of the global low-calorie food industry, encompassing various market segments, geographic regions, applications, technologies, and industry focus areas. The report delves into product types such as low-calorie snacks, beverages, dairy items, and meal replacements, providing insights into their market share and growth potential. It also examines distribution channels, including online retail, supermarkets, and specialty stores, highlighting their impact on market dynamics. Geographically, the report covers key regions such as North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, analyzing regional market trends, consumer behavior variations, and regulatory influences. The scope extends to emerging markets and niche segments, identifying opportunities for growth and innovation.

Technological advancements play a crucial role in shaping the low-calorie food market. The report explores the adoption of artificial intelligence in product development, blockchain for supply chain transparency, smart packaging solutions, and sustainable manufacturing technologies. These innovations are driving efficiency, enhancing consumer engagement, and aligning with sustainability objectives. Furthermore, the report addresses industry focus areas, including the growing demand for functional foods, the influence of weight-loss medications on dietary preferences, and the impact of regulatory changes on product formulations. It provides a detailed overview of the factors influencing market growth, challenges faced by industry players, and strategic initiatives undertaken to capitalize on emerging opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 12350.28 Million |

|

Market Revenue in 2032 |

USD 24077.87 Million |

|

CAGR (2025 - 2032) |

7.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Nestlé S.A., Danone S.A., Unilever PLC, PepsiCo, Inc., General Mills, Inc., The Kraft Heinz Company, Ajinomoto Co., Inc., Cargill, Incorporated, Tate & Lyle PLC, Ingredion Incorporated, Kerry Group plc, SunOpta Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |