Reports

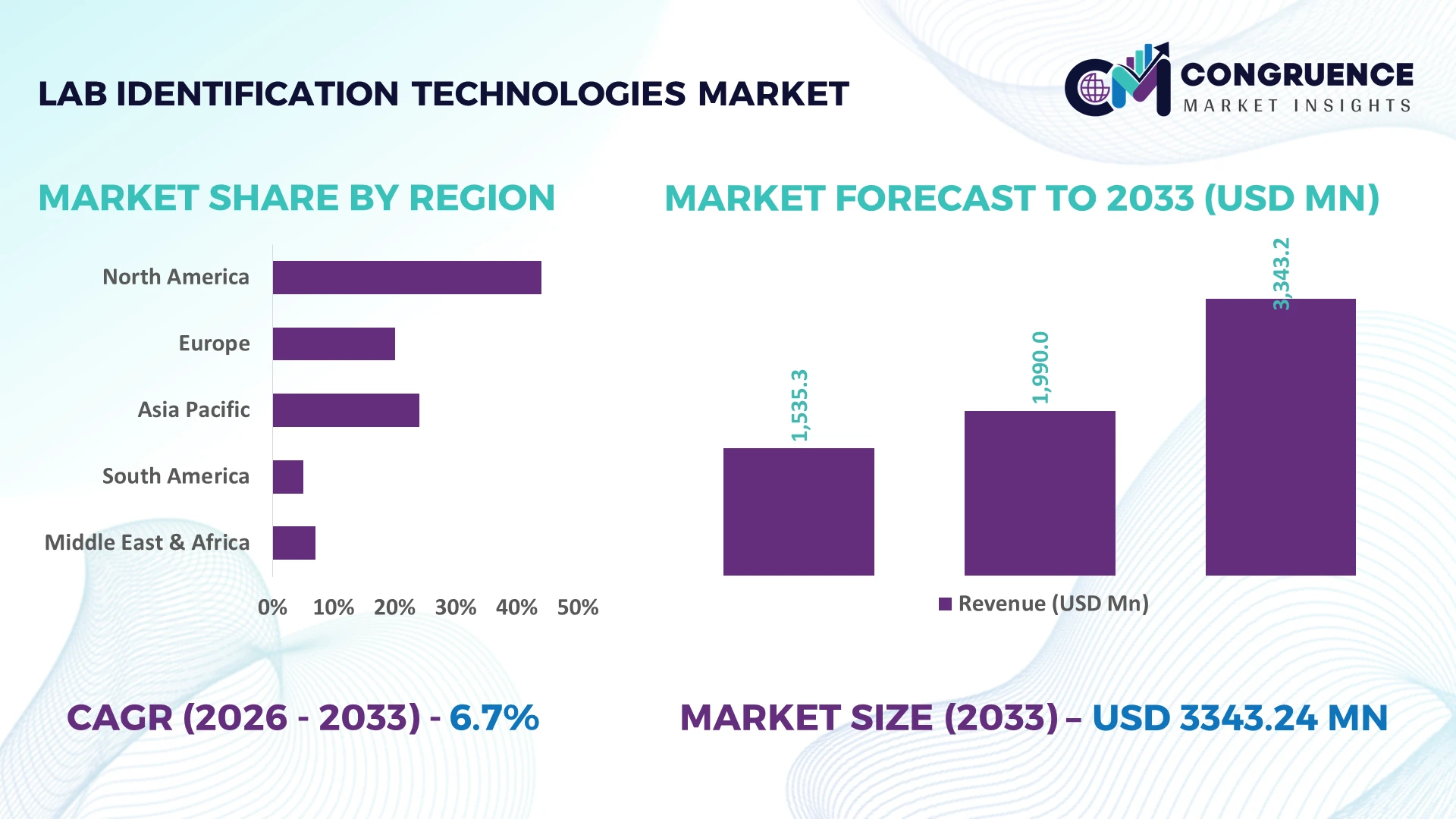

The Global Lab Identification Technologies Market was valued at USD 1990 Million in 2025 and is anticipated to reach a value of USD 3343.24 Million by 2033 expanding at a CAGR of 6.7% between 2026 and 2033. Growth is driven by rapid laboratory automation, expanding barcode and RFID-enabled sample traceability, stricter regulatory compliance, and AI-integrated laboratory information workflows that improve identification accuracy and operational efficiency.

The United States leads the global Lab Identification Technologies Market with approximately 36% market share, supported by extensive life sciences research, over 13,000 clinical laboratories, and sustained investments in biotechnology and precision diagnostics. Compared with Germany, which benefits from advanced industrial laboratory infrastructure, the U.S. demonstrates higher adoption of RFID-enabled identification systems, exceeding 62% across large laboratory networks. Continued healthcare innovation, resilient supply-chain modernization, and strategic responses to evolving global trade dynamics reinforce long-term competitiveness and technology deployment.

Organizations prioritizing scalable digital identification platforms and automation-ready laboratory infrastructure will strengthen operational resilience and long-term competitive positioning.

Market Size & Growth: USD 1990 Million (2025) to USD 3343.24 Million (2033) at 6.7% CAGR, driven by AI-enabled laboratory automation and digital sample traceability.

Top Growth Drivers: Laboratory automation (+31%), barcode/RFID adoption (+27%), precision diagnostics expansion (+24%) accelerate global market development.

Short-Term Forecast: By 2028, sample identification errors decline 28% while laboratory workflow efficiency improves 22% through digital integration.

Emerging Technologies: AI, RFID, cloud-based LIMS, and automated label verification improve identification accuracy above 99%.

Regional Leaders: North America exceeds USD 1.2 Billion, Europe approaches USD 0.9 Billion, Asia-Pacific surpasses USD 0.8 Billion with expanding laboratory modernization.

Consumer/End-User Trends: More than 68% of large laboratories prioritize automated identification for regulatory compliance and operational consistency.

Pilot/Case Example: 2026 digital pathology deployment improved specimen tracking accuracy by 30% and reduced processing delays by 18%.

Competitive Landscape: Top five players control nearly 48% market share, led by Thermo Fisher Scientific, Zebra Technologies, Brady Corporation, Honeywell, and GA International.

Regulatory & ESG Impact: Digital traceability initiatives reduce labeling waste by 16% while strengthening laboratory compliance performance.

Investment & Funding: Over USD 1.1 Billion supports laboratory digitalization, strategic partnerships, manufacturing expansion, and automation deployment amid supply-chain diversification.

Innovation & Future Outlook: Smart labels, AI-assisted verification, and interoperable identification platforms strengthen next-generation laboratory ecosystems and global expansion strategies.

Laboratory identification technologies continue expanding across clinical diagnostics, pharmaceutical manufacturing, biobanking, and academic research where reliable sample traceability is critical. AI-assisted verification, RFID-enabled asset tracking, and durable smart labeling solutions improve workflow consistency, with automated identification adoption increasing by approximately 29% across advanced laboratories. Ongoing regulatory digitalization and supply-chain resilience initiatives are accelerating enterprise investment, setting the foundation for the strategic market analysis that follows.

Laboratory identification technologies have become a strategic investment priority as pharmaceutical manufacturers, clinical laboratories, and biotechnology companies strengthen sample traceability, regulatory compliance, and digital workflow integration. Infrastructure modernization and accelerated laboratory digitalization are reshaping procurement priorities, while resilient supply-chain strategies encourage standardized identification platforms capable of supporting multi-site operations with higher data integrity and faster processing.

AI-enabled barcode and RFID identification systems process samples approximately 35% faster than conventional manual labeling while reducing identification errors by nearly 30%, lowering operational costs and improving laboratory productivity. The United States leads large-scale deployment through integrated laboratory automation, whereas Japan emphasizes compact, precision-driven identification solutions for high-density research facilities. Over the next two to three years, automated identification deployment across advanced laboratories is expected to exceed 70%, supported by wider cloud-based laboratory information management integration and growing digital compliance requirements.

A leading pharmaceutical manufacturer deploying RFID-enabled specimen tracking across multiple production sites can reduce inventory reconciliation time by nearly 25% while strengthening audit readiness and chain-of-custody verification. In response, technology providers are expanding software partnerships, investing in interoperable identification platforms, and strengthening regional manufacturing capabilities to secure long-term competitive positioning through scalable, data-driven laboratory ecosystems.

Expanding laboratory automation is fundamentally increasing demand for advanced identification technologies across diagnostics, pharmaceuticals, and life sciences. More than 64% of newly modernized laboratories now integrate barcode or RFID-based identification, while automated sample tracking reduces processing delays by approximately 28% and identification errors by nearly 30%. The United States continues expanding digital laboratory infrastructure following stricter electronic record compliance requirements, encouraging enterprise-wide workflow standardization. In response, technology vendors are investing in AI-assisted verification software, expanding RFID manufacturing capacity, and forming partnerships with laboratory information management providers. The strongest competitive advantage increasingly comes from combining identification hardware, software, and analytics into unified operational platforms rather than supplying standalone labeling solutions.

Legacy laboratory infrastructure continues to restrict seamless deployment of advanced identification technologies. Nearly 42% of medium-sized laboratories operate mixed hardware environments, while integration expenses account for almost 20% of digital laboratory modernization budgets. Germany and several industrial markets face interoperability challenges where older laboratory instruments remain operational despite increasing digital compliance expectations. These structural limitations delay implementation schedules, increase validation costs, and reduce enterprise scalability. Companies are responding through localized manufacturing, standardized communication protocols, long-term integration agreements, and modular software architectures that simplify migration from legacy systems. Operational success increasingly depends on reducing compatibility barriers rather than introducing additional identification hardware.

The strongest opportunity lies in combining AI, RFID, cloud connectivity, and predictive laboratory analytics into unified identification ecosystems. More than 55% of biotechnology organizations are expanding digital laboratory investments, while intelligent workflow automation improves asset utilization by approximately 24% and reduces manual verification activities by nearly 32%. Singapore continues strengthening national biomedical research infrastructure through advanced digital laboratory initiatives, creating favorable conditions for integrated identification platforms. Companies are increasing R&D spending, developing interoperable cloud solutions, and expanding strategic partnerships with laboratory software providers. Long-term differentiation will increasingly depend on data interoperability and predictive operational intelligence rather than hardware performance alone.

As laboratories become increasingly interconnected, maintaining secure, scalable identification infrastructure presents a major execution challenge. Around 48% of laboratory organizations identify cybersecurity and connected-device management as critical digital priorities, while approximately 37% report shortages of skilled automation specialists capable of managing integrated laboratory systems. The United Kingdom continues strengthening cybersecurity expectations for healthcare and research infrastructure, increasing operational complexity for technology providers. Companies must invest in secure cloud architectures, workforce development, and continuous software validation while expanding strategic partnerships with cybersecurity specialists. Sustainable market leadership will depend on delivering highly secure, interoperable, and easily scalable identification ecosystems across distributed laboratory networks.

AI-Powered Sample Verification: Laboratories are embedding AI-assisted image recognition into barcode validation and specimen identification, improving verification accuracy by nearly 32% while reducing manual review time by 27%. Growing regulatory scrutiny of laboratory traceability and persistent workforce shortages are accelerating deployment across the United States. Technology providers are integrating AI with laboratory information platforms and expanding software partnerships to standardize quality control without disrupting existing laboratory workflows.

RFID Deployment Expands Rapidly: RFID adoption for specimen tracking and laboratory asset visibility has increased by approximately 29%, while inventory search time has declined by nearly 35% and misplaced samples by 26%. Pharmaceutical manufacturers in Germany are extending RFID across production and quality-control laboratories to strengthen chain-of-custody management. Vendors are scaling interoperable hardware portfolios and restructuring supply partnerships to support enterprise-wide deployment with lower implementation complexity.

Cloud-Connected Laboratory Operations: Cloud-enabled laboratory information systems now support over 58% of newly digitalized laboratory environments, reducing reporting turnaround by 24% and improving multi-site data accessibility by 31%. Enterprise laboratories in Japan increasingly prioritize centralized identification management to coordinate geographically distributed facilities. Software companies are expanding subscription-based platforms, strengthening cybersecurity capabilities, and integrating automated compliance documentation into daily laboratory operations.

Sustainable Smart Label Innovation: Durable liner-free labels, recyclable identification materials, and low-energy thermal printing technologies are reducing labeling waste by nearly 18% while lowering consumable usage by 21%. Environmental compliance requirements and procurement modernization are reshaping purchasing decisions across healthcare laboratories. Manufacturers are investing in eco-designed consumables, automated printing systems, and regional production capacity, while premium laboratories increasingly evaluate lifecycle efficiency instead of focusing solely on label pricing.

Barcode Systems remain the dominant segment because of their low deployment cost, high scalability, and seamless compatibility with laboratory information systems. More than 68% of clinical laboratories continue using barcode-based identification for routine specimen management, supported by mature infrastructure and standardized regulatory workflows. Label Printers remain strategically important by enabling durable, high-volume identification, while Sample Tracking platforms strengthen operational visibility through integrated monitoring and chain-of-custody management. Laboratory Information Systems continue expanding as laboratories seek centralized data governance and workflow synchronization across multiple facilities.

RFID Systems represent the fastest-growing segment as laboratories prioritize real-time visibility, automated inventory control, and contactless identification. RFID-enabled workflows improve asset utilization by approximately 26% while reducing manual tracking activities by nearly 30%. Technology providers are expanding integrated hardware-software portfolios, forming interoperability partnerships, and investing in cloud-enabled identification ecosystems to address enterprise digital transformation priorities. Investment is steadily shifting from standalone identification devices toward intelligent, connected laboratory infrastructure capable of supporting automation at scale.

Sample Identification continues to dominate application demand because every diagnostic, pharmaceutical, and research workflow depends on accurate specimen recognition from collection through analysis. Approximately 72% of laboratory identification activities remain centered on sample labeling and verification, making this application operationally indispensable. Specimen Tracking follows closely as laboratories strengthen chain-of-custody documentation, while Asset Management and Inventory Management improve equipment utilization and consumable control. Workflow Automation increasingly connects these applications into unified digital laboratory environments, reducing administrative intervention and improving operational consistency.

Workflow Automation is the fastest-growing application as laboratories integrate AI, robotics, and laboratory information systems into daily operations. Automated workflows reduce processing time by approximately 25% while improving laboratory throughput by nearly 22%. Companies are expanding cloud-native software, introducing intelligent workflow orchestration, and strengthening implementation partnerships with enterprise laboratories. Competitive positioning increasingly depends on delivering integrated operational platforms rather than individual identification applications.

Diagnostic Laboratories remain the largest end-user segment because they process high specimen volumes requiring continuous identification accuracy, regulatory compliance, and rapid turnaround. Nearly 46% of enterprise identification deployments are concentrated within diagnostic laboratory environments where automation directly improves operational productivity. Hospitals maintain significant demand through integrated clinical testing services, while Research Institutes depend on advanced identification systems for complex experimental workflows. Pharmaceutical Companies continue investing in digital traceability across quality assurance and manufacturing operations.

Biotechnology Companies represent the fastest-growing end-user group as precision medicine, cell therapy, and genomic research expand demand for highly traceable laboratory ecosystems. Automated identification reduces sample management errors by approximately 28% while improving research workflow efficiency by nearly 24%. Suppliers are developing customized software, expanding collaborative partnerships, and introducing flexible pricing models tailored to emerging biotechnology enterprises. Future competitive advantage increasingly depends on supporting specialized research environments requiring scalable and interoperable identification technologies.

North America accounted for the largest market share at 38.6% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 7.9% CAGR between 2026 and 2033.

Digital laboratory integration strengthens enterprise competitiveness

North America maintains leadership through advanced laboratory automation, mature healthcare infrastructure, and widespread deployment of integrated identification technologies across pharmaceutical, clinical, and biotechnology facilities. The region contributes approximately 39% of global demand, supported by extensive adoption of laboratory information systems, barcode platforms, and RFID-enabled workflows. More than 65% of large laboratory networks have implemented automated identification environments, improving operational traceability and compliance. Enterprise partnerships increasingly focus on cloud-enabled laboratory ecosystems, while manufacturers continue expanding production capacity for intelligent labeling solutions to support precision diagnostics and decentralized laboratory operations.

United States Market Outlook: The United States remains the region's operational center due to its extensive clinical laboratory network, strong biotechnology ecosystem, and continuous investment in laboratory modernization. More than 62% of enterprise laboratories utilize integrated digital identification platforms, supported by advanced regulatory frameworks and widespread automation initiatives. Technology providers continue expanding domestic manufacturing, software integration capabilities, and strategic partnerships with healthcare systems, reinforcing the country's leadership in scalable laboratory identification infrastructure and next-generation diagnostic workflows.

Regulatory modernization accelerates digital traceability adoption

Europe continues strengthening its position through advanced regulatory compliance, laboratory standardization, and sustainable digital infrastructure investments. The region accounts for approximately 28% of global market activity, supported by pharmaceutical manufacturing, public healthcare laboratories, and academic research institutions. Automated identification deployment has expanded by nearly 24% across enterprise laboratories as organizations strengthen electronic documentation and specimen traceability. Manufacturers increasingly prioritize environmentally responsible labeling technologies while integrating interoperable software platforms to improve laboratory productivity and cross-border operational consistency.

Germany Market Outlook: Germany leads the European market through its strong pharmaceutical manufacturing base, industrial automation expertise, and advanced laboratory technology ecosystem. Nearly 58% of large pharmaceutical laboratories have upgraded integrated identification systems supporting digital quality management and automated specimen tracking. Domestic manufacturers continue investing in smart labeling technologies, industrial software integration, and collaborative innovation programs that strengthen laboratory efficiency while supporting highly regulated production and research environments.

Manufacturing expansion drives large-scale deployment

Asia-Pacific is emerging as the fastest-expanding regional market due to laboratory infrastructure expansion, biotechnology investment, and increasing healthcare digitalization. The region represents approximately 24% of global demand while recording the highest deployment momentum across clinical diagnostics and pharmaceutical manufacturing. More than 30% of newly commissioned laboratory facilities incorporate automated identification systems during initial deployment, reducing implementation complexity. International suppliers are expanding manufacturing partnerships and localized production capabilities to strengthen supply resilience and accelerate enterprise adoption throughout major industrial economies.

China Market Outlook: China leads regional expansion through large-scale healthcare infrastructure development, biotechnology manufacturing growth, and continuous laboratory modernization initiatives. More than 35% of newly established pharmaceutical laboratories deploy integrated barcode and RFID identification platforms from project initiation. Domestic technology providers are strengthening manufacturing capacity, software development, and automation partnerships while supporting national initiatives focused on laboratory digitalization, advanced life sciences research, and industrial innovation.

Healthcare modernization supports identification upgrades

South America is steadily expanding through healthcare infrastructure modernization, pharmaceutical manufacturing improvements, and greater laboratory digitalization. The region contributes approximately 6% of global market demand, with public and private laboratories investing in automated identification technologies to strengthen operational efficiency. Digital specimen tracking implementation has increased by nearly 18% across larger diagnostic networks, although infrastructure differences continue influencing deployment speed. Technology providers are responding through localized distribution partnerships, technical support expansion, and modular implementation strategies that reduce integration costs for medium-sized laboratories.

Brazil Market Outlook: Brazil remains the region's largest market because of its extensive diagnostic laboratory network, expanding pharmaceutical sector, and growing investment in healthcare technology. Approximately 45% of major private laboratory groups have accelerated digital identification upgrades supporting workflow automation and regulatory compliance. International suppliers continue strengthening regional partnerships, localized service capabilities, and training programs that improve implementation success while addressing operational diversity across public and private laboratory environments.

Infrastructure investment reshapes laboratory capabilities

The Middle East & Africa market is advancing through healthcare infrastructure investment, laboratory modernization, and expanding biotechnology capabilities. The region accounts for approximately 3.4% of global demand, with increasing deployment of automated identification systems across reference laboratories and specialized healthcare facilities. Laboratory digitalization projects have improved specimen traceability by nearly 20% in newly modernized institutions. Global technology companies are expanding strategic partnerships with healthcare providers while supporting infrastructure upgrades and workforce development programs to improve long-term operational efficiency.

Saudi Arabia Market Outlook: Saudi Arabia leads regional investment through large-scale healthcare transformation programs, advanced hospital development, and expanding laboratory infrastructure. More than 40% of newly established tertiary healthcare laboratories incorporate integrated identification technologies during commissioning, improving digital workflow management and regulatory compliance. Technology vendors continue expanding regional implementation teams, software partnerships, and training initiatives to support national healthcare modernization priorities and strengthen laboratory operational excellence.

Thermo Fisher Scientific, Zebra Technologies, Brady Corporation, Honeywell, and GA International compete directly for enterprise laboratory identification projects, while specialized software vendors challenge hardware manufacturers through integrated digital ecosystems. Global technology leaders compete against regional labeling suppliers on platform integration, whereas OEMs compete with software-driven innovators on workflow intelligence. The top five players collectively control approximately 48% of the market, creating a moderately consolidated structure. Competition centers on technology integration, deployment speed, customization, and lifecycle service rather than hardware pricing alone. AI-enabled identification platforms improve workflow efficiency by nearly 30%, RFID solutions reduce tracking time by about 35%, and localized manufacturing lowers delivery lead times by approximately 18%. Companies strengthen market position through cloud partnerships, manufacturing expansion, interoperable software development, and selective vertical integration. Competitive momentum is shifting toward intelligent end-to-end laboratory ecosystems instead of standalone identification products. High regulatory validation requirements and software interoperability remain key entry barriers. Sustainable leadership demands integrated platforms, rapid deployment capability, strong compliance expertise, and scalable customer support.

Thermo Fisher Scientific

Zebra Technologies

Brady Corporation

Honeywell

GA International

SATO Holdings Corporation

Brother Industries, Ltd.

Datalogic S.p.A.

Toshiba Tec Corporation

Citizen Systems Japan Co., Ltd.

Seiko Epson Corporation

TSC Auto ID Technology Co., Ltd.

Advanced laboratory identification increasingly combines AI-assisted verification, RFID tracking, cloud-connected Laboratory Information Systems, and intelligent barcode platforms into unified operational environments. More than 60% of newly digitalized enterprise laboratories deploy integrated identification ecosystems instead of isolated hardware solutions. AI-assisted validation improves specimen identification accuracy by approximately 32%, while RFID-enabled tracking reduces manual search time by nearly 35%, enabling faster laboratory throughput and stronger regulatory compliance across distributed facilities.

Traditional barcode-only workflows remain essential for routine operations, but integrated AI and RFID platforms outperform legacy identification systems by reducing manual intervention by approximately 30% and lowering operational errors by nearly 28%. Large pharmaceutical manufacturers and diagnostic laboratory networks benefit most because synchronized identification, asset tracking, and workflow automation improve productivity without increasing workforce requirements. Software interoperability has become a stronger competitive differentiator than hardware performance, encouraging vendors to prioritize cloud integration and modular platform architectures.

Between 2026 and 2028, edge computing, digital twins for laboratory operations, and IoT-enabled smart labeling are expected to reshape enterprise deployment strategies. Automated identification adoption is projected to exceed 70% across advanced laboratory networks, strengthening predictive workflow management and remote asset visibility. Organizations investing now in interoperable digital ecosystems will secure faster validation, stronger operational resilience, lower compliance costs, and durable competitive differentiation as laboratory automation becomes increasingly data-driven.

October 2024: GA International (LabTAG) partnered with eLabNext to integrate laboratory identification labels with a digital laboratory platform, enabling seamless sample management and workflow automation across research laboratories. Compatibility covers 100% of LabTAG label portfolios, strengthening end-to-end traceability and laboratory efficiency.

June 2025: Brady Corporation introduced industrial barcode readers delivering 99.995% decoding accuracy using advanced image-processing technology, enhancing laboratory identification reliability and reducing scanning failures in regulated environments. The innovation strengthens high-throughput laboratory automation and compliance-focused identification workflows. Source: industryemea.com

April 2026: Brady EMEA and Caretag formed a strategic partnership combining identification technology with UHF RFID surgical instrument tracking. The integrated solution enables instrument packing processes over 33% faster than conventional DataMatrix scanning while improving lifecycle traceability and regulatory compliance for hospitals. Source: caretag.eu

May 2026: Zebra Technologies partnered with SK&T to deploy passive UHF RFID for real-time pharmacy medication inventory visibility, replacing manual stock verification with automated tracking. The solution delivers item-level inventory monitoring, improving replenishment accuracy, reducing stock discrepancies, and strengthening pharmaceutical supply-chain operations. Source: rfidnews.co.uk

This report provides comprehensive analysis of the global Lab Identification Technologies Market across Barcode Systems, RFID Systems, Label Printers, Sample Tracking, and Laboratory Information Systems. It evaluates key applications including Sample Identification, Specimen Tracking, Asset Management, Inventory Management, and Workflow Automation, together with demand across Hospitals, Diagnostic Laboratories, Research Institutes, Pharmaceutical Companies, and Biotechnology Companies. The assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa while examining enterprise adoption patterns, deployment maturity, and technology integration trends.

The report incorporates competitive benchmarking, innovation analysis, regional deployment dynamics, and strategic technology developments shaping market evolution between 2026 and 2033. More than 60% enterprise digitalization trends, laboratory automation progress, identification workflow modernization, and interoperability priorities are assessed alongside emerging niche opportunities. The findings support investment planning, product portfolio optimization, expansion strategy, partnership evaluation, competitive positioning, and long-term decision-making for technology providers, manufacturers, healthcare organizations, and institutional laboratory operators.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 1990 Million |

Market Revenue in 2033 | USD 3343.24 Million |

CAGR (2026 - 2033) | 6.7% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Thermo Fisher Scientific, Zebra Technologies, Brady Corporation, Honeywell, GA International, SATO Holdings Corporation, Brother Industries, Ltd., Datalogic S.p.A., Toshiba Tec Corporation, Citizen Systems Japan Co., Ltd., Seiko Epson Corporation, TSC Auto ID Technology Co., Ltd. |

Customization & Pricing | Available on Request (10% Customization is Free) |