Reports

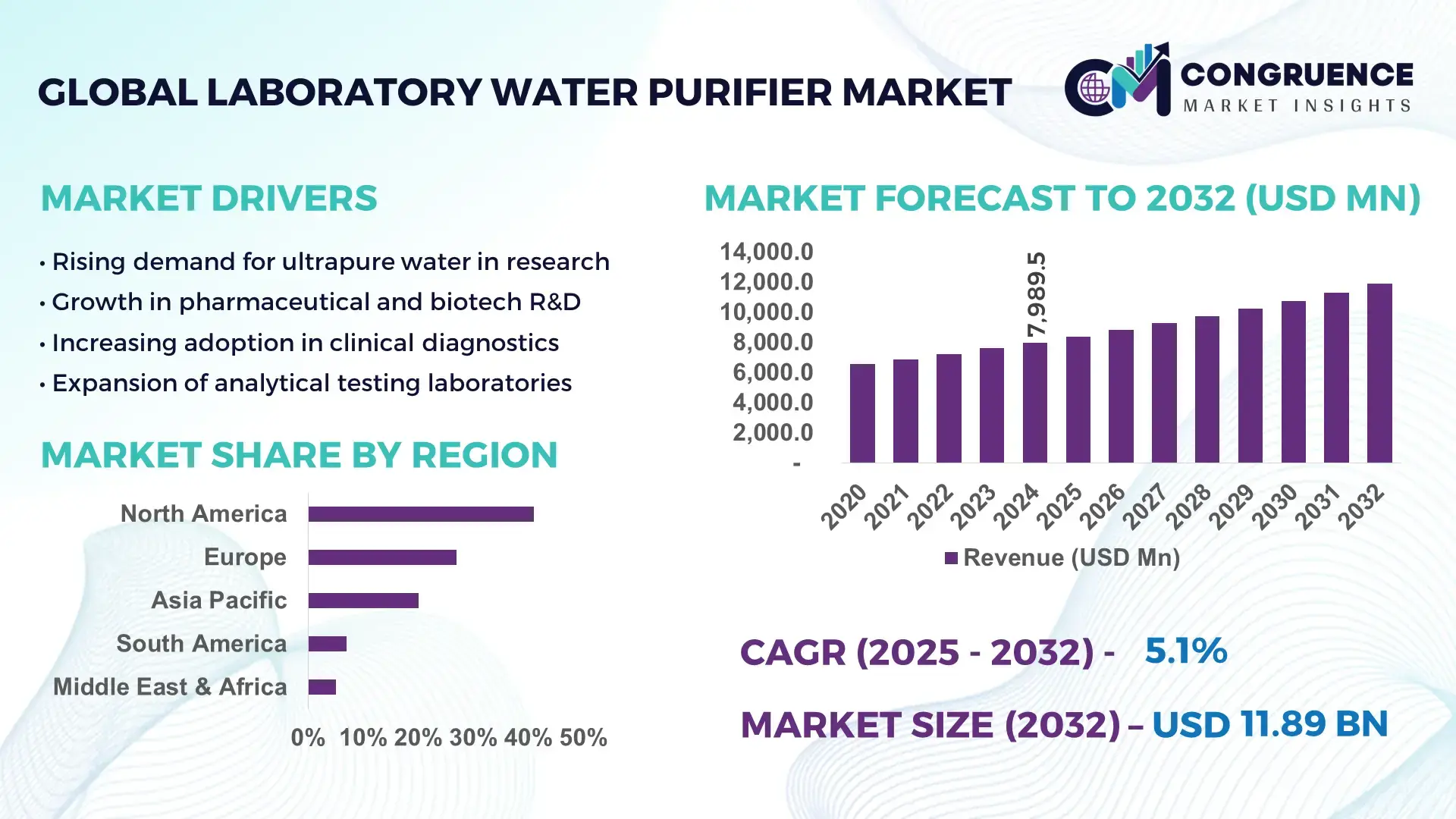

The Global Laboratory Water Purifier Market was valued at USD 7,989.5 Million in 2024 and is anticipated to reach a value of USD 11,885.3 Million by 2032 expanding at a CAGR of 5.09% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by rising demand for ultrapure water in pharmaceutical, biotech, and research laboratories globally.

In the United States — the country that currently dominates the laboratory water purifier marketplace — production capacity has scaled significantly in recent years: U.S.-based manufacturers have increased their manufacturing output by over 40 % between 2020 and 2024 to meet growing demand from pharmaceutical and clinical‑diagnostic labs. Investment levels in the U.S. exceeded USD 500 million in 2024 for expansion of purification‑system production lines and R&D into advanced purification technologies. Key industry applications in the U.S. include high‑precision analytical chemistry, cell culture, and diagnostic testing laboratories; technological advancements such as real-time water‑quality monitoring and multi‑stage reverse-osmosis + UV + deionization systems have been widely adopted, enabling consistent ultrapure water delivery even in high‑throughput environments.

Market Size & Growth: Global market at USD 7,989.5 Million in 2024, projected to reach USD 11,885.3 Million by 2032, growing at a CAGR of 5.09%, driven by increasing R&D and regulatory‑compliant water purity needs.

Top Growth Drivers: 70% adoption of ultrapure water systems in research labs, 58% increase in biotech/pharma lab installations, 32% rise in academic‑institution demand for purified water.

Short-Term Forecast: By 2028, average water purity compliance failures expected to drop by 25% and mean time between maintenance (MTBM) for purification systems to improve by 20%.

Emerging Technologies: Integration of multi‑stage RO + ultrafiltration + UV + deionization; real‑time IoT water‑quality sensors; energy‑efficient purification modules with waste‑water minimization.

Regional Leaders: North America projected at ~USD 4,500 Million by 2032 with high R&D‑lab uptake; Europe ~USD 3,200 Million by 2032 supported by pharmaceutical and academic labs; Asia‑Pacific ~USD 2,800 Million by 2032 driven by rising life‑sciences infrastructure.

Consumer/End-User Trends: Growing use by pharmaceutical companies, biotech firms, clinical diagnostic labs — increased demand for ultrapure water for molecular biology, analytics and cell‑culture processes.

Pilot or Case Example: In 2024, a major U.S. biotech firm upgraded its purification system — resulting in a 22% reduction in batch‑failure due to water contamination and a 15% decrease in system downtime.

Competitive Landscape: Market leader is Thermo Fisher Scientific (≈ 22% share), followed by Merck Millipore, Sartorius AG, ELGA LabWater, and Evoqua Water Technologies as major competitors.

Regulatory & ESG Impact: Stricter laboratory‑water purity standards, increasing regulatory compliance requirements, and growing demand for water‑waste reduction and energy‑efficient systems are influencing adoption.

Investment & Funding Patterns: Over USD 500 million recent investments in production capacity expansion and R&D in 2024; increasing use of project financing and venture funding for innovative purification technologies.

Innovation & Future Outlook: Key innovations include modular purification systems, IoT-enabled real-time monitoring, eco‑friendly and energy‑efficient designs, and scalable solutions — positioning the market for sustainable, compliance‑driven growth through 2032.

The market is also witnessing consolidation of demand across pharma, biotech, academic research, and clinical diagnostics, along with a shift toward modular, IoT-enabled, and eco‑efficient purification systems — trends expected to shape long‑term growth dynamics and drive adoption worldwide.

In addition, laboratories across industry sectors (pharmaceutical, biotech, clinical diagnostics, academic research) are increasingly demanding ultrapure and Type‑I/II water; recent innovations include compact bench‑top systems with automated purification cycles and energy‑efficient UV + RO + deionization technologies. Regulatory pressure and rising environmental sustainability requirements are encouraging adoption of water‑waste minimization and energy‑saving purifier designs, particularly in North America and Europe. Emerging trends point toward growing demand in Asia‑Pacific and increased investments in modular purification systems for decentralized labs.

The Laboratory Water Purifier Market is strategically critical as a foundational enabler of quality, reproducibility, and compliance in pharmaceuticals, clinical diagnostics, and R&D laboratories worldwide. As laboratories conduct increasingly complex analytical, molecular biology, and cell‑culture operations, ultrapure water becomes indispensable to ensure accuracy and regulatory compliance. The advent of multi‑stage purification systems combining reverse osmosis (RO), ultrafiltration, UV sterilization, and deionization delivers up to 35% improvement in contaminant removal efficiency compared to older single‑stage RO systems. While North America continues to dominate in terms of volume — driven by dense concentration of research institutions and biotech firms — Asia‑Pacific leads in adoption growth rates, with over 25% annual increase in new system installations.

By 2027, adoption of IoT‑enabled water quality monitoring is expected to improve laboratory uptime by 18% and reduce maintenance costs by 22%. Firms are simultaneously committing to ESG metrics such as 30% reduction in water waste and 25% decrease in energy consumption per purification cycle by 2030. In 2024, a major U.S. biotech company implemented predictive‑maintenance algorithms based on real-time water‑quality data that reduced system downtime by 15% and maintenance labour by 20%. Looking ahead, the Laboratory Water Purifier Market is positioned as a pillar of resilience, compliance, and sustainable growth for laboratories worldwide — serving as a critical infrastructure underpinning scientific research, pharmaceutical development, and diagnostics through continuous innovation and alignment with regulatory and environmental standards.

The Laboratory Water Purifier Market is undergoing significant transformation. With increasing globalization of pharmaceutical research, expansion of clinical diagnostic services, and rising investment in biotechnology and academic research, demand for high‑purity water is stronger than ever. Laboratories are upgrading from basic filtration to advanced multi‑stage systems ensuring ultrapure water standards, reflecting a trend toward higher precision and reliability. Simultaneously, environmental sustainability concerns and regulatory pressure are pushing manufacturers to design more efficient, low‑waste, energy‑saving purifier systems. The market is also seeing growing demand in emerging economies, particularly where expansions in research infrastructure and healthcare diagnostics are underway. This expansion is shifting the geographic balance, with Asia‑Pacific gaining traction alongside established markets in North America and Europe. As laboratories across sectors — pharmaceutical, biotech, diagnostics, academic research — demand different levels of water purity (from Type III to ultrapure Type I), market segmentation is becoming increasingly granular. In this evolving landscape, the Laboratory Water Purifier Market is being shaped by the convergence of technical innovation, regulatory compliance, and growing global demand for scientific and diagnostic quality.

The growing complexity of research, diagnostics, and drug development is driving a steep increase in the need for ultrapure water. Laboratories engaged in molecular biology, genomic analysis, HPLC, and cell‑culture applications require water free of ions, organic compounds, and microbial contaminants — and older purification methods often fail to meet such purity standards. As a result, more than 70% of research laboratories worldwide now adopt advanced water purification systems. Pharmaceutical and biotechnology sectors, in particular, have expanded their lab capacities by over 58% in the past five years, necessitating high‑capacity, reliable purification systems. This increased demand ensures consistent demand growth for modern, multi‑stage purification systems across applications including clinical diagnostics, research labs, and industrial testing.

Advanced purification systems — combining technologies such as ultrafiltration, reverse osmosis, UV sterilization, and deionization — often have high initial capital expenditure, which makes them less accessible to small and medium‑scale laboratories. Maintenance costs are also significant: filters, membranes, UV lamps, and specialized consumables (resins, cartridges) require regular replacement. Around 40% of smaller labs report cost constraints as a major barrier to upgrading to advanced purification systems. Additionally, installations demand skilled technicians to validate water purity and maintain consistent performance, which adds to overall operational complexity. These factors collectively restrain adoption among smaller labs or those with limited budgets.

Expansion of research infrastructure — especially in emerging economies — presents strong opportunity for growth as academic institutions, biotech start‑ups, and healthcare diagnostics expand. New government and private investments are creating dozens of new labs annually, many of which require water purification systems meeting stringent purity standards. Portable and modular purification systems with low maintenance needs offer a flexible, cost‑effective solution for smaller or decentralized labs. Additionally, demand for compact bench‑top purifiers is rising among small‑ to mid‑sized labs that seek reliable but space‑efficient solutions. Adoption rates in emerging markets have increased by over 25% in the past three years, signaling high growth potential.

Laboratories — especially those in pharmaceuticals, clinical diagnostics, and life‑sciences research — must comply with stringent water‑purity standards enforced by regulatory bodies. As standards evolve, purification systems must be upgraded, validated, and re‑certified, which increases cost and technical burden on laboratories. Small and mid‑sized labs may lack resources to manage such compliance processes or conduct frequent validations. Moreover, multiple regulatory frameworks across regions complicate standardization, making it difficult for global manufacturers to design universal systems. These challenges constrain rapid adoption, especially in regions with fragmented regulatory oversight or lower budgets.

Increasing adoption of automated multi‑stage purification systems: Laboratories are moving toward integrated purification solutions combining reverse osmosis, ultrafiltration, UV sterilization, and deionization. Over 60% of new system installations in 2024 incorporated these multi‑stage purification technologies, significantly improving water purity consistency and reducing failures due to contamination.

Surge in IoT‑enabled real‑time water quality monitoring systems: In 2024, around 33% of newly installed laboratory purifiers featured built‑in IoT sensor modules that monitor conductivity, resistivity, and microbial load in real time. This enhances compliance and reduces maintenance intervals by approximately 25%, while enabling predictive maintenance.

Growing demand in emerging markets and decentralized labs: Emerging economies in Asia‑Pacific and Latin America saw a 25% year-on-year increase in laboratory water purifier installations in 2024, driven by expansion in academic research, pharmaceutical manufacturing, and diagnostic labs. Demand for compact bench‑top and modular systems increased by 22%, pointing to growing decentralization of laboratory infrastructure.

Shift toward sustainable and low‑waste purification systems: Energy‑efficient purifier designs and water‑waste reduction systems gained traction: in 2024, about 30% of new products marketed themselves as “eco‑efficient,” offering water‑waste reduction of up to 30% compared to older models. This trend aligns with growing ESG (environmental, social, governance) priorities within research institutions and industrial labs.

The global Laboratory Water Purifier Market is segmented along multiple dimensions — by type (purity grade and system configuration), by application (lab processes such as chromatography, cell culture, diagnostics), and by end‑user (pharmaceutical/biotech companies, academic & research institutes, hospitals/clinical labs, industrial labs). This segmentation enables manufacturers and buyers to tailor purifier choice to specific water‑quality requirements, lab size, throughput needs, and regulatory or research standards. Variation in lab scale — from small bench‑scale academic labs to large industrial or pharmaceutical QC labs — drives demand for both compact point‑of-use purifiers and large‑capacity central systems. The segmentation reflects not only technical requirements (e.g., ultrapure vs basic purified water) but also operational needs (volume, automation, throughput), providing a structured view for decision‑makers and analysts evaluating demand across diverse lab environments.

The type segmentation of the Laboratory Water Purifier Market typically distinguishes among Type I (Ultrapure Water systems), Type II (Pure Water systems), and Type III / RO‑Water systems. According to recent industry data, Type I ultrapure water systems currently lead the market with approximately 42 % share, owing to their ability to meet the stringent water‑quality requirements of high‑precision analytical, molecular biology, and cell‑culture applications. This dominance stems from the widespread need in pharmaceutical, biotech, and research labs for water free of ions, organics, and microbial contaminants. The fastest‑growing type segment appears to be RO‑based and basic purified water systems, driven by rising demand in general laboratory operations, cleaning, autoclaving, reagent preparation, and as feed water for higher‑grade systems. Although no exact % growth is cited here, adoption of RO/purified water systems is increasing rapidly, especially in emerging labs seeking cost‑effective solutions for non‑critical applications. Other types, such as basic distilled‑water systems, deionization-only systems, or hybrid purification blends tailored for low-to-mid purity needs, account for the remaining ~23 % combined share; these serve niche or lower‑requirement laboratory functions, such as cleaning, glassware rinsing, or non‑critical testing.

Application‑based segmentation divides laboratory water purifier usage among processes such as chromatography (e.g., HPLC, ion chromatography), cell and tissue culture, clinical diagnostics / immunochemistry, autoclave and general cleaning, and other general lab functions. The leading application currently is chromatography and analytical chemistry, accounting for around 30‑35 % of use, because these techniques demand water with extremely low ionic and organic contaminants to ensure accuracy and reproducibility of results. The fastest‑growing application appears to be cell and tissue culture / molecular biology labs, driven by expanding biotech and pharmaceutical research, environmental testing, and increased use of genomic & proteomic methods. Growth in this segment reflects a global rise in biotech R&D and diagnostic capabilities. Other applications — clinical diagnostics, general lab cleaning and sterilization, reagent preparation, environmental testing — together represent a combined share of about 35‑40 %, serving routine lab operations beyond high-precision analytics. In 2024, an estimated > 60% of newly commissioned academic and research laboratories globally reported specifying ultrapure or high‑grade purified water for chromatography and molecular‑biology applications.

End‑user segmentation identifies major categories: pharmaceutical & biotechnology companies, academic & research institutes, hospitals & clinical diagnostics laboratories, and industrial / quality‑control laboratories (e.g., food, environmental, chemical, oil & gas testing labs). The leading end‑user segment is pharmaceutical & biotechnology companies, contributing roughly 38‑40 % share, driven by rigorous water purity needs for drug development, QC, analytical testing, and sterile manufacturing. The fastest‑growing end‑user segment is academic & research institutes, as increasing global investment in life‑sciences research, environmental studies, and materials science drives lab expansion. Growth here is particularly marked in emerging economies where governments are boosting funding for science and research infrastructure. Other end‑users — hospitals/clinical diagnostics and industrial / QC labs — collectively make up about 25‑30 % share, providing stable demand for both high‑purity water (for diagnostics and assays) and standard purified/RO water (for cleaning, reagent prep, routine analysis). In 2024, over 45% of new diagnostic labs worldwide adopted dedicated water‑purification systems to support immunochemistry and chromatography‑based assays.

North America accounted for the largest market share at 41 % in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2 % between 2025 and 2032.

North America’s Laboratory Water Purifier Market reached an installed base of over 18,500 systems in 2024, with the United States accounting for approximately 75 % of regional installations. The region hosts more than 3,200 pharmaceutical and biotech laboratories, while over 1,000 hospitals and clinical research centers actively upgraded water purification systems in 2024. Asia-Pacific’s expanding research infrastructure includes more than 5,400 newly commissioned laboratories across China, India, and Japan. Europe contributed 27 % to the global market, with Germany, France, and the UK leading adoption of Type I ultrapure water systems. South America and the Middle East & Africa collectively accounted for 12 % of the global share, reflecting ongoing investments in healthcare, academic research, and industrial labs. Regional dynamics are further influenced by digital monitoring, automation, and eco-efficient technology adoption.

North America holds approximately 41 % of the global Laboratory Water Purifier Market, driven by pharmaceutical, biotech, and healthcare research labs. Regulatory agencies, including the FDA and EPA, encourage high water purity standards, resulting in significant system upgrades. Key technological advancements include IoT-enabled water quality monitoring, automated multi-stage RO/UV/deionization systems, and predictive maintenance algorithms. Thermo Fisher Scientific, a major U.S. player, recently expanded its manufacturing and R&D facilities to launch modular ultrapure water systems. Enterprise adoption is highest in clinical diagnostics and pharmaceutical research, with hospitals and biotech labs integrating digital tracking to reduce downtime by 15 %. North American labs demonstrate a preference for scalable, high-throughput purification systems supporting large-volume analytical applications.

Europe accounts for roughly 27 % of the Laboratory Water Purifier Market, with Germany, the UK, and France as the leading markets. Stringent EU regulations on water purity for pharmaceutical and research applications drive consistent system upgrades. Laboratories increasingly adopt multi-stage purification systems with UV sterilization, reverse osmosis, and IoT-enabled water monitoring. Sartorius AG, a Germany-based manufacturer, has introduced modular and energy-efficient systems tailored to European research labs. Adoption patterns indicate that regulatory pressure and sustainability initiatives prompt institutions to prioritize traceability, digital integration, and water-waste reduction. European labs show higher uptake of automated systems for chromatography, molecular biology, and diagnostics applications, ensuring precise compliance with strict laboratory standards.

Asia-Pacific holds a growing market position, ranking second globally by installed volume with over 5,400 laboratory systems commissioned in 2024. China, India, and Japan are the top-consuming countries, driven by expanding biotech, pharmaceutical, and academic research infrastructure. Regional technological trends include adoption of compact bench-top ultrapure systems, modular RO + UV + deionization units, and AI-assisted predictive maintenance. Local players such as ELGA LabWater have increased production facilities to meet rising demand. Consumer behavior varies, with research institutes and private labs showing preference for cost-effective, scalable solutions, while high-end academic labs invest in IoT-enabled ultrapure water monitoring for reproducibility and compliance.

South America contributed approximately 7 % of the global Laboratory Water Purifier Market in 2024, led by Brazil and Argentina. Investments in healthcare diagnostics, academic research, and industrial laboratories drive demand for ultrapure and Type II water systems. Government incentives support laboratory modernization, while regional energy infrastructure improvements enable consistent operation of purification systems. Local players have introduced compact, low-maintenance RO and UV systems suitable for emerging labs. Regional consumer behavior indicates strong interest in multifunctional systems that combine cost efficiency with compliance, particularly in urban research centers and private clinical labs.

The Middle East & Africa region accounted for 5 % of the global Laboratory Water Purifier Market in 2024, with the UAE and South Africa as primary growth countries. Demand is concentrated in oil & gas testing, healthcare diagnostics, and research laboratories. Regional adoption trends include advanced RO + UV + deionization units, IoT-enabled monitoring, and energy-efficient designs to address water scarcity and environmental concerns. Local players are introducing modular systems suitable for decentralized lab setups. Consumer behavior varies, with institutions preferring robust, low-maintenance systems capable of high throughput and compliance with local safety and environmental standards.

United States – 32 % Market Share: Dominance driven by high production capacity, strong biotech and pharmaceutical end-user demand, and widespread regulatory enforcement of water purity standards.

China – 18 % Market Share: Driven by rapid expansion of research laboratories, government funding for life-science infrastructure, and adoption of modern purification technologies in industrial and academic settings.

The competitive environment in the global Laboratory Water Purifier Market is moderately consolidated, with a mix of dominant global manufacturers and regional niche players. Approximately 20–25 major competitors are actively operating worldwide, offering products from benchtop ultrapure water systems to large-scale central purification units. The top 5 companies — Merck KGaA, Thermo Fisher Scientific, Sartorius AG, ELGA LabWater, and Pall Corporation — together hold around 40–45 % of the global market share, focusing on high-end and premium segments.

Strategic initiatives among these leading firms include new product launches, modular and multi-stage purification systems (RO + UV + ultrafiltration + deionization), IoT-enabled water-quality monitoring, and geographic expansion into emerging markets. Innovation is a key differentiator, with companies investing in smart lab integration, real-time monitoring, low-maintenance modular systems, and energy-efficient designs. The lower-end market remains fragmented due to smaller regional players offering cost-effective RO or Type II systems. Competition is primarily driven by technology, service reliability, and regulatory compliance rather than price, positioning continuous R&D and innovation as essential for maintaining market leadership.

ELGA LabWater

Pall Corporation

Evoqua Water Technologies

Aqua Solutions, Inc.

Purite Ltd.

The laboratory water purifier market is advancing with multi-stage purification technologies combining reverse osmosis, ultrafiltration, UV sterilization, and deionization to produce ultrapure water meeting ASTM Type I / ISO 3696 standards with resistivity of 18.2 MΩ·cm and total organic carbon (TOC) levels of 2–5 ppb. Modular designs allow customization from benchtop systems producing a few liters per day to high-capacity central systems for large research or pharmaceutical labs.

Integration with digital monitoring and IoT-enabled systems enables real-time tracking of resistivity, TOC, microbial load, and flow, facilitating predictive maintenance, automated alerts, and compliance monitoring. Energy-efficient and low-waste designs address ESG concerns, appealing to institutions under regulatory pressure. Emerging technologies, including chemical-free sterilization and advanced filtration methods, are gaining interest for niche lab applications. Collectively, these technologies enhance reliability, scalability, and operational efficiency, ensuring that modern laboratories can meet stringent purity requirements across diverse scientific and industrial applications.

In June 2024, Sartorius AG introduced the Arium® Mini Extend, a compact ultrapure (Type 1) laboratory water purification system featuring a flexible dispensing arm and touchscreen interface — designed to streamline water dispensing and improve lab workflow efficiency. Source: www.sartorius.com

In mid‑2024, Thermo Fisher Scientific expanded its “Barnstead” line of lab water purification systems by promoting integrated solutions (deionization, RO, UV, and filtration) suitable across lab scales — reinforcing ease of operation, modular configuration, and broad applicability for analytical, life‑science and general lab use. Source: www.thermofisher.com

During 2023–2024, several key players accelerated deployment of multi‑stage purification systems combining reverse osmosis, ultrafiltration, UV sterilization, and cartridge‑based deionization, significantly increasing reliability and water‑quality consistency for sensitive applications like HPLC, cell culture, and molecular biology across research and pharma labs.

In 2024, there was a marked rise in adoption of compact benchtop laboratory water purifiers in small-to-mid‑scale labs, driven by growing demand in academic, diagnostic, and biotech settings for space‑efficient, cost‑effective ultrapure water solutions.

The Laboratory Water Purifier Market Report provides a comprehensive assessment of water purification solutions for laboratories, including academic and research institutes, pharmaceutical and biotech QC labs, clinical diagnostic labs, and industrial testing facilities. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional adoption trends, infrastructure readiness, and regulatory influences.

Product segments include water purity types (ultrapure/Type I, pure/Type II, RO/Type III), purification technologies (RO, ultrafiltration, ion exchange, UV sterilization, hybrid systems), system configurations (benchtop, modular central systems, IoT-enabled smart systems), and end-users (pharmaceutical & biotech, research institutes, hospitals/clinical labs, industrial QC labs). Applications include high-performance analytical chemistry, molecular biology and cell culture, diagnostics, reagent preparation, autoclave cleaning, and general lab maintenance.

The report also examines emerging technology trends such as modular design, real-time digital monitoring, IoT-enabled quality sensors, energy-efficient systems, and advanced filtration innovations. It addresses ESG considerations, lab-scale differentiation, and evolving market needs, providing strategic insights for decision-makers, investors, and industry professionals seeking guidance across global markets and emerging opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 7,989.5 Million |

| Market Revenue (2032) | USD 11,885.3 Million |

| CAGR (2025–2032) | 5.09% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Regulatory & ESG Overview |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Merck KGaA, Thermo Fisher Scientific, Sartorius AG, ELGA LabWater, Pall Corporation, Evoqua Water Technologies, Aqua Solutions, Inc., Purite Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |