Reports

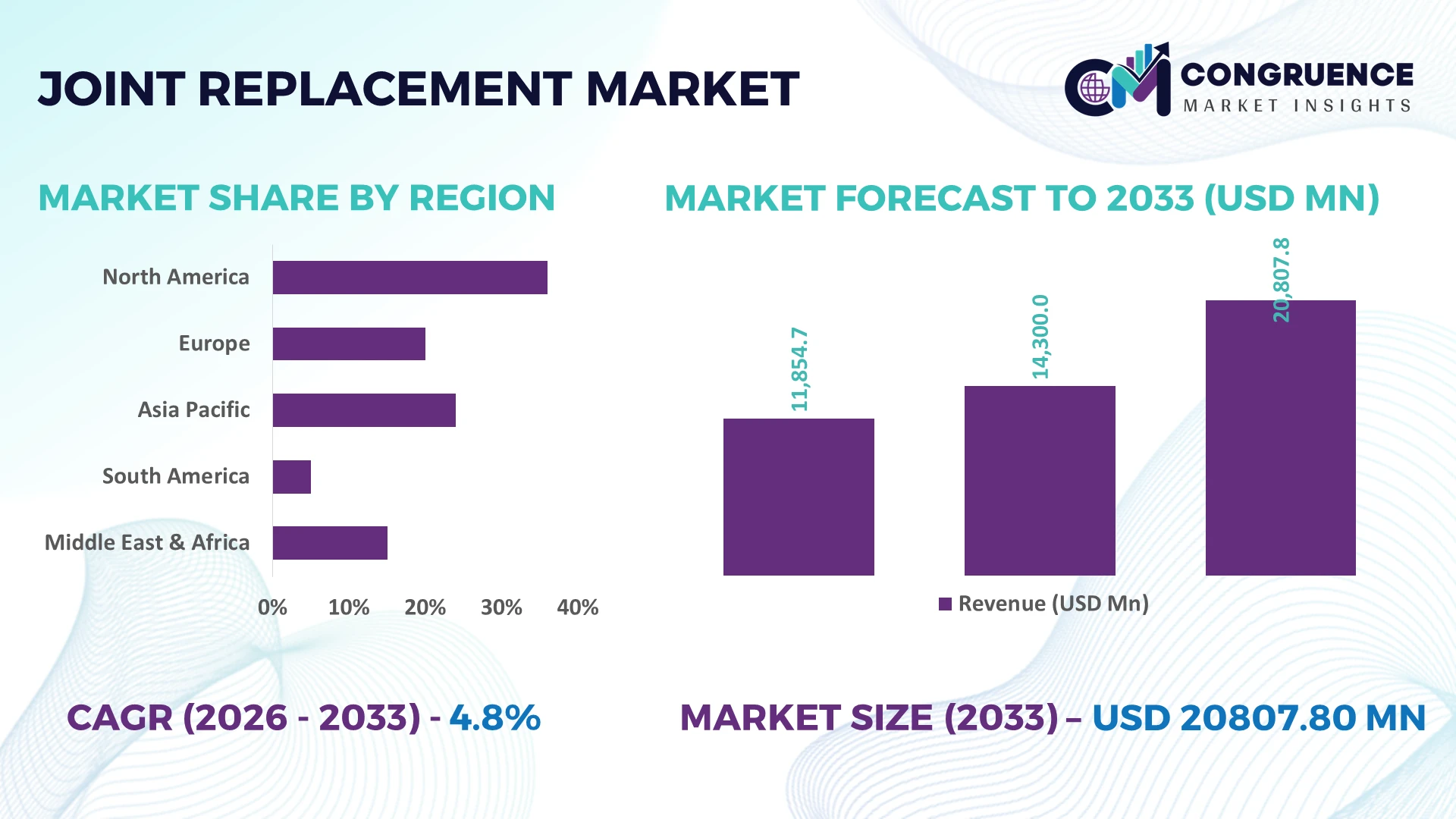

The Global Joint Replacement Market was valued at USD 14300 Million in 2025 and is anticipated to reach a value of USD 20807.8 Million by 2033 expanding at a CAGR of 4.8% between 2026 and 2033. Market expansion is driven by rapid adoption of robotic-assisted orthopedic surgery, advanced implant biomaterials, outpatient joint replacement pathways, and digitally integrated surgical planning that improves procedural precision while reducing revision rates.

The United States dominates the global joint replacement market with approximately 38% of global procedure volume, supported by annual orthopedic investments exceeding USD 7 billion, widespread robotic-assisted surgery adoption above 30%, and strong reimbursement infrastructure. Compared with Germany, where advanced orthopedic implant utilization continues expanding through hospital modernization programs, the U.S. benefits from larger procedural capacity despite ongoing global supply-chain realignments following evolving international trade policies in 2026. This leadership strengthens innovation pipelines and reinforces long-term competitive positioning for manufacturers expanding premium implant portfolios.

Strategic implication: Companies prioritizing robotic ecosystems, localized manufacturing, and value-based orthopedic solutions are positioned to capture sustainable competitive advantages across high-growth healthcare markets.

Market Size & Growth: USD 14300 Million (2025) to USD 20807.8 Million (2033) at 4.8% CAGR, supported by robotic surgery integration and advanced implant manufacturing.

Top Growth Drivers: Robotic procedures +30%, outpatient surgeries +24%, highly durable implant adoption +18%.

Short-Term Forecast: By 2028, surgical workflow efficiency improves 20% while average hospital implant inventory costs decline 12%.

Emerging Technologies: AI surgical planning, robotic-assisted systems, and 3D-printed implants accelerate precision and implant longevity.

Regional Leaders: North America exceeds USD 8.1 billion, Europe reaches USD 5.4 billion, Asia-Pacific surpasses USD 4.8 billion, driven by hospital modernization and regional expansion.

Consumer/End-User Trends: More than 35% of eligible procedures shift toward minimally invasive and rapid-recovery treatment pathways.

Pilot/Case Example: 2026 orthopedic digital navigation programs improved implant alignment accuracy by approximately 18% across participating hospitals.

Competitive Landscape: Leading manufacturers collectively hold nearly 60% market share, with Zimmer Biomet, Stryker, DePuy Synthes, Smith+Nephew, and Exactech driving innovation.

Regulatory & ESG Impact: Sustainable manufacturing initiatives reduce production waste by nearly 15% while strengthening global compliance standards.

Investment & Funding: More than USD 2.5 billion supports manufacturing expansion, strategic partnerships, and smart orthopedic technology development amid supply-chain diversification.

Innovation & Future Outlook: Smart implants, digital patient monitoring, and personalized orthopedic solutions accelerate next-generation competitive differentiation.

Growing demand for knee, hip, and shoulder replacement procedures continues reshaping the Joint Replacement Market as hospitals expand robotic operating capabilities and adopt patient-specific implants. Advanced biomaterials and AI-assisted surgical planning improve procedural consistency, while nearly 28% of leading orthopedic centers are integrating digital care pathways. Manufacturing localization and evolving medical device regulations further strengthen operational resilience, setting the stage for the strategic market analysis that follows.

The Joint Replacement Market has become a strategic priority as healthcare providers compete on surgical precision, patient outcomes, and operational efficiency rather than procedure volume alone. Digital orthopedic platforms, robotic-assisted surgery, and localized implant manufacturing are reshaping competitive positioning, while supply-chain restructuring since 2026 has accelerated regional sourcing strategies for critical implant components. Manufacturers increasingly align production with hospital networks to improve delivery reliability and reduce procurement risk.

Robotic-assisted joint replacement systems achieve implant placement accuracy improvements of approximately 20% while reducing average operating room time by nearly 15% compared with conventional manual procedures, lowering overall procedural costs through fewer revisions and shorter hospital stays. The United States leads large-scale deployment through integrated robotic surgery programs, whereas Japan emphasizes precision navigation and aging-focused orthopedic care with higher adoption across specialized hospitals. Over the next two to three years, digital surgical planning utilization is expected to exceed 40% among major orthopedic centers, supported by expanding AI-enabled workflow integration.

Manufacturers are expanding strategic partnerships with hospital groups, investing in patient-specific implant production, and strengthening regional manufacturing capacity. A growing number of orthopedic providers now combine robotic platforms with digital rehabilitation programs to improve recovery consistency and resource utilization. Companies establishing integrated technology ecosystems and resilient production networks will secure stronger competitive differentiation, improve operational performance, and reinforce long-term leadership across the evolving joint replacement value chain.

Robotic-assisted surgery, advanced biomaterials, and patient-specific implant manufacturing continue transforming orthopedic care by improving procedural precision and long-term implant performance. More than 30% of leading orthopedic hospitals now utilize robotic platforms, while revision surgeries have declined by approximately 15% in digitally assisted procedures. Around 25% of premium implant portfolios incorporate advanced porous materials that enhance biological fixation. Following supply-chain restructuring and domestic manufacturing incentives in the United States, manufacturers are expanding localized production and strategic supplier partnerships. Companies are simultaneously investing in AI-enabled surgical planning, expanding orthopedic training programs, and introducing integrated implant ecosystems, creating stronger clinical differentiation while improving hospital productivity and procurement resilience.

High capital investment requirements and procurement volatility remain significant barriers for wider adoption, particularly among mid-sized healthcare providers. Robotic orthopedic systems can increase initial infrastructure costs by over 35%, while specialized implant inventories raise procurement expenses by approximately 18%. Global dependence on titanium alloys and precision medical-grade components continues exposing manufacturers to supply disruptions and delivery uncertainty. Hospitals in emerging economies frequently delay technology upgrades because reimbursement frameworks evolve more slowly than innovation cycles. To reduce operational risk, companies are expanding localized manufacturing, negotiating long-term supplier agreements, diversifying material sourcing, and standardizing implant platforms that improve inventory management while supporting more predictable production planning.

AI-assisted surgical planning, smart implants, and connected postoperative monitoring are creating measurable opportunities beyond conventional implant sales. Digital rehabilitation platforms improve patient engagement by approximately 22%, while predictive analytics reduce unplanned follow-up interventions by nearly 18%. India is expanding advanced orthopedic infrastructure through private hospital investments, creating favorable conditions for digital orthopedic ecosystems. Manufacturers are increasing investment in patient-specific 3D-printed implants, software-enabled surgical navigation, and integrated data platforms that combine surgical planning with recovery monitoring. The emerging shift toward outcome-based orthopedic care enables companies to differentiate through complete clinical solutions rather than standalone implant products, strengthening long-term customer retention.

Successfully integrating robotics, AI software, imaging platforms, and hospital information systems remains a complex execution challenge. Nearly 27% of healthcare facilities report workflow integration delays during advanced orthopedic technology implementation, while specialist workforce shortages extend deployment timelines by approximately 20%. Germany and other advanced manufacturing countries continue addressing medical engineering talent gaps alongside increasingly rigorous cybersecurity requirements for connected surgical systems. Companies must expand surgeon education programs, strengthen software interoperability, invest in secure digital infrastructure, and collaborate with technology partners to ensure consistent clinical performance. Organizations capable of scaling integrated orthopedic ecosystems efficiently will achieve stronger operational resilience and sustained competitive advantage.

Advanced Robotic Workflow Expansion: Robotic-assisted joint replacement is moving from flagship hospitals into broader orthopedic networks, with robotic procedure volumes increasing by nearly 28% and digital preoperative planning adoption exceeding 40% among major healthcare systems. Standardized workflows reduce operating room time by approximately 15% while improving implant alignment consistency. Following healthcare infrastructure modernization in the United States, manufacturers are expanding robotic platform partnerships, surgeon certification programs, and integrated software ecosystems to accelerate deployment without disrupting existing surgical pathways.

Localized Implant Manufacturing Growth: Orthopedic manufacturers are restructuring production networks by regionalizing implant manufacturing and critical component sourcing after continued supply-chain disruptions. Domestic procurement of selected implant components has increased by roughly 20%, while average lead times have fallen nearly 18%. Companies are investing in additive manufacturing, supplier diversification, and automated quality inspection to improve inventory resilience, shorten delivery cycles, and maintain regulatory compliance across high-volume orthopedic facilities.

Personalized Implant Design Adoption: Patient-specific implants and AI-enabled surgical planning are becoming routine for complex orthopedic cases, improving implant fit by approximately 16% and reducing revision-related complications by nearly 12%. Hospitals in Japan increasingly combine advanced imaging with customized implant production to optimize clinical outcomes. Manufacturers are strengthening software partnerships, expanding digital engineering capabilities, and integrating 3D printing into production strategies to support precision-driven orthopedic care and differentiated product portfolios.

Outpatient Procedure Transformation: Same-day joint replacement continues expanding as enhanced recovery protocols increase outpatient orthopedic procedures by approximately 22% while reducing average hospital stays by nearly 30%. Workforce shortages are encouraging greater procedural standardization and digital rehabilitation monitoring to maintain clinical quality. Companies are responding through ambulatory surgery center collaborations, remote patient engagement platforms, and bundled orthopedic service models that improve operational efficiency while supporting higher patient throughput.

Knee Replacement remains the dominant segment, accounting for approximately 48% of global procedure volume because of its broad clinical applicability, standardized surgical pathways, and strong reimbursement support. High osteoarthritis prevalence and continuous robotic integration reinforce procedural scalability across large hospital systems. Hip Replacement follows as a mature segment with consistent adoption driven by aging populations and improved implant longevity. Meanwhile, Shoulder Replacement is the fastest-growing category, supported by expanding sports medicine programs and reverse shoulder implant innovation, with annual procedure adoption increasing by nearly 14%. Manufacturers continue prioritizing advanced polyethylene components, navigation technologies, and personalized implant systems to strengthen clinical outcomes.

Ankle Replacement and Elbow Replacement represent smaller but strategically important segments addressing complex orthopedic conditions through specialized implants and precision instrumentation. Nearly 35% of new orthopedic product launches emphasize patient-specific implant technologies across multiple joint categories, reflecting shifting investment priorities. Companies are expanding surgeon education, strengthening orthopedic distribution partnerships, and increasing localized manufacturing capacity to support differentiated portfolios and broader procedural adoption across both established and emerging joint replacement categories.

Osteoarthritis remains the leading application, representing nearly 70% of joint replacement procedures due to rising longevity, higher obesity prevalence, and earlier clinical intervention. Standardized treatment pathways and improved implant durability support large-scale deployment across hospitals. Revision Surgery is emerging as the fastest-growing application, expanding by approximately 13% as first-generation implants reach replacement cycles and advanced revision technologies improve long-term patient outcomes. Manufacturers are developing modular implant systems, enhanced fixation technologies, and digital planning platforms to improve complex surgical efficiency.

Trauma and Sports Injuries continue benefiting from increasing participation in active lifestyles and rapid orthopedic intervention programs, while Rheumatoid Arthritis maintains a specialized but clinically significant role supported by advances in biologic therapies and targeted patient selection. Around 32% of orthopedic centers have integrated AI-assisted surgical planning into complex application workflows, improving procedural consistency. Companies are expanding clinical collaborations, investing in specialized implant portfolios, and optimizing digital care pathways to strengthen competitive positioning across evolving orthopedic treatment applications.

Hospitals remain the dominant end-user because of comprehensive surgical infrastructure, multidisciplinary orthopedic teams, and access to advanced robotic systems, accounting for approximately 62% of procedural deployment. Their ability to manage complex and revision surgeries sustains demand concentration despite rising outpatient treatment models. Ambulatory Surgical Centers represent the fastest-growing end-user segment, with procedure volumes increasing by nearly 18% as minimally invasive techniques, enhanced recovery pathways, and reimbursement optimization improve outpatient feasibility. Manufacturers increasingly customize implant portfolios and digital workflow solutions specifically for these high-efficiency facilities.

Orthopedic Clinics continue expanding specialized consultation and follow-up services, while Rehabilitation Centers strengthen recovery outcomes through digitally monitored therapy programs. Specialty Clinics are growing in complex musculoskeletal treatment supported by focused expertise and integrated diagnostic capabilities. More than 30% of orthopedic technology partnerships now target ambulatory care environments, reflecting changing procurement priorities. Companies are introducing flexible pricing strategies, integrated service agreements, and ecosystem partnerships that improve customer retention while addressing distinct operational requirements across every end-user category.

North America accounted for the largest market share at 41.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 6.3% CAGR between 2026 and 2033.

Robotic Surgery Leadership Strengthens Clinical Standardization

North America maintains the highest deployment concentration through advanced orthopedic infrastructure, widespread robotic-assisted surgery, and integrated hospital networks. The region performs more than 40% of global high-value robotic joint replacement procedures, supported by mature reimbursement systems and continuous investment in digital operating rooms. Nearly 35% of large orthopedic centers utilize AI-assisted surgical planning as part of routine workflows, improving procedural consistency and resource utilization. Implant manufacturers continue expanding localized production, strategic hospital partnerships, and surgeon training initiatives to strengthen supply resilience while accelerating adoption of next-generation orthopedic technologies across both inpatient and outpatient settings.

United States Market Outlook: The United States remains the regional technology leader through its extensive orthopedic hospital network, high robotic surgery penetration, and strong medical device innovation ecosystem. More than 30% of complex joint replacement procedures now involve robotic assistance in major health systems, while domestic manufacturers continue expanding precision implant production and digital surgery platforms. Strategic collaboration between healthcare providers and orthopedic technology companies supports faster clinical deployment, enhanced procedural standardization, and improved long-term implant performance.

Manufacturing Modernization Supports Premium Orthopedic Care

Europe benefits from advanced implant manufacturing, strict medical device quality standards, and continuous modernization of orthopedic services. Germany, France, and the United Kingdom collectively account for a substantial share of regional procedure volumes through specialized orthopedic hospitals and established clinical expertise. Approximately 28% of implant manufacturers have expanded automation within precision manufacturing facilities to improve production efficiency and quality consistency. Companies increasingly emphasize sustainable manufacturing, digital surgical planning, and strategic supplier diversification to strengthen operational resilience while supporting premium orthopedic treatment pathways.

Germany Market Outlook: Germany leads European orthopedic manufacturing through advanced engineering capabilities, highly specialized medical technology clusters, and strong clinical research collaboration. Automated implant production continues expanding across precision manufacturing facilities, while digital orthopedic navigation systems are increasingly integrated into major surgical centers. Continued investment in high-value implant technologies and surgeon education programs strengthens Germany's competitive position as a strategic innovation and production hub for advanced joint replacement solutions.

Healthcare Expansion Accelerates Procedural Scale

Asia-Pacific is experiencing rapid deployment driven by expanding healthcare infrastructure, rising orthopedic procedure volumes, and increasing access to advanced implant technologies. China, Japan, India, and South Korea continue investing in specialized orthopedic hospitals and localized manufacturing capabilities. More than 25% of newly commissioned orthopedic operating rooms incorporate digital imaging and navigation technologies, improving workflow efficiency and surgical precision. Manufacturers are expanding regional production facilities, strengthening distributor partnerships, and increasing localized research activities to support growing demand while reducing import dependency across high-volume healthcare markets.

China Market Outlook: China is emerging as the region's largest operational market through expanding orthopedic infrastructure, domestic implant manufacturing, and supportive industrial investment. Advanced medical device production capacity continues increasing as manufacturers scale localized facilities and automated production lines. Large hospital networks are rapidly adopting robotic orthopedic systems, while domestic enterprises strengthen competitiveness through product innovation, strategic partnerships, and expanded clinical training programs that improve nationwide deployment efficiency.

Hospital Modernization Improves Orthopedic Access

South America continues strengthening orthopedic services through healthcare infrastructure upgrades, expanding specialist networks, and improved access to advanced implants. Brazil and Argentina account for the majority of regional procedural activity, supported by modernization initiatives across major hospital systems. Approximately 20% of leading orthopedic providers have expanded minimally invasive joint replacement capabilities, improving surgical throughput and patient recovery. International manufacturers continue reinforcing regional distribution partnerships, localized training initiatives, and inventory optimization strategies despite procurement constraints and uneven healthcare investment across several markets.

Brazil Market Outlook: Brazil represents the largest orthopedic market in South America through its extensive hospital network, expanding private healthcare sector, and growing adoption of advanced surgical technologies. Major urban medical centers continue investing in robotic orthopedic platforms and digital imaging systems, while implant suppliers strengthen local distribution partnerships to improve product availability. Increased procedural standardization and surgeon education programs are supporting broader adoption of high-performance orthopedic solutions throughout the country's healthcare system.

Healthcare Investment Expands Advanced Orthopedic Capacity

The Middle East & Africa market is advancing through large-scale healthcare modernization, specialty hospital expansion, and increasing investment in orthopedic excellence centers. Gulf countries continue leading deployment of advanced surgical technologies, while selected African markets improve orthopedic access through infrastructure development. Nearly 18% of newly commissioned specialty hospitals incorporate digital orthopedic operating environments and advanced imaging platforms. Manufacturers are expanding regional partnerships, technical support capabilities, and clinical education initiatives to strengthen deployment quality and long-term operational sustainability across evolving healthcare systems.

Saudi Arabia Market Outlook: Saudi Arabia leads regional transformation through sustained healthcare investment, hospital expansion, and adoption of advanced orthopedic technologies under national healthcare modernization initiatives. High-capacity specialty hospitals continue integrating robotic surgery platforms and digital surgical planning systems into orthopedic departments. International manufacturers are strengthening local partnerships, expanding clinical training programs, and supporting technology transfer initiatives that improve procedural quality while reinforcing the country's position as the region's primary orthopedic innovation and treatment hub.

The Joint Replacement Market is led by Zimmer Biomet, Stryker, DePuy Synthes, Smith+Nephew, and Exactech, with global technology leaders competing against regional implant manufacturers that emphasize cost efficiency and localized distribution. The top five players collectively control approximately 58% of the market, creating a concentrated competitive structure. Competition centers on robotic integration, implant longevity, digital surgical planning, and supply-chain resilience rather than pricing alone. Robotic-assisted platforms improve surgical accuracy by nearly 20%, while localized manufacturing reduces procurement lead times by approximately 18% and automated production lowers quality variation by around 15%. Leading companies are expanding manufacturing capacity, acquiring digital health capabilities, strengthening hospital partnerships, and integrating software with implant portfolios to secure long-term customer relationships. Regional manufacturers compete through value-oriented implants, faster delivery, and customized procurement programs. Rising regulatory requirements and surgeon training investments create significant entry barriers. Winning requires integrated orthopedic ecosystems, resilient manufacturing networks, continuous implant innovation, and measurable clinical outcomes that differentiate products beyond conventional hardware alone.

Zimmer Biomet

Stryker Corporation

DePuy Synthes

Smith+Nephew

Exactech

Corin Group

Enovis Corporation

MicroPort Orthopedics

DJO Global

B. Braun Melsungen AG

LimaCorporate

Aesculap AG

Robotic-assisted joint replacement, AI-enabled surgical planning, and advanced navigation systems define current technology leadership across orthopedic care. More than 35% of leading orthopedic hospitals now utilize digital planning platforms before complex procedures, while robotic workflows improve implant positioning accuracy by approximately 20% and reduce operating room time by nearly 15%. Manufacturers increasingly integrate imaging, navigation, and implant planning into unified surgical ecosystems, strengthening procedural consistency and supporting standardized clinical pathways that improve hospital productivity and long-term implant performance.

Emerging technologies include patient-specific 3D-printed implants, smart orthopedic sensors, advanced porous biomaterials, and cloud-based postoperative monitoring. Compared with conventional implant planning, AI-assisted workflows reduce preoperative planning time by approximately 30% while improving implant fit by nearly 16%. Technology leaders with integrated software and robotic portfolios gain stronger competitive differentiation than manufacturers relying solely on traditional implant products. Hospitals benefit through lower revision rates, optimized inventory planning, and more predictable operating schedules.

Between 2026 and 2028, connected orthopedic ecosystems combining AI analytics, robotic execution, digital rehabilitation, and predictive implant monitoring will become mainstream across high-volume surgical centers. Adoption of digitally integrated orthopedic platforms is expected to exceed 45% among major healthcare networks. Companies investing early in interoperable technologies, cybersecurity, automation, and precision manufacturing will strengthen competitive positioning, accelerate product differentiation, and establish durable operational advantages as orthopedic care shifts toward data-driven clinical decision-making.

March 2026 Stryker introduced new additions to its Triathlon Total Knee System and expanded the Mako SmartRobotics portfolio at AAOS 2026, including Mako Shoulder and Triathlon Gold. The company now supports treatment for more than 150 million patients annually, strengthening its robotics-led orthopedic ecosystem. Source: stryker.com

July 2025 Zimmer Biomet signed a definitive agreement to acquire Monogram Technologies, adding AI-driven semi-autonomous and fully autonomous orthopedic robotics to its portfolio. The transaction valued Monogram at approximately USD 177 million, significantly expanding Zimmer Biomet's robotics and navigation capabilities. Source: zimmerbiomet.com

March 2025 Stryker unveiled the fourth-generation Mako 4 SmartRobotics platform with expanded hip, knee, spine, and shoulder applications during the AAOS Annual Meeting. The platform surpassed 1.5 million Mako procedures across 45 countries, reinforcing leadership in robotic-assisted joint replacement workflows. Source: aaos.org

October 2025 Zimmer Biomet completed its acquisition of Monogram Technologies after Monogram's CT-based AI-navigated knee robotic technology received FDA 510(k) clearance earlier in 2025. The acquisition positions the company to commercialize autonomous orthopedic robotic capabilities beginning in 2027. Source: investor.zimmerbiomet.com

The report provides comprehensive analysis of the Joint Replacement Market across Knee Replacement, Hip Replacement, Shoulder Replacement, Ankle Replacement, and Elbow Replacement, while evaluating demand across Osteoarthritis, Rheumatoid Arthritis, Trauma, Sports Injuries, and Revision Surgery. It assesses deployment trends among Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers, Rehabilitation Centers, and Specialty Clinics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The study also examines robotic surgery, AI-assisted planning, navigation systems, smart implants, and advanced biomaterials influencing clinical and operational performance.

The analysis benchmarks more than 10 major industry participants, highlighting technology adoption, manufacturing strategies, partnership activity, localization initiatives, and competitive positioning. Quantitative assessment of procedure patterns, digital orthopedic adoption, and end-user deployment supports investment prioritization, product expansion planning, supply-chain optimization, and strategic decision-making. The report further identifies emerging niche opportunities, evolving procurement models, and technology integration trends expected to reshape competitive dynamics between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 14300 Million |

Market Revenue in 2033 | USD 20807.8 Million |

CAGR (2026 - 2033) | 4.8% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Zimmer Biomet, Stryker Corporation, DePuy Synthes, Smith+Nephew, Exactech, Corin Group, Enovis Corporation, MicroPort Orthopedics, DJO Global, B. Braun Melsungen AG, LimaCorporate, Aesculap AG |

Customization & Pricing | Available on Request (10% Customization is Free) |