Reports

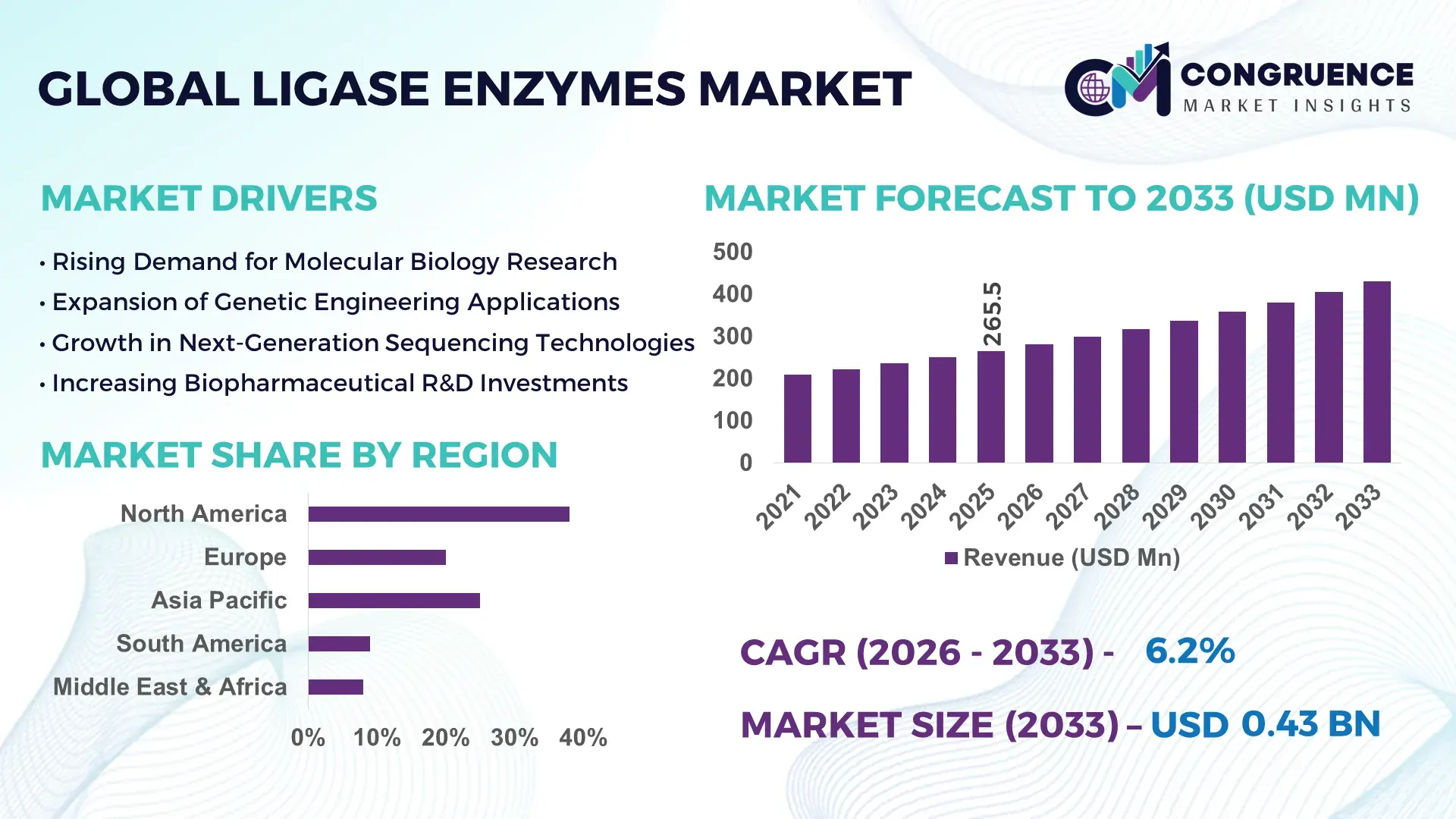

The Global Ligase Enzymes Market was valued at USD 265.5 Million in 2025 and is anticipated to reach a value of USD 429.59 Million by 2033 expanding at a CAGR of 6.2% between 2026 and 2033. This expansion is largely driven by increasing demand for advanced molecular biology tools used in genomics, DNA sequencing, and precision medicine research.

The United States continues to demonstrate strong industrial capacity and technological advancement in the ligase enzymes market through extensive biotechnology research infrastructure and large-scale genomic research initiatives. The country hosts more than 2,000 biotechnology companies and over 1,500 life science research laboratories actively utilizing DNA ligase enzymes for cloning, sequencing, and synthetic biology workflows. Government-backed research funding for genomics and biotechnology exceeds USD 45 billion annually, supporting extensive enzyme development and manufacturing capabilities. In addition, North America accounts for nearly 38% of global molecular biology reagent consumption, reflecting high adoption across pharmaceutical R&D, academic laboratories, and clinical diagnostics. More than 65% of next-generation sequencing workflows in the region incorporate ligase enzymes for DNA library preparation, highlighting their critical role in genetic research and biotechnology innovation.

Market Size & Growth: The ligase enzymes market was valued at USD 265.5 Million in 2025 and is projected to reach USD 429.59 Million by 2033, expanding at a CAGR of 6.2%, driven by rapid growth in genomics research, biotechnology manufacturing, and molecular diagnostics.

Top Growth Drivers: Rising genomics research adoption (45%), expansion of molecular diagnostics laboratories (38%), and increasing use of recombinant DNA technologies in pharmaceutical R&D (32%).

Short-Term Forecast: By 2028, automation in genomic sample preparation is expected to improve laboratory processing efficiency by nearly 30% and reduce reagent waste by approximately 18%.

Emerging Technologies: CRISPR-based genome editing platforms, high-fidelity DNA ligase engineering, and automated DNA library preparation technologies are transforming molecular biology workflows.

Regional Leaders: North America is projected to reach USD 165 Million by 2033 driven by strong biotech infrastructure; Europe may exceed USD 120 Million supported by academic research networks; Asia-Pacific is expected to approach USD 95 Million due to rapid expansion of genomic sequencing centers.

Consumer/End-User Trends: Pharmaceutical companies, contract research organizations, and academic research institutes represent the largest end-user groups, accounting for over 70% of ligase enzyme consumption in molecular cloning and DNA assembly applications.

Pilot or Case Example: In 2024, a genomic sequencing initiative in South Korea implemented automated ligase-based DNA assembly workflows that improved sequencing throughput by 35% and reduced laboratory processing time by 22%.

Competitive Landscape: The market leader holds approximately 21% share, followed by major biotechnology suppliers including Thermo Fisher Scientific, New England Biolabs, Merck KGaA, Promega Corporation, and Takara Bio.

Regulatory & ESG Impact: Increasing adoption of sustainable biotechnology manufacturing practices and stricter biosafety regulations are encouraging enzyme suppliers to develop environmentally efficient enzyme production processes with reduced chemical waste.

Investment & Funding Patterns: Global investment in genomics research infrastructure and biotechnology innovation exceeded USD 60 billion between 2022 and 2025, significantly accelerating enzyme development programs and production capacity expansion.

Innovation & Future Outlook: Next-generation engineered ligases, enzyme stabilization technologies, and AI-assisted protein design are expected to reshape enzyme efficiency and broaden applications across diagnostics, gene therapy, and synthetic biology.

Ligase enzymes play a critical role across several life science sectors including pharmaceutical drug development, genetic engineering, and clinical diagnostics. Pharmaceutical and biotechnology companies account for roughly 40% of enzyme consumption due to extensive DNA cloning and recombinant protein development activities. Academic and research institutes contribute nearly 35% through genomic studies and molecular biology experimentation. Continuous innovation in enzyme engineering has produced high-fidelity ligases with improved reaction speed and temperature tolerance, increasing laboratory efficiency. Additionally, expanding adoption of personalized medicine and large-scale genomic sequencing initiatives across North America, Europe, and Asia-Pacific is significantly influencing regional consumption patterns and accelerating long-term demand for advanced ligase enzyme technologies.

The ligase enzymes market holds strong strategic relevance within the biotechnology and life sciences ecosystem because these enzymes serve as foundational tools in DNA replication, repair, recombination, and molecular cloning. Their role is particularly critical in advanced genomic technologies including gene therapy development, synthetic biology, and next-generation sequencing platforms. As global investments in biotechnology infrastructure continue to rise, ligase enzymes are becoming essential components of automated molecular workflows used by pharmaceutical companies, contract research organizations, and diagnostic laboratories.

Technological innovation is reshaping the efficiency of ligase enzyme applications. For instance, engineered high-fidelity DNA ligase technology delivers nearly 40% higher ligation accuracy compared to conventional T4 DNA ligase protocols commonly used in earlier molecular cloning techniques. These improvements significantly reduce experimental errors in genomic assembly and DNA sequencing preparation. Regional trends also highlight evolving adoption patterns. North America dominates in production volume due to its strong biotechnology manufacturing base, while Asia-Pacific leads in adoption expansion with nearly 48% of newly established genomic research laboratories integrating advanced ligase enzyme platforms into sequencing workflows. In the near term, automation and artificial intelligence are expected to influence laboratory processes involving ligase enzymes. By 2027, AI-assisted enzyme design and automated sample preparation systems are expected to improve molecular biology workflow efficiency by approximately 30%, reducing experimental turnaround times and increasing reproducibility in research environments.

Environmental and regulatory considerations are also shaping strategic planning across biotechnology firms. Many enzyme manufacturers are committing to sustainability goals such as reducing biochemical production waste by 25% by 2030 through improved fermentation technologies and environmentally optimized purification processes. A notable micro-scenario occurred in 2024 when a biotechnology research program in Japan implemented automated DNA assembly platforms integrated with optimized ligase enzyme formulations, achieving a 33% increase in cloning efficiency and a 20% reduction in laboratory processing time. These developments demonstrate how advanced ligase enzyme technologies can improve research productivity.

The rapid expansion of genomics research and molecular diagnostics is a primary factor accelerating the demand for ligase enzymes worldwide. Global DNA sequencing output has increased dramatically over the past decade, with modern sequencing platforms capable of generating more than 20 terabases of genomic data in a single run. Ligase enzymes play a crucial role in preparing sequencing libraries by joining DNA fragments during the sample preparation stage. Nearly 70% of next-generation sequencing workflows rely on ligation reactions to construct DNA libraries for analysis. The growth of personalized medicine and genetic testing has further increased demand for molecular biology reagents used in clinical laboratories. More than 30 million genetic tests are conducted globally each year, many of which involve DNA manipulation techniques that require ligase enzymes. Pharmaceutical companies developing gene therapies and recombinant proteins also depend on DNA ligase enzymes for cloning and plasmid construction processes. As biotechnology infrastructure expands and genome research programs continue to grow, the demand for highly efficient and thermostable ligase enzymes is expected to remain strong across research institutions and clinical diagnostic laboratories.

Despite growing demand, the ligase enzymes market faces several technical and production-related limitations that can restrain wider adoption. Manufacturing high-purity enzymes requires complex fermentation processes, specialized purification technologies, and strict quality control protocols to ensure enzyme activity and stability. These processes involve advanced bioprocessing infrastructure and skilled personnel, increasing operational complexity for enzyme manufacturers. Another limitation relates to enzyme stability under varying laboratory conditions. Many ligase enzymes require specific temperature ranges and reaction buffers to maintain optimal activity. If conditions deviate from recommended parameters, ligation efficiency can decline significantly, affecting experimental reliability. Studies have shown that inefficient ligation reactions can reduce cloning success rates by up to 25% in poorly optimized workflows. Furthermore, storage and transportation of biological reagents require controlled temperature environments to maintain enzyme functionality. Cold chain logistics and specialized packaging add operational challenges for global distribution networks. These technical limitations can increase operational costs for research laboratories and biotechnology firms, which may slow adoption in cost-sensitive markets and smaller research facilities.

The expansion of synthetic biology and gene therapy research presents significant opportunities for the ligase enzymes market. Synthetic biology initiatives aim to design and construct new biological systems, requiring precise DNA assembly techniques that depend heavily on ligase enzymes. DNA ligases are widely used in Gibson assembly, Golden Gate cloning, and other DNA assembly methods that enable scientists to construct complex genetic circuits. The global number of gene therapy clinical trials has exceeded 2,000 studies across various therapeutic areas, including cancer treatment, rare genetic disorders, and neurological diseases. These research programs rely extensively on molecular cloning and plasmid construction, both of which require efficient ligase enzymes for DNA fragment joining. Additionally, advances in enzyme engineering have created ligases capable of functioning under a broader range of temperatures and reaction conditions, improving laboratory flexibility. Emerging biotechnology hubs in Asia-Pacific countries such as China, India, and Singapore are also expanding genomic research infrastructure and biotechnology startups, increasing demand for molecular biology tools. As synthetic biology applications expand into industrial biotechnology, agriculture, and bioengineering sectors, ligase enzymes are expected to play an increasingly vital role in enabling complex DNA manipulation technologies.

Regulatory compliance and scientific reproducibility represent ongoing challenges for the ligase enzymes market, particularly in clinical and pharmaceutical applications. Molecular biology reagents used in regulated environments such as diagnostic laboratories and drug development programs must meet strict quality and validation standards. Enzyme suppliers are required to comply with international laboratory quality guidelines and biotechnology manufacturing regulations to ensure product consistency and safety. Reproducibility of experimental results is another critical issue within life sciences research. Variations in enzyme activity, buffer composition, and experimental protocols can lead to inconsistent ligation efficiency, affecting the reliability of molecular cloning and sequencing experiments. Studies across academic research laboratories have indicated that reproducibility issues can affect nearly 20–30% of biological experiments due to variations in reagents and experimental conditions. Additionally, the increasing complexity of genetic engineering experiments requires highly specialized enzyme formulations and optimized protocols. Research institutions must invest in training, laboratory automation, and standardized workflows to reduce experimental variability. These technical and regulatory challenges require continuous innovation in enzyme manufacturing and quality assurance to maintain reliability and ensure consistent performance across global biotechnology laboratories.

• Expansion of Next-Generation Sequencing Workflows:

The rapid growth of next-generation sequencing technologies is significantly increasing demand for ligase enzymes used in DNA library preparation and genomic assembly. More than 70% of modern sequencing protocols rely on ligation reactions to attach adapters and assemble DNA fragments before sequencing. Global sequencing capacity has expanded dramatically, with high-throughput platforms now capable of generating over 20 terabases of genomic data in a single run. Research laboratories have reported that automated library preparation systems using optimized ligase enzymes can reduce sequencing preparation time by nearly 35% while improving ligation efficiency by approximately 28%. In large genomic research facilities across North America and Europe, adoption of automated sequencing workflows has increased by more than 40% in the past five years, further strengthening demand for high-performance ligase enzymes.

• Growing Adoption of Synthetic Biology and DNA Assembly Technologies:

Synthetic biology applications are increasingly driving the use of ligase enzymes in complex DNA construction and gene circuit engineering. Approximately 65% of synthetic biology experiments require precise DNA ligation processes during plasmid assembly and gene synthesis workflows. Advanced cloning techniques such as Golden Gate Assembly and Gibson Assembly have improved genetic assembly efficiency by nearly 30% compared to conventional cloning techniques. Biotechnology laboratories conducting large-scale DNA assembly projects have reported a 25% increase in enzyme consumption as research programs expand into industrial biotechnology, agricultural engineering, and microbial bio-manufacturing. Additionally, more than 3,500 synthetic biology research initiatives worldwide now integrate automated DNA assembly platforms that rely on optimized ligase enzyme formulations.

• Engineering of High-Fidelity and Thermostable Ligase Enzymes:

Advancements in enzyme engineering are enabling the development of high-fidelity ligase enzymes capable of operating under broader reaction conditions and delivering improved performance. Engineered DNA ligases have demonstrated up to 40% higher ligation accuracy and nearly 20% faster reaction rates compared with earlier enzyme formulations. Thermostable ligases capable of functioning at temperatures above 60°C are increasingly used in diagnostic assays and polymerase chain reaction workflows. These enhanced enzymes also exhibit improved stability during long experimental procedures, reducing reaction failures by approximately 18%. Biotechnology manufacturers have reported a 32% increase in research investment directed toward protein engineering programs aimed at optimizing enzyme structure and catalytic efficiency.

• Increasing Integration of Automation and AI-Assisted Laboratory Platforms:

Automation and artificial intelligence are reshaping molecular biology laboratories and influencing the adoption of ligase enzyme technologies. Automated DNA assembly and cloning platforms have reduced manual laboratory processes by nearly 45%, allowing researchers to conduct high-throughput experiments with greater accuracy. AI-assisted protein design platforms are also accelerating enzyme optimization, reducing experimental enzyme design cycles by nearly 30%. In addition, robotic liquid-handling systems integrated with ligase-based reactions have improved experimental reproducibility by approximately 25% in large biotechnology laboratories. The integration of automated laboratory systems has increased by over 50% among major pharmaceutical research organizations, creating a sustained demand for ligase enzymes compatible with high-throughput experimental environments.

The ligase enzymes market is segmented based on type, application, and end-user industries, each contributing to the expanding adoption of molecular biology tools in biotechnology and genomic research. Product types include DNA ligase enzymes, RNA ligase enzymes, and specialized thermostable ligases designed for diagnostic and sequencing workflows. Applications span molecular cloning, next-generation sequencing library preparation, genetic engineering, and diagnostic assay development. Molecular cloning remains one of the most widely used applications due to its importance in gene manipulation and recombinant protein development. End-users primarily include pharmaceutical and biotechnology companies, academic research institutions, contract research organizations, and clinical diagnostic laboratories. These sectors collectively account for a significant share of enzyme consumption as global genomic research activities expand. Increasing laboratory automation and synthetic biology innovation are further influencing segmentation patterns and driving adoption across multiple scientific disciplines.

DNA ligase enzymes represent the leading product type within the ligase enzymes market, accounting for approximately 58% of overall adoption due to their essential role in DNA replication, repair, and recombinant DNA technologies. These enzymes are widely used in molecular cloning, plasmid construction, and DNA sequencing preparation. RNA ligases currently hold nearly 24% of the market as they are utilized in RNA sequencing workflows, microRNA analysis, and RNA labeling applications. However, thermostable ligase enzymes represent the fastest-growing product segment with an estimated CAGR of around 7.4%, driven by their ability to function at higher temperatures and their increasing application in diagnostic assays and nucleic acid amplification technologies. Specialized ligase variants and engineered enzymes designed for synthetic biology applications contribute the remaining 18% of the market, serving niche applications such as DNA assembly automation and gene editing workflows. These specialized enzymes are gaining attention due to their enhanced catalytic efficiency and reaction specificity.

Molecular cloning remains the dominant application for ligase enzymes, accounting for nearly 46% of total market utilization. The widespread use of cloning techniques in genetic engineering, recombinant protein production, and gene therapy research has made ligase enzymes indispensable tools in biotechnology laboratories. Next-generation sequencing library preparation follows closely with approximately 32% adoption, reflecting the growing number of genomic sequencing programs worldwide. However, diagnostic assay development is emerging as the fastest-growing application segment, with an estimated CAGR of about 7.8%, supported by expanding genetic testing and molecular diagnostic technologies. Other applications including synthetic biology research, gene editing workflows, and nucleic acid labeling collectively contribute around 22% of market demand. These segments are expanding as biotechnology research diversifies into areas such as metabolic engineering and microbial genome design.

Pharmaceutical and biotechnology companies represent the largest end-user segment in the ligase enzymes market, accounting for approximately 41% of total demand. These organizations rely extensively on ligase enzymes for gene therapy research, recombinant protein production, and molecular drug discovery workflows. Academic and research institutions account for around 34% of market adoption due to the high volume of genomics, molecular biology, and synthetic biology studies conducted in universities and public research laboratories. Contract research organizations are emerging as the fastest-growing end-user segment, with an estimated CAGR of about 7.1%, driven by increasing outsourcing of biotechnology research and genomic analysis services. Clinical diagnostic laboratories, agricultural biotechnology firms, and forensic laboratories collectively contribute the remaining 25% of enzyme consumption. These sectors are expanding their use of ligase enzymes for DNA-based disease diagnostics, crop genetic modification studies, and forensic DNA profiling.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2026 and 2033.

The global distribution of the ligase enzymes market reflects strong biotechnology infrastructure, research investments, and expanding genomic sequencing activities across major regions. North America leads with a 38% share due to extensive pharmaceutical research programs, more than 2,500 biotechnology companies, and over 1,700 active genomics laboratories conducting molecular biology experiments. Europe follows with approximately 29% of global demand, supported by more than 900 academic research institutions and advanced biomedical innovation hubs. Asia-Pacific currently contributes nearly 24% of global consumption, driven by rapid expansion of genomic sequencing centers and biotechnology manufacturing facilities in China, Japan, and India. South America accounts for roughly 5% of the market with increasing adoption of molecular diagnostics in Brazil and Argentina, while the Middle East & Africa collectively hold close to 4% share as research infrastructure expands through government biotechnology investment programs. Regional differences in laboratory automation adoption, biotechnology R&D expenditure, and genomic medicine initiatives continue to influence demand patterns for ligase enzymes worldwide.

How Are Advanced Biotechnology Laboratories Accelerating Demand for DNA Assembly Technologies?

North America represents approximately 38% of the global ligase enzymes market, making it the most mature regional ecosystem for molecular biology tools and biotechnology innovation. The region hosts more than 2,000 biotechnology companies and over 1,500 research laboratories focused on genomics, drug discovery, and synthetic biology. Pharmaceutical R&D programs and precision medicine initiatives drive significant demand for DNA ligase enzymes used in cloning, sequencing, and recombinant DNA research. Regulatory agencies have strengthened support for genomic medicine, with federal biotechnology research funding exceeding USD 45 billion annually for life sciences innovation. Technological transformation within laboratories has also accelerated adoption of automated DNA assembly platforms and robotic liquid-handling systems capable of processing thousands of molecular reactions per day. One example is a leading biotechnology supplier that expanded enzyme engineering facilities in the United States in 2024 to increase production capacity for high-fidelity DNA ligases used in next-generation sequencing workflows. Regional consumer behavior reflects high enterprise adoption across healthcare research institutions and pharmaceutical companies, where more than 65% of molecular biology workflows incorporate automated enzyme-based technologies to improve experimental efficiency and reproducibility.

What Role Do Research Collaboration and Regulatory Frameworks Play in Expanding Molecular Biology Innovation?

Europe holds nearly 29% of the global ligase enzymes market, supported by strong biomedical research programs and advanced academic collaboration networks. Countries such as Germany, the United Kingdom, and France lead regional adoption due to their well-established biotechnology industries and extensive genomic research initiatives. Germany alone hosts more than 700 biotechnology companies and several large molecular research institutes conducting DNA sequencing and synthetic biology experiments. The region also benefits from comprehensive regulatory frameworks that encourage responsible biotechnology innovation and laboratory safety standards. Sustainability initiatives within European biotechnology manufacturing have pushed companies to adopt environmentally efficient enzyme production technologies that reduce chemical waste by nearly 20%. In addition, advanced gene editing research and synthetic biology platforms are expanding across European innovation hubs, accelerating demand for specialized ligase enzymes. A major European enzyme manufacturer recently launched engineered ligase formulations optimized for automated DNA assembly platforms, improving ligation accuracy by nearly 35%. Regional consumer behavior shows strong emphasis on regulatory compliance and validated laboratory reagents, resulting in growing demand for high-purity enzymes used in clinical research and pharmaceutical development programs.

How Is Rapid Biotechnology Expansion Transforming Demand for Advanced Molecular Tools?

Asia-Pacific currently represents roughly 24% of the global ligase enzymes market and ranks among the fastest-growing regions due to large-scale expansion of biotechnology infrastructure and genomic research programs. China, Japan, and India are the leading consuming countries, collectively accounting for more than 70% of regional demand for molecular biology reagents. China alone has established more than 1,200 biotechnology startups and research facilities focused on genomics, gene editing, and precision medicine applications. Manufacturing infrastructure across Asia-Pacific has also expanded significantly, with multiple enzyme production facilities increasing annual output to support growing regional demand. Biotechnology innovation hubs in Shanghai, Tokyo, and Bangalore are investing heavily in synthetic biology research and DNA sequencing technologies capable of processing millions of genetic samples annually. A Japanese biotechnology company introduced high-efficiency ligase enzymes designed for automated genomic assembly systems used in clinical research laboratories. Consumer behavior across the region reflects rapid adoption of biotechnology tools within academic institutions and contract research organizations, where genomic sequencing projects and pharmaceutical discovery programs continue to drive strong demand for ligase enzymes.

How Are Expanding Genomic Research Initiatives Supporting Growth in Molecular Biology Tools?

South America accounts for approximately 5% of the global ligase enzymes market, with Brazil and Argentina emerging as the leading regional consumers of molecular biology reagents. Brazil hosts more than 200 life science research institutes and biotechnology laboratories actively conducting genetic research, agricultural biotechnology studies, and disease diagnostics programs that require DNA ligase enzymes. Government initiatives supporting biotechnology research and public health genomics programs have strengthened regional laboratory infrastructure. Several national research programs now focus on genetic disease identification and crop improvement, which require advanced DNA manipulation technologies. Trade partnerships with North American and European biotechnology suppliers have also improved access to high-quality molecular biology reagents. In Brazil, a biotechnology research institute recently implemented automated sequencing workflows capable of processing more than 50,000 genomic samples annually using ligase-based library preparation technologies. Regional consumer behavior indicates that adoption is largely driven by academic research institutions and public health laboratories seeking improved genomic analysis capabilities for agricultural genetics and infectious disease monitoring.

What Factors Are Driving the Expansion of Biotechnology Research Infrastructure?

The Middle East & Africa region holds close to 4% of the global ligase enzymes market but is gradually expanding due to increasing investment in biotechnology research infrastructure and medical genomics initiatives. Countries such as the United Arab Emirates, Saudi Arabia, and South Africa are leading regional growth through government-funded biotechnology programs and advanced healthcare research projects. Several biotechnology innovation zones have been established in the Gulf region to promote genomic research and pharmaceutical development. These initiatives have led to the establishment of modern molecular biology laboratories capable of performing high-throughput DNA sequencing and genetic diagnostics. Technological modernization programs are also integrating automated laboratory equipment and advanced bioinformatics platforms to support large-scale research studies. In South Africa, a biotechnology research center recently launched a national genomic surveillance program capable of processing more than 100,000 DNA samples annually using advanced ligase-based sequencing technologies. Regional consumer behavior shows increasing adoption among healthcare research institutes and academic laboratories seeking to improve genetic disease diagnostics and epidemiological monitoring capabilities.

United States – 34% market share: The United States dominates the Ligase Enzymes Market due to its extensive biotechnology infrastructure, large pharmaceutical R&D investment, and more than 1,500 active genomics laboratories conducting molecular biology research.

Germany – 11% market share: Germany leads the European Ligase Enzymes Market with strong biotechnology manufacturing capabilities, over 700 life science companies, and extensive research activity in genetic engineering and synthetic biology.

The ligase enzymes market is moderately consolidated, with a group of global biotechnology companies maintaining strong technological leadership while several smaller specialized enzyme developers contribute to niche innovation. More than 35 active companies worldwide manufacture or supply ligase enzymes used in molecular biology, genomic sequencing, and synthetic biology research. The top five companies collectively account for nearly 55% of total market activity due to their established distribution networks, extensive research capabilities, and diversified product portfolios covering molecular biology reagents.

Competition is strongly driven by technological innovation, particularly in enzyme engineering, reaction optimization, and automated laboratory integration. Companies are investing heavily in protein engineering technologies to develop high-fidelity ligases capable of improving DNA assembly accuracy by more than 35%. Several suppliers are also expanding production facilities to support increasing demand from genomics laboratories and pharmaceutical research organizations.

Strategic collaborations and partnerships are also shaping the competitive landscape. Biotechnology firms frequently collaborate with genomic sequencing platform developers to optimize enzyme formulations used in automated library preparation systems. Product launches remain a major competitive strategy, with new ligase variants designed for high-throughput sequencing workflows and diagnostic assays entering the market each year.

Additionally, companies are integrating digital tools and AI-assisted protein design systems to accelerate enzyme discovery and improve catalytic efficiency. These innovations are enabling faster experimental workflows and expanding the application scope of ligase enzymes across biotechnology research, clinical diagnostics, and synthetic biology industries.

Thermo Fisher Scientific

New England Biolabs

Merck KGaA

Promega Corporation

Takara Bio Inc.

Agilent Technologies

Qiagen N.V.

Bio-Rad Laboratories

Enzymatics Inc.

Jena Bioscience GmbH

Lucigen Corporation

GenScript Biotech Corporation

Technological progress in enzyme engineering and molecular biology automation is significantly transforming the ligase enzymes market. DNA ligases are essential catalysts used to join DNA fragments during replication, recombination, and repair processes, making them indispensable for modern genomic research and biotechnology production. One of the most important technological advancements involves the development of high-fidelity ligases with enhanced specificity and faster reaction kinetics. Engineered ligases now demonstrate up to 40% higher ligation accuracy and nearly 25% improved reaction efficiency compared with earlier enzyme formulations, enabling researchers to perform complex DNA assembly with reduced experimental error rates.

Another major innovation is the integration of ligase enzymes into automated next-generation sequencing (NGS) library preparation systems. High-throughput sequencing facilities can process more than 10,000 DNA samples per week using robotic liquid-handling platforms that incorporate ligase-based adapter ligation steps. These automated workflows have reduced laboratory processing time by approximately 35% while improving reproducibility by nearly 30%. Thermostable ligase enzymes represent another emerging technology, capable of functioning at temperatures above 60°C and maintaining stability for extended reaction cycles. These properties make them highly valuable in molecular diagnostics and nucleic acid amplification assays used in clinical laboratories.

Artificial intelligence is also beginning to influence enzyme design and optimization. AI-assisted protein engineering platforms can evaluate thousands of potential amino acid configurations within enzyme structures, shortening enzyme development cycles by nearly 30%. These systems are enabling biotechnology companies to design ligases with improved catalytic efficiency, broader buffer compatibility, and increased stability under variable laboratory conditions. Additionally, advancements in synthetic biology platforms and CRISPR gene editing technologies are expanding the use of ligase enzymes for constructing complex genetic circuits and engineered microbial genomes.

Digital laboratory ecosystems are further accelerating technological transformation in this market. Cloud-connected laboratory automation systems and integrated data analytics tools now allow research facilities to monitor enzyme reaction efficiency, sample throughput, and experimental success rates in real time. Such innovations are improving operational efficiency across biotechnology laboratories and strengthening the role of advanced ligase enzymes in genomic sequencing, gene therapy development, and synthetic biology manufacturing.

• In January 2025, Thermo Fisher Scientific expanded its molecular biology reagent portfolio by launching an advanced DNA ligase formulation optimized for high-throughput next-generation sequencing library preparation. The product improves adapter ligation efficiency and enables automated genomic workflows in large sequencing laboratories. Source: www.thermofisher.com

• In September 2024, New England Biolabs introduced an improved thermostable DNA ligase designed for high-temperature nucleic acid amplification and diagnostic assays. The enzyme demonstrates enhanced stability in extended reaction cycles and supports molecular diagnostic applications requiring highly reliable ligation reactions. Source: www.neb.com

• In April 2024, Promega Corporation released an optimized ligase enzyme system developed for automated cloning and DNA assembly platforms. The system was designed to increase cloning efficiency and compatibility with robotic liquid-handling instruments used in high-throughput synthetic biology laboratories.

• In November 2024, Takara Bio announced the expansion of its molecular biology enzyme manufacturing capacity in Japan to support rising global demand for DNA ligases used in genomic sequencing and gene therapy research programs. The facility upgrade increased enzyme production throughput and improved quality control capabilities.

The Ligase Enzymes Market Report provides a comprehensive analysis of the global industry covering technological developments, product segmentation, application trends, and regional market dynamics. The report evaluates multiple enzyme categories including DNA ligases, RNA ligases, and thermostable ligase variants used in molecular cloning, DNA repair studies, sequencing library preparation, and synthetic biology research. DNA ligase products represent the most widely utilized segment due to their central role in DNA recombination, plasmid construction, and genome assembly technologies. From an application perspective, the report examines major areas including molecular cloning, next-generation sequencing library preparation, diagnostic assay development, and genetic engineering workflows. Molecular cloning remains one of the most extensively used applications across biotechnology laboratories, while sequencing library preparation has become increasingly important with the expansion of global genomics initiatives processing millions of genetic samples annually.

The study also evaluates end-user industries such as pharmaceutical and biotechnology companies, academic and research institutions, contract research organizations, and clinical diagnostic laboratories. Pharmaceutical companies represent a major user group due to their extensive use of recombinant DNA technologies and gene therapy research programs. Academic research laboratories also account for significant demand as global universities and public research institutions conduct large-scale genomic studies and molecular biology experiments. Geographically, the report covers key regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. North America and Europe collectively account for a large proportion of global molecular biology reagent consumption due to advanced research infrastructure and high biotechnology investment levels. Meanwhile, Asia-Pacific has emerged as a rapidly expanding region with growing biotechnology manufacturing capabilities and increasing genomic sequencing initiatives in countries such as China, Japan, and India.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

6.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Thermo Fisher Scientific, New England Biolabs, Merck KGaA, Promega Corporation, Takara Bio Inc., Agilent Technologies, Qiagen N.V., Bio-Rad Laboratories, Enzymatics Inc., Jena Bioscience GmbH, Lucigen Corporation, GenScript Biotech Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |