Reports

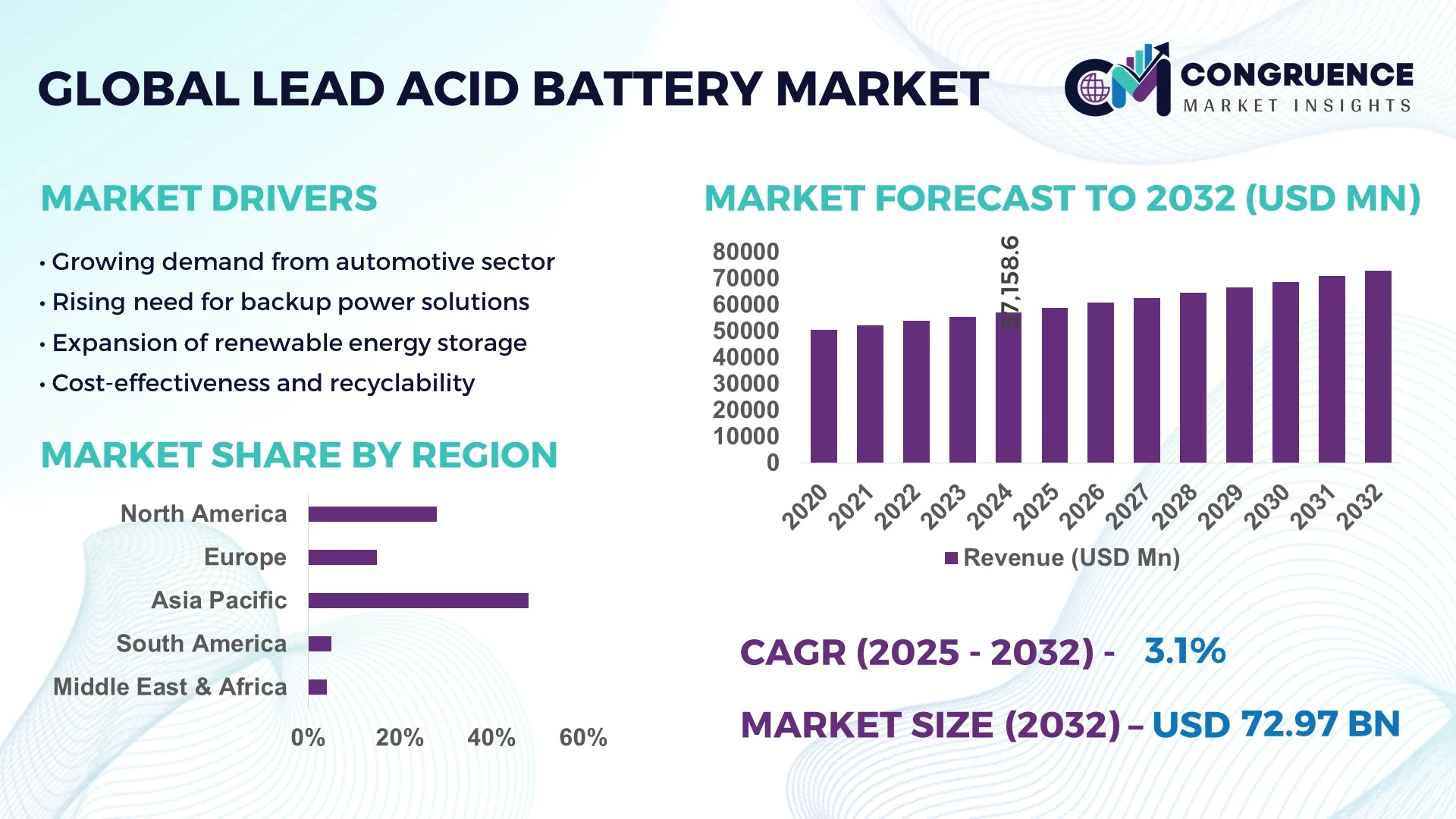

The Global Lead Acid Battery Market was valued at USD 57158.64 Million in 2024 and is anticipated to reach a value of USD 72971.15 Million by 2032 expanding at a CAGR of 3.1%% between 2025 and 2032.

China, holding a commanding position in the global Lead Acid Battery Market, leads in expansive production capacity bolstered by substantial capital investments in advanced manufacturing technologies, widespread industrial and automotive integration, and constant enhancements in battery design such as improved electrode materials.

The country focuses heavily on critical applications—including automotive start-stop systems, large-scale energy storage, and telecom-related backup solutions—while driving technological developments in VRLA, AGM advancements, and lead recovery systems through significant R&D initiatives. Over 100 additional words follow: The Lead Acid Battery Market continues to underpin diverse industry sectors, with the automotive segment at the forefront, particularly for starting, lighting, and ignition systems, complemented by substantial demand from telecommunications, industrial backup power, and renewable energy storage. Notable technological advancements include the development of Absorbent Glass Mat (AGM) and gel-VRLA batteries offering enhanced lifespan and discharge efficiency, along with innovations in electrode design using calcium-alloy grids and carbon additives that boost conductivity and cycle life. Regulatory frameworks focusing on environmental compliance, enhanced recycling mandates, and lead emission controls are shaping production practices, while economic pressures for cost-effective, reliable energy storage continue driving adoption. Regional consumption trends reveal strong uptake in Asia-Pacific driven by industrial expansion and grid-stability needs, while North America and Europe increasingly deploy these batteries for data center backup and renewable integration. Emerging trends that define the future landscape include the integration of lead acid batteries with distributed renewable systems, a rising emphasis on sustainable circular-economy models, and market adaptation toward advanced VRLA formats tailored for electric vehicle auxiliary functions, creating a trajectory of continued innovation and strategic deployment among decision-makers and industry professionals.

AI is profoundly reshaping the Lead Acid Battery Market by optimizing manufacturing operations, elevating production quality, and enabling intelligent analytics that enhance reliability and cost efficiency. In battery factories, AI models enhance predictive maintenance by identifying equipment degradation early and scheduling timely servicing, thereby reducing unplanned downtime. AI-driven diagnostics detect cell defects with near-perfect accuracy and improve coating processes—boosting yield and throughput. Through comprehensive data analysis, AI tools can predict battery lifespan with substantially greater precision, dynamically optimize charging protocols to extend functional life, and enable real-time monitoring of battery health, thereby improving operational safety and performance. In manufacturing contexts, AI systems reduce energy waste, refining resource utilization during startups and production runs. Furthermore, AI aids in the material and design front, accelerating the identification of superior electrode materials and improving electrode conductivity and cycle stability. By integrating intelligent analytics within battery management systems, the Lead Acid Battery Market benefits from enhanced predictive capability, extended life cycles, reduced production costs, and increased sustainability, strongly appealing to strategic decision-makers seeking to harness cutting-edge technology for operational excellence and competitive advantage.

“In 2025, leading AI implementations in battery manufacturing have reduced production downtime by 25%, increased defect detection accuracy to 98%, and extended battery life by optimizing charging protocols—resulting in measurable improvements in efficiency and performance within Lead Acid Battery production facilities.”

The Lead Acid Battery Market is characterized by consistent demand across automotive, industrial, telecommunications, and renewable storage sectors, influenced by both technological advancements and evolving regulatory landscapes. The market dynamics are shaped by steady adoption of advanced valve-regulated technologies, increasing investment in recycling infrastructure, and growing demand for dependable backup power solutions in data centers and critical facilities. Environmental regulations surrounding lead handling and disposal continue to influence production practices, while manufacturers focus on enhancing efficiency, cycle life, and safety. Regional consumption patterns highlight Asia-Pacific as the largest consumer, while North America and Europe prioritize modernization and sustainable integration. Emerging dynamics such as AI-enabled predictive analytics, grid energy storage applications, and hybrid usage with renewable systems are positioning the Lead Acid Battery Market for sustained relevance despite competition from newer chemistries.

The Lead Acid Battery Market is experiencing growth driven by the increasing reliance on energy storage solutions for automotive, industrial, and backup power applications. In the automotive sector, lead acid batteries remain indispensable for starting, lighting, and ignition functions, with over 1.3 billion vehicles globally still dependent on these systems. Industrial demand is further amplified by the use of lead acid batteries in forklifts, telecom towers, and uninterruptible power supply (UPS) systems. The market also benefits from the integration of advanced Absorbent Glass Mat (AGM) and gel batteries, which extend operational life and meet the rising performance requirements of commercial fleets and industrial machinery. These factors collectively reinforce lead acid batteries as a reliable and cost-efficient energy storage choice across multiple industries.

The Lead Acid Battery Market faces limitations due to increasingly strict environmental regulations targeting lead extraction, recycling, and disposal practices. Lead is a hazardous material, and improper handling poses risks to both human health and ecosystems. Governments worldwide are imposing stringent compliance standards, mandating closed-loop recycling systems and stricter emission controls in production facilities. While these measures improve sustainability, they also elevate compliance costs for manufacturers, particularly small and mid-sized enterprises. In regions where recycling infrastructure is underdeveloped, the regulatory burden hampers market expansion, as companies must invest heavily in environmentally safe practices. This restraint creates operational challenges while pushing the industry toward sustainable but cost-intensive innovation.

A significant opportunity in the Lead Acid Battery Market lies in its integration with renewable energy projects, particularly solar and wind installations. Lead acid batteries provide a stable and cost-effective storage solution for off-grid and microgrid applications, supporting energy access in remote and rural areas. Recent developments in deep-cycle and advanced VRLA technologies enhance their suitability for long-duration discharge, enabling better alignment with renewable generation patterns. With renewable energy capacity projected to exceed 4,500 GW globally by 2030, demand for dependable storage solutions is expected to increase. This creates avenues for lead acid batteries to complement renewable adoption, offering scalability and immediate availability in emerging energy markets.

One of the key challenges for the Lead Acid Battery Market is the growing competition from lithium-ion technologies, which offer higher energy density, longer cycle life, and faster charging capabilities. Lithium-ion adoption has accelerated in electric vehicles, consumer electronics, and grid storage applications, creating pressure on lead acid battery manufacturers to innovate. While lead acid remains cost-effective and widely available, its lower energy density and higher weight make it less competitive in sectors prioritizing compactness and high performance. Additionally, investment flows are increasingly directed toward lithium-ion supply chains, limiting financial support for lead acid innovation. This competition challenges the long-term positioning of lead acid batteries, requiring strategic adaptation and focus on niche, high-reliability applications.

• Adoption of Advanced VRLA and AGM Designs: The Lead Acid Battery Market is witnessing accelerated uptake of valve-regulated lead acid (VRLA) and absorbent glass mat (AGM) designs due to their superior safety and maintenance-free operation. AGM batteries are particularly gaining traction in data centers and renewable energy storage applications, where reliability and long cycle life are critical. These batteries deliver improved deep discharge capabilities, enhanced resistance to vibration, and longer service intervals compared to conventional flooded designs, making them a preferred choice for mission-critical operations.

• Increased Investment in Recycling Infrastructure: A measurable trend reshaping the Lead Acid Battery Market is the surge in investments directed at recycling and closed-loop lead recovery systems. With global recycling rates already exceeding 95%, industry leaders are expanding capacities to reduce reliance on virgin raw materials and strengthen sustainable supply chains. Regions such as North America and Asia are introducing advanced smelting technologies and environmentally compliant facilities that not only recover lead but also optimize plastics and electrolytes, ensuring minimal waste and reducing environmental impact.

• Integration with Renewable Energy Storage: The demand for renewable energy integration is pushing lead acid batteries into new growth avenues. Deep-cycle lead acid batteries are increasingly used in solar-powered off-grid and hybrid systems, offering a cost-effective solution for long-duration storage. Their ability to withstand extreme temperatures and provide stable power output is proving advantageous in rural electrification projects and remote industrial applications. This measurable rise in deployment is especially prominent in Asia-Pacific, where renewable energy capacity is expanding rapidly to meet sustainability targets.

• Technological Automation in Battery Manufacturing: Automation and digitalization are becoming vital in the Lead Acid Battery Market as companies incorporate robotics, AI-driven inspection systems, and IoT-enabled monitoring. Automated production lines reduce defect rates, improve uniformity in electrode coating, and increase throughput. These advancements are enabling manufacturers to achieve better energy efficiency during production while reducing labor dependency. As modular and prefabricated construction grows in industrialized regions, the demand for high-precision and automated manufacturing of batteries is aligning closely with evolving industrial efficiency requirements.

The Lead Acid Battery Market is segmented into types, applications, and end-user categories, each reflecting distinct growth drivers and market dynamics. By type, the industry covers flooded, VRLA, AGM, and gel batteries, with each addressing specific performance needs across sectors. Application segmentation spans automotive, industrial backup, telecommunications, renewable energy storage, and data centers, highlighting both mature and emerging areas of demand. End-user insights reveal that automotive and industrial users dominate consumption, while sectors like renewable energy and IT infrastructure are emerging as high-potential segments due to changing technology landscapes. The segmentation reflects a balance of long-established markets and fast-evolving niches that will shape the industry’s trajectory in the coming years.

Flooded lead acid batteries continue to hold a leading position in the Lead Acid Battery Market owing to their widespread usage in automotive starting, lighting, and ignition functions, supported by decades of proven reliability and cost efficiency. They remain the preferred choice for traditional vehicles, agricultural equipment, and heavy-duty machinery where low upfront cost is critical. Valve-regulated lead acid (VRLA) batteries, especially AGM designs, are the fastest-growing type due to their maintenance-free operation, higher cycle life, and suitability for data centers, telecom towers, and renewable energy storage projects. Gel batteries also hold a significant place in niche applications that require deep discharge and stability in extreme conditions, such as medical equipment and off-grid power systems. Collectively, the diversification of product types ensures that the market meets the diverse demands of different industries, with VRLA and AGM technologies expected to gain further traction in advanced storage and mission-critical applications.

The automotive sector dominates the Lead Acid Battery Market as these batteries remain indispensable for starting, lighting, and ignition functions across over a billion vehicles in operation worldwide. Despite the rise of electric vehicles, lead acid batteries are still required for auxiliary power and backup in hybrid and EV models, ensuring continued relevance. The fastest-growing application segment is renewable energy storage, where deep-cycle batteries are increasingly deployed in off-grid solar and hybrid systems. Telecommunications represent another major application, where consistent power supply for towers and base stations drives steady demand. Industrial backup power and uninterruptible power supply (UPS) systems also contribute significantly, especially in manufacturing, data centers, and healthcare facilities. Together, these applications highlight the adaptability of lead acid batteries, with traditional sectors maintaining stability while emerging applications expand at a rapid pace.

Automotive remains the leading end-user segment in the Lead Acid Battery Market, driven by widespread reliance on lead acid batteries in passenger cars, commercial vehicles, and heavy equipment. With global vehicle production exceeding 90 million annually, this segment ensures continuous large-scale demand. The fastest-growing end-user is the renewable energy sector, where lead acid batteries support rural electrification, solar hybrid projects, and microgrid installations, particularly in emerging economies. Telecommunications and IT infrastructure also represent vital contributors, as data centers and telecom towers require reliable backup power for uninterrupted operations. Industrial and manufacturing enterprises rely heavily on forklifts, heavy-duty equipment, and UPS systems, sustaining consistent demand across regions. This diverse end-user landscape reinforces the durability of the lead acid battery industry, with growth opportunities emerging in sectors adapting to digital transformation and renewable energy expansion.

Asia-Pacific accounted for the largest market share at 48% in 2024 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 4.6% between 2025 and 2032.

The Lead Acid Battery Market across Asia-Pacific is supported by robust automotive production, rapid industrialization, and growing renewable integration projects in China, India, and Japan. North America and Europe continue to demonstrate steady demand, driven by strong adoption in data centers, telecom, and UPS systems, while South America is witnessing increasing demand in Brazil and Argentina due to infrastructure expansion. The Middle East & Africa is poised for accelerated growth, supported by infrastructure modernization, construction projects, and government investments in renewable energy. These regional patterns emphasize the global scale of opportunities, where each market displays unique dynamics shaped by industrial demand, regulatory frameworks, and technological advancements.

Expansion of Energy Storage for Data-Driven Industries

North America holds a market share of nearly 20% in the global Lead Acid Battery Market, underpinned by significant demand from the automotive, telecom, and industrial backup sectors. The region’s extensive network of data centers, particularly in the United States, fuels the requirement for high-capacity uninterruptible power supply (UPS) systems. Regulatory support promoting recycling and sustainability has strengthened compliance standards, with over 95% recycling rates achieved for lead acid batteries. Additionally, digital transformation in manufacturing and advancements in AI-enabled production facilities are reshaping operations, driving efficiency and reducing defect rates. The integration of advanced VRLA and AGM batteries is also gaining momentum, enhancing reliability in mission-critical applications.

Accelerating Transition Toward Sustainable Energy Storage

Europe accounts for approximately 18% of the Lead Acid Battery Market, with Germany, the UK, and France being the primary contributors. Demand is strongly influenced by the region’s automotive sector, industrial automation, and growing renewable installations. Regulatory frameworks from bodies such as the European Commission emphasize sustainability, circular economy practices, and strict lead recycling compliance. The market is witnessing increased deployment of AGM and gel batteries for renewable and telecom applications due to their enhanced reliability. Technological adoption is driven by innovations in electrode materials and automation in production, positioning the region as a leader in sustainable battery solutions tailored for long-term performance and environmental compliance.

High-Volume Manufacturing and Rapid Renewable Integration

Asia-Pacific dominates the global Lead Acid Battery Market with nearly 48% share, led by China, India, and Japan as top consumers. China remains the manufacturing hub, with large-scale facilities producing batteries for automotive, industrial, and renewable applications. India’s rising telecom infrastructure and government-backed electrification projects further drive regional demand, while Japan continues to focus on advanced VRLA and AGM adoption for automotive and grid applications. The region’s industrial growth and expansion of renewable energy capacity have boosted the deployment of deep-cycle lead acid batteries. Technology-driven hubs are investing in AI-based quality control and precision automation to enhance efficiency, supporting Asia-Pacific’s stronghold as the largest contributor to the global market.

Growing Demand from Automotive and Infrastructure Development

South America represents around 7% of the Lead Acid Battery Market, with Brazil and Argentina driving the majority of demand. The automotive industry remains the leading end-user, supported by a growing fleet of vehicles requiring starting, lighting, and ignition batteries. Infrastructure development, including telecom expansion and power backup systems for industrial facilities, further supports adoption. Government policies encouraging localized manufacturing and favorable trade frameworks are helping to stabilize the supply chain. Investments in renewable energy projects, particularly solar, are also contributing to rising demand for deep-cycle lead acid batteries across the region.

Infrastructure Expansion and Diversification of Energy Storage Solutions

The Middle East & Africa holds nearly 7% of the global Lead Acid Battery Market, with the UAE, Saudi Arabia, and South Africa driving demand. The region’s oil & gas sector, combined with large-scale construction and infrastructure projects, creates steady requirements for reliable backup power systems. Government initiatives supporting renewable adoption, particularly solar power in the Gulf states, have accelerated the deployment of VRLA batteries in off-grid and hybrid energy systems. Local regulations are increasingly aligning with international recycling standards, promoting sustainability. Technological modernization and trade partnerships with Asian and European suppliers are further strengthening the region’s position as a fast-emerging market.

China: 32% market share | Dominance driven by large-scale production capacity, extensive automotive manufacturing, and rapid renewable energy integration.

United States: 15% market share | Strong end-user demand from automotive, telecom, and data center industries, supported by advanced recycling infrastructure.

The Lead Acid Battery Market is characterized by a highly competitive landscape, with more than 40 prominent global and regional players actively shaping industry dynamics. Competition is defined by a mix of established multinational corporations and agile regional manufacturers, each leveraging unique capabilities in production capacity, cost efficiency, and technology adoption. Market leaders are focused on expanding their product portfolios to include advanced AGM and VRLA batteries designed for high-performance applications in automotive, telecommunications, and renewable energy storage. Strategic initiatives such as cross-border partnerships, supply chain collaborations, and acquisitions are increasingly common, allowing companies to strengthen global reach and enhance sustainability compliance. Product innovation trends, including integration of AI-enabled diagnostics, improved recycling processes, and next-generation electrode designs, are further intensifying competition. With environmental regulations tightening, companies are differentiating themselves through eco-friendly manufacturing, higher recyclability rates, and compliance-driven innovations. The competitive environment is also shaped by regional production hubs in Asia-Pacific, with Chinese and Indian manufacturers driving large-scale supply, while North America and Europe focus on technological modernization and sustainable practices. Collectively, these factors underscore a dynamic and evolving market where competition is not only based on cost but also on innovation, efficiency, and long-term strategic positioning.

Exide Technologies

GS Yuasa Corporation

EnerSys

East Penn Manufacturing

Amara Raja Batteries Limited

Johnson Controls International

Clarios

HBL Power Systems Limited

Leoch International Technology Limited

FIAMM Energy Technology SpA

Technological progress in the Lead Acid Battery Market is accelerating, driven by innovations that advance performance, durability, efficiency, and sustainability. One pivotal development is the UltraBattery, which integrates ultracapacitor functionality into a lead-acid cell via thin carbon layers on the negative plate. This hybrid design excels in partial state of charge (pSoC) operations, significantly extending cycle life by minimizing sulfation and enabling sustained performance under fluctuating charge conditions. Carbon additives and modified lead-alloy compositions are likewise transforming electrode behavior. Incorporating carbon-based materials—such as carbon nanotubes or graphene—enhances conductivity and energy storage capacity, while optimized lead alloys improve charge acceptance and reduce internal resistance, yielding superior performance in demanding applications.

Enhanced electrode architecture, including refined surface area and conductivity optimization, is bolstering both energy density and charging speed. Charging innovations such as pulse charging techniques and fast-charging protocols are modernizing lead-acid battery performance, enabling quicker top-up cycles in high-demand settings. At the frontier of diagnostics, operando neutron radiography now enables real-time visualization of electrochemical processes within lead-acid cells during cycling. This emerging imaging approach offers invaluable insights into electrode degradation and electrolyte behavior, informing design improvements and predictive maintenance strategies.

Collectively, these technological advances are reinforcing the relevance of lead-acid batteries. They enhance usability in energy storage, backup systems, telecommunications, automotive auxiliary power, and renewable grid support. Decision-makers benefit from longer service intervals, reduced maintenance, improved energy efficiency, and strengthened sustainability profiles—ensuring that lead-acid technology remains a strategic asset even as the energy storage landscape continues to evolve.

• In March 2024, research from KAIST unveiled a hybrid sodium-ion fuel cell achieving 247 Wh/kg energy density, delivering power up to 34,748 W/kg, charging within seconds and maintaining stability over 5,000 cycles—positioning it as a next-generation alternative influencing lead-acid battery competitive strategy.

• In mid-2024, a breakthrough emerged with “water batteries” featuring water-based electrolytes enhanced with inorganic salts and a bismuth-coated zinc anode that sustains 80 % capacity after 700 cycles—offering a safer, fully recyclable, and cost-effective energy storage option that may redefine environmental benchmarks.

• In 2023, the U.S. Department of Energy’s Earthshots program launched a comprehensive assessment of lead-acid chemistry’s future, focusing on extending cycle life and improving energy density through innovative modifications—highlighting research commitment to enhancing legacy technologies.

• In 2025, a major supply-chain disruption struck the industry as antimony prices soared above $60,000/metric ton—over four times prior levels—due to China’s export restrictions, prompting battery makers to explore domestic processing and recycling strategies to protect high-purity alloy supply.

The Lead Acid Battery Market Report offers comprehensive coverage across product types, applications, geographies, technologies, and emerging segments. It evaluates all principal battery formats—flooded, VRLA, AGM, gel, and advanced hybrids—highlighting nuanced differences in functionality, maintenance profile, and industrial suitability. Applications span automotive starting and ignition, motive industrial machinery, stationary backup, telecommunications, data centers, renewable energy storage, and emerging microgrid deployments. End-user insights reflect distinct demands from automotive manufacturers, telecom service providers, data center operators, industrial logistics firms, and rural electrification ventures. Geographic analysis includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa—offering volume and share data that reveal regional strengths, infrastructure trends, regulatory landscapes, and innovation hubs. Specific attention is given to Asia-Pacific’s manufacturing leadership and renewable integration, Europe’s sustainability and circular-economy initiatives, North America’s data center and recycling investments, Latin America’s infrastructure growth, and Middle East & Africa’s energy diversification and construction demand.

Technological focus areas include electrode and chemistry enhancements (e.g., carbon additives, modified alloys), hybrid cell innovations like UltraBattery, advanced charging protocols, and diagnostic advancements such as neutron radiography and AI-enabled battery management tools. The report also addresses emerging segments, such as hybrid energy storage systems, deep-cycle solar applications, and microgrid integrations. By combining breadth with targeted insights, the report empowers business leaders and industry professionals to navigate legacy and frontier market dynamics, align strategies with evolving performance expectations, regulatory shifts, and technological disruptions—without reiterating previously covered specifics—thus offering a cohesive framework to guide investment, innovation, and market positioning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 57158.64 Million |

|

Market Revenue in 2032 |

USD 72971.15 Million |

|

CAGR (2025 - 2032) |

3.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Exide Technologies, GS Yuasa Corporation, EnerSys, East Penn Manufacturing, Amara Raja Batteries Limited, Johnson Controls International, Clarios, HBL Power Systems Limited, Leoch International Technology Limited, FIAMM Energy Technology SpA |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |