Reports

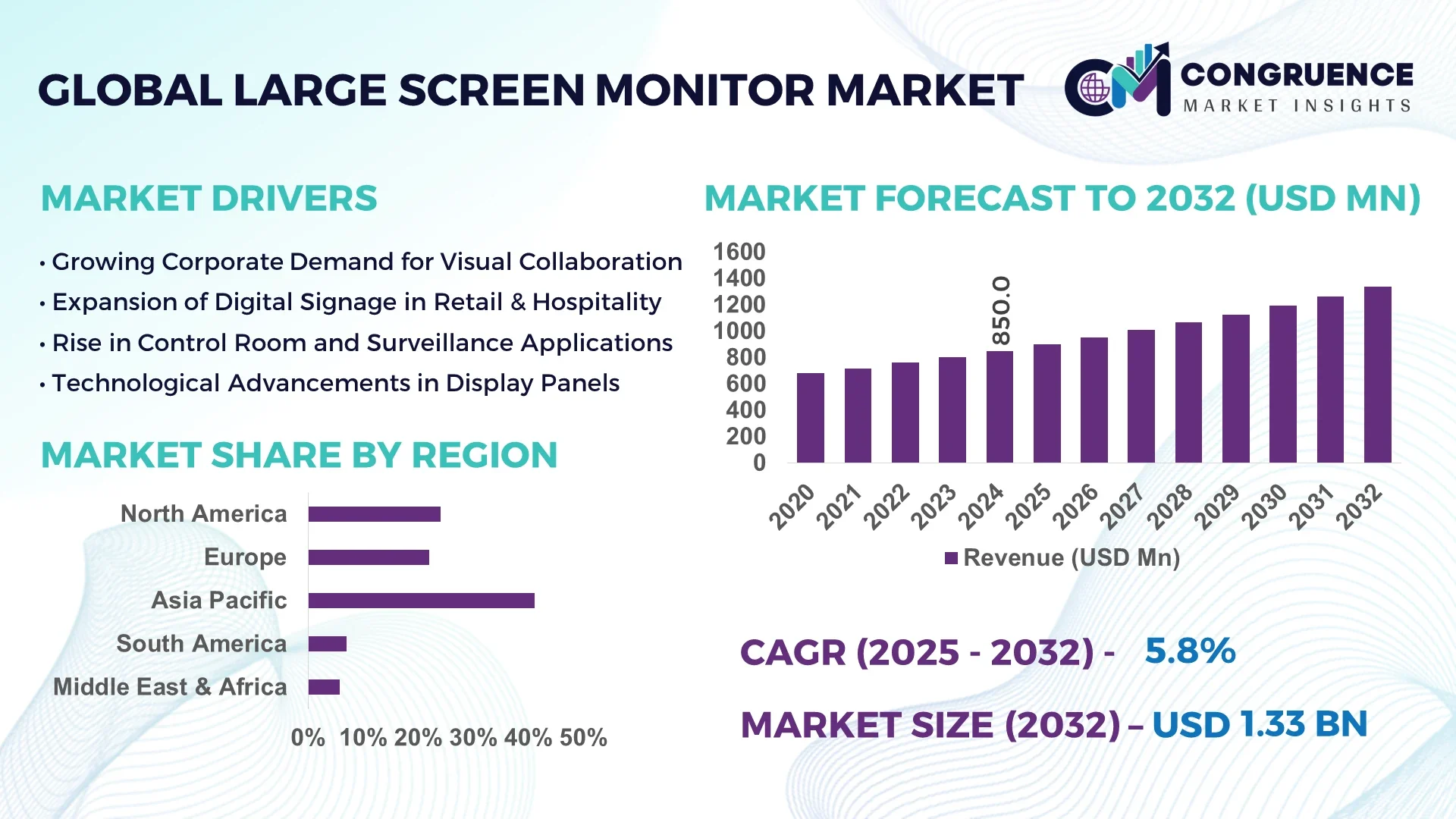

The Global Large Screen Monitor Market was valued at USD 850.0 Million in 2024 and is anticipated to reach a value of USD 1,334.5 Million by 2032 expanding at a CAGR of 5.8% between 2025 and 2032.

China leads production capacity in the Large Screen Monitor Market, operating over 50 manufacturing plants with annual output exceeding 20 million square feet of display panels. Substantial investment—over USD 400 million in 2023 alone—has been dedicated to advanced OLED and mini-LED lines. The country supports high-demand applications in control centers, broadcast studios, and corporate conferencing, while its R&D labs focus on quantum-dot enhancement and ultra-thin glass technologies.

Globally, the Large Screen Monitor Market is segmented across broadcast and media, command and control, corporate conferencing, entertainment venues, and education. Broadcast and media systems contribute approximately 25% of units, requiring 4K and 8K resolution standards. Recent innovations include touch-integrated 120‑inch panels and curved video walls that auto-calibrate to ambient lighting. Regulatory drivers include energy-efficiency mandates such as the EU’s EcoDesign standards, pushing vendors to reduce power draw by 15% year‑on‑year. Economic factors—like increased remote-work spending—are redirecting demand toward large, ultra-high-definition displays in home offices and telepresence rooms. Regional consumption is accelerating fastest in Southeast Asia, where annual growth in installation projects has surpassed 12% due to urban infrastructure upgrades. Emerging trends show a pivot to interactive AI-powered conferencing screens that integrate video analytics and gesture recognition—market outlook for 2025–2026 remains robust with strong pipeline investments in hybrid-work technologies.

AI is rapidly reshaping the Large Screen Monitor Market by enhancing operational efficiency, content management, and user interactivity. Intelligent display controllers now dynamically adjust brightness and color balance based on real‑time ambient sensing, reducing calibration time by up to 40%. In corporate environments, AI-driven conferencing monitors can detect participants, automatically frame speakers, and optimize video layouts—resulting in a 30% improvement in meeting setup speed. Control‑room displays leverage AI to prioritize alerts, highlighting critical security or network events, and lowering operator response time by an average of 25%.

Content management systems (CMS) integrated with AI enable large screen video walls to auto-schedule ads, announcements, or emergency alerts depending on audience analytics. Some systems deploy machine vision to count viewers and tailor content by demographic—improving engagement metrics by 15–20%. In manufacturing and logistics, AI-powered error-detection overlays on diagnostic monitors have reduced inspection times by nearly 35%, thanks to real-time anomaly recognition.

These advancements foster a shift from static display infrastructure to smart, adaptive visual ecosystems. The Large Screen Monitor Market now includes embedded AI modules for edge processing, allowing firmware updates capable of adding new machine-learning models. Vendors are investing heavily in low-latency neural‑processing units (NPUs) integrated with display controllers to support AI tasks locally—minimizing cloud dependency and improving data privacy.

AI also enhances lifecycle management: predictive failure analysis on large screen panels identifies potential faults—such as backlight degradation or driver chip aging—before they affect uptime. This capability increases overall operational uptime by roughly 18%, reducing maintenance costs and improving ROI for enterprises deploying large-scale displays. This transition illustrates a clear pivot in the Large Screen Monitor Market: from hardware-first to software-enabled, performance-optimized smart display platforms.

“In 2024, a major Korean display manufacturer deployed AI‑based calibration across its 75‑inch panels, reducing color‑uniformity variance from ±3 ΔE to ±0.5 ΔE—cutting calibration time per unit from 45 minutes to under 12.”

The Large Screen Monitor Market Dynamics encompass supply‑chain pressures, standardization of display formats, rising demand for hybrid‑office spaces, and sustainability mandates. As raw‑material costs (e.g., rare earths, specialty glass) fluctuate, suppliers and manufacturers negotiate layered contracts to lock pricing and ensure production stability. Format convergence—such as ultra-wide OLED panels—drives new industry standards, encouraging interoperability across control‑room and digital signage systems. Decision‑makers must balance these dynamics while deploying solutions tailored to regional energy‑efficiency regulations, particularly in North America and the EU.

The surge in hybrid-working models has created strong demand in the Large Screen Monitor Market for immersive conferencing displays ranging from 65 to 100 inches with integrated touch and camera arrays. In 2024, global procurement of such systems increased by more than 28% compared to 2022, based on supplier shipments. These large-format monitors enable multi-camera view switching and real-time whiteboarding, improving remote-team collaboration and accelerating deployment cycles by an average of 22%. Corporate decision-makers are allocating larger portions of IT budgets to retrofit executive boardrooms with these intelligent display solutions, thus directly boosting market volume with higher-spec, premium units.

In regions including parts of Africa, Southeast Asia, and Latin America, persistent infrastructure limitations—such as unreliable power grids and limited internet bandwidth—are constraining deployment of sophisticated Large Screen Monitor Market solutions. Approximately 35% of rural and semi-urban installation projects in 2024 encountered delays or system downgrades due to voltage instability and intermittent connectivity. These challenges forced suppliers to ship lower-brightness models and forgo AI-integrated firmware features, thereby compressing average selling prices by an estimated 10–15%. Such constraints hinder pilots for advanced displays and reduce economies of scale for manufacturers seeking to expand into these territories.

Emerging energy-recovery technologies—such as heat-to-power modules attached to large LED-backlit panels—offer untapped optimization opportunities in the Large Screen Monitor Market. In 2025, early-stage pilot installations in Scandinavian public venues captured excess heat from display units, converting it to a small amount of thermal energy for HVAC pre‑conditioning. These pilots demonstrated up to 12 W of recovered heat per display unit, cutting venue heating loads by 3–5%. Decision-makers in government and large commercial venues are now exploring scalable rollouts, seeking to differentiate on sustainability while leveraging display infrastructure as energy efficiency assets.

New regulations governing coatings and solder used in large‑format panels—such as the EU’s Restriction of Hazardous Substances (RoHS) revision 3—impose stricter limits on lead, hexavalent chromium, and certain per‑fluorinated compounds. Suppliers in the Large Screen Monitor Market now must certify full-panel supply chains, often requiring an additional 6–9 months of testing per batch. This has extended product introduction timelines by approximately 20% and increased batch-level testing costs by up to USD 55,000. Compliance also requires traceability measures across metal suppliers, affecting lead times and reducing flexibility for rapid production scaling.

Expansion of Modular Construction Integration: The adoption of modular and prefabricated construction techniques has increased procurement of factory-configured, high-precision Large Screen Monitor Market systems. Manufacturers are now supplying pre-bent, integrated display assemblies compatible with off‑site production lines. In North America and Europe, installation cycles for control-room and command-center projects have accelerated by 30%, reducing on-site labor hours by 25%. Demand for customizable bezel-free panels—ranging from 75 to 110 inches—has grown by over 40% year-on-year.

Shift toward Interactive Video-Wall Analytics: Large Screen Monitor Market solutions increasingly include embedded analytics: video walls can now detect foot traffic and estimate crowd size with ±5% accuracy. Retail and transportation hubs report 18% higher dwell-time interactions as displays showcase dynamic content aligned with consumer behavior. Manufacturers are adding local AI modules capable of 60–120 fps video processing, improving responsiveness in real-time environments.

Surge in Regulatory-Efficient Panel Designs: With environmental regulations tightening, vendors are releasing next-gen display models using 30% less power through adaptive backlighting and duty-cycle dimming. Over 60,000 units deployed in public-sector projects in 2024 demonstrated a 22% decrease in average power consumption during operational hours. This shift supports decision-makers managing carbon budgets and energy costs.

Proliferation of Embedded Touch & AI Conferencing Solutions: In the Large Screen Monitor Market, demand for touch-enabled displays with integrated AI camera systems grew by 35% in corporate deployments between 2023 and 2024. These solutions offer auto-framing, voice-activity detection, and real-time transcription overlays. Enterprises adopting such systems report up to 28% faster meeting starts and 32% higher user engagement during hybrid sessions.

The Large Screen Monitor Market is segmented by type, application, and end-user categories, reflecting diverse demand drivers and operational requirements across global industries. Product types vary from LCD and OLED to MicroLED and laser-based panels, catering to resolution, brightness, and energy-efficiency needs. Application-wise, displays are utilized in control rooms, corporate conferencing, digital signage, broadcast environments, and education, with differentiated adoption patterns shaped by project scale and technology compatibility. In terms of end-users, sectors such as corporate enterprises, government agencies, educational institutions, and commercial venues define procurement volume and innovation focus. Market trends indicate increasing demand for interactive and AI-enabled formats across all segments, driven by digital transformation, remote collaboration needs, and enhanced visual performance standards. These segmentation dimensions enable decision-makers to assess product positioning strategies, application-specific integration requirements, and end-user behavior, ultimately guiding both manufacturing priorities and channel expansion strategies.

In the Large Screen Monitor Market, LCD remains the dominant product type due to its mature supply chain, affordability, and wide availability in sizes ranging from 65 to 120 inches. The adoption of LCD-based large monitors continues in government control rooms, educational setups, and transportation hubs where high reliability and moderate cost are critical. OLED displays are the fastest-growing type, fueled by their superior contrast, deep blacks, and thin form factors ideal for premium conferencing rooms and high-end retail environments. Manufacturers are investing heavily in flexible OLED production lines to meet rising demand for curved and ultra-thin installations.

MicroLED technology, while still nascent, is gaining traction in large-format commercial installations thanks to its energy efficiency, high brightness, and long lifespan, making it ideal for outdoor or high-ambient-light environments. Laser-based panels, though niche, are emerging in immersive environments like simulation training and high-fidelity media production, offering superior color accuracy and longevity. These diverse product types are enabling tailored solutions across a broad array of commercial and institutional projects.

The most prominent application of large screen monitors is in control rooms, where multi-screen environments demand seamless video wall displays with high brightness, real-time data rendering, and long operational lifespans. These use cases include traffic management centers, utilities, and defense installations requiring continuous uptime and rapid data visualization. Corporate conferencing is the fastest-growing application, supported by increasing hybrid work adoption and the need for intelligent displays with built-in AI features, such as auto-framing, participant tracking, and voice-based control.

Digital signage remains a key application in retail, hospitality, and transportation, especially for dynamic content delivery and audience engagement. Educational institutions are also expanding deployment of interactive large screen panels, particularly in lecture halls and virtual learning studios. Meanwhile, broadcast and studio production facilities continue to use ultra-high-resolution displays for real-time content previewing and editing. As AI and edge-computing become integral, large screen applications are evolving to deliver not just passive content but immersive, interactive, and adaptive experiences across various operational settings.

Corporate enterprises represent the leading end-user segment in the Large Screen Monitor Market, with ongoing investments in high-specification conference room solutions, virtual collaboration suites, and digital lobbies. These deployments support remote and hybrid workforces, with many firms standardizing on 4K or higher resolutions and integrating multi-platform conferencing systems. Government agencies are the fastest-growing end-user group, driven by large-scale infrastructure upgrades and smart-city control initiatives that require durable, high-performance visual displays in command and control centers.

Educational institutions continue to expand adoption, especially universities and technical schools, where large screen monitors are central to blended learning environments and real-time student engagement. Commercial venues such as airports, hotels, and entertainment centers are deploying large-format displays to enhance customer experiences and provide real-time information. Additionally, the healthcare sector is beginning to adopt large screen monitors for telemedicine conferencing and advanced visualization in training rooms. Together, these end-user groups are shaping market demand based on their evolving digital transformation strategies and specialized operational needs.

Asia-Pacific accounted for the largest market share at 41.2% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2025 and 2032.

Asia-Pacific's dominance stems from the concentration of manufacturing facilities, large-scale public infrastructure investments, and widespread deployment across smart cities and education sectors. China, Japan, and India are central to both consumption and production, with rapid digitalization accelerating panel deployment across all major verticals. Meanwhile, North America is expected to see robust expansion, driven by strong demand for enterprise conferencing systems, digital signage upgrades in transportation hubs, and AI-integrated control-room applications. Factors such as rapid enterprise tech adoption, government investments in digital infrastructure, and advancements in display integration with cloud-based platforms are propelling North America’s upward trajectory in the Large Screen Monitor Market. Regional market variations are further shaped by regulatory environments, localized technology demand, and varying levels of economic stimulus for digitization projects.

North America held approximately 26.3% of the global Large Screen Monitor Market share in 2024, driven by high corporate investment in hybrid work solutions and advanced conferencing displays. Major industries boosting demand include finance, defense, healthcare, and education, all of which are rapidly modernizing command centers and collaborative spaces. The U.S. government’s digital modernization programs and infrastructure spending bills have provided strategic support for tech upgrades in federal buildings and public services. Notably, AI-integrated large screens are being adopted in security and surveillance centers, offering real-time analytics capabilities. Technological transformation in the region emphasizes low-latency AI displays with edge processing, touchless interaction, and voice-controlled interfaces. These innovations are improving operational efficiency across sectors, and the growing shift toward sustainable procurement is prompting adoption of energy-efficient, recyclable panel solutions in commercial installations.

Europe accounted for approximately 21.4% of the global Large Screen Monitor Market in 2024. Key countries such as Germany, the UK, and France are leading the demand for large-format displays, primarily in public transportation, smart classrooms, and corporate communication hubs. The European Commission’s green procurement mandates and the EcoDesign Directive are driving a surge in demand for energy-efficient panels. These policies are encouraging manufacturers to focus on low-emission production techniques and recyclable display technologies. The rise of smart-city projects in Germany and digital learning initiatives in France is further boosting adoption. Additionally, emerging technologies like MicroLED and AI-integrated control units are gaining traction in operational control environments and large-scale public venues. European firms are actively investing in sustainable innovations and integrating digital display infrastructures into long-term climate goals and regulatory frameworks.

Asia-Pacific leads the Large Screen Monitor Market with the highest market volume and unit deployment globally in 2024. China, Japan, and India are the top consumers, with China alone accounting for more than 50% of all regional shipments. The region benefits from high production scalability, low-cost labor, and robust domestic demand for digital display technologies across sectors like education, retail, transportation, and smart cities. In Japan, precision manufacturing supports innovation in OLED and MicroLED panels, while India’s growing education and government sectors are rapidly deploying large screens under digital literacy and smart governance initiatives. Infrastructure upgrades, coupled with heavy investment in AI-based content management systems, are fueling display adoption across Tier 1 and Tier 2 cities. Regional technology clusters in Shenzhen, Tokyo, and Bangalore are acting as innovation hubs, integrating cloud-computing, AI analytics, and 8K resolution advancements into mainstream production.

South America, led by Brazil and Argentina, contributed approximately 6.2% of the global Large Screen Monitor Market share in 2024. The demand in this region is largely infrastructure-driven, with sectors such as transportation, energy, and government services integrating large format monitors for control rooms and digital public interfaces. Brazil has implemented new tax incentives for tech modernization projects, accelerating demand in smart transportation and public information systems. Argentina, meanwhile, is deploying large-format LED monitors in urban transit hubs and government-led education initiatives. Regional trends also show increased reliance on solar-powered and battery-optimized screens for remote and rural areas. Digital transformation efforts supported by regional trade blocs are expected to facilitate easier importation of high-tech components, boosting availability and price competitiveness of advanced displays across South America.

The Middle East & Africa region is emerging as a significant player in the Large Screen Monitor Market, with strong growth driven by UAE and South Africa. In 2024, the region accounted for approximately 4.9% of global market volume. Oil & gas, construction, and public safety sectors are the main adopters, using large screens for data monitoring, surveillance, and interactive command systems. Governments are investing heavily in smart-city projects—such as Dubai’s Vision 2030—and integrating AI-powered visual systems in public infrastructure. Technological modernization is being supported by favorable trade agreements and joint ventures that facilitate the inflow of advanced panel components and software ecosystems. Regulatory frameworks are evolving to accommodate higher display energy standards and digital content governance, ensuring that new deployments align with future-ready and sustainable objectives across urban and semi-urban regions.

China – 31.7% Market Share

High production capacity, well-established manufacturing infrastructure, and wide-scale public sector deployment drive China’s leadership in the Large Screen Monitor Market.

United States – 18.6% Market Share

Strong end-user demand across corporate, defense, and public administration sectors fuels consistent large-screen display integration and innovation in the U.S. market.

The Large Screen Monitor Market features a highly competitive environment with over 70 globally active manufacturers and solution providers, ranging from display hardware producers to system integrators and software-driven interface developers. Key players maintain strong market positioning through continuous innovation in display technology, user interface design, and embedded AI capabilities. Companies are actively pursuing strategic partnerships with enterprise solution providers to deliver integrated conferencing and signage solutions tailored to hybrid work and smart infrastructure needs.

In 2023 and 2024, competition intensified with a noticeable increase in product launches of ultra-thin, bezel-less, and energy-efficient panels designed for both indoor and semi-outdoor applications. Mergers and acquisitions also reshaped the competitive landscape, with several regional players consolidating their portfolios to expand geographic reach. Display firms are increasingly differentiating through proprietary calibration software, edge-AI processing units, and touchless control innovations.

Firms are also focusing on vertical integration, bringing panel manufacturing, firmware development, and software services under one umbrella to improve efficiency and brand consistency. In parallel, investments in R&D for MicroLED, mini-LED, and quantum dot enhancements are becoming a key differentiator. Competitive dynamics remain strong, with vendors adapting to sustainability mandates, rising customer expectations for interactive content delivery, and cross-platform compatibility requirements in enterprise and government use cases.

Samsung Electronics Co., Ltd.

LG Display Co., Ltd.

Sony Corporation

Panasonic Holdings Corporation

Sharp NEC Display Solutions

BOE Technology Group Co., Ltd.

Leyard Optoelectronic Co., Ltd.

Barco NV

ViewSonic Corporation

BenQ Corporation

Hisense Visual Technology Co., Ltd.

AU Optronics Corporation

Planar Systems, Inc.

Dell Technologies Inc.

Christie Digital Systems USA, Inc.

Technological advancements are redefining the Large Screen Monitor Market with innovations focused on visual clarity, interactivity, energy efficiency, and AI integration. Recent improvements in OLED and MicroLED technologies have enabled slimmer, brighter, and more power-efficient large displays suitable for both commercial and industrial settings. MicroLED panels now offer peak brightness levels exceeding 2,000 nits, ideal for outdoor and semi-outdoor deployments in high-ambient light environments. Manufacturers are also integrating quantum-dot enhancement layers to expand color gamut and improve dynamic range.

The use of touchless gesture recognition and voice-assisted control systems has risen sharply, especially in public and healthcare applications. AI-enabled monitors are being developed with automatic color calibration, real-time anomaly detection, and adaptive brightness based on environmental sensors, optimizing energy use and user experience. AI-powered conferencing displays now feature multi-camera smart tracking and voice activity analysis, streamlining remote communication for enterprise users.

Furthermore, the incorporation of edge-processing units within display controllers is minimizing latency and dependency on cloud-based infrastructure. Interactive whiteboards with embedded natural language processing (NLP) capabilities and real-time content transcription are being adopted widely in educational institutions and corporate environments. These technology trends indicate a shift from static presentation screens to dynamic, data-rich and intelligent visual solutions, offering decision-makers a compelling mix of utility, scalability, and long-term ROI.

• In March 2024, Samsung unveiled its 140-inch MicroLED display targeting luxury residential and enterprise use, featuring modular design and over 1,600 nits of brightness, supporting ultra-low latency streaming and 120Hz refresh rates.

• In October 2023, LG introduced AI Picture Pro 3.0 in its commercial large-screen displays, improving object detection and real-time scene optimization, significantly enhancing visual accuracy for corporate installations.

• In May 2024, Barco launched its next-gen video wall controller series equipped with embedded AI that enables automated content scaling and energy usage tracking, supporting 24/7 mission-critical environments.

• In December 2023, Hisense deployed its VisionHub interactive large display across 60 corporate campuses in Asia, integrating real-time collaboration tools, digital whiteboards, and biometric login for security.

The Large Screen Monitor Market Report offers a comprehensive analysis of key segments, regional dynamics, end-user trends, and technology shifts that influence business strategies across the industry. The report covers major product types such as LCD, OLED, MicroLED, and laser-based displays, detailing their operational roles, advantages, and deployment patterns. Applications evaluated include command and control centers, corporate conferencing systems, broadcast studios, educational environments, and digital signage networks.

Geographically, the report spans all primary markets—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—with in-depth assessments of demand trends, investment activity, infrastructure development, and regulatory influence. It evaluates enterprise, government, education, and commercial sectors to provide end-user-specific insights into adoption behavior, technology preference, and customization needs.

Emerging focus areas include AI-embedded smart displays, touchless and voice-interactive technologies, and sustainable product designs. The report also highlights niche market trends such as remote collaboration suites, real-time surveillance integration, and energy recovery systems in display environments. Analysts and decision-makers will gain actionable intelligence on product innovation cycles, supply chain configurations, strategic partnerships, and evolving global standards that shape the current and future landscape of the Large Screen Monitor Market.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 850.0 Million |

| Market Revenue (2032) | USD 1,334.5 Million |

| CAGR (2025–2032) | 5.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Samsung Electronics Co., Ltd., LG Display Co., Ltd., Sony Corporation, Panasonic Holdings Corporation, Sharp NEC Display Solutions, BOE Technology Group Co., Ltd., Leyard Optoelectronic Co., Ltd., Barco NV, ViewSonic Corporation, BenQ Corporation, Hisense Visual Technology Co., Ltd., AU Optronics Corporation, Planar Systems, Inc., Dell Technologies Inc., Christie Digital Systems USA, Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |