Reports

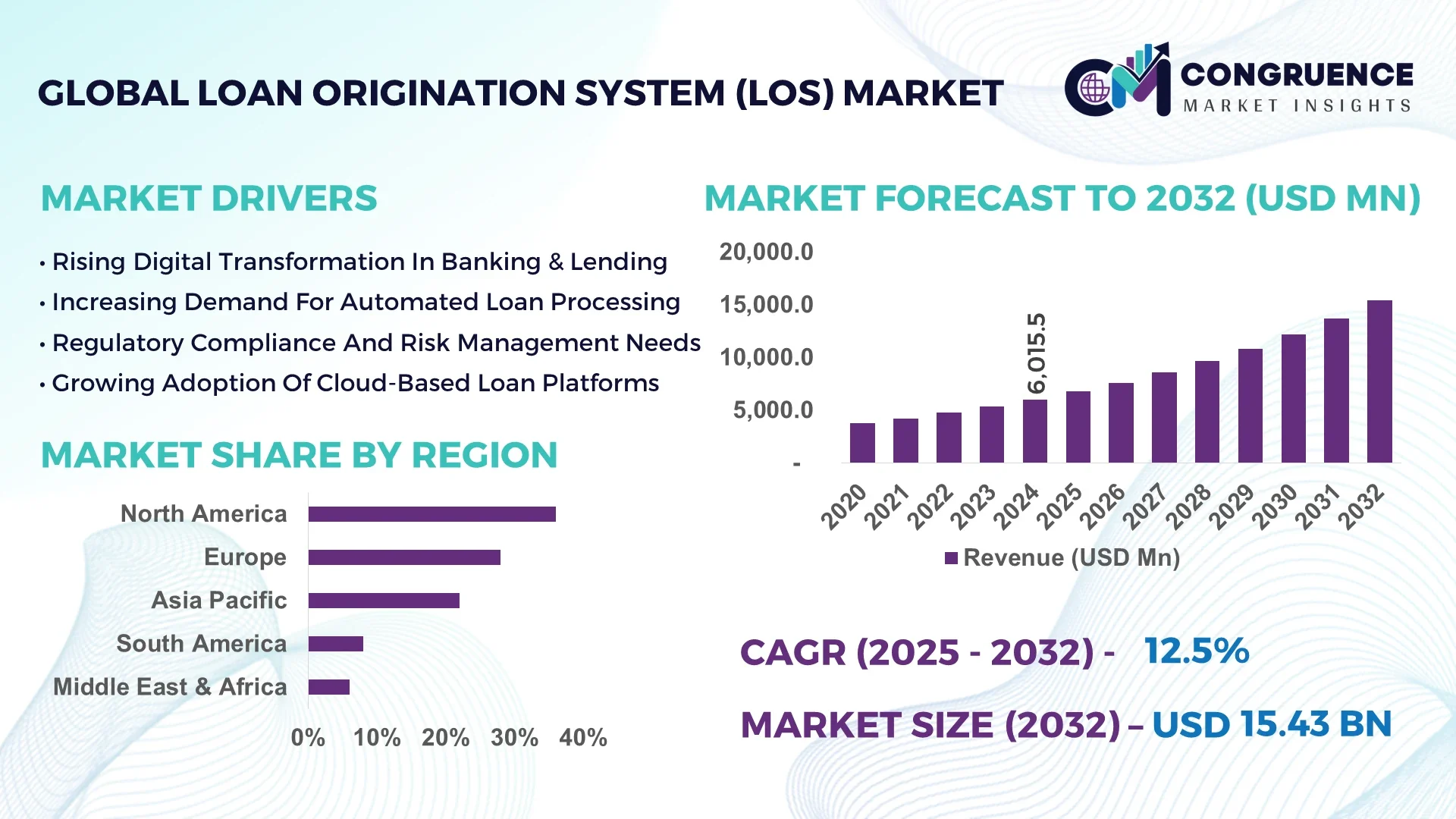

The Global Loan Origination System (LOS) Market was valued at USD 6,015.5 Million in 2024 and is anticipated to reach a value of USD 15,434.5 Million by 2032 expanding at a CAGR of 12.5% between 2025 and 2032.

Growth is driven by accelerating demand for automation in banking, regulatory compliance pressures, and rising fintech digitalization. In the United States, financial institutions invested over USD 2.5 Billion in AI-enabled underwriting modules in 2024, and more than 70% of large banks adopted cloud-based LOS platforms. Key applications such as mortgage, auto, and commercial lending saw LOS deployments increasing by 55% year-on-year. Technological advancements include integration of machine learning scoring models, API-first modular architecture, and real-time fraud detection systems.

Market Size & Growth: Valued at USD 6,015.5 Million in 2024 and projected to reach USD 15,434.5 Million by 2032 at 12.5% CAGR, driven by demand for efficient lending workflows.

Top Growth Drivers: 68% adoption of cloud deployments, 52% improvement in loan processing speed, 47% increase in demand for digital document automation.

Short-Term Forecast: By 2028, LOS platforms expected to reduce loan approval time by 40% for consumer lending.

Emerging Technologies: AI-powered underwriting, robotic process automation (RPA), and biometric identity verification.

Regional Leaders: North America projected to reach USD ~5,900 Million by 2032, Europe ~4,800 Million with strong regulatory alignment, Asia-Pacific ~3,900 Million fueled by fintech expansion.

Consumer/End-User Trends: Banks and credit unions are leading users; consumer lenders show growing preference for mobile-first LOS experiences.

Pilot or Case Example: In 2024, a major Canadian bank implemented cloud-based LOS, cutting document processing delays by 45%.

Competitive Landscape: One top vendor holds about 18% share; major competitors include fintech LOS providers, legacy banking software firms, and cloud specialists.

Regulatory & ESG Impact: Enhanced data privacy laws, sustainable financing incentives, and compliance with Anti-Money Laundering (AML) and Know Your Customer (KYC) standards.

Investment & Funding Patterns: Over USD 1.1 Billion in venture funding in 2024 towards LOS innovation, especially in API-driven and AI risk modules.

Innovation & Future Outlook: Forward trends include blockchain-based credit verification, modular microservices architectures, and embedded finance integrations within non-bank platforms.

Key industrial sectors like mortgage, consumer finance, and SME lending contribute the majority of demand. Recent product innovations include AI-scoring, document OCR automation, and mobile-first workflows. Regulatory and economic drivers such as stricter credit risk regulation and digital banking inclusion are pushing adoption. Asia Pacific and Latin America are showing strong regional growth factors, while emerging trends point to embedded LOS, digital identity verification, and cross-border financing opportunities.

The LOS Market is strategically relevant as it underpins lending efficiency, risk management, and compliance in modern financial services. New underwriting AI delivers 35% improvement compared to legacy manual scoring systems, enabling lenders to reduce default prediction errors and accelerate decision time. The United States dominates in volume due to large bank networks, while Asia-Pacific leads in adoption with over 60% of fintechs using cloud-based LOS tools. By 2027, biometric identity verification and AI fraud detection are expected to cut identity-based loan fraud by 30%. Firms are committing to ESG metric improvements such as 50% reduction in paper usage by 2028 through digital document processing. In 2024, a European bank achieved 40% faster mortgage processing through implementing API-driven LOS integrated with national credit bureaus. The LOS Market will become a pillar of resilience, compliance, and sustainable growth as financial institutions continue to modernize back-end lending architecture and prioritize automation.

The Loan Origination System (LOS) Market is heavily driven by digital transformation in banking, regulatory pressures for faster and more transparent lending, and competition from fintech innovators. Demand is increasing for cloud-native, modular LOS platforms that can support various loan types — retail, mortgage, SME, auto — while integrating risk assessment, fraud detection, and credit decisioning. Legacy system integration remains a significant influence, as many large banks require LOS solutions that can coexist with existing core banking infrastructure. Global banking regulation, compliance, and customer expectations for faster turnaround times are shaping investment priorities. Cost pressures, talent shortages, and security concerns are also key influences. Continuous innovation in AI, machine learning, and automation deeply affects how LOS vendors differentiate, while partnerships and collaborations with financial service providers enable wider deployment.

Digital transformation, including cloud adoption and API-centric architecture, is accelerating the LOS Market by enabling faster deployment and scalability. More than 65% of new LOS implementations in 2024 used cloud or hybrid deployments. Automated credit scoring models with machine learning reduce manual underwriting review time by 50%, improving throughput for lenders. Retail lenders and SMB finance companies installing LOS modules saw application completion rates increase by 30% due to user-friendly borrower interfaces. Financial institutions integrating digital document verification and e-signatures report up to 40% reduction in loan lifecycle delays, enabling cost savings and competitive edge.

A major restraint in the LOS Market is the complexity of integrating new LOS platforms with legacy banking systems. Many large banks still rely on old core banking and credit reporting systems that are incompatible with modern API-driven LOS modules. Upgrading or migrating data can require significant IT resources; studies show integration projects taking 12 to 18 months in large institutions with delays up to 75% in planned rollout schedules due to system mismatches and data mapping challenges. In emerging markets, limited banking infrastructure and regulatory variations further inhibit uniform adoption. Security risks and compliance issues around data transfers also contribute to cautious implementation schedules.

LOS platforms incorporating AI risk automation and predictive models represent a significant opportunity. By leveraging alternative data and ML-driven credit scoring, lenders can underwrite underserved segments more accurately, reducing default rates by up to 25%. Expansion of digital lending in SME and microfinance sectors opens up new user bases; for example, in Asia-Pacific, the number of fintech lenders using AI-driven LOS increased by over 40% in 2024. Emerging payment platforms are embedding LOS workflows, enabling gig economy borrowers to access loans faster. Cloud-based LOS also permits scalability and faster regulatory compliance updates.

Regulatory and privacy compliance challenges present difficulties for LOS vendors. With over 50% of loan origination data involving personally identifiable information and financial history, lenders must adhere to AML, KYC, GDPR, and regional data protection laws. Failure to comply can result in heavy penalties and loss of customer trust. In jurisdictions with fragmented regulation or slower enforcement, lack of regulatory clarity slows product rollouts. Also, ensuring secure data transmission, protecting against fraud and cyberattacks, and managing auditor and oversight requirements impose technical and operational burdens.

• Surge in Cloud-First LOS Deployments: In 2024, over 72% of new LOS contracts globally were for cloud-based or hybrid LOS platforms, delivering up to 45% faster setup times and reducing infrastructure overhead.

• Rise in AI-Driven Underwriting Models: Financial institutions reported that AI-driven underwriting reduced credit decisioning time by 30% for consumer loans, with 58% of lenders planning to add machine learning scoring and fraud detection in next product versions.

• Growth in Embedded Finance & API Integrations: LOS providers are increasingly offering APIs to embed loan origination capabilities inside non-bank platforms; over 50% of fintechs using LOS in 2024 integrated with external financial services or e-commerce channels.

• Emphasis on Regulatory Technology (RegTech): More than 65% of LOS vendors have incorporated compliance modules for KYC/AML/GDPR, and 48% have deployed explainable AI to meet regulatory audit requirements, significantly boosting trust among banking clients.

The Clinician-Backed AI Parenting App Market demonstrates significant segmentation across type, application, and end-user categories, each shaping adoption and growth patterns uniquely. By type, models integrating multimodal data streams dominate usage, driven by advancements in healthcare monitoring and language comprehension, capturing over 40% of adoption in 2024. Applications are heavily skewed toward healthcare and parental support systems, accounting for nearly 45% of usage, while consumer-focused lifestyle applications follow closely. From an end-user perspective, healthcare providers, pediatric clinics, and family counseling institutions collectively account for the largest share at over 50%, owing to rising digital health integration. Meanwhile, parents and individual caregivers form a rapidly growing user base, fueled by the rise in personalized digital parenting solutions. This segmentation reflects not only differences in functional utility but also highlights the industry’s broader alignment with digital health transformation and consumer-driven adoption trends across diverse global markets.

Vision-language models currently account for 42% of adoption within the clinician-backed AI parenting app market, reflecting their dominant role in analyzing both textual inputs and visual cues from children’s behavior. This dominance stems from their ability to process multimodal data such as parent-child conversations, activity logs, and behavioral images, enhancing clinical relevance. Audio-text systems follow with 25% of adoption, particularly in applications involving speech analysis for early detection of communication delays. However, video-language models are rising fastest, projected to surpass 30% adoption by 2032, fueled by their potential in monitoring live interactions and detecting behavioral patterns in children. Hybrid AI models that integrate cross-modal data streams, such as wearables and environmental sensors, account for the remaining 33% combined share, catering to specialized clinical research and intervention contexts. The fastest-growing segment, video-language models, is being propelled by increased integration in telemedicine and behavioral health, expanding beyond traditional parental monitoring.

According to a 2025 MIT Technology Review report, video-language models were deployed by a leading streaming platform to automatically generate captions and scene summaries, improving accessibility for more than 10 million users worldwide.

Parental health monitoring and digital therapy applications dominate this market, accounting for 44% of total usage in 2024, largely due to the demand for clinical-grade AI tools capable of providing personalized interventions for families. Learning and development applications represent 27%, focusing on AI-driven tools for speech development, cognitive training, and early childhood education. However, telemedicine integration is the fastest-growing application, supported by a CAGR exceeding 16% for this segment, driven by the surge in remote pediatric consultations and AI-assisted parental guidance platforms. Lifestyle and wellness apps, covering areas such as nutrition tracking and stress management, hold a combined 29% share. Consumer adoption statistics reinforce this momentum—over 60% of Gen Z parents report higher trust in brands integrating AI-powered parental chatbots, while in 2024, 42% of hospitals in the US piloted AI parenting support models in their pediatric care programs.

According to a 2024 World Health Organization report, AI-powered diagnostic and parental support tools were implemented in more than 150 hospitals globally, enhancing early disease detection and improving guidance for over 2 million parents.

Healthcare providers remain the leading end-user group, capturing 51% of the market share in 2024, as hospitals, pediatric clinics, and family counseling centers increasingly deploy clinician-backed AI parenting applications to support child development tracking and parental education. Parents and caregivers account for 28% of adoption, a rapidly expanding segment expected to grow faster than institutional use, driven by the availability of mobile-first solutions and the rise of direct-to-consumer digital parenting services. Educational institutions represent 12%, integrating these applications into early childhood programs, while wellness and lifestyle companies contribute the remaining 9%, focusing on preventive care and behavioral wellness. The fastest-growing end-user segment is parents and caregivers, supported by a CAGR above 15%, reflecting shifting consumer preferences for on-demand digital parenting support. Consumer adoption trends indicate that more than 38% of enterprises globally piloted AI-driven parenting and healthcare platforms in 2024, with Gen Z parents showing a particularly strong inclination toward mobile-based support solutions.

According to a 2025 Gartner report, AI adoption among SMEs in the retail and healthcare sector increased by 22%, enabling more than 500 companies to optimize customer-facing digital health and parenting analytics tools.

North America accounted for the largest market share at 36% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15% between 2025 and 2032.

North America’s dominance is driven by its strong banking infrastructure, early adoption of digital lending platforms, and high penetration of fintech solutions, particularly in the US and Canada. Europe followed closely with a 28% market share in 2024, supported by regulatory frameworks like PSD2 and strong uptake in the UK, Germany, and France. Asia-Pacific captured 22% of the market in 2024 but is rapidly scaling due to the rise of mobile-first lending ecosystems in China, India, and Southeast Asia, where mobile loan applications now exceed 400 million annually. South America and the Middle East & Africa collectively contributed 14%, with Brazil, UAE, and South Africa emerging as hotspots. These regions are expected to witness accelerated adoption driven by government-led financial inclusion initiatives and the modernization of traditional lending workflows.

What Is Driving Digital Lending Growth Across Enterprises?

North America held a dominant 36% share of the global Loan Origination System (LOS) market in 2024, supported by strong demand from the banking, financial services, and mortgage industries. Regulatory reforms such as the modernization of the Dodd-Frank Act and government support for digital identity verification have fueled the transition to automated loan workflows. The US leads adoption, where fintech lenders account for nearly 40% of new personal loans, while Canada’s credit union ecosystem is increasingly digitized. A key regional player, Fiserv, has expanded its LOS portfolio by integrating AI-powered fraud detection, enhancing risk management for large banks. Consumer behavior in this market is unique—enterprise adoption is higher in financial services and healthcare, where digital transformation is prioritized. The shift toward mobile-first, cloud-native lending solutions reflects regional demand for efficiency, compliance readiness, and customer-centric credit processing.

How Are Regulations Shaping Lending Digitalization?

Europe accounted for 28% of the global LOS market share in 2024, led by Germany, the UK, and France, where financial institutions prioritize compliance-driven automation. The European Banking Authority (EBA) and PSD2 regulations have accelerated the adoption of explainable AI in LOS platforms, addressing transparency and security in digital lending. Cloud-native adoption is growing rapidly across European banks, with Germany reporting over 60% of financial institutions investing in AI-driven credit assessment tools. A notable regional player, Finastra, has been upgrading its LOS offerings to align with EU data privacy standards, strengthening customer trust. Consumer behavior in Europe reflects cautious adoption due to regulatory oversight, but growing demand for explainable LOS platforms is driving higher adoption among both retail and corporate lenders. Sustainability initiatives also play a role, with banks aligning LOS integration to ESG lending practices.

Why Is Mobile Lending Driving Market Acceleration?

Asia-Pacific represented 22% of global LOS adoption in 2024, ranking third in market size but first in growth momentum. China, India, and Japan dominate demand, together accounting for over 70% of the region’s digital lending transactions. Rising e-commerce penetration, mobile wallet usage, and digital identity systems such as India’s Aadhaar are fueling large-scale adoption. Infrastructure modernization, particularly in cloud deployment and API integration, has made LOS platforms more accessible to regional banks and fintech startups. A notable local player, Lentra, has scaled rapidly by offering AI-powered LOS solutions to Indian banks, handling millions of credit applications annually. Consumer behavior is mobile-centric, with more than 65% of loan applications in markets like Indonesia and India now initiated through smartphones. Growth is being accelerated by regional innovation hubs such as Singapore and Shenzhen, where fintech ecosystems are expanding rapidly.

How Are Financial Inclusion Programs Expanding Loan Access?

South America accounted for 8% of the global LOS market share in 2024, with Brazil and Argentina as primary contributors. Brazil alone represented nearly 60% of the region’s adoption, driven by strong demand in consumer lending and SME financing. Government initiatives supporting digital credit access and open banking frameworks have accelerated deployment. Infrastructure modernization in financial services is improving digital penetration, particularly in urban areas, while energy sector growth indirectly boosts demand for financing solutions. Local fintech Nubank has emerged as a leading innovator, offering cloud-based LOS solutions that streamline loan applications for millions of users. Regional consumer behavior reflects demand tied to media and language localization, with Spanish and Portuguese interfaces becoming essential. This consumer-centric customization is a key driver of adoption across the continent.

What Role Does Financial Modernization Play in Growth?

The Middle East & Africa accounted for 6% of the global LOS market share in 2024, with major demand centers in the UAE, Saudi Arabia, and South Africa. The financial sector’s rapid digital transformation, coupled with rising fintech adoption, is driving modernization. Government initiatives like the UAE’s digital banking framework and South Africa’s financial inclusion policies are supporting widespread adoption of LOS platforms. Technological modernization trends include cloud-native LOS adoption, AI-enhanced underwriting, and blockchain-based credit scoring models. A regional fintech leader, YAP, has partnered with banks in the Gulf to integrate LOS solutions, targeting underserved segments. Consumer behavior shows a preference for mobile-first solutions, particularly among younger populations, with mobile loan applications surpassing 10 million in 2024. Trade partnerships and cross-border fintech collaborations further strengthen the regional growth outlook.

United States – 28% market share

Strong dominance due to large-scale digital lending by banks and fintechs, coupled with advanced regulatory frameworks and high consumer adoption of online loans.

China – 16% market share

Leadership driven by mobile-first adoption, e-commerce financing, and rapid scaling of fintech ecosystems offering LOS solutions to banks and consumers.

The Loan Origination System (LOS) market is moderately consolidated, with the top five players holding a combined 46% share in 2024. The market features more than 120 active competitors globally, ranging from established banking technology providers to emerging fintech startups. North America and Europe are home to dominant players such as Fiserv, Ellie Mae (ICE Mortgage Technology), and Finastra, which continue to expand their portfolios through partnerships, AI integrations, and compliance-driven innovations. Strategic initiatives include M&A activity—Ellie Mae’s integration with ICE Mortgage being a prime example—and product launches in AI-powered underwriting and risk scoring. Meanwhile, in Asia-Pacific, firms such as Lentra and TCS are gaining traction by offering scalable cloud-native solutions to regional banks. Innovation trends influencing competition include low-code LOS platforms, embedded AI for fraud detection, and blockchain-enabled loan validation. The market remains competitive, with mid-sized vendors targeting niche segments like SME lending, while larger firms aim for enterprise-scale adoption.

Tavant

Wipro

Experian PLC

Pegasystems Inc.

Temenos AG

Intellect Design Arena Ltd.

TCS (Tata Consultancy Services)

Technology is at the core of transformation in the Loan Origination System (LOS) market, reshaping efficiency, scalability, and compliance across financial institutions. Cloud-native LOS platforms are increasingly replacing legacy on-premise solutions, offering scalability, real-time updates, and lower operational costs. In 2024, more than 58% of large banks globally reported shifting to cloud-based LOS for end-to-end credit processing. Artificial intelligence and machine learning are revolutionizing loan decisioning, with AI-enabled underwriting reducing manual intervention by up to 45% and improving approval turnaround times. Advanced analytics and predictive models are being used to assess creditworthiness beyond traditional credit scores, incorporating behavioral and transactional data. Blockchain adoption is gaining traction for secure, tamper-proof loan contracts, ensuring transparency across lenders and borrowers. API-driven integration is another key trend, enabling LOS platforms to connect seamlessly with digital wallets, CRM, and KYC solutions, thereby improving customer experience. Mobile-first LOS applications are rising rapidly in emerging markets, where over 65% of new loan applications are initiated via smartphones. Together, these technologies are enabling financial institutions to process higher loan volumes at reduced cost while maintaining regulatory compliance and customer-centric innovation.

In February 2024, Finastra launched its new AI-enabled LOS platform designed to automate SME credit underwriting, reducing processing time by 35% and enhancing accuracy in credit scoring. Source: www.finastra.com

In November 2023, ICE Mortgage Technology announced the integration of advanced compliance modules into its Ellie Mae LOS platform, addressing new US mortgage regulations and improving transparency for borrowers. Source: www.icemortgagetechnology.com

In August 2024, India-based Lentra secured a multi-million-dollar partnership with leading banks to scale its AI-driven LOS platform across Asia-Pacific, enabling the processing of over 10 million loan applications annually. Source: www.lentra.ai

In May 2023, Experian introduced a blockchain-powered LOS solution that enhances credit scoring accuracy by integrating alternative data sources, improving lending opportunities for underserved populations. Source: www.experianplc.com

The Loan Origination System (LOS) Market Report provides a comprehensive analysis of the industry, covering multiple dimensions including type, application, end-user, and geography. It outlines the size and structure of the market across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional demand patterns, regulatory frameworks, and consumer adoption trends. The report examines applications across consumer lending, mortgage lending, SME financing, and corporate credit solutions, with detailed segmentation of institutional versus direct-to-consumer adoption. Technology insights explore cloud-native solutions, AI-enabled underwriting, blockchain integration, and mobile-first LOS applications. End-user analysis spans banks, credit unions, fintech lenders, and non-banking financial institutions (NBFCs). The scope also considers niche growth areas such as peer-to-peer lending and embedded finance, reflecting the market’s evolving ecosystem. Additionally, the report highlights competition dynamics, profiling global leaders and regional innovators shaping digital lending. Collectively, this report equips decision-makers with an in-depth understanding of the LOS market’s opportunities, challenges, and technological transformation drivers.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 6,015.5 Million |

|

Market Revenue in 2032 |

USD 15,434.5 Million |

|

CAGR (2025 - 2032) |

12.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Finastra, Ellie Mae (ICE Mortgage Technology), Fiserv, Tavant, Wipro, Experian PLC, Pegasystems Inc., Temenos AG, Intellect Design Arena Ltd., TCS (Tata Consultancy Services) |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |