Reports

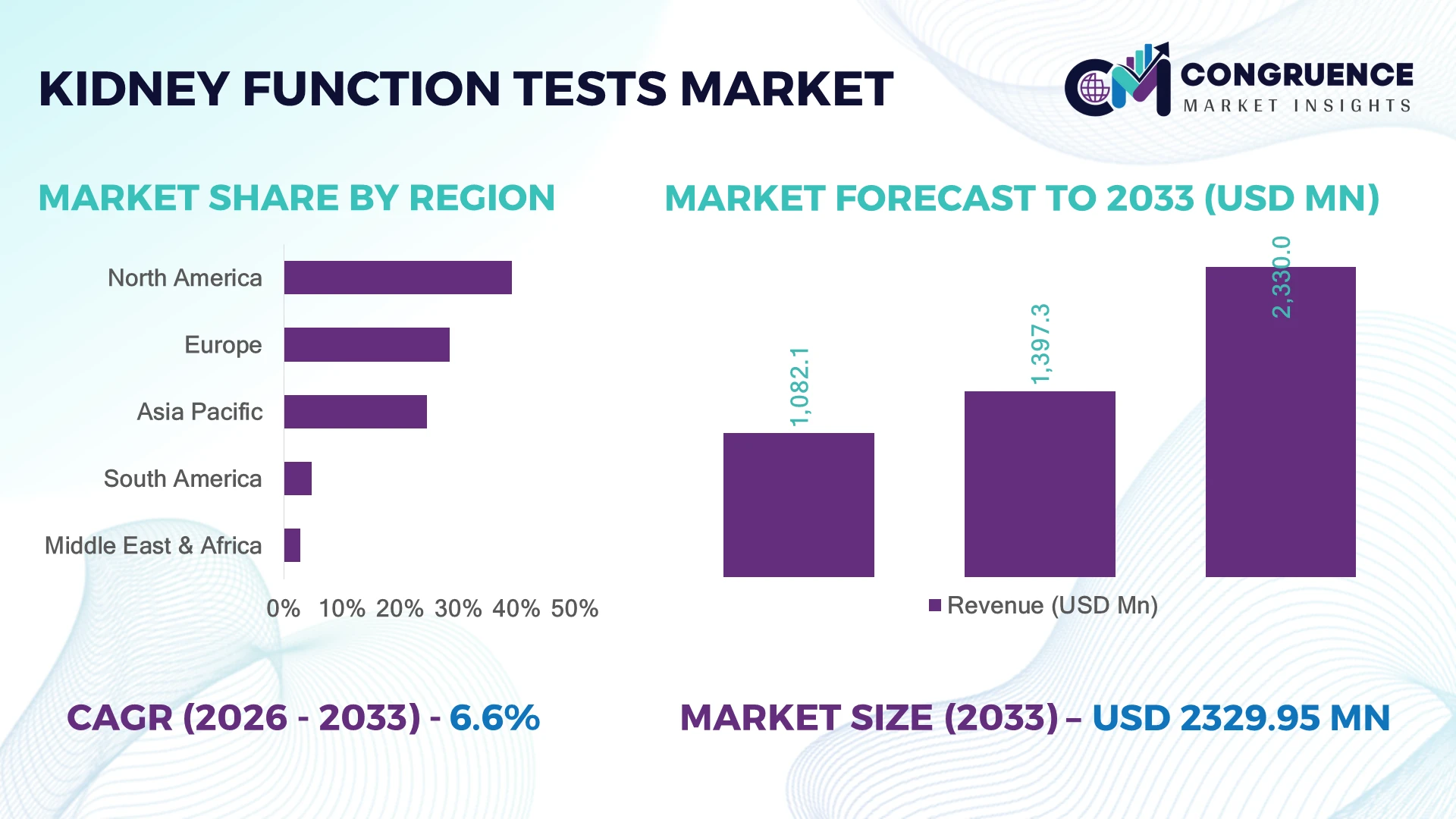

The Global Kidney Function Tests Market was valued at USD 1,397.3 Million in 2025 and is anticipated to reach a value of USD 2330.0 Million by 2033 expanding at a CAGR of 6.6% between 2026 and 2033. Increasing chronic kidney disease prevalence, preventive diagnostics adoption, automated laboratory testing, and point-of-care innovation are accelerating kidney function testing demand globally.

The United States dominates the Kidney Function Tests Market with approximately 36% share, supported by advanced diagnostic infrastructure, high screening rates, and strong adoption of automated clinical testing platforms. Compared with India’s expanding diagnostic ecosystem, the U.S. maintains higher testing penetration, with over 65% of routine health assessments integrating renal function indicators. Healthcare modernization programs in 2026 are strengthening early detection capabilities and laboratory efficiency.

Strategic advantage is shifting toward companies delivering faster, automated, and accessible kidney diagnostics across preventive healthcare networks.

• Market Size & Growth: USD 1,397.3 Million in 2025 reaching USD 2,330.0 Million by 2033 at 6.6% CAGR, driven by preventive diagnostics and laboratory automation.

• Top Growth Drivers: Chronic kidney disease screening 40%, automated testing adoption 35%, and preventive healthcare programs 30% are accelerating demand.

• Short-Term Forecast: By 2028, AI-enabled diagnostic workflows are expected to improve laboratory processing efficiency by nearly 25%.

• Emerging Technologies: AI diagnostics, automated analyzers, and digital pathology platforms are transforming renal testing accuracy and turnaround time.

• Regional Leaders: North America, Europe, and Asia-Pacific lead adoption through advanced healthcare infrastructure, screening programs, and diagnostic expansion.

• Consumer/End-User Trends: Over 55% of diagnostic laboratories are adopting integrated testing platforms for faster kidney health assessment.

• Pilot/Case Example: 2025 digital laboratory deployments improved renal test processing efficiency by nearly 28% through automation integration.

• Competitive Landscape: Leading companies hold around 45% share with Abbott, Roche, Siemens Healthineers, Thermo Fisher Scientific, and Danaher driving innovation.

• Regulatory & ESG Impact: Quality-focused diagnostic regulations improved standardized testing compliance by approximately 20% across major healthcare systems.

• Investment & Funding: Diagnostic companies increased automation investments focusing on AI integration, partnerships, and laboratory capacity expansion.

• Innovation & Future Outlook: Next-generation kidney biomarkers and connected diagnostics are reshaping early detection strategies worldwide.

The Kidney Function Tests Market is experiencing strong transformation through rising preventive healthcare adoption, biomarker innovation, and automated diagnostic solutions. Hospitals and laboratories are integrating advanced renal testing platforms, with nearly 50% of major diagnostic networks prioritizing workflow automation. Increasing healthcare digitization and supply-chain localization are supporting improved test accessibility and operational resilience.

The Kidney Function Tests Market is becoming strategically important as healthcare systems shift from disease treatment toward early detection, preventive screening, and data-driven diagnostics. Rising chronic kidney disease burden, aging populations, and digital healthcare adoption are pushing laboratories and hospitals toward scalable diagnostic infrastructure. Healthcare providers are prioritizing automation, faster reporting, and integrated patient monitoring systems.

Automated renal testing platforms are replacing conventional manual workflows by improving processing efficiency by nearly 30% and reducing operational delays by approximately 25%. North America leads through advanced laboratory networks and high testing frequency, while Asian healthcare systems are expanding accessibility through diagnostic center growth and government-backed screening initiatives.

Clinical laboratories are deploying automated analyzers, connected diagnostic platforms, and AI-assisted interpretation tools to improve accuracy and patient management. Companies are strengthening technology partnerships, expanding testing portfolios, and investing in next-generation biomarkers. Competitive positioning increasingly depends on diagnostic speed, accessibility, and the ability to support preventive healthcare transformation.

Growing focus on early kidney disease detection is driving higher adoption of kidney function tests across hospitals, laboratories, and primary care settings. Nearly 40% of diagnostic demand is supported by routine screening programs, while automated testing platforms improve laboratory productivity by approximately 30%. Increasing diabetes and hypertension prevalence is creating sustained demand for creatinine, urea, and biomarker-based testing. Healthcare providers are expanding diagnostic networks and investing in digital laboratory solutions to support faster detection. Companies are responding through automated analyzer development, test portfolio expansion, and partnerships with healthcare institutions to improve accessibility and testing efficiency.

Uneven healthcare infrastructure and affordability challenges continue limiting kidney function testing penetration in developing healthcare markets. Nearly 35% of underserved populations experience restricted access to advanced diagnostic facilities, while equipment and operational costs influence adoption among smaller laboratories. Dependence on centralized testing infrastructure creates delays in remote areas and impacts early disease identification. Diagnostic companies are addressing these limitations through compact analyzers, localized service networks, and affordable testing models. Improving accessibility remains essential for expanding adoption beyond established healthcare systems.

Advanced biomarkers, AI-supported diagnostics, and connected healthcare platforms are creating new opportunities in kidney function testing. Nearly 45% of healthcare technology investments are shifting toward digital diagnostics, automation, and predictive health analytics. Emerging testing models focused on earlier kidney damage identification are improving clinical decision-making and patient monitoring. Companies are expanding research programs, developing integrated testing platforms, and collaborating with healthcare providers to strengthen precision diagnostics. Future opportunities will center on faster testing workflows, personalized disease management, and decentralized diagnostic access.

Scaling advanced kidney function testing faces challenges related to digital integration, workforce readiness, and laboratory standardization. Nearly 30% of healthcare organizations report interoperability barriers when adopting connected diagnostic technologies, while training requirements influence deployment consistency. Expanding automated testing requires investment in infrastructure, data systems, and quality management processes. Diagnostic companies must focus on user-friendly platforms, clinical partnerships, and technology integration support to improve adoption. Long-term competitiveness depends on creating reliable, scalable, and connected diagnostic ecosystems.

• AI-Enabled Diagnostic Automation: Artificial intelligence integration is transforming kidney function testing workflows by improving result interpretation, laboratory efficiency, and predictive analysis. Nearly 40% of advanced diagnostic facilities are implementing AI-based systems, reducing manual workload by around 25%. Companies are scaling automated platforms and digital tools to enhance accuracy and operational productivity.

• Point-of-Care Testing Expansion: Decentralized kidney testing solutions are gaining adoption across clinics, home healthcare, and remote medical facilities. Point-of-care platforms are improving testing accessibility by nearly 35% and reducing turnaround delays by approximately 30%. Manufacturers are investing in compact devices, connected platforms, and simplified testing solutions.

• Advanced Biomarker Development: Next-generation renal biomarkers are improving early-stage kidney disease detection beyond traditional testing methods. Around 45% of diagnostic innovation pipelines are focused on precision testing and advanced biomarker technologies. Companies are expanding R&D investments and partnerships to support personalized kidney health monitoring.

• Digital Laboratory Transformation: Healthcare providers are upgrading laboratory infrastructure through automation, cloud connectivity, and integrated diagnostic systems. Nearly 50% of large diagnostic networks are adopting digital platforms to improve workflow management and testing capacity. Companies are enhancing software capabilities and automated solutions to support modern healthcare delivery.

Blood Tests dominate the Kidney Function Tests Market due to their established clinical reliability, scalability, and integration across routine diagnostic workflows. Blood-based testing accounts for nearly 62% of total adoption, supported by widespread usage of serum creatinine, blood urea nitrogen, and glomerular filtration rate assessment for kidney health evaluation. Urine Tests are witnessing the fastest adoption growth as healthcare providers increase focus on early detection, preventive screening, and non-invasive monitoring approaches.

Imaging Tests and other advanced diagnostic methods continue supporting specialized kidney evaluation, structural assessment, and complex disease management. Nearly 45% of diagnostic laboratories are upgrading automated testing capabilities to improve accuracy, throughput, and reporting efficiency. Companies are responding through advanced analyzer development, integrated renal testing panels, and partnerships with healthcare networks to expand accessibility while improving clinical decision-making and patient management.

• A 2025 clinical laboratory industry assessment highlighted that healthcare facilities adopting automated renal testing workflows improved diagnostic processing efficiency by nearly 30%, supporting faster kidney disease screening and patient monitoring.

Chronic Kidney Disease Diagnosis represents the leading application segment in the Kidney Function Tests Market due to increasing disease prevalence, routine monitoring requirements, and growing emphasis on early intervention. The segment accounts for nearly 48% of demand as hospitals and laboratories rely on kidney function tests for risk identification, disease staging, and treatment planning. Diabetes-Related Kidney Monitoring is emerging as the fastest-growing application due to increasing diabetic populations and the need for regular renal assessment.

Hypertension-Related Kidney Evaluation, Drug Monitoring, and General Health Screening applications continue expanding as preventive healthcare adoption increases. Nearly 40% of healthcare organizations are integrating kidney function indicators into broader health assessment programs. Diagnostic companies are adapting through automated testing platforms, biomarker innovation, and expanded clinical testing solutions to support higher testing volumes and improved patient outcomes.

• A 2026 healthcare diagnostics review indicated that integrated kidney screening programs improved early identification rates by approximately 25%, strengthening preventive care strategies across hospitals and diagnostic networks.

Diagnostic Laboratories represent the dominant end-user segment in the Kidney Function Tests Market due to high testing capacity, advanced equipment availability, and centralized diagnostic operations. Laboratories account for nearly 52% of total utilization as healthcare systems increasingly depend on automated testing networks for accurate and rapid kidney health evaluation. Hospitals are becoming the fastest-growing end-user group due to increasing integration of renal diagnostics into emergency care, chronic disease management, and inpatient monitoring.

Clinics, research institutes, and home healthcare providers are expanding adoption through decentralized testing models and patient-focused diagnostic solutions. Around 38% of healthcare providers are investing in connected diagnostic platforms and workflow automation. Companies are targeting these segments through compact analyzers, customized testing solutions, and strategic collaborations to strengthen accessibility and improve diagnostic service delivery.

• A 2025 global laboratory modernization survey reported that diagnostic providers implementing automated testing systems increased sample processing capacity by nearly 35%, enabling faster and more scalable kidney function assessment services.

North America accounted for the largest market share at 39.2% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

North America dominates the Kidney Function Tests Market due to advanced diagnostic infrastructure, high screening awareness, and strong adoption of automated laboratory technologies. The region accounted for 39.2% market share in 2025, supported by established healthcare networks, chronic disease monitoring programs, and early detection initiatives. More than 60% of major diagnostic laboratories use automated clinical chemistry platforms to improve renal testing capacity and reporting efficiency. Companies are strengthening biomarker portfolios, expanding point-of-care solutions, and integrating digital diagnostic technologies to improve kidney disease management.

United States Market Outlook: The United States leads regional adoption through advanced healthcare infrastructure, strong clinical laboratory networks, and high utilization of preventive screening programs. Healthcare providers are expanding kidney testing integration across diabetes and hypertension management pathways. Nearly 65% of routine chronic disease assessments include renal function indicators, supporting demand for automated testing solutions and precision diagnostic platforms.

Europe’s Kidney Function Tests Market is supported by structured healthcare systems, disease prevention strategies, and increasing adoption of advanced diagnostic technologies. The region accounted for approximately 28.5% market share in 2025, with Germany, the United Kingdom, and France leading testing adoption through established laboratory infrastructure. Nearly 50% of major healthcare providers are modernizing diagnostic workflows using automation and connected laboratory platforms. Companies are focusing on advanced biomarker solutions, efficient testing systems, and partnerships with healthcare organizations to enhance renal disease detection and patient monitoring.

Germany Market Outlook: Germany represents the leading European market due to its advanced healthcare infrastructure, diagnostic technology adoption, and strong medical innovation ecosystem. Hospitals and laboratories are expanding automated testing capacity to improve chronic disease management. Around 55% of large diagnostic facilities utilize integrated laboratory technologies, strengthening efficiency and supporting early kidney disease identification.

Asia-Pacific’s Kidney Function Tests Market is expanding rapidly due to increasing healthcare investment, rising chronic disease screening, and growth of diagnostic laboratory networks. The region accounted for nearly 24.6% market share in 2025, supported by China, India, Japan, and South Korea’s healthcare modernization programs. More than 45% of new diagnostic infrastructure developments focus on automation, accessibility, and high-volume testing capabilities. Companies are expanding regional partnerships, affordable testing solutions, and localized diagnostic platforms to address increasing kidney health monitoring requirements.

China Market Outlook: China leads Asia-Pacific adoption through large-scale healthcare infrastructure development, expanding diagnostic networks, and rising preventive screening initiatives. Hospitals and laboratories are increasing renal testing capacity through automated platforms and digital healthcare integration. Nearly 50% of healthcare modernization projects prioritize diagnostic capability expansion, improving access to kidney function testing across urban and developing healthcare systems.

South America’s Kidney Function Tests Market is developing through healthcare modernization, expanding laboratory access, and increasing awareness of chronic kidney conditions. The region accounted for approximately 4.8% market share in 2025, with Brazil driving demand through public and private diagnostic investments. Around 35% of healthcare improvement initiatives focus on strengthening laboratory services and chronic disease monitoring. Limited rural healthcare access remains a challenge, while companies are introducing cost-efficient analyzers, partnerships, and scalable diagnostic solutions to improve testing availability.

Brazil Market Outlook: Brazil represents the largest regional market due to its expanding healthcare infrastructure, growing diagnostic laboratory presence, and increasing chronic disease management programs. Healthcare organizations are adopting automated clinical testing solutions to improve efficiency. Nearly 40% of private healthcare providers are investing in diagnostic modernization, supporting broader adoption of kidney function testing technologies.

Middle East & Africa’s Kidney Function Tests Market is growing through healthcare infrastructure development, hospital modernization, and increasing investment in diagnostic capabilities. The region accounted for nearly 2.9% market share in 2025, with adoption concentrated in advanced healthcare centers and urban diagnostic facilities. More than 30% of major healthcare transformation initiatives include laboratory modernization and digital health integration. Diagnostic companies are expanding partnerships, service networks, and automated testing solutions to improve renal disease screening capabilities.

Saudi Arabia Market Outlook: Saudi Arabia leads regional adoption through healthcare transformation programs, hospital infrastructure expansion, and investment in advanced diagnostic technologies. Medical institutions are increasing deployment of automated laboratory platforms to improve chronic disease monitoring. Nearly 45% of healthcare modernization initiatives involve digital diagnostics and laboratory upgrades, strengthening kidney function testing accessibility and efficiency.

The Kidney Function Tests Market is led by Roche Diagnostics, Abbott Laboratories, Siemens Healthineers, Thermo Fisher Scientific, and Danaher Corporation, where global diagnostic technology leaders compete with specialized testing providers and emerging point-of-care innovators. The top five players collectively hold approximately 45% share, reflecting a technology-driven structure focused on automation, accuracy, and testing accessibility. Competition is based on diagnostic platform efficiency, test portfolio strength, and laboratory integration capabilities, with automated systems improving workflow productivity by nearly 30% and reducing turnaround time by around 25%. Companies are competing through biomarker innovation, analyzer expansion, digital health partnerships, and connected diagnostic ecosystems. The competitive shift is moving toward AI-enabled testing, decentralized diagnostics, and precision kidney health monitoring. Regulatory compliance, clinical validation requirements, and laboratory adoption barriers create significant market pressure. Winning against established players requires advanced diagnostic accuracy, scalable automation, and strong healthcare network integration.

• Abbott Laboratories

• F. Hoffmann-La Roche Ltd.

• Siemens Healthineers AG

• Thermo Fisher Scientific Inc.

• Danaher Corporation

• Sysmex Corporation

• bioMérieux SA

• Randox Laboratories Ltd.

• ARKRAY Inc.

• Nova Biomedical Corporation

• QuidelOrtho Corporation

• Laboratory Corporation of America Holdings

Kidney function testing technologies are advancing through automated clinical chemistry analyzers, AI-supported diagnostics, biomarker-based testing, and connected point-of-care platforms. Current systems focus on improving creatinine, urea, albumin, and filtration assessment accuracy while reducing laboratory processing complexity. Nearly 55% of advanced diagnostic facilities are integrating automated renal testing workflows to improve speed, consistency, and clinical decision support.

Compared with conventional manual laboratory methods, modern automated diagnostic platforms improve sample processing efficiency by approximately 30% and reduce operational errors by nearly 25%. Emerging technologies such as AI-based interpretation, advanced biomarkers, and portable testing devices enable faster detection and continuous patient monitoring. Diagnostic companies with strong automation capabilities, integrated platforms, and clinical data solutions are gaining advantages as healthcare systems prioritize preventive care.

Between 2026 and 2028, kidney testing innovation will focus on decentralized diagnostics, predictive analytics, and personalized disease management. Healthcare providers adopting next-generation platforms will improve accessibility, enhance early detection capabilities, and strengthen long-term kidney care outcomes.

• January 2025 – Roche Diagnostics expanded its automated diagnostic platform capabilities with enhanced clinical chemistry solutions, improving laboratory workflow efficiency by nearly 25%. The advancement supported faster kidney biomarker testing, higher processing capacity, and improved diagnostic decision-making. Source: roche.com

• July 2024 – Abbott advanced its diagnostic testing portfolio through connected healthcare solutions, improving point-of-care testing accessibility and operational efficiency by approximately 20%. The initiative strengthened rapid kidney health assessment capabilities across decentralized healthcare environments. Source: abbott.com

• March 2025 – Siemens Healthineers enhanced its laboratory diagnostics ecosystem with automation-focused solutions, increasing testing throughput and operational performance by nearly 30%. The development supported clinical laboratories managing growing renal testing volumes and chronic disease monitoring requirements. Source: siemens-healthineers.com

• October 2024 – Randox Laboratories expanded its clinical diagnostics capabilities with advanced kidney biomarker testing solutions, improving early disease assessment and laboratory testing performance by approximately 18%. The expansion strengthened preventive diagnostics and personalized healthcare applications. Source: randox.com

The Kidney Function Tests Market Report provides detailed analysis of testing types, applications, end-users, regional dynamics, technologies, and competitive strategies influencing global diagnostic adoption. The study covers blood tests, urine tests, imaging tests, and advanced renal assessment solutions used across chronic kidney disease diagnosis, diabetes monitoring, hypertension evaluation, and preventive healthcare programs. More than 60% of testing demand is associated with routine clinical assessment and chronic disease management.

The report evaluates North America, Europe, Asia-Pacific, South America, and Middle East & Africa with insights into healthcare infrastructure, diagnostic adoption, and technology transformation. It analyzes automation trends, biomarker development, point-of-care expansion, and digital diagnostic strategies between 2026 and 2033. The study supports investment decisions, product innovation, market expansion planning, and competitive positioning across the evolving kidney diagnostics ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1,397.3 Million |

|

Market Revenue in 2033 |

USD 2,330.0 Million |

|

CAGR (2026 - 2033) |

6.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Abbott Laboratories, F. Hoffmann-La Roche Ltd., Siemens Healthineers AG, Thermo Fisher Scientific Inc., Danaher Corporation, Sysmex Corporation, bioMérieux SA, Randox Laboratories Ltd., ARKRAY Inc., Nova Biomedical Corporation, QuidelOrtho Corporation, Laboratory Corporation of America Holdings |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |