Reports

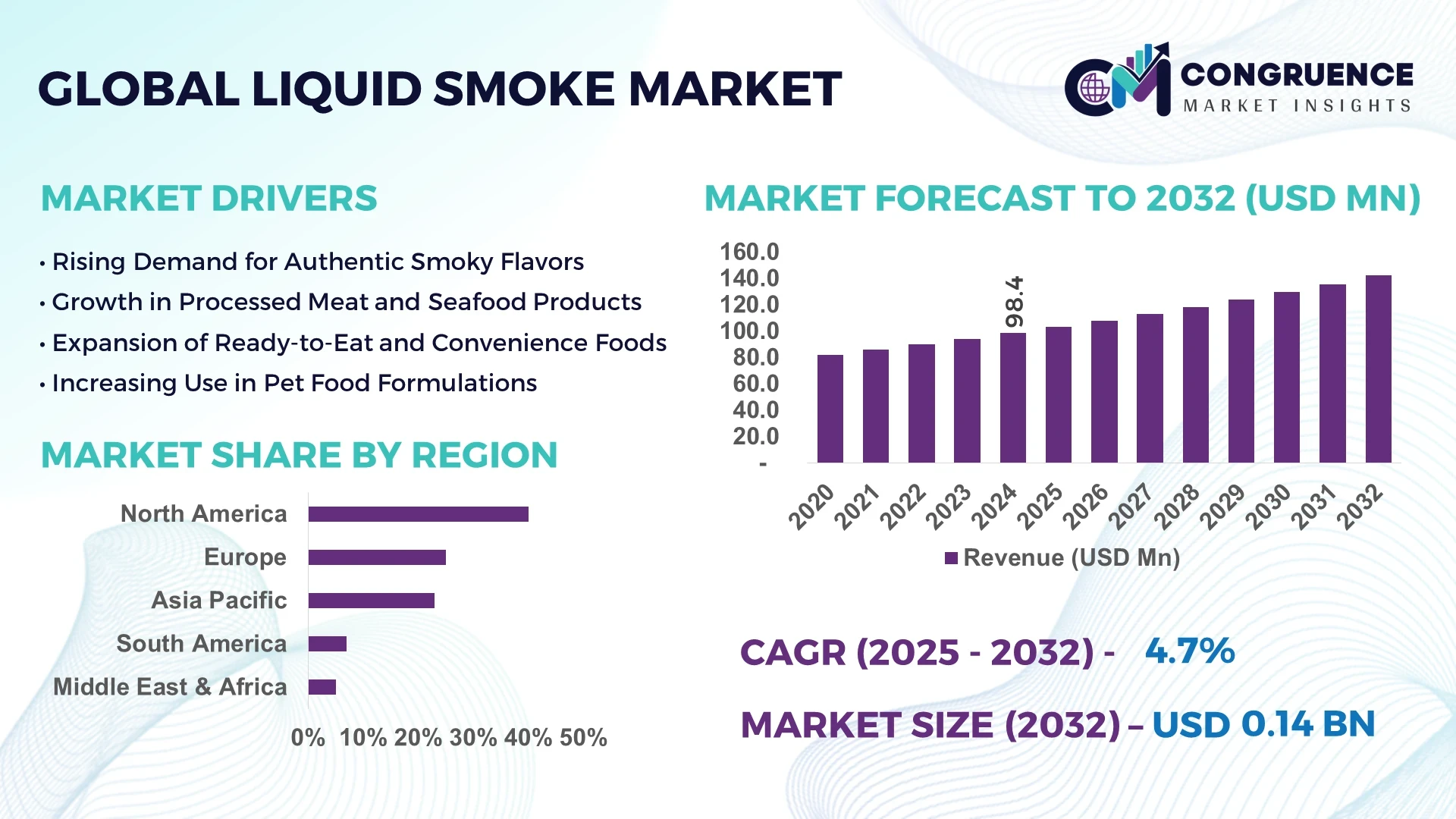

The Global Liquid Smoke Market was valued at USD 98.41 Million in 2024 and is anticipated to reach a value of USD 142.11 Million by 2032, expanding at a CAGR of 4.7% between 2025 and 2032.

The United States currently dominates the global liquid smoke market. This country plays a critical role in influencing innovation, product formulation, and industrial scale production of liquid smoke, particularly in food processing and barbecue flavoring sectors.

The global liquid smoke market is witnessing steady growth due to increasing demand for natural food additives and clean-label products. In 2024, meat processing applications accounted for over 30% of the market share, primarily due to the growing use of liquid smoke as a flavor enhancer and antimicrobial preservative. Barbecue sauces, ready-to-eat meals, and processed dairy products are increasingly incorporating liquid smoke to mimic the taste of traditional smoking methods without the associated time and cost. The Asia-Pacific region is poised for rapid growth due to rising meat consumption and growing adoption of Western-style cooking in countries like India, China, and Thailand. Furthermore, innovations in encapsulated liquid smoke powders and water-soluble variants are expanding its use across pet food, seasonings, marinades, and snack flavorings. As consumer preference shifts toward smoked flavor profiles, demand is also growing in the vegan and plant-based meat sectors.

Artificial Intelligence (AI) is transforming the liquid smoke market by introducing advanced solutions that improve product quality, reduce manufacturing errors, and streamline supply chains. AI-based automation is increasingly being adopted across extraction, filtration, and bottling processes to ensure consistency and reduce waste. AI-powered sensors and real-time monitoring systems now allow liquid smoke manufacturers to precisely control temperature, wood type, and moisture content—ensuring a uniform, high-quality product output.

AI is also playing a pivotal role in predictive analytics and flavor formulation. By analyzing consumer behavior data, regional taste preferences, and market trends, manufacturers can develop customized liquid smoke variants tailored to specific cuisines and consumer segments. The use of machine learning algorithms in R&D has significantly reduced product development cycles by predicting which wood smokes, temperatures, or concentrations yield the most marketable flavor profiles. Additionally, AI helps identify contaminants or inconsistencies before products leave the factory, enhancing food safety compliance.

Moreover, AI-driven supply chain systems optimize procurement, inventory, and logistics—ensuring that manufacturers can respond quickly to changing demand patterns. As demand for smoky flavors continues to grow in processed meats, sauces, and vegan alternatives, AI enables scalability and cost-efficiency across operations. These digital transformations are helping liquid smoke companies stay competitive while maintaining quality, sustainability, and innovation.

"In January 2024, a leading liquid smoke manufacturer implemented an AI-powered quality control system that utilizes machine learning algorithms to detect and correct deviations in flavor profiles during production. This system has resulted in a 15% increase in product consistency and a 10% reduction in production costs, demonstrating the tangible benefits of AI integration in the liquid smoke industry."

The liquid smoke market is evolving rapidly due to changing consumer preferences, technological innovations, and increasing global demand for smoked flavors in food. The market dynamics are being shaped by the growing need for natural flavoring agents, especially in processed meats, plant-based alternatives, and ready-to-eat meals. There is a significant push from food processors toward clean-label ingredients and smoke-flavor substitutes that are free from carcinogenic compounds found in traditional smoking methods. In regions such as North America and Europe, regulations are encouraging safer alternatives like liquid smoke. Additionally, global fast-food chains are incorporating smoked sauces and smoky flavors into their menus, increasing market penetration. As manufacturers invest in product innovations like spray-dried and oil-soluble variants, the liquid smoke market continues to diversify its end-user base, which includes snack food producers, meat processors, sauce manufacturers, and even beverage formulators.

The demand for clean-label, smoke-flavored food products is a key driver in the liquid smoke market. Consumers are increasingly aware of the health risks associated with traditional smoking, which has led to higher adoption of liquid smoke for its safer application. Over 65% of processed meat manufacturers now use liquid smoke due to its ability to deliver flavor while eliminating hazardous polycyclic aromatic hydrocarbons (PAHs). In 2024, snack manufacturers began using liquid smoke extract in potato chips, popcorn, and nuts to enhance appeal without artificial additives. Plant-based meat alternatives are also incorporating liquid smoke flavoring to mimic real grilled taste. With regulatory agencies pushing for clean-label transparency, liquid smoke is emerging as a preferred ingredient in ready meals, frozen foods, and condiments. This driver is strengthening product demand across both premium and mass-market segments globally.

Despite its advantages, the liquid smoke market faces notable restraints due to complex regulatory requirements and regional labeling laws. Regulatory bodies in regions like the European Union often classify liquid smoke as a “smoke flavoring primary product”, requiring detailed safety assessments. The application process can delay time-to-market, particularly for new formulations. Additionally, there is rising consumer concern regarding natural versus artificial smoke labeling, which puts pressure on manufacturers to provide transparent ingredient disclosures. In many countries, food products using liquid smoke must meet strict residue limits, testing protocols, and documentation, increasing compliance costs. Furthermore, small-scale manufacturers may struggle with adhering to varying import/export guidelines, especially when expanding into Asia-Pacific and Latin America. These regulatory hurdles continue to hinder innovation and slow down broader adoption across food segments.

The growing popularity of plant-based diets is opening up new opportunities for the liquid smoke market, especially in the vegan meat and dairy alternatives segment. As consumers seek healthier, environmentally friendly food options, the demand for authentic smoky flavor in non-meat products is surging. In 2024, over 28% of plant-based burger brands reported integrating liquid smoke to replicate the grilled flavor traditionally achieved through open-flame cooking. Similarly, vegan cheese and dairy-free spreads are using water-soluble liquid smoke to mimic smoked dairy characteristics. This opportunity is driving innovation in flavor encapsulation technologies, enabling broader use in dry mixes, sauces, frozen entrées, and seasonings. Emerging markets like India, Brazil, and South Korea are witnessing increased consumer exposure to these flavors, enhancing market potential. Manufacturers who offer customized, allergen-free smoke variants can leverage this expanding niche.

A significant challenge in the liquid smoke market is limited consumer awareness and widespread misconceptions regarding its composition and safety. Many consumers mistakenly believe liquid smoke is a synthetic or chemically produced additive, deterring purchase and use in home cooking and gourmet food products. Despite being derived from real wood combustion, lack of education about the production process continues to stigmatize its usage. Furthermore, some foodservice providers are hesitant to use liquid smoke due to concerns over flavor authenticity, fearing that customers might notice a difference from traditionally smoked items. In addition, branding limitations and inconsistent labeling across regions create confusion in retail aisles. This challenge is amplified in emerging economies where culinary exposure to smoky flavors is still nascent. Unless industry stakeholders ramp up awareness campaigns and transparency, the growth potential of the market may remain underutilized, especially in direct-to-consumer channels.

• Increased Demand from Plant-Based Food Producers: The rise of plant-based meat and dairy alternatives is creating a significant demand for liquid smoke in food manufacturing. In 2024, over 30% of vegan meat companies globally incorporated liquid smoke into their recipes to provide authentic grilled and roasted flavors. This trend is particularly strong in North America, where brands are offering plant-based sausages, burgers, and jerky with added smoke flavor to enhance sensory appeal. The liquid smoke market is increasingly targeting manufacturers of tofu, tempeh, and seitan-based products that aim to mimic the taste of flame-grilled meat without actual smoking processes.

• Adoption of Liquid Smoke in Snack Seasonings and Sauces: The use of liquid smoke in snack flavorings and condiments is on the rise across the global food industry. In 2024, more than 18% of barbecue-flavored chips and popcorn varieties launched in the market featured liquid smoke as a primary flavoring ingredient. Similarly, liquid smoke is becoming a key component in hot sauces, marinades, and salad dressings, offering depth of flavor without traditional wood-smoking. The versatility of liquid smoke across wet and dry applications is making it a favored additive in packaged goods, particularly in the U.S., U.K., and Japan.

• Growth in Clean-Label and Natural Additive Preference: Consumers are showing a growing preference for natural food additives and clean-label ingredients, boosting the demand for liquid smoke products that are derived from hardwoods without synthetic chemicals. In 2024, nearly 60% of food product developers expressed a preference for liquid smoke over artificial smoke flavorings due to its natural profile. Liquid smoke variants labeled as "all-natural," "preservative-free," or "wood-derived" are witnessing faster adoption across frozen meals and processed meat brands. This trend is also encouraging manufacturers to offer customized and organic-certified liquid smoke solutions.

• Wider Penetration in Global Quick-Service Restaurant Chains: Quick-service restaurants (QSRs) are increasingly using liquid smoke in their sauces, grilled items, and seasoning bases. In 2024, several major international fast-food chains introduced smoky chicken wings, flame-grilled burgers, and barbecue wraps using liquid smoke-enhanced sauces. The ability to deliver smoky flavor without extended cooking times has enabled faster menu preparation and consistency across outlets. Asia-Pacific, in particular, is seeing high adoption among franchise brands expanding in urban centers where traditional smoking is impractical due to space or regulation constraints. This QSR-driven demand is contributing to stable growth in the global liquid smoke market.

The global Liquid Smoke Market is segmented based on type, application, and end-user insights, with each playing a crucial role in defining growth trajectories and innovation patterns. Types of liquid smoke such as Hickory, Mesquite, Applewood, and others are utilized differently across various food processing applications. Applications of liquid smoke span across Meat & Seafood, Sauces, Dairy, Snacks, and Pet Food, with demand driven by flavor, shelf-life extension, and smoke-free processing methods. End-users include Food Processing Companies, Quick Service Restaurants (QSRs), Catering Services, Household Consumers, and Institutional Buyers. Hickory liquid smoke dominates the market due to its robust smoky aroma, while QSRs are emerging as the fastest-growing end-users. Globally, Meat & Seafood continues to be the top application area, accounting for a substantial share of liquid smoke consumption. However, the rise of plant-based and snack product innovations is shifting the dynamics of fastest growth within the market.

The liquid smoke market by type is segmented into Hickory, Mesquite, Applewood, Oakwood, and Others. Among these, Hickory liquid smoke held the largest market share in 2024, accounting for over 38% of the global volume. Its rich, deep smoky profile is widely preferred in processed meat and BBQ sauce manufacturing. Mesquite follows closely with a share of 24%, especially favored in Latin cuisines and grilling products. Applewood is gaining popularity in seafood and vegan meat due to its lighter, sweeter aroma and flavor profile. Oakwood, often used in dairy and cheese flavorings, contributes modestly to the market.

The fastest-growing type is Applewood liquid smoke, projected to expand significantly due to its high adoption in plant-based and gourmet food applications. In 2024, Applewood variants experienced over 17% year-over-year growth, driven by consumer demand for subtle smoky flavors in non-meat categories. The increasing production of natural liquid smoke concentrates with customizable intensity is also fueling growth across all segments, with premium hardwood variants attracting new food innovation projects.

Liquid smoke finds application in Meat & Seafood, Sauces & Condiments, Dairy Products, Snack Foods, and Pet Food. In 2024, the Meat & Seafood segment dominated the market with more than 45% share, as liquid smoke is extensively used in products like sausages, hot dogs, deli meats, and smoked fish. It enhances shelf-life and reduces microbial load while providing traditional smoky taste without physical smoking chambers. The Sauces & Condiments segment accounted for nearly 22%, incorporating liquid smoke in BBQ sauces, marinades, dips, and glazes.

The fastest-growing segment is Snack Foods, especially in flavored chips, popcorn, and protein snacks, with annual demand increasing by 19%. Manufacturers are using liquid smoke in dry seasoning mixes and as a flavor enhancer in baked and extruded snack categories. The Dairy segment, including smoked cheese and butter, continues to expand steadily. With a growing focus on flavor versatility and health-conscious cooking, more food processors are integrating liquid smoke across multi-category applications to achieve clean-label smokiness.

Based on end-user segmentation, the Liquid Smoke Market serves Food Processing Companies, Quick Service Restaurants (QSRs), Catering Services, Household Consumers, and Institutional Buyers. Food Processing Companies are the largest end-users, contributing to over 52% of total market demand in 2024. These firms use liquid smoke for mass production of smoked meats, flavored sauces, dairy, and snacks. The segment prefers concentrated and water-soluble liquid smoke formats for ease of mixing and quality consistency.

The fastest-growing end-user segment is Quick Service Restaurants (QSRs), growing at over 21% annually due to their need for efficient, scalable flavor solutions without relying on physical smoking. Liquid smoke allows QSRs to maintain taste uniformity across chains and reduce prep times. Household Consumers also represent a growing user base, especially in urban settings where traditional wood-smoking is impractical. With the rise of gourmet home cooking trends and e-commerce, many liquid smoke brands are now offering consumer-size bottles directly online and in retail outlets.

North America accounted for the largest market share at 40% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.6% between 2025 and 2032.

North America’s dominance in the liquid smoke market is driven by the growing demand in meat processing, BBQ sauces, and the presence of major food processing companies. The region's widespread adoption of convenience foods and its strong retail market infrastructure further support the demand for liquid smoke. However, the Asia-Pacific region is emerging as the fastest-growing market, largely due to the rise in demand for processed food, along with growing awareness of the benefits of liquid smoke as a natural flavoring agent.

Dominating the Liquid Smoke Scene with Growing Demand

The North American Liquid Smoke Market was the largest in 2024, accounting for 40% of the global market share. The demand is primarily driven by the meat processing industry, with a strong preference for hickory and mesquite variants of liquid smoke for meat and seafood products. The region also sees significant growth in the sauces and condiments market, where liquid smoke is increasingly used to enhance flavors without the need for traditional smoking methods. Notably, the adoption of liquid smoke in ready-to-eat meals and snacks is on the rise, supported by both consumer demand for convenience and innovation by food manufacturers. Regulatory approvals and quality standards in North America further fuel market growth.

Embracing Natural Flavor Innovations in Liquid Smoke

In Europe, the liquid smoke market continues to expand, with a strong preference for milder flavors like applewood and oakwood in gourmet foods, sauces, and smoked cheeses. The region holds 25% of the global market share. European consumers are becoming more inclined toward natural, clean-label ingredients, boosting the demand for liquid smoke as a flavor enhancer in plant-based foods and dairy products. Moreover, European regulations for food additives and flavorings allow for the increased use of liquid smoke in a variety of culinary applications. The market is witnessing significant innovation, with companies in Europe leading the way in creating new blends and flavors suited for the evolving consumer palate.

Expanding Horizons in Liquid Smoke Consumption

Asia-Pacific is the fastest-growing region in the liquid smoke market, with an increasing preference for natural flavoring agents. This region accounted for 18% of the market share in 2024. Growth is primarily attributed to rising consumer interest in processed food, including snacks, sauces, and ready-to-eat meals, which utilize liquid smoke for added flavor. The rising popularity of Western culinary traditions in countries like China, India, and Japan is further propelling the adoption of liquid smoke, especially in meat and seafood products. Additionally, advancements in food preservation and the increasing need for clean-label ingredients drive the liquid smoke market in this region.

Tapping into the Flavor Revolution with Liquid Smoke

The South American Liquid Smoke Market holds 7% of the global market share, with countries like Brazil leading the demand for liquid smoke, particularly in the meat and BBQ segments. With a significant focus on traditional smoking techniques, liquid smoke has become an essential ingredient for preserving flavors and extending the shelf-life of processed meats. The growing number of food processing plants and the rising consumption of fast-food products are expected to contribute to the market’s expansion. Furthermore, the awareness of natural flavoring agents in sauces and marinades is fostering an increase in liquid smoke usage across the region.

Emerging Markets and the Growing Appeal of Liquid Smoke

The Middle East & Africa region represents a smaller share of the global liquid smoke market, contributing approximately 5% in 2024. However, it is witnessing gradual growth due to the region’s growing food processing sector and the adoption of liquid smoke in smoked meat products. The demand for liquid smoke is rising due to its ability to provide rich smoky flavors without traditional smoking, which is essential in regions with limited access to wood-based smoking methods. The region’s evolving food preferences and growing export demand for processed food products are expected to contribute to this market’s growth in the coming years.

United States: The US holds the largest market share in the North American liquid smoke market due to high demand in the meat industry and BBQ sauces, with over 40% of the market share.

Germany: Germany ranks as the second-largest market in Europe with a growing demand for gourmet smoked flavors in dairy and plant-based products, capturing 17% of the market share.

The Liquid Smoke Market is highly competitive, with numerous players focusing on innovation, product diversification, and global expansion. Key market participants are increasingly investing in research and development to enhance the quality and variety of liquid smoke products to meet the growing demand for natural flavoring agents. These companies are also exploring various distribution channels, including online retail, to cater to consumer preferences. The industry is characterized by the presence of both established players and new entrants, which makes it highly fragmented. Several key players are involved in producing different types of liquid smoke, such as hickory, mesquite, applewood, and oakwood, which are highly favored by consumers in food processing and culinary applications. Additionally, strategic partnerships, mergers, and acquisitions are increasingly common as companies aim to strengthen their market position, expand their product offerings, and enter new geographical regions. The competitive landscape is dynamic, with regional players also vying for market share.

Red Arrow Products Company

Colgin Liquid Smoke

Lorin Industries

The Original Coney Island Liquid Smoke

Georgia Pacific LLC

Scott Roberts Hot Sauce

Natural Smoke Inc.

Oregon Smoke Tree

Kerry Group

Fuchs Group

The Liquid Smoke Market is benefiting from advancements in production technology that enable the creation of more diverse and high-quality flavor profiles. The use of cutting-edge methods such as flash distillation and steam distillation is increasingly popular for producing concentrated and purified liquid smoke products. This technology ensures that the liquid smoke retains the natural aroma and flavor profiles of smoked wood, providing a more authentic taste in food products without the use of traditional smoking methods. The process involves capturing the smoke from burning wood and condensing it into a liquid form, making it easy to incorporate into a wide range of food items, from meats to sauces and even vegetarian alternatives. Additionally, emerging technologies in packaging are enhancing the shelf life of liquid smoke, ensuring that products maintain their flavor and freshness over extended periods. These innovations are fueling market growth as companies strive to meet consumer demand for natural, clean-label flavoring agents. The ongoing focus on product sustainability and eco-friendly manufacturing processes is also playing a critical role in driving technological advancements in the liquid smoke sector.

In March 2023, McCormick & Company, Inc. acquired Smokehouse Flavors, Inc., a leading manufacturer of liquid smoke products in the United States. This acquisition is expected to strengthen McCormick's position in the liquid smoke market and expand its product offerings.

In January 2023, Liquid Smoke Flavors, Inc. announced the launch of its new line of liquid smoke flavors, including hickory, mesquite, applewood, and maple. The new flavors are designed to appeal to a wider range of consumers and be used in various dishes.

In August 2023, SkyQuest Technology Consulting Pvt. Ltd. projected that the liquid smoke market would attain a USD 122.05 million value by 2030, driven by the rising preference for smoky flavors in food and beverages. The report highlights that liquid smoke provides an efficient and consistent means to achieve the desired taste profile, contributing to its widespread adoption across various cuisines and products.

In February 2024, Kerry Group announced a substantial investment aimed at increasing production capacity to meet the rising global demand for liquid smoke products. This move underscores Kerry Group's commitment to expanding its presence in the liquid smoke market and catering to the growing consumer demand for natural flavoring agents.

The Liquid Smoke Market Report provides a thorough analysis of the global liquid smoke market, offering valuable insights into key market trends, growth drivers, and challenges. The report covers the market's diverse segments, such as product types, applications, distribution channels, and regional dynamics, to provide a comprehensive overview of the liquid smoke industry.

The report outlines the market's growth potential, particularly in the food and beverage sector, where liquid smoke is gaining popularity due to its natural and smoky flavor profile. This flavoring agent is increasingly used in processed meats, sauces, marinades, and other products, making it an essential ingredient for manufacturers seeking to meet consumer preferences for authentic tastes.

Geographically, the liquid smoke market shows significant growth across regions such as North America, Europe, and Asia-Pacific. North America remains a dominant market, driven by high demand in the food processing industry, while Europe is witnessing steady growth, particularly in organic and natural liquid smoke products.

The report also highlights technological innovations, such as advancements in liquid smoke production, which improve product quality and sustainability. Furthermore, competitive strategies, including mergers, acquisitions, and new product launches, are analyzed to understand the market dynamics and competitive landscape.

With a focus on providing actionable insights, the Liquid Smoke Market Report serves as a crucial tool for industry stakeholders to navigate the evolving landscape of the global liquid smoke market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 98.41 Million |

|

Market Revenue in 2032 |

USD 142.11 Million |

|

CAGR (2025 - 2032) |

4.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Red Arrow Products Company, Colgin Liquid Smoke, Lorin Industries, The Original Coney Island Liquid Smoke, Georgia Pacific LLC, Scott Roberts Hot Sauce, Natural Smoke Inc., Oregon Smoke Tree, Kerry Group, Fuchs Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |