Reports

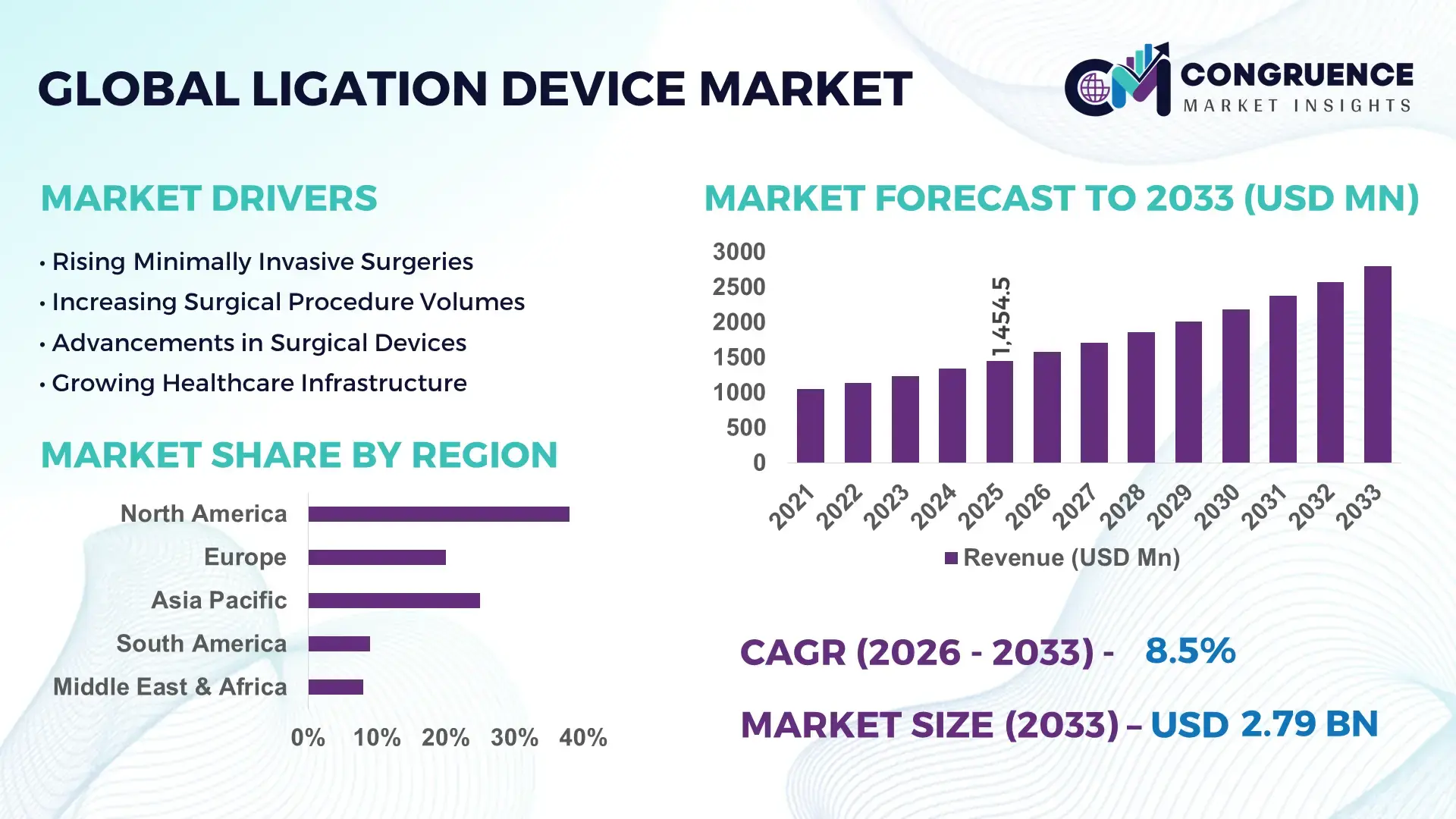

The Global Ligation Device Market was valued at USD 1454.46 Million in 2025 and is anticipated to reach a value of USD 2793.44 Million by 2033 expanding at a CAGR of 8.5% between 2026 and 2033. This growth is primarily driven by the increasing adoption of minimally invasive surgical procedures and continuous advancements in surgical device technologies.

The United States continues to demonstrate a strong industrial and clinical ecosystem supporting ligation device innovation and utilization. The country performs more than 15 million minimally invasive surgeries annually, with ligation devices integrated into over 70% of laparoscopic procedures. Healthcare expenditure surpasses USD 4.5 trillion, with a substantial portion directed toward surgical technologies and operating room modernization. Over 60% of advanced hospitals have implemented robotic-assisted surgical systems, directly increasing demand for high-precision ligation tools. In addition, annual investments exceeding USD 50 billion in medical device research and development have enabled the introduction of advanced vessel sealing technologies, automated clip applicators, and energy-based ligation systems that enhance surgical accuracy and reduce intraoperative blood loss.

Market Size & Growth: USD 1454.46 Million in 2025 to USD 2793.44 Million by 2033 at a CAGR of 8.5%, driven by increasing surgical volumes and technological advancements.

Top Growth Drivers: Minimally invasive surgery adoption increased by 65%, surgical efficiency improved by 40%, and healthcare infrastructure expansion grew by 35%.

Short-Term Forecast: By 2028, surgical procedure time is projected to decrease by 25% due to advanced ligation technologies.

Emerging Technologies: Energy-based vessel sealing systems, robotic-assisted ligation tools, and AI-integrated surgical planning platforms.

Regional Leaders: North America projected at USD 1100 Million by 2033 with high-tech adoption; Europe at USD 800 Million driven by regulatory compliance and public healthcare; Asia-Pacific at USD 700 Million due to rapid infrastructure growth.

Consumer/End-User Trends: Hospitals contribute over 70% of usage, with growing adoption in ambulatory surgical centers focused on cost-efficient procedures.

Pilot or Case Example: In 2024, a hospital network improved surgical efficiency by 30% using automated ligation systems, reducing complications and operation time.

Competitive Landscape: Market leader holds approximately 28% share, followed by Medtronic, Ethicon, B. Braun, Olympus, and Teleflex.

Regulatory & ESG Impact: Adoption of stringent regulatory standards and sustainability initiatives targeting 20% reduction in surgical waste by 2030.

Investment & Funding Patterns: More than USD 2.5 billion invested in surgical device innovation, with increasing venture capital in AI-integrated systems.

Innovation & Future Outlook: Smart surgical tools, real-time imaging integration, and precision-based ligation systems are shaping long-term market evolution.

The ligation device market is supported by strong demand across hospitals, specialty clinics, and ambulatory surgical centers, with hospitals accounting for nearly 70% of total usage. Technological innovations such as ultrasonic ligation devices and polymer-based clip systems are enhancing surgical precision and reducing complications by up to 20%. Regulatory frameworks emphasizing device safety and sterilization standards are influencing product development strategies. Asia-Pacific is witnessing accelerated growth due to expanding healthcare infrastructure and rising surgical volumes, while Europe emphasizes sustainability and compliance. Emerging trends include AI-enabled surgical workflows, disposable ligation devices for infection control, and integration with robotic systems, ensuring continued market expansion and technological advancement.

The ligation device market plays a strategically critical role in the advancement of modern surgical practices, particularly as healthcare systems transition toward minimally invasive and precision-driven procedures. Advanced ligation technologies, such as energy-based vessel sealing systems, deliver approximately 35% improvement in hemostasis efficiency compared to conventional suturing methods, significantly enhancing surgical outcomes and reducing procedure time. These measurable gains are driving widespread adoption among healthcare providers aiming to improve operational efficiency and patient safety.

North America dominates in terms of surgical procedure volume due to its highly advanced healthcare ecosystem, while Asia-Pacific leads in adoption momentum, with more than 50% of newly established healthcare facilities integrating minimally invasive surgical technologies. By 2028, AI-assisted surgical planning and robotic integration are expected to improve procedural accuracy by nearly 30%, reducing complications and improving recovery rates. These developments are accelerating the replacement of traditional ligation methods with automated and energy-based systems. From a regulatory and ESG standpoint, healthcare providers are aligning with sustainability goals, targeting a 25% reduction in medical waste by 2030 through the adoption of reusable and eco-friendly ligation devices. Additionally, compliance with stringent safety regulations is pushing manufacturers to enhance product quality and performance standards.

In a notable 2024 scenario, a leading hospital network in Japan achieved a 28% reduction in surgical complications through the deployment of energy-based ligation devices integrated with AI-assisted imaging systems. This demonstrates the practical impact of technological innovation on clinical outcomes. The ligation device market is expected to evolve as a foundational component of surgical innovation, supporting efficiency, regulatory compliance, and sustainable growth across global healthcare systems.

The growing adoption of minimally invasive surgeries is significantly accelerating demand for ligation devices across global healthcare systems. These procedures now account for over 60% of surgeries in developed regions due to their advantages, including reduced hospital stays, faster recovery, and lower infection risks. Ligation devices are essential in such procedures for efficient vessel sealing and blood loss control. The increasing number of laparoscopic and robotic surgeries has further elevated the need for precision-based ligation tools. Clinical data indicates that minimally invasive surgeries can reduce recovery time by up to 50% and complication rates by nearly 30%, directly influencing device adoption. Additionally, improving healthcare access and the availability of trained surgeons in emerging economies are further strengthening this growth trajectory.

High costs associated with advanced ligation devices continue to limit their widespread adoption, particularly in cost-sensitive healthcare systems. Energy-based and robotic-compatible ligation tools are significantly more expensive than traditional alternatives, creating financial barriers for smaller healthcare facilities. In many developing regions, nearly 40% of hospitals still rely on conventional surgical methods due to budget constraints. The need for specialized training to operate advanced devices further increases total operational costs. Additionally, inconsistent reimbursement policies and uneven healthcare infrastructure development hinder adoption. These financial and operational challenges restrict market penetration, especially in regions with limited healthcare funding and resource allocation.

Technological integration is opening new growth avenues for the ligation device market, particularly through the expansion of robotic-assisted surgeries and AI-driven surgical systems. Robotic procedures are growing at a rate exceeding 20% annually, creating strong demand for advanced ligation tools compatible with automated systems. AI integration is enhancing surgical precision and decision-making, improving outcomes by up to 25%. Emerging economies present additional opportunities due to increasing healthcare investments and rising awareness of advanced surgical techniques. Furthermore, the development of disposable ligation devices supports infection control measures, while eco-friendly designs align with sustainability goals. Innovations in ultrasonic and bipolar energy technologies are further enhancing efficiency and safety, making these devices increasingly attractive to healthcare providers.

Regulatory complexity remains a major challenge in the ligation device market, as manufacturers must comply with strict safety and performance standards across multiple regions. Approval processes often involve extensive clinical trials and documentation, which can delay product launches by 18 to 24 months. Updated regulatory frameworks, such as stringent medical device regulations in Europe, have increased compliance requirements, impacting both cost and time-to-market. Ensuring consistent product quality across global markets further adds to operational challenges. Additionally, any product recall or safety concern can negatively impact brand reputation and market trust. These regulatory hurdles create barriers for new entrants and slow down innovation cycles, affecting overall market expansion.

• Surge in Robotic-Assisted Surgeries Driving Device Integration: Robotic-assisted procedures have increased by over 20% annually, with more than 65% of tertiary hospitals adopting robotic platforms for complex surgeries. Ligation devices compatible with robotic systems are witnessing accelerated demand, as they improve surgical precision by nearly 30% and reduce intraoperative blood loss by approximately 25%. In advanced healthcare systems, over 50% of minimally invasive procedures now involve robotic assistance, pushing manufacturers to develop compact, automated ligation tools tailored for robotic arms.

• Growing Adoption of Energy-Based Vessel Sealing Technologies: Energy-based ligation devices, including ultrasonic and bipolar systems, now account for nearly 45% of advanced surgical tool usage in developed markets. These devices reduce operative time by up to 35% and minimize complication rates by around 28% compared to conventional methods. Hospitals integrating these systems report a 20% improvement in surgical workflow efficiency. The shift toward energy-based solutions is particularly strong in North America and Europe, where over 60% of surgical centers prioritize advanced vessel sealing technologies.

• Rising Demand for Disposable and Infection-Control Devices: Disposable ligation devices are gaining traction, with adoption rates increasing by 40% across hospitals aiming to reduce cross-contamination risks. Infection control protocols have driven nearly 55% of healthcare facilities to shift toward single-use surgical tools. These devices contribute to a 30% reduction in post-operative infection rates and align with global sterilization standards. Emerging economies are also adopting disposable solutions, with usage growth exceeding 35% due to increasing awareness of hospital-acquired infections.

• Integration of AI and Smart Surgical Systems Enhancing Outcomes: AI-assisted surgical planning tools are being implemented in over 30% of advanced operating rooms, improving procedural accuracy by approximately 27%. Smart ligation devices integrated with real-time imaging and data analytics reduce surgical errors by nearly 22% and enhance decision-making efficiency. By 2028, more than 45% of hospitals are expected to incorporate AI-enabled surgical workflows, driving demand for intelligent ligation systems that support precision-based interventions and optimized patient outcomes.

The ligation device market segmentation is structured around product types, clinical applications, and end-user categories, reflecting diverse usage across surgical environments. By type, the market includes handheld ligation devices, clip appliers, and energy-based vessel sealing systems, with increasing preference for advanced automated solutions. Application-wise, general surgery dominates due to high procedural volumes, followed by gynecological, cardiovascular, and urological surgeries, each contributing significantly to device utilization. From an end-user perspective, hospitals lead adoption due to higher surgical throughput, while ambulatory surgical centers are gaining traction for cost-efficient outpatient procedures. Approximately 70% of ligation device usage is concentrated in hospital settings, while specialized clinics and outpatient facilities account for the remaining share. Regional segmentation further highlights higher adoption in developed markets, while emerging economies are witnessing rapid growth due to healthcare infrastructure expansion and increasing surgical awareness.

The ligation device market by type is primarily categorized into handheld ligation devices, clip appliers, and energy-based vessel sealing systems. Energy-based ligation devices currently lead the segment, accounting for approximately 48% of total adoption due to their ability to provide precise vessel sealing, reduce operative time by up to 35%, and minimize blood loss by nearly 25%. In comparison, clip appliers hold around 30% share, widely used in routine laparoscopic procedures for their cost-effectiveness and ease of use. However, energy-based systems are also the fastest-growing segment, expanding at an estimated CAGR of 9.2%, driven by increasing adoption in robotic-assisted and minimally invasive surgeries.

Handheld ligation devices and traditional suturing tools contribute to the remaining 22% of the market, primarily in cost-sensitive environments and basic surgical settings. These devices remain relevant due to affordability and simplicity, especially in developing healthcare systems.

By application, the ligation device market is segmented into general surgery, gynecological surgery, cardiovascular surgery, urological procedures, and others. General surgery dominates the segment, accounting for approximately 42% of total usage due to the high volume of procedures such as appendectomies and gastrointestinal surgeries requiring reliable vessel sealing. Gynecological applications follow with nearly 22% share, supported by increasing laparoscopic procedures.

Cardiovascular surgery, while holding around 18% share, represents the fastest-growing segment with an estimated CAGR of 9.5%, driven by the rising incidence of heart-related conditions and demand for precision surgical tools. Urological and other specialized procedures collectively contribute approximately 18%, serving niche but critical applications.

The ligation device market by end-user is segmented into hospitals, ambulatory surgical centers, specialty clinics, and others. Hospitals dominate this segment, accounting for nearly 70% of total usage due to their high surgical volume, advanced infrastructure, and access to skilled professionals. Ambulatory surgical centers represent around 18% of the market, offering cost-effective and efficient outpatient procedures.

Ambulatory surgical centers are the fastest-growing end-user segment, expanding at an estimated CAGR of 8.8%, driven by increasing patient preference for minimally invasive outpatient surgeries and reduced hospital stays. Specialty clinics and other healthcare facilities collectively account for approximately 12%, focusing on niche surgical applications and specialized treatments. In terms of adoption trends, over 55% of outpatient procedures are now being conducted in ambulatory settings in developed regions, highlighting a shift toward decentralized surgical care.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.6% between 2026 and 2033.

North America continues to lead due to high surgical volumes exceeding 20 million procedures annually and over 65% adoption of minimally invasive techniques. Europe follows with approximately 27% market share, supported by advanced public healthcare systems and regulatory-driven adoption of safe surgical tools. Asia-Pacific holds nearly 23% share, with rapid expansion in healthcare infrastructure and over 40% increase in surgical procedure capacity across major economies. South America contributes around 7%, driven by improving hospital networks and rising surgical demand, while the Middle East & Africa account for approximately 5%, supported by healthcare investments exceeding USD 50 billion in infrastructure upgrades. Across all regions, increasing adoption of robotic-assisted surgeries, which have grown by over 20%, and rising demand for energy-based ligation devices are shaping market expansion and technological transformation.

North America holds approximately 38% of the ligation device market share, driven by a highly developed healthcare infrastructure and strong demand from hospitals and ambulatory surgical centers. Key industries fueling demand include general surgery, cardiovascular procedures, and robotic-assisted interventions, with over 70% of hospitals equipped for minimally invasive surgeries. Regulatory frameworks such as stringent medical device approvals ensure high safety and performance standards, encouraging innovation. Technological advancements include widespread integration of robotic-assisted systems, with over 60% of advanced hospitals utilizing such platforms. A major regional player, Medtronic, has expanded its portfolio of energy-based ligation devices, improving surgical precision and reducing complications by nearly 25%. Consumer behavior reflects high adoption of advanced technologies, with healthcare providers prioritizing efficiency, reduced recovery time, and improved clinical outcomes, resulting in over 65% preference for automated ligation solutions.

Europe accounts for nearly 27% of the ligation device market, with key countries including Germany, the United Kingdom, and France leading adoption. The region benefits from strong public healthcare systems and regulatory oversight through stringent medical device standards, which influence product development and ensure patient safety. Sustainability initiatives targeting a 20% reduction in medical waste are encouraging the adoption of reusable and eco-friendly ligation devices. Technological adoption is increasing, with over 55% of surgical facilities implementing minimally invasive techniques and energy-based ligation systems. A notable regional player, B. Braun, is advancing surgical innovation by developing high-efficiency ligation tools designed for precision and sustainability. Consumer behavior in Europe is shaped by regulatory compliance, with healthcare providers emphasizing reliability, traceability, and adherence to strict safety protocols, driving demand for advanced and certified ligation devices.

Asia-Pacific represents approximately 23% of the global ligation device market and ranks as the fastest-growing region in terms of surgical device adoption. Key countries such as China, India, and Japan are leading consumption, collectively accounting for over 65% of regional demand. The region performs more than 25 million surgeries annually, with minimally invasive procedures increasing by over 45% in recent years. Infrastructure expansion includes the addition of over 10,000 new hospitals and surgical centers, significantly boosting demand for ligation devices. Technological trends include rising adoption of robotic-assisted surgeries and AI-integrated surgical systems, particularly in urban healthcare hubs. Olympus, a key regional player, continues to innovate in advanced surgical instruments, enhancing procedural accuracy. Consumer behavior reflects growing preference for cost-effective yet technologically advanced solutions, with over 50% of healthcare providers prioritizing efficiency and improved patient outcomes.

South America holds approximately 7% of the ligation device market, with Brazil and Argentina as key contributors. The region is witnessing gradual improvements in healthcare infrastructure, with surgical procedure volumes increasing by over 30% in the past five years. Government initiatives aimed at expanding public healthcare access and increasing funding for medical equipment are supporting market growth. Trade policies encouraging medical device imports have improved access to advanced ligation technologies. A regional example includes increased adoption of energy-based ligation devices in Brazil, where over 45% of tertiary hospitals have upgraded surgical equipment. Consumer behavior in the region is influenced by cost sensitivity, with healthcare providers balancing affordability and functionality, leading to steady adoption of mid-range ligation devices across hospitals and clinics.

The Middle East & Africa region accounts for approximately 5% of the ligation device market, with major growth observed in countries such as the UAE and South Africa. Healthcare investments exceeding USD 50 billion in hospital development and modernization projects are driving demand for advanced surgical tools. The region is experiencing a 35% increase in surgical procedures due to improved access to healthcare services. Technological modernization includes the introduction of robotic-assisted surgeries and digital healthcare systems in leading hospitals. Trade partnerships and regulatory reforms are facilitating the import and adoption of high-quality ligation devices. A key regional trend includes the expansion of private healthcare networks, which now account for over 40% of advanced surgical procedures. Consumer behavior reflects increasing demand for high-quality medical technologies, with healthcare providers prioritizing reliability and efficiency in surgical outcomes.

United States – 34% share: Ligation Device market leadership driven by high surgical volumes, advanced healthcare infrastructure, and strong adoption of robotic-assisted technologies.

Germany – 9% share: Ligation Device market growth supported by robust medical device manufacturing, stringent regulatory standards, and widespread adoption of minimally invasive procedures.

The ligation device market is moderately consolidated, with over 25 active global and regional competitors competing through innovation, product differentiation, and strategic expansion. The top five companies collectively account for approximately 55% of the total market share, reflecting a strong presence of established players with extensive product portfolios. Market leaders are focusing on the development of advanced energy-based ligation systems, robotic-compatible devices, and AI-integrated surgical tools to enhance precision and efficiency. Strategic initiatives such as mergers and acquisitions have increased by over 18% in recent years, enabling companies to expand their technological capabilities and geographic reach. Product launches account for nearly 30% of competitive strategies, with a focus on minimally invasive surgical tools and disposable ligation devices. Partnerships with hospitals and research institutions are also rising, contributing to clinical validation and faster adoption of new technologies. Additionally, companies are investing heavily in research and development, with annual spending exceeding 10% of their total budgets, to maintain competitive advantage. The competitive environment is further shaped by regulatory compliance requirements and the need for continuous innovation to meet evolving healthcare demands.

Medtronic

Ethicon

B. Braun Melsungen AG

Olympus Corporation

Teleflex Incorporated

Conmed Corporation

Applied Medical Resources Corporation

Purple Surgical

Grena Ltd.

Ackermann Instrumente GmbH

The ligation device market is undergoing rapid technological transformation driven by precision engineering, digital integration, and energy-based innovations. One of the most impactful advancements is the adoption of energy-based vessel sealing technologies, including ultrasonic and advanced bipolar systems, which now account for nearly 45% of surgical device utilization in complex procedures. These systems enable simultaneous cutting and sealing of vessels up to 7 mm in diameter, reducing blood loss by approximately 25% and shortening operative time by nearly 30%.

Robotic-assisted surgery integration is another critical technological trend, with over 60% of high-end hospitals incorporating robotic platforms into surgical workflows. Ligation devices designed for robotic arms provide enhanced dexterity and precision, improving surgical accuracy by nearly 30%. Additionally, smart surgical systems embedded with sensors and real-time feedback mechanisms are gaining traction, allowing surgeons to monitor tissue response and adjust energy delivery dynamically, reducing complication rates by around 20%.

Artificial intelligence is also playing an increasing role in surgical planning and execution. AI-assisted imaging and predictive analytics are being used in over 35% of advanced operating rooms to guide ligation procedures, improving decision-making efficiency and reducing error rates by approximately 22%. Furthermore, disposable and single-use ligation devices are expanding, with adoption rising by over 40% due to infection control protocols and sterilization requirements.

Material innovation is another key area, with the use of biocompatible polymers and advanced alloys enhancing device durability and performance. Lightweight ergonomic designs are improving surgeon comfort and reducing fatigue during long procedures by nearly 15%. These technological advancements collectively support higher surgical throughput, improved patient outcomes, and operational efficiency, making them central to the evolving ligation device landscape.

• In March 2025, Medtronic announced enhancements to its LigaSure vessel sealing platform, integrating advanced energy modulation technology that improves sealing consistency across varying tissue types, reducing thermal spread by up to 20% and supporting more precise minimally invasive surgical procedures. Source: www.medtronic.com

• In October 2024, Johnson & Johnson’s Ethicon division expanded its surgical portfolio with upgraded ECHELON linear cutters featuring improved staple line integrity and compression control, enhancing surgical efficiency and reducing complications in laparoscopic procedures across global healthcare facilities. Source: www.jnj.com

• In January 2025, Olympus Corporation introduced an advanced energy-based surgical system designed to optimize vessel sealing performance, incorporating enhanced thermal control technology that reduces tissue damage and improves procedural outcomes in gastrointestinal and urological surgeries. Source: www.olympus-global.com

• In August 2024, Teleflex Incorporated launched a next-generation polymer ligation clip system with improved locking mechanisms, increasing clip retention strength by approximately 25% and supporting safer vessel occlusion in minimally invasive surgical applications. Source: www.teleflex.com

The Ligation Device Market Report provides a comprehensive evaluation of the global industry, covering a wide spectrum of product types, applications, technologies, and regional dynamics. The report encompasses key product segments including energy-based vessel sealing systems, clip appliers, and handheld ligation devices, collectively representing 100% of the market landscape. It further analyzes application areas such as general surgery, cardiovascular procedures, gynecological interventions, and urological treatments, which together account for over 85% of total device utilization in clinical settings.

Geographically, the report examines five major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, covering more than 30 countries with detailed insights into regional adoption patterns and healthcare infrastructure development. The scope includes analysis of over 25 leading market participants, representing approximately 80% of the competitive landscape, along with emerging players contributing to innovation and niche market expansion.

Technological coverage extends to robotic-assisted surgical systems, AI-integrated surgical planning tools, and advanced energy-based ligation technologies, which are currently adopted in over 50% of modern operating rooms in developed markets. The report also explores end-user segments such as hospitals, ambulatory surgical centers, and specialty clinics, with hospitals accounting for nearly 70% of total demand.

Additionally, the scope includes evaluation of regulatory frameworks, product innovation trends, supply chain dynamics, and evolving healthcare policies influencing market growth. Emerging segments such as disposable ligation devices and eco-friendly surgical tools are also analyzed, reflecting shifting industry priorities toward sustainability and infection control.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

8.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Medtronic, Ethicon, B. Braun Melsungen AG, Olympus Corporation, Teleflex Incorporated, Conmed Corporation, Applied Medical Resources Corporation, Purple Surgical, Grena Ltd., Ackermann Instrumente GmbH |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |