Reports

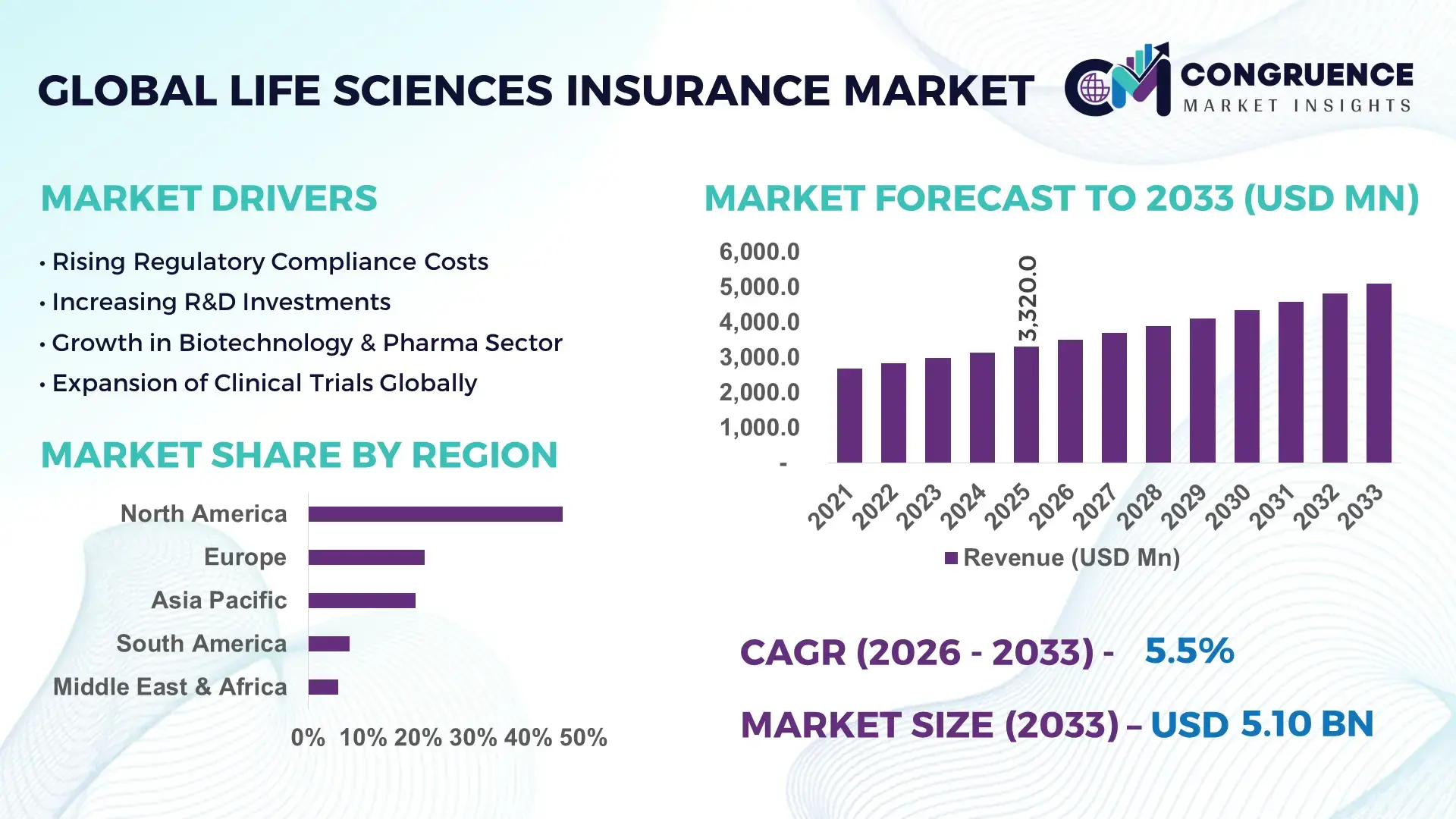

The Global Life Sciences Insurance Market was valued at USD 3,320.0 Million in 2025 and is anticipated to reach a value of USD 5,095.2 Million by 2033, expanding at a CAGR of 5.5% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by rising clinical trial activity, increasing regulatory exposure, and higher financial risk associated with advanced life sciences innovation.

The United States holds the leading position in the Life Sciences Insurance Market due to the scale and maturity of its life sciences ecosystem. The country hosts 8,000+ biotechnology companies and 3,000+ pharmaceutical manufacturers, generating consistent demand for clinical trial insurance, product liability, cyber-risk, and professional indemnity coverage. U.S. life sciences R&D spending exceeds USD 230 billion annually, increasing insured asset intensity. Over 65% of global Phase III clinical trials are conducted or sponsored from the U.S., significantly raising trial-related insurance demand. Additionally, nearly 70% of large U.S. life sciences firms use AI-driven underwriting and digital risk analytics platforms to enhance claims prediction, compliance tracking, and policy optimization.

Market Size & Growth: Valued at USD 3,320.0 Million in 2025 and projected to reach USD 5,095.2 Million by 2033, driven by expanding R&D risk exposure and complex regulatory requirements.

Top Growth Drivers: Clinical trial expansion (42%), regulatory compliance intensity (36%), cyber-risk exposure growth (31%).

Short-Term Forecast: By 2028, digital underwriting is expected to reduce policy processing timelines by approximately 28%.

Emerging Technologies: AI-based underwriting models, predictive claims analytics, blockchain-enabled policy administration.

Regional Leaders: North America (USD 2.15 Billion by 2033), Europe (USD 1.55 Billion), Asia Pacific (USD 0.95 Billion) with increasing biotech insurance adoption.

Consumer / End-User Trends: Pharmaceutical manufacturers and CROs account for over 58% of total insurance demand.

Pilot or Case Example: In 2024, a U.S.-based CRO reduced claims settlement delays by 34% using AI-enabled insurance platforms.

Competitive Landscape: Market leader holds ~18% share, followed by Allianz, AXA XL, Chubb, Zurich Insurance, and Munich Re.

Regulatory & ESG Impact: ESG-linked disclosures and stricter trial transparency rules are reshaping policy structures.

Investment & Funding Patterns: Over USD 4.6 Billion invested globally in specialty insurance and insurtech platforms.

Innovation & Future Outlook: Integration of real-time clinical and operational data is redefining life sciences risk coverage.

Life Sciences Insurance demand is led by pharmaceutical manufacturing (38%), biotechnology R&D (29%), medical devices (21%), and contract research services (12%). Innovation in AI underwriting, cyber-liability bundling, and parametric insurance is reshaping product offerings, while regulatory pressure and globalized trials continue to influence regional consumption patterns and future market expansion.

The Life Sciences Insurance Market has become a strategic enabler for innovation continuity, compliance assurance, and operational resilience across pharmaceutical, biotechnology, and medical device industries. As R&D investments grow in scale and complexity, insurance coverage now extends beyond traditional liability to include cyber-risk, IP litigation, trial interruption, and environmental exposure. AI-driven underwriting delivers nearly 35% improvement in risk assessment accuracy compared to conventional actuarial models. North America dominates in insurance volume, while Europe leads in regulatory-driven adoption, with over 62% of life sciences enterprises integrating compliance-linked insurance frameworks.

By 2028, predictive analytics and automation are expected to reduce claims resolution time by nearly 30%. Firms are also committing to ESG-linked risk strategies, targeting 25% reduction in environmental liability exposure by 2030. In 2024, a leading U.S. pharmaceutical company achieved a 22% reduction in operational risk incidents through AI-enabled insurance risk monitoring. Looking forward, the Life Sciences Insurance Market is positioned as a pillar of resilience, regulatory compliance, and sustainable growth across global life sciences value chains.

The Life Sciences Insurance Market is shaped by increasing scientific complexity, cross-border clinical trials, regulatory scrutiny, and digital transformation. Growth in biologics, gene therapies, and personalized medicine has elevated financial and compliance risks, driving demand for specialized insurance products. Insurers are increasingly adopting digital platforms to enhance underwriting accuracy, claims efficiency, and real-time risk monitoring, reinforcing the market’s strategic importance.

Global clinical trial volumes have increased by over 45%, with Phase III trials often exceeding USD 100 Million per project. This expansion raises exposure to participant liability, regulatory penalties, and operational risks, significantly boosting insurance demand across sponsors and CROs.

Advanced therapies and multi-region trials increase underwriting complexity and premium costs. Limited historical risk data for emerging therapies further constrains actuarial precision, especially for smaller biotech firms.

AI-based risk modeling reduces manual assessment effort by nearly 40%, enabling insurers to expand coverage to mid-sized biotech firms and introduce dynamic, usage-based insurance models.

Divergent regulations across the FDA, EMA, and Asia-Pacific authorities require region-specific policy structures, increasing administrative and compliance burdens for insurers.

AI-Driven Risk Assessment: Nearly 48% of insurers now use AI tools, improving underwriting accuracy by 32% and reducing claim volatility by 18%.

Cyber Liability Expansion: With over 60% of life sciences firms handling sensitive genomic data, cyber insurance adoption has risen by 41%.

Modular Facility Coverage Growth: Around 55% of new life sciences facilities use modular construction, increasing demand for construction-risk and operational insurance coverage.

Integrated Risk Policies: About 46% of large pharmaceutical companies now prefer bundled insurance solutions, reducing administrative overhead by 27%.

The Life Sciences Insurance Market is segmented based on type, application, and end-user, reflecting the diverse risk profiles and operational complexities across the life sciences value chain. By type, the market includes clinical trial insurance, product liability insurance, professional indemnity insurance, cyber insurance, and environmental liability coverage, each addressing distinct regulatory and operational exposures. Application-wise, insurance demand spans pharmaceutical manufacturing, biotechnology research, medical device development, and contract research activities, with risk intensity varying by development stage and geography. End-user segmentation highlights pharmaceutical companies, biotechnology firms, contract research organizations (CROs), medical device manufacturers, and academic or research institutions. Increasing clinical trial volumes, higher digital data usage, and stricter compliance requirements are reshaping segmentation dynamics, with insurers offering more customized and bundled coverage models aligned to end-user risk maturity and operational scale.

Clinical trial insurance represents the leading type within the Life Sciences Insurance Market, accounting for approximately 34% of total adoption, due to the rising number of late-stage trials, higher participant protection requirements, and increased regulatory scrutiny. Product liability insurance follows closely, holding around 27%, driven by post-market surveillance obligations and litigation risks associated with pharmaceuticals and medical devices. However, cyber insurance is the fastest-growing type, expanding at an estimated 8.9% CAGR, supported by the rapid digitization of clinical data, cloud-based R&D platforms, and heightened exposure to data breaches involving genomic and patient information.

Professional indemnity and environmental liability insurance together account for a combined 39% share, serving niche but critical roles in covering regulatory non-compliance, manufacturing contamination, and cross-border operational risks. These segments are increasingly bundled into integrated policies to simplify risk management for mid-sized and large enterprises.

• In 2025, a national health research authority reported that over 70% of newly approved clinical trials required mandatory clinical trial liability coverage before participant enrollment, reinforcing the dominance of this insurance type.

Pharmaceutical manufacturing is the leading application segment, representing approximately 41% of insurance demand, due to high asset intensity, complex supply chains, and strict regulatory oversight during production and distribution. Biotechnology research accounts for about 29%, reflecting elevated risk during early-stage innovation, biologics development, and gene-based therapies. Medical device development contributes nearly 18%, driven by product recalls, quality failures, and global compliance requirements. Contract research activities and other applications collectively hold a combined 12% share.

Among these, biotechnology research insurance applications are growing fastest, with an estimated 9.4% CAGR, supported by increased venture funding, decentralized trials, and accelerated approval pathways. In 2025, more than 46% of biotech firms globally reported expanding insurance coverage beyond basic liability to include cyber and IP-related risks. Additionally, 38% of CROs indicated increased insurance spending tied to multinational trial execution and data governance requirements.

• In 2025, a global health policy organization documented that AI-assisted clinical research platforms were insured across more than 180 active trials, improving protocol compliance and reducing trial disruption incidents.

Pharmaceutical companies form the largest end-user segment, accounting for approximately 44% of total insurance adoption, due to large-scale manufacturing operations, global distribution networks, and sustained litigation exposure. Biotechnology firms follow with nearly 32%, reflecting growing innovation intensity and higher risk concentration during R&D stages. Contract research organizations represent about 14%, while medical device manufacturers and academic research institutions together contribute a combined 10% share.

The biotechnology segment is the fastest-growing end-user group, expanding at an estimated 9.8% CAGR, driven by increased clinical trial activity, regulatory acceleration programs, and higher reliance on digital platforms. In 2025, over 52% of biotech companies reported adopting bundled insurance solutions covering clinical, cyber, and professional risks. Meanwhile, 41% of CROs indicated rising demand for customized trial insurance linked to regional regulatory requirements.

• In 2025, a government-backed innovation agency reported that more than 600 biotechnology startups adopted structured insurance frameworks as a prerequisite for institutional funding and international trial participation.

North America accounted for the largest market share at 46.2% in 2025, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2026 and 2033.

North America’s dominance is supported by high clinical trial density, advanced insurance penetration, and strong regulatory enforcement, while Asia-Pacific growth is driven by expanding pharmaceutical manufacturing, rising biotech investments, and increasing cross-border clinical research. Europe follows with a 27.4% share, supported by stringent compliance frameworks and sustainable healthcare policies. South America and the Middle East & Africa collectively account for 13.1% of the market, with rising demand tied to healthcare infrastructure expansion, regional clinical research activity, and improved regulatory alignment. Across regions, increasing digitalization, higher insured asset values, and growing cyber-risk exposure are reshaping regional insurance adoption patterns.

The region holds approximately 46.2% of the global Life Sciences Insurance Market, reflecting mature insurance adoption across pharmaceutical, biotechnology, and medical device industries. Demand is driven by large-scale drug manufacturing, high clinical trial volumes, and extensive use of digital health platforms. Regulatory frameworks mandate comprehensive liability, trial, and cyber insurance coverage, increasing policy depth per enterprise. Over 65% of late-stage clinical trials are sponsored or managed from this region, intensifying trial-related insurance demand. Digital transformation is notable, with more than 68% of insurers deploying AI-driven underwriting and claims analytics. A leading regional insurer expanded integrated cyber and trial-risk coverage in 2025, supporting over 400 life sciences clients. Enterprise buyers in healthcare and finance-heavy ecosystems show higher bundled-policy adoption, exceeding 55% among large firms.

Europe accounts for around 27.4% of the Life Sciences Insurance Market, with Germany, the UK, and France representing over 61% of regional demand. Strong regulatory oversight, clinical trial transparency requirements, and sustainability-linked compliance frameworks are driving insurance uptake. Environmental and product liability coverage remains critical due to strict manufacturing and waste management rules. Over 48% of insured entities in the region now require explainable risk models to align with governance standards. Adoption of digital underwriting platforms has crossed 50% among large insurers. A prominent regional insurance group launched ESG-linked liability policies covering carbon exposure and supply-chain risks. Buyer behavior reflects compliance-driven purchasing, with regulatory pressure increasing demand for transparent and auditable insurance structures.

Asia-Pacific ranks second by growth momentum and contributes approximately 19.5% of global market volume. China, India, and Japan together account for over 70% of regional demand, driven by pharmaceutical manufacturing expansion, biosimilar production, and clinical research outsourcing. More than 42% of new drug manufacturing facilities commissioned since 2023 are located in this region, increasing asset and liability insurance needs. Technology hubs are accelerating adoption of cloud-based policy management and AI risk scoring. A regional insurer expanded coverage for over 300 biotech firms engaged in cross-border trials. Buyer behavior is cost-sensitive but rapidly evolving, with SMEs increasingly adopting modular insurance packages linked to mobile and digital platforms.

South America holds nearly 7.6% of the global market, led by Brazil and Argentina, which together contribute over 68% of regional demand. Expansion of public healthcare systems, localized drug manufacturing, and medical device assembly is increasing insurance needs. Government incentives supporting domestic pharmaceutical production have raised insured operational footprints. Trade policy adjustments have also increased cross-border clinical research, driving trial insurance demand. A regional insurer partnered with hospital networks to extend professional liability coverage across 120+ facilities. Buyer behavior shows insurance adoption closely tied to regulatory approvals and localization requirements, particularly in pharmaceutical supply chains.

The Middle East & Africa region accounts for approximately 5.5% of global demand, with the UAE and South Africa emerging as key growth centers. Investment in healthcare infrastructure, biologics manufacturing, and clinical research hubs is increasing insurance penetration. Over 35% of new healthcare facilities launched since 2024 include mandatory liability and cyber coverage requirements. Digital modernization is accelerating, with insurers adopting cloud-based underwriting tools. A regional insurer expanded trial insurance support for 50+ multinational research projects. Buyer behavior varies widely, with higher adoption among government-backed healthcare and research institutions compared to private SMEs.

United States – 38.6% Market Share: Strong pharmaceutical production capacity, high clinical trial volumes, and advanced regulatory enforcement drive sustained insurance demand.

Germany – 9.4% Market Share: High-value pharmaceutical manufacturing, stringent compliance requirements, and advanced healthcare infrastructure support insurance adoption.

The competitive environment in the Life Sciences Insurance Market is defined by a mix of specialty insurers, global underwriting giants, large brokerage networks, and emerging digital-first players. There are 30+ active competitors offering tailored risk solutions for clinical trials, product liability, cyber risk, professional indemnity, and integrated risk portfolios. The market displays a moderately consolidated structure, with the top 5 companies holding approximately 32–35% combined share of global specialty life sciences risk premiums, indicating significant room for differentiated players and niche underwriters. Major incumbents include Allianz, Munich Re, Chubb, AXA XL, and Zurich Insurance, each with deep risk management expertise and broad geographic footprints. Strategic initiatives have accelerated competitive intensity: Munich Re Specialty launched a dedicated life science liability business in North America in 2025 to serve pharmaceuticals, clinical sponsors, and medical device makers with flexible, comprehensive coverage solutions; Skyward Specialty rolled out a new life sciences liability product in late 2024 to expand its healthcare underwriting suite, enhancing product breadth and claims management capabilities. Global brokerages such as Marsh McLennan and Aon continue to integrate analytics-driven risk modeling and bespoke program structuring, while insurers invest heavily in digital underwriting platforms, AI-enabled risk assessment tools, and integrated policy administration systems to improve customer experience and precision. Innovation trends—such as embedded cyber cover, real-time data analytics, and parametric response modules—are compelling competitors to evolve beyond traditional liability products, intensifying competition and raising service expectations for life sciences enterprises worldwide.

AXA XL

Zurich Insurance Group

AIG (American International Group)

Swiss Re

Berkshire Hathaway Specialty Insurance

Tokio Marine HCC

Sompo International

Liberty Mutual Insurance

Everest Re Group

Markel Corporation

Beazley Group

The Life Sciences Insurance Market is being reshaped by a wave of technological innovation aimed at enhancing underwriting precision, accelerating claims processing, and enriching customer engagement. Advanced analytics and AI-driven risk modeling are increasingly core components of underwriting workflows, enabling insurers to integrate real-time clinical, operational, and regulatory data streams into dynamic risk profiles for pharmaceutical, biotech, and medical device clients. These technologies empower underwriters to surface nuanced exposures—such as protocol deviation risk or cyber-attack likelihood—more rapidly than traditional actuarial approaches. Emerging capabilities in machine learning support pattern recognition across claims histories and policy portfolios, improving fraud detection and loss projection accuracy. Meanwhile, blockchain and distributed ledger solutions are being piloted to foster transparency and streamline multi-party data sharing across insurers, brokers, and clients, ensuring secure verification of coverage terms and claims status. Digital platforms with mobile-first interfaces are enhancing client interactions, allowing life sciences enterprises to access policy documents, file claims, and receive automated compliance alerts from anywhere. The integration of parametric models is enabling instant payouts for pre-defined risk triggers—an attractive feature for rapid-response exposures like data breaches or supply chain interruptions. Together, these technologies are reducing operational friction, lowering administrative costs, and enabling insurers to offer tailored, scalable products that align with the complex risk landscapes of modern life sciences organizations, meeting the needs of decision-makers focused on resiliency, risk transparency, and strategic coverage design.

• In June 2025, Munich Re Specialty–North America launched a dedicated Life Science Liability business line offering comprehensive product defect, clinical trial, cyber, and professional liability coverage for pharmaceuticals, medical devices, dietary supplements, and contract services. Source: www.munichre.com

• In March 2025, The Doctors Company agreed to acquire specialty insurer ProAssurance in a transaction valued at approximately USD 1.3 billion, bringing ProAssurance’s life sciences liability and medical technology coverage into an expanded risk platform. Source: www.reuters.com

• In December 2025, Willis Towers Watson announced a planned acquisition of brokerage firm Newfront in a deal worth up to USD 1.3 billion, aimed at enhancing its technology-driven insurance distribution and specialty risk capabilities across sectors including life sciences. Source: www.reuters.com

• In May 2025, Alphabet’s life sciences division Verily completed the sale of its stop-loss insurance subsidiary Granular to Elevance Health, enabling strategic realignment of investments toward core AI-driven health solutions. Source: www.businessinsider.com

The Life Sciences Insurance Market Report provides a comprehensive examination of risk transfer solutions and their application across pharmaceutical, biotechnology, medical device, and clinical research ecosystems. It covers detailed segmentation by policy type—including clinical trial liability, product liability, professional indemnity, cyber risk, environmental liability, and bundled coverage modules tailored for complex exposures. The geographic scope encompasses North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering comparative insights into regional risk profiles, regulatory environments, insurer capabilities, and adoption patterns. The report analyzes end-user groups such as large pharmaceutical manufacturers, mid-sized biotech innovators, contract research organizations, and institutional research entities, detailing how coverage needs and purchasing behaviors vary. It also highlights emerging and digital technologies shaping underwriting, claims management, and customer engagement, such as AI risk scoring, advanced analytics, digital policy administration platforms, blockchain-enabled data sharing, and parametric coverage triggers. Regulatory and compliance landscapes are explored, including global and regional frameworks affecting policy design, data security requirements, and liability frameworks. The report also includes competitive insights profiling global insurers, specialty underwriters, and brokerage networks that serve the life sciences sector, summarizing strategic initiatives, product innovations, and market positioning. Niche segments such as embedded insurance offerings, ESG-aligned risk products, and integrated cyber-liability frameworks are also examined to provide decision-makers with a full view of current capabilities and future expansion opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 3,320.0 Million |

| Market Revenue (2033) | USD 5,095.2 Million |

| CAGR (2026–2033) | 5.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Allianz SE; Munich Re; Chubb Limited; AXA XL; Zurich Insurance Group; AIG; Swiss Re; Berkshire Hathaway Specialty Insurance; Tokio Marine HCC; Sompo International; Liberty Mutual Insurance; Everest Re Group; Markel Corporation; Beazley Group |

| Customization & Pricing | Available on Request (10% Customization Free) |