Reports

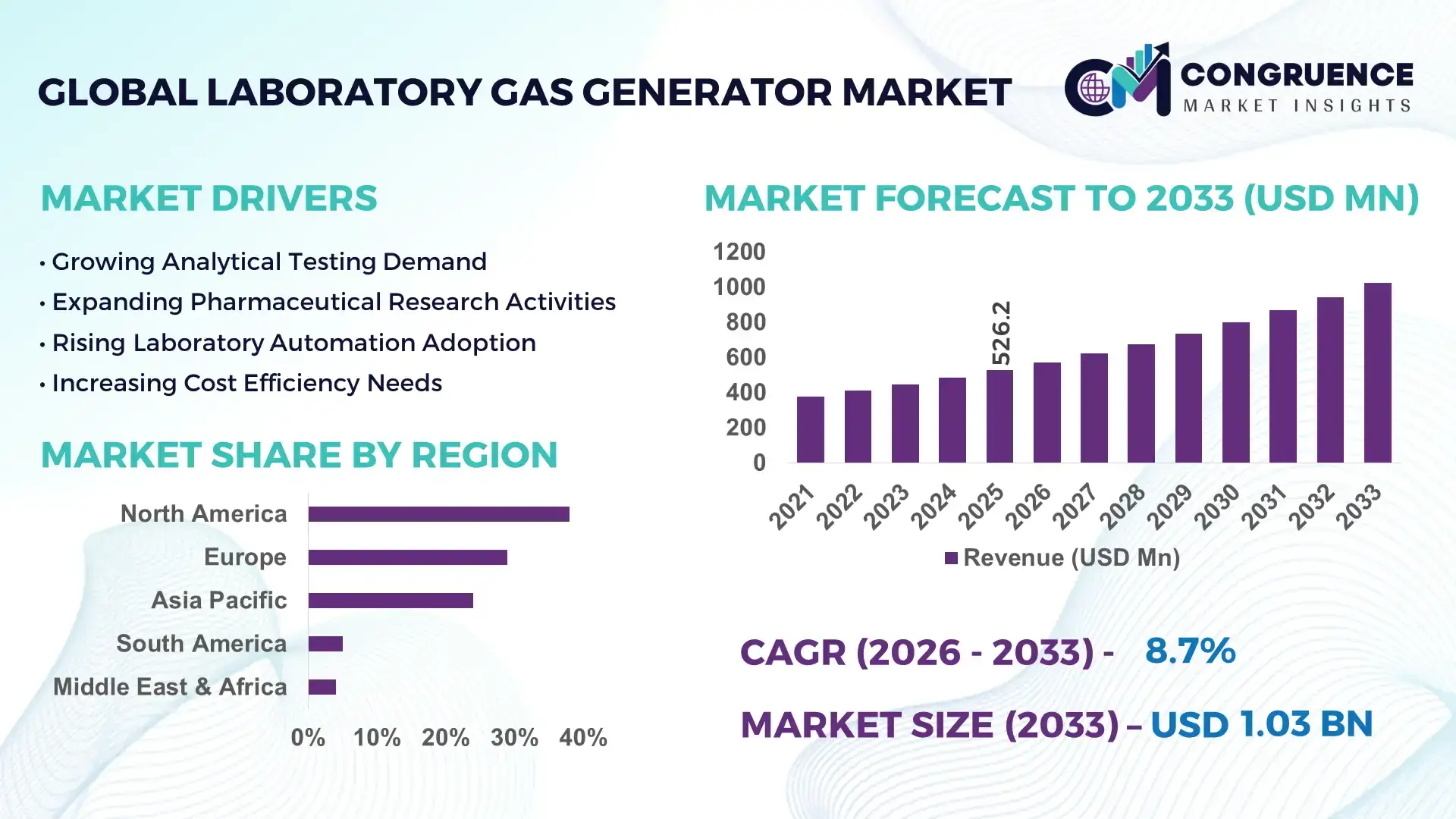

The Global Laboratory Gas Generator Market was valued at USD 526.2 Million in 2025 and is anticipated to reach a value of USD 1,025.6 Million by 2033 expanding at a CAGR of 8.7% between 2026 and 2033.The market is being accelerated by the replacement of high-pressure gas cylinders with on-site gas generation systems, enabling laboratories to reduce gas procurement costs by 25–40% while improving operational safety and supply continuity. Growing deployment of advanced chromatography, mass spectrometry, and life science research platforms is increasing demand for ultra-high-purity nitrogen, hydrogen, and zero-air generators across pharmaceutical, environmental, and analytical testing facilities. Between 2024 and 2026, laboratory operators have increasingly prioritized supply-chain resilience following geopolitical disruptions affecting industrial gas logistics, while stricter laboratory safety regulations are encouraging decentralized gas generation infrastructure. The ongoing shift toward automation and digital laboratory environments is further strengthening adoption of connected gas generation systems capable of predictive maintenance and remote monitoring.

The United States remains the dominant country in the global market, accounting for approximately 31% of total demand, supported by more than 18,000 pharmaceutical and biotechnology research facilities and one of the world's largest installed bases of analytical instrumentation. Over 65% of advanced chromatography laboratories in the country have integrated on-site nitrogen generation solutions to improve uptime and reduce dependence on delivered gas cylinders. Compared with traditional cylinder-based supply models, modern laboratory gas generators can reduce downtime related to gas replacement by over 35%, creating measurable productivity gains. Significant investment in life sciences, semiconductor research, environmental monitoring, and clinical diagnostics continues to reinforce the country's leadership position.

For manufacturers and investors, competitive advantage increasingly depends on delivering integrated, high-purity, digitally connected gas generation platforms that optimize laboratory efficiency while strengthening operational resilience.

Market Size & Growth: USD 526.2 million in 2025 is projected to reach USD 1,025.6 million by 2033, supported by laboratory automation, on-site gas generation adoption, and supply-chain optimization.

Top Growth Drivers: Laboratory automation (+42%), pharmaceutical R&D expansion (+38%), and analytical testing demand growth (+34%) are accelerating market momentum.

Short-Term Forecast: By 2028, laboratories are expected to reduce gas procurement costs by 30% while improving equipment uptime by 25%.

Emerging Technologies: AI-enabled monitoring, IoT-connected generators, and advanced membrane separation technologies are improving purity levels by over 20%.

Regional Leaders: North America (USD 360M+), Europe (USD 280M+), and Asia-Pacific (USD 240M+) lead adoption through research infrastructure expansion.

Consumer/End-User Trends: More than 68% of new analytical laboratories now prioritize on-site gas generation over cylinder-based systems.

Pilot/Case Example: A 2025 pharmaceutical laboratory modernization project achieved a 32% reduction in gas-related downtime through integrated nitrogen generation.

Competitive Landscape: Top suppliers collectively control nearly 45% of market activity, led by established analytical gas technology providers.

Regulatory & ESG Impact: On-site systems reduce transportation-related emissions by approximately 20% while strengthening laboratory safety compliance.

Investment & Funding: More than USD 450 million has been directed toward laboratory infrastructure upgrades, digitalization, and gas-generation deployment programs.

Innovation & Future Outlook: High-purity hydrogen generation, predictive maintenance, and connected laboratory ecosystems are redefining next-generation operational models.

Pharmaceutical and biotechnology laboratories contribute approximately 41% of total market demand, followed by environmental testing at 24% and academic research institutions at 18%. Recent innovation has focused on AI-enabled monitoring platforms, high-efficiency membrane technologies, and compact hydrogen generation systems that improve gas purity by over 20%. North America and Europe collectively account for nearly 62% of installed capacity, while Asia-Pacific is recording the fastest expansion due to laboratory infrastructure investment and localized manufacturing. Regulatory scrutiny on laboratory safety and ongoing supply-chain diversification are further accelerating technology upgrades. These developments are creating a foundation for deeper strategic transformation across the industry.

Laboratory gas generation is rapidly transforming from a supporting laboratory utility into a strategic infrastructure asset that directly influences operational continuity, analytical accuracy, cost control, and research productivity. As pharmaceutical innovation accelerates, environmental testing requirements intensify, and advanced analytical instrumentation becomes increasingly sophisticated, organizations are shifting away from traditional gas cylinder dependence toward integrated gas generation ecosystems.

The market is being reshaped by rising pressure to improve laboratory resilience amid global supply-chain disruptions and stricter safety compliance requirements. Facilities that previously relied on centralized gas deliveries are increasingly prioritizing on-site production capabilities to eliminate logistical vulnerabilities and optimize operating efficiency. Modern membrane-based nitrogen generation technology improves operational efficiency by 35% while reducing lifecycle costs by 30% compared to legacy cylinder-based supply systems. This measurable advantage is accelerating adoption across pharmaceutical quality-control laboratories, biotechnology research centers, and environmental testing facilities.

North America leads in overall market volume with approximately 38% demand concentration, while Asia-Pacific leads in adoption acceleration and infrastructure expansion, supported by more than 14% growth in advanced laboratory installations. Over the next two to three years, laboratories implementing connected gas generation platforms are expected to achieve 25% higher operational uptime and reduce gas-related maintenance interventions by nearly 20%.

ESG considerations are also emerging as a competitive differentiator. On-site generation can reduce transportation-related emissions by approximately 20%, improve safety compliance, and lower waste associated with cylinder handling and logistics. In one pharmaceutical quality-control facility, deployment of automated nitrogen generation systems improved instrument utilization rates by 28% while reducing gas replacement interruptions by 33%. Investment strategies are clearly shifting toward digitally connected, high-purity generation systems, with manufacturers expanding service capabilities, predictive maintenance platforms, and integrated laboratory infrastructure offerings. Organizations that successfully align gas generation investments with automation, sustainability, and operational optimization objectives will strengthen competitive positioning, improve resilience, and capture long-term performance advantages as laboratory ecosystems continue transforming globally.

The Laboratory Gas Generator Market is undergoing significant transformation as laboratories increasingly prioritize operational independence, analytical precision, and cost optimization. Demand is expanding across pharmaceutical research, biotechnology development, environmental testing, food safety analysis, clinical diagnostics, and academic research institutions. Advanced analytical instruments require continuous access to high-purity gases, making on-site generation a strategic alternative to traditional cylinder supply models. Technology improvements in membrane separation, pressure swing adsorption, and hydrogen generation are improving efficiency, reliability, and scalability. Simultaneously, laboratories are seeking solutions that reduce safety risks, transportation dependency, and operational interruptions. Industry participants are investing in digital monitoring platforms, predictive maintenance capabilities, and compact high-performance systems to strengthen competitive differentiation. The interaction between technology advancement, regulatory compliance, laboratory automation, and supply-chain resilience continues to redefine purchasing priorities and long-term market development.

The strongest growth engine in the market is the rapid expansion of automated analytical laboratories that require uninterrupted access to high-purity gases. More than 65% of newly installed chromatography systems are now integrated with dedicated gas generation infrastructure, while laboratory automation initiatives have increased by approximately 40% across pharmaceutical and biotechnology facilities. As analytical throughput requirements rise, organizations are replacing cylinder-based systems that create operational interruptions and safety challenges. Global supply-chain restructuring has further reinforced this transition by exposing vulnerabilities associated with delivered gas logistics. The result is a direct cause-and-effect relationship: higher instrument utilization creates greater demand for continuous gas availability, which in turn accelerates investment in on-site generation. Companies are responding through production expansion, strategic technology partnerships, and development of digitally connected platforms that improve uptime by over 25% while strengthening customer retention.

Despite strong demand fundamentals, upfront investment requirements remain a structural limitation. Installation and integration costs can be 25–35% higher than short-term cylinder procurement alternatives, creating barriers for smaller laboratories and budget-constrained institutions. Approximately 30% of laboratories in emerging markets continue to rely on conventional gas supply due to infrastructure limitations and technical expertise gaps. Supply concentration in specialized filtration components and precision control systems also introduces procurement risks during periods of industrial disruption. These constraints directly affect scalability, deployment speed, and purchasing decisions. To mitigate exposure, manufacturers are increasingly offering leasing programs, long-term service agreements, and modular system architectures that reduce initial capital burdens. Diversified supplier networks and localized support models are also helping companies improve deployment flexibility while reducing dependence on concentrated component ecosystems.

The most attractive opportunities are emerging at the intersection of digital laboratories, decentralized research infrastructure, and advanced analytical testing. Connected gas generation systems equipped with predictive diagnostics can reduce maintenance interventions by 20% while improving operational visibility by more than 30%. Emerging economies are increasing laboratory modernization investments, with advanced analytical capacity expanding by approximately 15% annually in several high-growth regions. A significant innovation shift is occurring around AI-enabled performance monitoring, remote asset management, and integrated laboratory ecosystems. Beyond traditional pharmaceutical demand, environmental testing, semiconductor research, and food safety laboratories are creating new demand pockets. Companies are positioning for future dominance through expanded R&D spending, ecosystem partnerships, and software-enabled service models. The strategic upside extends beyond equipment sales, creating recurring revenue opportunities through monitoring, maintenance, and performance optimization services.

The market's primary challenge lies in balancing rapid adoption with performance consistency, regulatory compliance, and infrastructure readiness. Nearly 22% of laboratory operators cite system integration complexity as a major deployment obstacle, while maintenance-related performance variability can affect analytical reliability by up to 15% if improperly managed. Increasing laboratory digitization also places pressure on cybersecurity, interoperability, and data management capabilities. Real-world infrastructure limitations, including inconsistent power quality in developing regions, further complicate deployment. These barriers affect long-term sustainability by increasing operational risk and slowing adoption rates among conservative end-users. To remain competitive, companies must invest aggressively in reliability engineering, service networks, digital support capabilities, and strategic partnerships. The ability to deliver scalable, compliant, and high-performance solutions will increasingly determine leadership positions as the market continues evolving.

38% Increase in Connected Generator Deployments Reshaping Laboratory Operations Laboratory operators are integrating IoT-enabled gas generators at a rapidly increasing pace, with connected installations rising by 38% and remote monitoring utilization exceeding 55%. Predictive maintenance tools are reducing unplanned service interventions by nearly 22%, improving instrument availability. Manufacturers are scaling software integration capabilities and expanding digital service offerings to strengthen recurring customer engagement.

31% Reduction in Cylinder Dependency Forcing Procurement Model Changes Laboratories are reducing dependence on delivered gas cylinders, with on-site generation adoption increasing by 31% across advanced testing facilities. Gas replacement events have declined by approximately 35%, improving workflow continuity. Supply-chain disruptions and transportation volatility have accelerated this shift, prompting companies to redesign procurement strategies and prioritize operational self-sufficiency.

27% Growth in Asia-Based Installations Redefining Regional Demand Distribution Deployment activity across Asia-Pacific has increased by 27%, driven by pharmaceutical manufacturing expansion, laboratory modernization programs, and localized equipment production. More than 45% of new analytical laboratory projects now include integrated gas generation infrastructure. Manufacturers are responding through regional partnerships, localized assembly operations, and expanded technical support networks.

24% Rise in Service-Based Business Models Optimizing Lifecycle Value Service subscriptions, performance contracts, and equipment-as-a-service offerings have expanded by 24%, reflecting changing customer purchasing preferences. Organizations are prioritizing predictable operating expenses and guaranteed uptime metrics over capital-intensive ownership models. This shift is redefining competitive dynamics, forcing suppliers to combine equipment innovation with long-term operational support and performance accountability.

The Laboratory Gas Generator Market is segmented by type, application, and end-user, reflecting diverse operational requirements across analytical laboratories and research environments. Demand remains concentrated in nitrogen generation systems due to their widespread use in chromatography and mass spectrometry applications, while hydrogen generation is gaining momentum as laboratories seek higher efficiency and safer alternatives to gas cylinders. Approximately 46% of total demand originates from analytical instrumentation applications, highlighting the market’s strong dependence on precision testing environments. Pharmaceutical and biotechnology organizations account for nearly 41% of end-user demand, reinforcing the strategic importance of research-driven purchasing decisions. Demand is increasingly shifting toward automated, digitally monitored gas generation platforms that improve operational continuity and reduce dependence on external gas supply networks. For decision-makers, understanding where demand is concentrated and where adoption is accelerating is essential for prioritizing product development, investment allocation, and regional expansion strategies.

The nitrogen gas generators segment dominates the Laboratory Gas Generator Market, accounting for approximately 48% of total demand in 2025. Its leadership position is supported by broad deployment across chromatography, mass spectrometry, and analytical testing laboratories where continuous nitrogen supply is critical for instrument performance. Nitrogen generators offer lower operating costs, improved safety, and seamless integration with laboratory workflows, making them the preferred choice for high-throughput facilities. Hydrogen gas generators represent the fastest-growing segment, with adoption increasing at approximately 11.4% annually as laboratories transition toward cleaner and more efficient carrier gas solutions. Compared with traditional cylinder-based hydrogen supply, modern generators provide enhanced safety controls and reduce logistical complexity. Hydrogen systems are increasingly being adopted in advanced gas chromatography applications where performance optimization is a priority. Zero air generators, combined with specialty gas generation systems, account for roughly 29% of total market demand and maintain strong relevance in environmental testing, emissions monitoring, and calibration applications. Companies are expanding portfolios with compact, digitally connected systems that support multiple gas outputs and predictive maintenance capabilities. Demand is clearly shifting toward integrated platforms that combine purity, automation, and operational efficiency, creating attractive investment opportunities in advanced gas generation technologies while reducing reliance on conventional gas delivery models.

Analytical Instrumentation remains the largest application segment, accounting for approximately 46% of total market demand. The concentration of demand within this segment reflects the extensive use of gas generators in gas chromatography, liquid chromatography-mass spectrometry, and other precision analytical platforms. Continuous gas availability directly impacts instrument productivity, making on-site generation a critical operational requirement. Life Sciences and Pharmaceutical Research is the fastest-expanding application area, recording annual demand growth of approximately 12.1%. Increasing drug development activity, biologics research, and quality-control testing are driving adoption of high-purity gas generation systems. Compared with mature analytical testing environments, pharmaceutical research facilities increasingly prioritize integrated gas generation solutions that support automation and uninterrupted workflows. Environmental Testing, Food Safety Analysis, and Academic Research collectively account for approximately 37% of market demand. These applications are benefiting from stricter quality standards, increased monitoring requirements, and expanding laboratory infrastructure investments. Organizations are deploying scalable gas generation platforms to reduce operational risks and improve testing consistency. The market is witnessing a clear transition from standalone gas supply models toward integrated laboratory infrastructure solutions, making application-specific customization and performance optimization increasingly important for suppliers seeking long-term growth opportunities.

Pharmaceutical and Biotechnology Companies represent the largest end-user segment, accounting for approximately 41% of total market demand. Their leadership is driven by intensive analytical testing requirements, regulatory compliance standards, and extensive reliance on chromatography and mass spectrometry systems. High instrument utilization rates create strong demand for reliable, uninterrupted gas supply solutions.Contract Research Organizations (CROs) are the fastest-growing end-user category, with adoption increasing by approximately 12.8% annually. Rising outsourcing activity across drug discovery, clinical testing, and laboratory services is expanding the need for scalable and cost-efficient gas generation infrastructure. Compared with established pharmaceutical organizations, CROs prioritize flexible deployment models and rapid operational scalability. Academic Research Institutes, Environmental Testing Laboratories, and Clinical Diagnostic Centers collectively account for approximately 44% of market demand. These users increasingly favor compact, low-maintenance systems that reduce operating expenses and improve laboratory independence. Manufacturers are responding through customized product configurations, service-based contracts, and strategic partnerships tailored to diverse laboratory environments. Future demand is shifting toward organizations seeking greater automation, operational resilience, and long-term cost optimization, making customer-specific solutions a critical competitive differentiator.

North America accounted for the largest market share at 38.0% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.4% between 2026 and 2033.

North America maintains leadership through its concentration of pharmaceutical research facilities, advanced analytical laboratories, and high-value scientific infrastructure. Europe follows with approximately 29% market share, supported by strong regulatory compliance requirements and laboratory modernization initiatives. Asia-Pacific accounts for nearly 24% of demand and is rapidly expanding due to pharmaceutical manufacturing growth, biotechnology investment, and increasing analytical testing capacity. South America and the Middle East & Africa collectively contribute approximately 9% of global demand, supported by improving laboratory infrastructure and industrial testing requirements. Supply-chain diversification, localized manufacturing, and laboratory digitalization initiatives are reshaping regional investment priorities. Companies are increasingly focusing expansion strategies on Asia-Pacific while strengthening innovation capabilities in North America and Europe to maintain global competitiveness.

North America accounts for approximately 38% of global Laboratory Gas Generator Market demand, making it the largest regional market. Pharmaceutical research, biotechnology innovation, environmental testing, and semiconductor development remain the primary demand drivers. Increasing laboratory safety requirements and operational continuity objectives are accelerating adoption of on-site gas generation systems. More than 65% of newly commissioned analytical laboratories now integrate connected gas generation technologies with automated monitoring capabilities. Laboratory infrastructure modernization programs have improved deployment rates by approximately 28% across major research hubs. Enterprise buyers increasingly prioritize lifecycle cost reduction, operational resilience, and predictive maintenance capabilities over conventional gas procurement models. These trends continue to encourage manufacturers to expand regional service networks, strengthen digital offerings, and prioritize North America as a critical innovation and commercialization center.

Europe represents approximately 29% of global market demand, supported by strong pharmaceutical, environmental testing, and industrial research activity across Germany, the United Kingdom, France, and the Netherlands. Regulatory emphasis on laboratory safety, emissions reduction, and operational efficiency is driving accelerated adoption of on-site gas generation systems. Nearly 58% of laboratory modernization projects now include sustainability-focused infrastructure upgrades. Organizations are increasingly implementing energy-efficient generation technologies capable of reducing operational energy consumption by approximately 18%. Compliance-driven procurement behavior remains a defining market characteristic, with enterprises prioritizing quality, reliability, and long-term regulatory alignment. Manufacturers are responding through advanced filtration technologies, digital monitoring capabilities, and environmentally optimized product designs. The region continues to function as a key driver of innovation, forcing suppliers to continuously improve efficiency and compliance performance.

Asia-Pacific accounts for approximately 24% of global demand and ranks as the fastest-expanding regional market. China, Japan, South Korea, and India are leading adoption through pharmaceutical manufacturing expansion, biotechnology investment, and laboratory infrastructure development. More than 45% of newly established analytical laboratories in major industrial centers now include integrated gas generation systems. Regional manufacturing advantages and localized supply chains are reducing deployment costs by nearly 20% compared with imported alternatives. Organizations increasingly prioritize speed, scalability, and operational efficiency, accelerating mass adoption of advanced laboratory technologies. Manufacturers are expanding production capacity, strengthening local partnerships, and increasing regional service coverage. Asia-Pacific has become a critical market for scale-driven growth, making it a strategic priority for global expansion initiatives.

South America contributes approximately 5% of global market demand, with Brazil and Argentina representing the largest regional opportunities. Growth is being supported by pharmaceutical manufacturing expansion, food safety testing requirements, and environmental monitoring initiatives. However, infrastructure limitations and budget constraints continue to affect purchasing decisions across many laboratory environments. Approximately 42% of procurement decisions remain heavily influenced by total ownership costs and financing flexibility. Adoption of compact and modular gas generation systems has increased by nearly 16% as laboratories seek affordable modernization pathways. Enterprises remain highly price-sensitive but increasingly recognize the operational benefits of on-site generation technologies. The region presents a balanced opportunity profile where long-term growth potential is significant, but successful market penetration requires localized strategies and cost-effective solutions.

The Middle East & Africa accounts for approximately 4% of global market demand, with key activity concentrated in the United Arab Emirates, Saudi Arabia, and South Africa. Demand is driven by energy-sector testing, healthcare expansion, environmental monitoring, and industrial research programs. Regional investment in laboratory modernization has increased by approximately 21% over recent years, improving adoption of advanced analytical infrastructure. More than 35% of newly funded laboratory projects now incorporate automated gas generation technologies. Organizations increasingly prioritize reliability, reduced logistics dependency, and operational efficiency when evaluating laboratory equipment investments. Strategic partnerships, infrastructure development programs, and technology transfer initiatives are strengthening market foundations. The region continues emerging as a strategic growth opportunity where modernization and investment are accelerating demand for advanced laboratory solutions.

United States – 31% Market Share: Benefits from extensive pharmaceutical R&D activity, advanced analytical laboratory infrastructure, and widespread adoption of automated testing technologies.

China – 14% Market Share: Driven by large-scale pharmaceutical manufacturing, rapid laboratory expansion, localized production capabilities, and strong investment in scientific research infrastructure.

The Laboratory Gas Generator Market is characterized by competition between global technology leaders such as PEAK Scientific, Parker Hannifin, LNI Swissgas, Claind, and VICI DBS, alongside regional specialists competing on pricing, service responsiveness, and customized laboratory solutions. The top five players collectively account for approximately 54% of global market activity, creating a moderately consolidated competitive environment.

Competition is increasingly centered on gas purity, digital monitoring capabilities, energy efficiency, and lifecycle ownership costs rather than equipment pricing alone. Advanced nitrogen generators equipped with predictive diagnostics can reduce maintenance interventions by nearly 20%, while energy-efficient systems lower operating costs by 15–25%. More than 60% of premium laboratory procurements now evaluate digital service capabilities as a key purchasing criterion.

Leading suppliers are expanding through strategic partnerships with analytical instrument manufacturers, regional service network expansion, product innovation, and integrated laboratory infrastructure offerings. The competitive landscape is shifting toward connected gas generation ecosystems and long-term service contracts, creating stronger customer retention. Technical certification requirements, installed service infrastructure, and application-specific expertise remain major entry barriers. Winning in this market requires superior gas purity performance, digital integration capabilities, global service coverage, and the ability to deliver measurable operational savings.

Parker Hannifin Corporation

Claind S.r.l.

VICI DBS

F-DGSi

Proton OnSite

ErreDue S.p.A.

FST GmbH

Domnick Hunter Gas Generation

LabTech S.r.l.

Air Products and Chemicals, Inc.

Nel Hydrogen

Angstrom Advanced Inc.

Technology innovation is rapidly redefining the Laboratory Gas Generator Market as laboratories prioritize operational continuity, gas purity, automation, and cost optimization. Current market adoption is dominated by Pressure Swing Adsorption (PSA) and membrane separation technologies, which collectively account for nearly 72% of installed systems globally. Advanced PSA platforms are improving nitrogen purity levels above 99.999% while reducing energy consumption by approximately 18% compared with previous-generation systems.

A major technology transition is occurring through the integration of IoT-enabled monitoring, predictive maintenance software, and intelligent diagnostics. Connected gas generators can reduce unexpected downtime by nearly 25% while improving service planning accuracy by more than 20%. Approximately 48% of newly installed premium laboratory gas generation systems now incorporate remote monitoring capabilities. These technologies provide laboratories with real-time visibility into gas quality, pressure stability, and system health, creating measurable operational advantages.

Hydrogen generation technology is emerging as a disruptive growth area, particularly in gas chromatography applications. Modern hydrogen generators improve carrier gas efficiency by approximately 30% while reducing recurring supply costs by nearly 35% compared with conventional cylinder-based alternatives. This transition is helping laboratories improve analytical throughput while strengthening safety controls.

Between 2026 and 2028, AI-enabled performance optimization, cloud-connected diagnostics, and multi-gas integrated generation platforms are expected to become competitive differentiators. Companies with strong software capabilities, digital service ecosystems, and high-purity generation technologies will be best positioned to capture premium laboratory infrastructure investments as customers increasingly prioritize automation, reliability, and lifecycle value.

June 2025 – PEAK Scientific launched its Intura series of hydrogen, nitrogen, and zero-air laboratory generators featuring a significantly smaller footprint and lower power consumption than predecessor platforms. The product line incorporates improved PSA dryer technology and enhanced filtration systems, strengthening laboratory efficiency and space optimization. [Compact Platform Shift] Source: www.scientistlive.com

June 2025 – PEAK Scientific unveiled the Intura range at ASMS 2025, introducing redesigned CAT chamber technology and advanced AirMax filtration. The new systems were engineered to provide one of the smallest footprints in the laboratory gas generation segment while supporting flexible flow and pressure requirements. [Footprint Optimization]

May 2026 – PEAK Scientific introduced the Genius NEO platform, positioned as its most advanced nitrogen generator with enhanced sustainability and performance characteristics. The launch reflects accelerating industry demand for higher-purity gas generation and digitally optimized laboratory infrastructure solutions. [Next-Gen Nitrogen]

March 2025 – Laboratory users reported successful deployment of centralized nitrogen generation systems supporting up to 12 LC-MS instruments from a single installation, delivering an estimated payback period of approximately 13 months compared with liquid nitrogen alternatives. This highlights growing adoption of large-scale laboratory gas infrastructure models. [Centralized Supply Trend]

The Laboratory Gas Generator Market Report provides comprehensive coverage of the industry across major product categories, applications, end-user segments, regional markets, and technology ecosystems. The analysis evaluates nitrogen gas generators, hydrogen gas generators, zero air generators, and specialty gas generation systems while assessing demand across analytical instrumentation, pharmaceutical research, environmental testing, food safety laboratories, clinical diagnostics, and academic research institutions. The report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, enabling detailed regional benchmarking and opportunity assessment.

The study delivers deep analytical coverage of more than 15 strategic segment combinations, profiling key market participants, technology adoption trends, purchasing patterns, and competitive positioning. Approximately 48% of newly installed systems now incorporate digital monitoring functionality, while advanced nitrogen generation technologies represent nearly half of installed market demand. The report also evaluates adoption trends associated with connected laboratory infrastructure, predictive maintenance platforms, and high-purity gas generation technologies.

From a strategic perspective, the report supports investment prioritization, product portfolio planning, geographic expansion strategies, competitive benchmarking, and technology roadmapping. Particular focus is placed on emerging opportunities in automated laboratory environments, hydrogen generation applications, and integrated digital service models. Forward-looking coverage for 2026–2033 highlights evolving customer requirements, technology shifts, operational efficiency trends, and competitive developments that are expected to influence long-term market positioning and growth opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 526.2 Million |

| Market Revenue (2033) | USD 1,025.6 Million |

| CAGR (2026–2033) | 8.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | PEAK Scientific; Parker Hannifin Corporation; LNI Swissgas; Claind S.r.l.; VICI DBS; F-DGSi; Proton OnSite; ErreDue S.p.A.; FST GmbH; Domnick Hunter Gas Generation; LabTech S.r.l.; Air Products and Chemicals, Inc.; Nel Hydrogen; Angstrom Advanced Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |